Fourth Quarter 2022 Economic Review and Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits The most common cause of low prices is pessimism – sometimes pervasive, sometimes specific to a company or industry. We want to do business in such an environment, not because we like pessimism but because we like the prices it produces. It’s optimism that is the enemy of the rational buyer.

The most common cause of low prices is pessimism – sometimes pervasive, sometimes specific to a company or industry. We want to do business in such an environment, not because we like pessimism but because we like the prices it produces. It’s optimism that is the enemy of the rational buyer.

– Warren Buffett, 1990 Chairman’s Letter to Shareholders

The economic tea leaves suggest that 2023 could be another challenging year for both stocks and bonds. However, the outlook is more balanced given that equity valuations are much lower and bond yields much higher.

While 2022 was a rough year for investors, there is hope that the Federal Reserve will be able to achieve a “soft landing.” While inflation is still running well above the Federal Reserve’s 2% target, it appears to have peaked and has fallen faster than many expected. In addition, while the real GDP decreased at an annual rate of 1.6% in the first quarter and 0.6% in the second, it recovered in the third, growing 2.9%; and the Fourth Quarter 2022 Survey of Professional Forecasters from the Philadelphia Federal Reserve calls for continued growth in the fourth quarter, though at a lower rate of 1.0%. The labor market also continues to be quite strong, with unemployment ending November at 3.7%.

This was the first year that both the S&P 500 Index and long-term Treasury bonds (20-year maturity) experienced double-digit declines. The closest to that was in 1969 when the S&P 500 lost 8.5% and long-term Treasury bonds lost 5.1%. In addition, global diversification didn’t help, as both the MSCI EAFE and emerging market Indices also experienced double-digit losses, which were fueled by high levels of uncertainty and the U.S. dollar’s appreciation.

The VIX, the market’s measure of volatility and thus uncertainty, spent most of 2022 trading well above the range of 13-19 that is considered average. In fact, there were nine episodes when the VIX breached 30 – reaching a peak of 37.5 on March 8th. VIX levels above 20 are not only considered high, but they have been found to be predictive of high volatility over the next month. Because investors and thus markets dislike uncertainty, volatility has been negatively correlated with equity returns – when the risk of negative outcomes increases, investors demand larger risk premiums, driving P/E ratios down.

Here are 14 risks that investors should be aware of that explain the continued high level of uncertainty.

Risks to economic growth

A slew of factors point to the risk of slower economic growth and the increasing risk of recession:

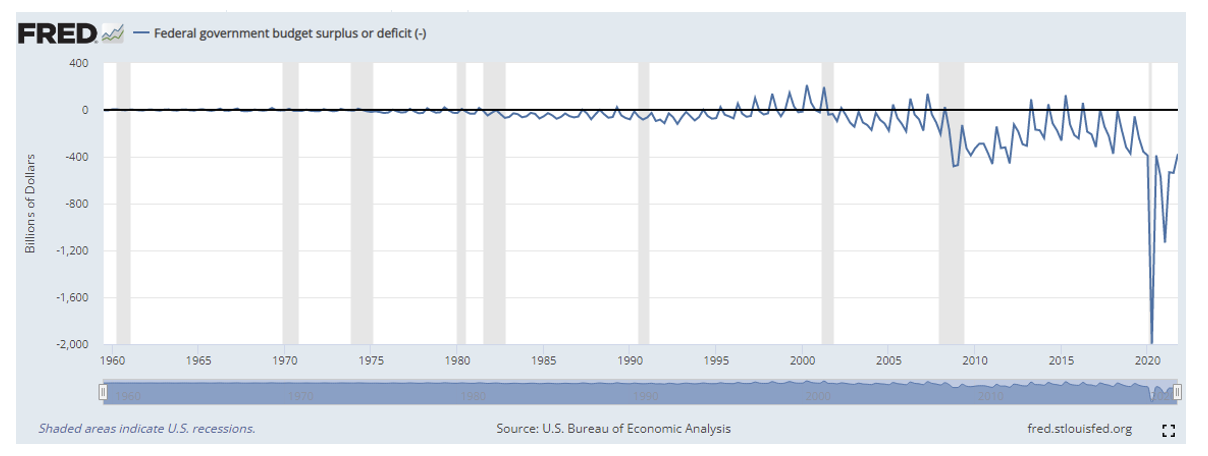

- Reduced fiscal stimulus. As seen in the chart below from the Federal Reserve, while the budget deficit is still large, the economy is receiving less fiscal stimulus, the result of a shrinking fiscal deficit. In fiscal year 2022, total government spending was $6.3 trillion and total revenue was $4.9 trillion, resulting in a deficit of $1.4 trillion, a decrease of $1.4 trillion from the previous fiscal year. The shrinking deficit was a result of both reduced pandemic-related spending and increased tax revenue as the economy recovered.

With the Republicans winning control of the House, it is unlikely we will see increased fiscal stimulus.

- Tighter monetary policy. In September the Federal Reserve began a program of quantitative tightening, shrinking its roughly $9 trillion balance sheet by almost $100 billion a month. As the Fed’s purchases of bonds during its period of quantitative easing helped drive bond yields lower, its reduction in holdings of bonds could cause yields to go higher. In addition, reductions in its holdings could also tighten liquidity conditions, which could cause credit spreads to widen. A 2022 study by Fed economist Bill Wei concluded that a $2.2 trillion passive roll-off of nominal Treasury securities from the Federal Reserve’s balance sheet over three years is equivalent to an increase of 29 basis points in the current federal funds rate at normal times but 74 basis points during crisis periods.

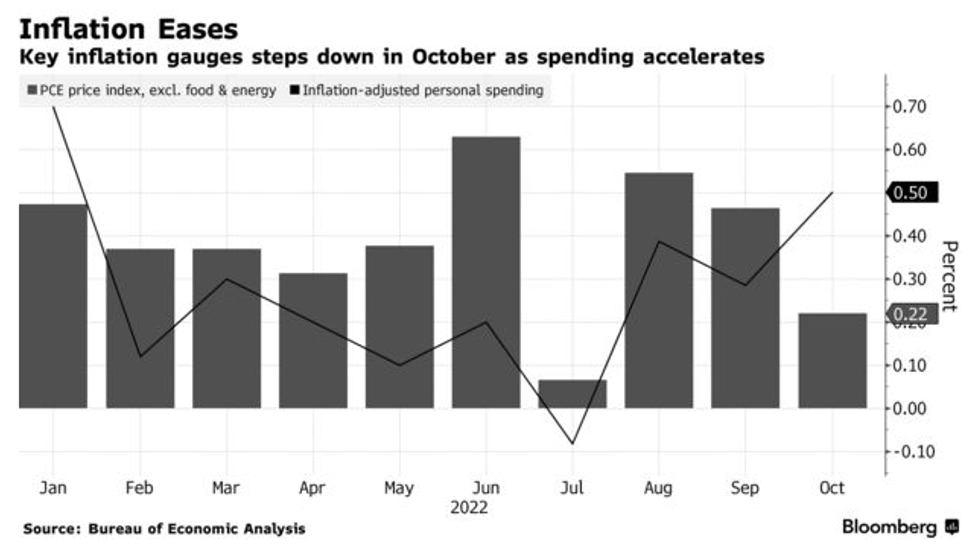

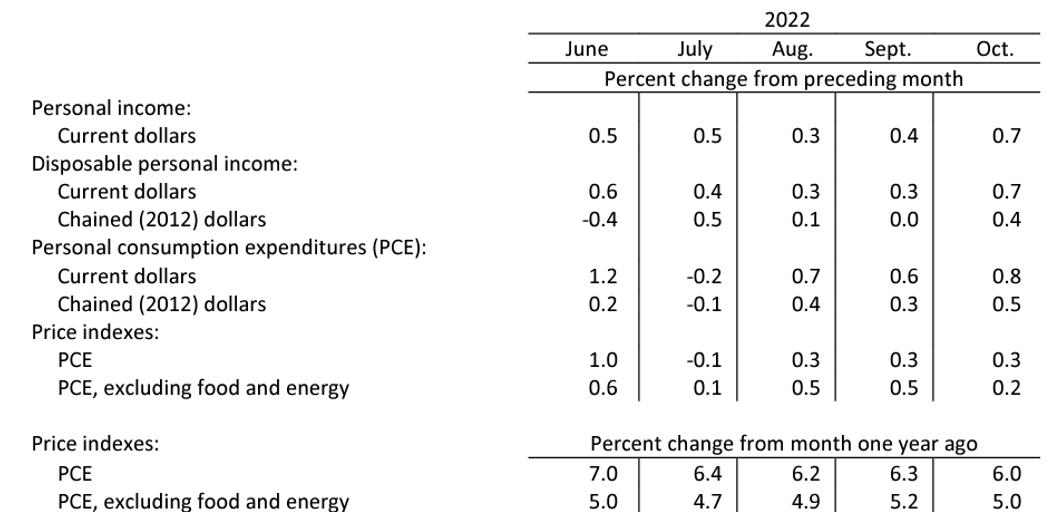

It seems likely (though far from certain) that the Federal Reserve will continue to raise the Fed funds rate to at least 5% because, while core inflation has peaked and begun to fall, it is well above the Fed’s 2% target. While the Fed’s preferred inflation measure, the core personal consumption expenditures (PCE) price index excluding food and energy rose just 0.2% in October from a month earlier. The gauge was still up 5% year-over-year, though that was a step down from September’s upwardly revised 5.2% gain. The overall PCE price index increased 0.3% for a third month but was still up 6% from a year ago. The Fed is not likely to stop raising rates until the Fed funds rate is above the core inflation rate.

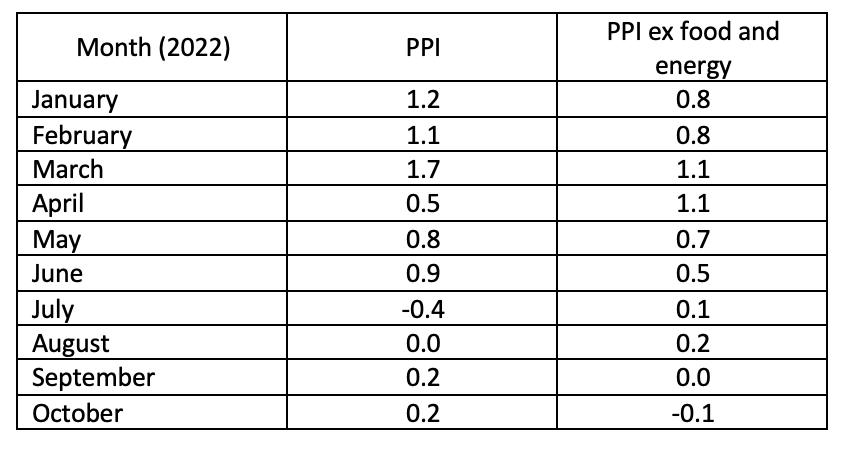

Another indicator, the producer price index (PPI), also shows that inflation is slowing. The PPI (core PPI), after averaging an increase of 1% (0.8%) over the first six months of the year, increased an average of just 0% (0.05%) over the four months ending in October.

The market received more good news with the release of the November CPI on December 13, as inflation came in lower than the market was expecting. The Consumer Price Index for all urban consumers (CPI-U) rose just 0.1% in November on a seasonally adjusted basis after increasing 0.4% in October, and the index for all items less food and energy (the core index) rose 0.2% in November after rising 0.3% in October. The year-over-year non-seasonally adjusted headline CPI came in at 7.1%, down from 7.8% the previous month. Year-over-year core CPI (ex food and energy) came in at 6.0%, down from 6.3% the previous month.

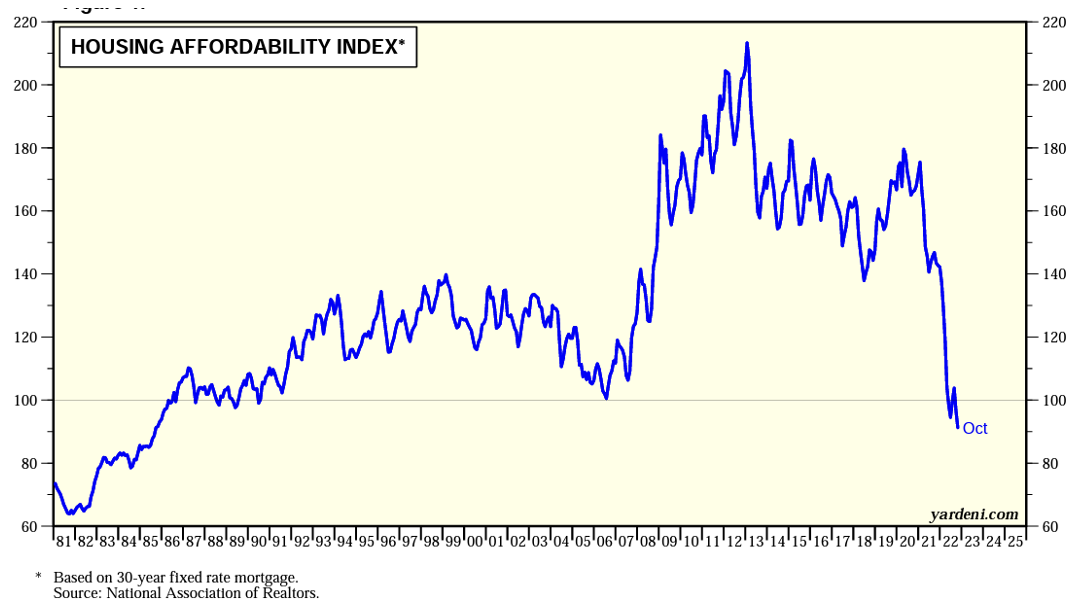

- The housing market has been hit hard by the dramatic rise in mortgage rates. Housing plays an important role in the economy, with a combined contribution to GDP generally averaging 15-18%. Residential investment (which includes construction of new single-family and multifamily structures, residential remodeling, production of manufactured homes and brokers’ fees, averaging 3-5% of GDP) and consumption of housing services (which includes gross rents and utilities paid by renters as well as owners’ imputed rents and utility payments, averaging 12-13% of GDP). October marked the ninth consecutive month of declining home sales, and while the median existing-home sales price was $379,100 in October, up 6.6% from a year ago, it was down 8.4% from the record high of $413,800 in June. As seen in the chart below, the impact of dramatically higher mortgage rates and rising home prices over the past few years has caused the housing affordability index to reach its lowest level in more than 30 years. Thus, housing is likely to be a continued drag on economic growth.

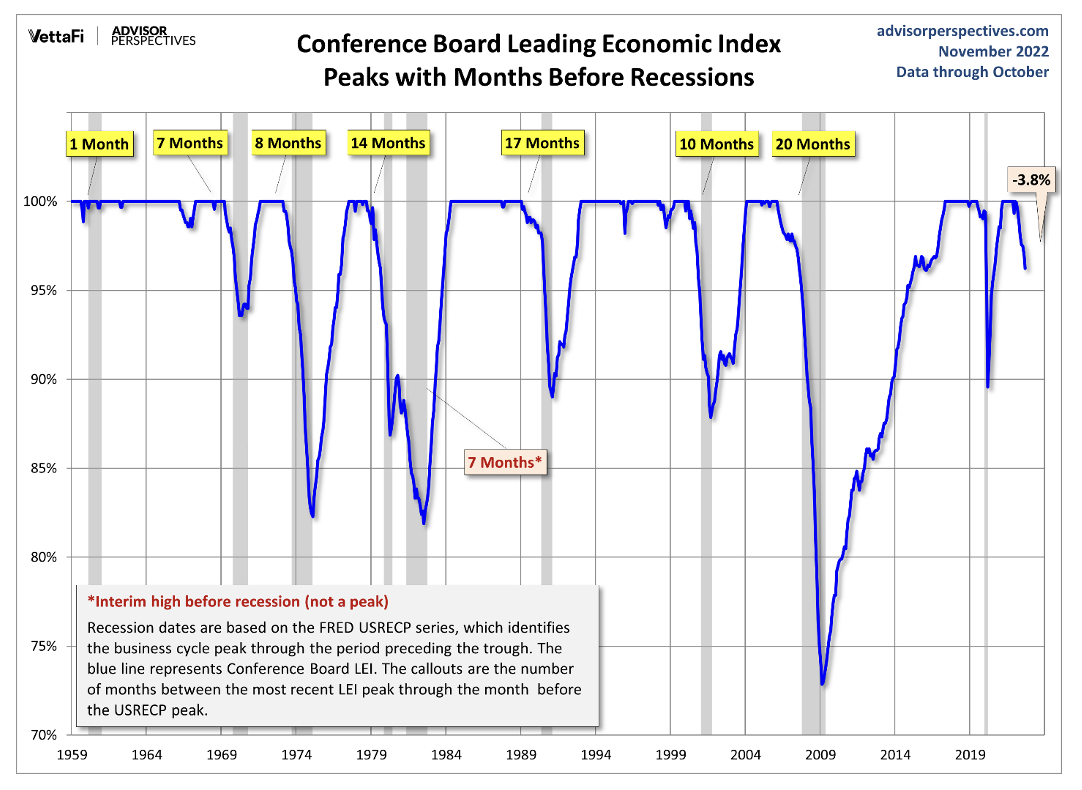

- The Conference Board’s October index of leading indicators fell for the eighth straight month, indicating an increasing risk of recession. The Leading Economic Index (LEI) fell 3.2% over the six-month period between April and October 2022, a reversal from its 0.5% growth over the previous six months. Over the past seven recessions dating back to 1959, the average time from the peak in the LEI to a recession was 11 months, with a range of just one month to as long as 20 months.

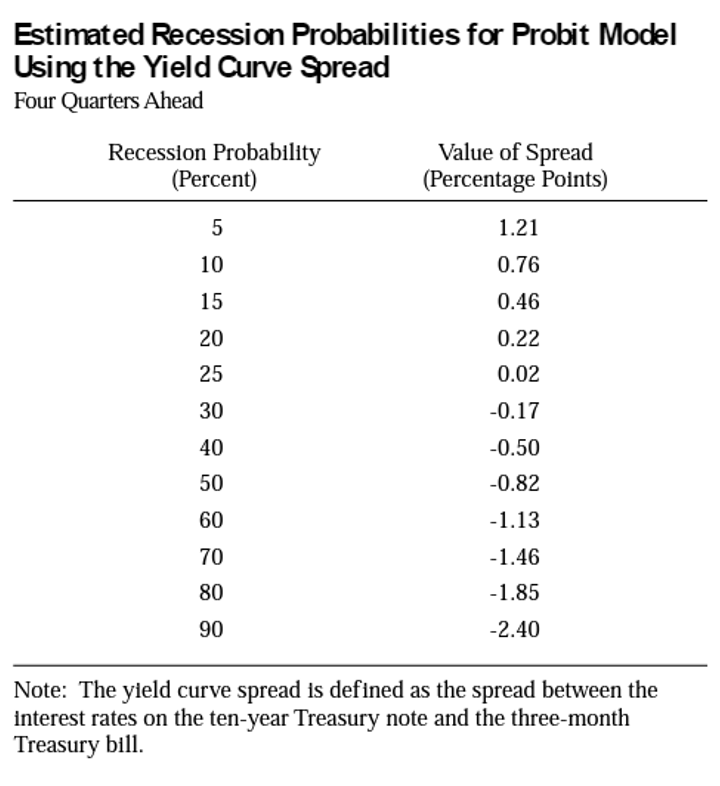

- The yield curve has remained inverted at historically high levels. The authors of the Federal Reserve of New York’s study, “The Yield Curve as a Predictor of U.S. Recessions,” concluded: “The yield curve – specifically, the spread between the interest rates on the ten-year Treasury note and the three-month Treasury bill – is a valuable forecasting tool. It is simple to use and significantly outperforms other financial and macroeconomic indicators in predicting recessions two to six quarters ahead.” The reason for the relationship is that monetary policy has a significant influence on the yield curve spread and hence on real activity over the next several quarters. A rise in the short rate tends to flatten the yield curve as well as slow real growth in the near term, and expectations of future inflation and real interest rates contained in the yield curve spread play an important role in the prediction of economic activity. The following chart shows their findings of the probability of a recession depending on the slope of the yield curve. As of December 12, 2022, the spread between the three-month and 10-year Treasury was -0.77%, indicating an estimated odds of recession of about 50%.

- Impact of a strong dollar. The much stronger fiscal response to the COVID crisis by the U.S. resulted in our economy recovering faster than the rest of the world and our interest rates rising faster as well. That led to a dramatically stronger dollar. From September 2021 through mid-September 2022, the dollar (based on the DXY index) rose from about 92 to about 112, a two-decade high and an increase of 22%. While a stronger dollar helps hold inflation down, it puts pressure on exports and increases our imports, increasing our trade deficit and negatively impacting economic growth as well as corporate profits (a strong dollar negatively impacts the foreign earnings of U.S. multinationals). That could lead to reduced earnings forecasts and lower P/E multiples. From that perspective, the good news is that the better recent inflation numbers have provided hope that the Fed can end its tight monetary policy sooner. That, combined with the weaker U.S. leading economic indicator and foreign central banks tightening monetary policies, led to the dollar reversing ground, falling back to under 105 by December 15.

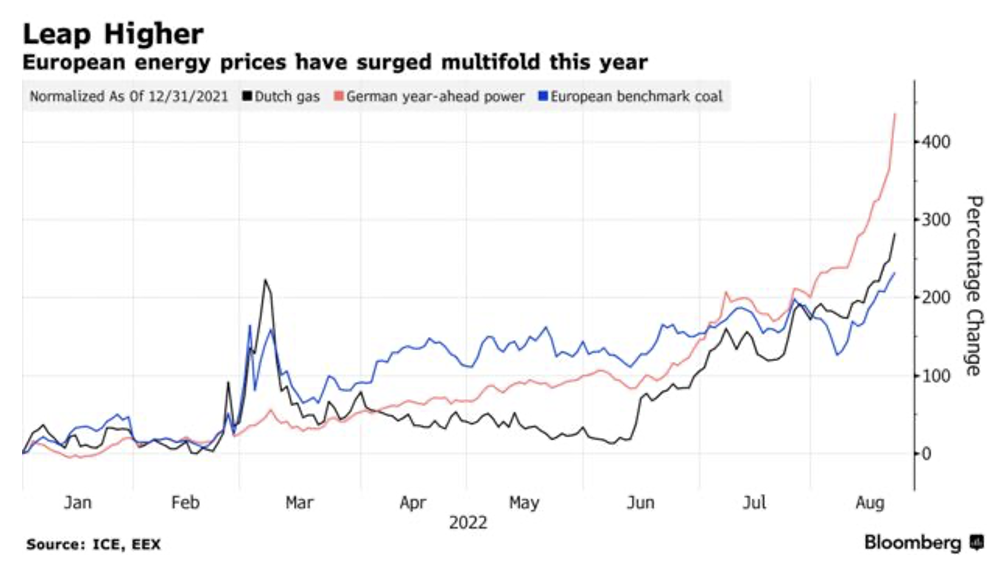

- The war in Ukraine led to a dramatic increase in gas prices, pushing Europe into a recession, with Germany (the largest European economy) particularly vulnerable.

If there is any good news from that, it is that the war in Ukraine, combined with the slowdown in China’s economy related to its housing crisis and the negative impacts of COVID-related shutdowns (the IMF, for example, now forecasts growth in China’s economy, the second largest, to slow to 3.2% in 2022, the slowest in 40 years), have slowed global growth and thus slowed the demand for all commodities, including energy-related ones. For example, after peaking at about $117 a barrel in May 2022, West Texas Crude Oil had fallen back to about $76 by December 13. That’s helpful in the fight against inflation and reduces the risk of a recession as higher energy prices act as a tax on consumers.

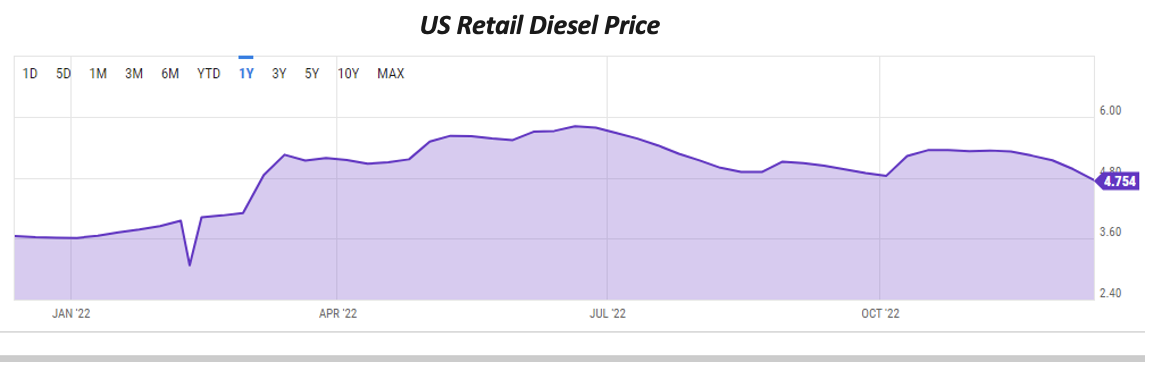

While energy prices have come down, the U.S. does face a significant problem in the shortage of diesel fuel. No fuel is more essential to the global economy than diesel. It powers trucks, buses, ships and trains. It drives machinery for construction, manufacturing and farming. It’s burned for heating homes. And with the high price of natural gas, in some places diesel is being used to generate power. Diesel in the spot market of New York harbor, a key benchmark, reached a peak of about $5.80 a gallon but had fallen to $4.74 a gallon by December 13. That is still about 30% above year-ago levels.

What’s Causing the Diesel Shortage? There are major constraints globally on refining capacity. Supplies of crude oil are already fairly tight. But the bottleneck is more acute when it comes to turning that raw commodity into fuels like diesel and gasoline. That’s partly a function of the pandemic, after lockdowns destroyed demand and forced refiners to close some of their least profitable plants. But the looming transition away from fossil fuels has also dented investments in the sector. Since 2020, U.S. refining capacity has shrunk by more than 1 million barrels per day.

- Tight labor markets. The U.S. labor market is about the tightest it has ever been, with 1.8 jobs posted for every unemployed person (10.7 million job openings at the end of October versus unemployed of 6.0 million). November’s unemployment rate was 3.7%, remaining in a range of 3.5-3.7% since March. There are now severe shortages in many occupations, such as pilots, nurses and teachers. As one example, Delta Air Lines and its pilots’ union reached agreement for raises topping 30% over four years. Exacerbating the problem of a tight labor market is that the COVID crisis led to the early retirement of many workers. The move to onshore jobs (to reduce the risks of global supply chains) will further tighten the labor market. Tight labor markets, while good for wages and the economy (as consumer spending accounts for about two-thirds of GDP), has the reverse effect on corporate profits. Thus, we could see a margin squeeze as the negotiating power shifts from employer to employee. In addition, tight labor markets mean that wage growth is likely to continue to be stronger than the Fed would like to see, and that inflation may be harder to bring down to the target. That means the Fed might have to keep rates higher for longer than the market is currently forecasting – a negative for both the stock and bond markets.

- Declining labor productivity. The U.S. Bureau of Labor Statistics third quarter report showed that nonfarm business sector labor productivity decreased 1.4%, reflecting a 1.9% increase in output and a 3.4% increase in hours worked. The 1.4% four-quarter decline is the first instance of three consecutive declines in this measure since 1982. In the first quarter of 2022, productivity experienced the worst quarterly decline since 1947, -7.4%. The second quarter’s decline was almost as bad, -4.1%. The third quarter was better, showing a slight increase of 0.3%. Over the last year, unit labor costs increased 6.1%. Tight labor markets are likely to keep upward pressure on wages.

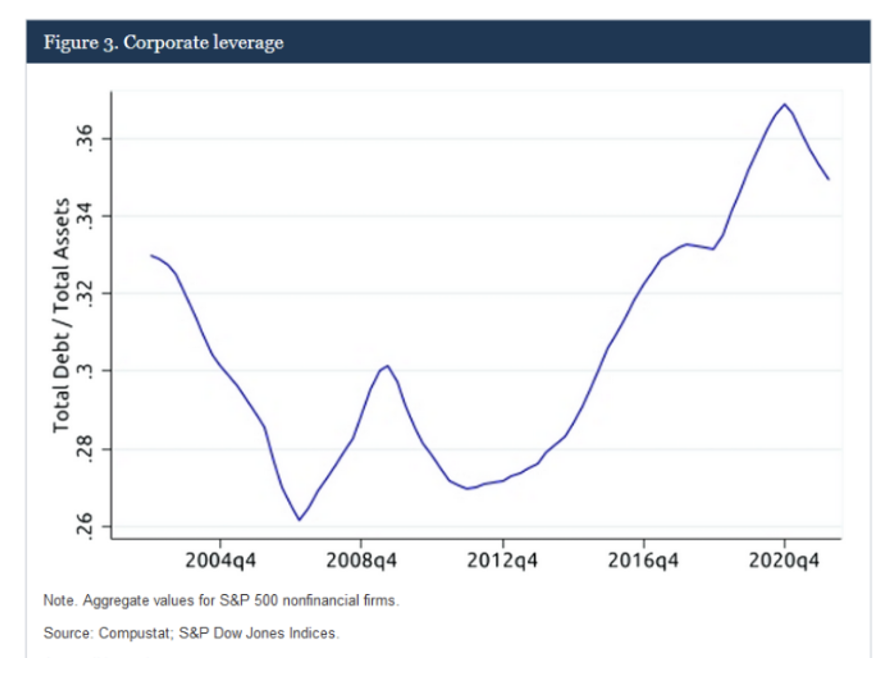

- Rising interest rates negatively impact corporate profits. Rising interest rates increase the cost of debt. The chart below demonstrates the positive impact on corporate profits of the four-decade long secular decline in interest rates. The dramatic rise in rates since the Fed began tightening policy will have the opposite effect.

The negative impact on corporate earnings will be compounded by the fact that corporations have increased their use of leverage (taking advantage of historically low rates), as seen in the following chart:

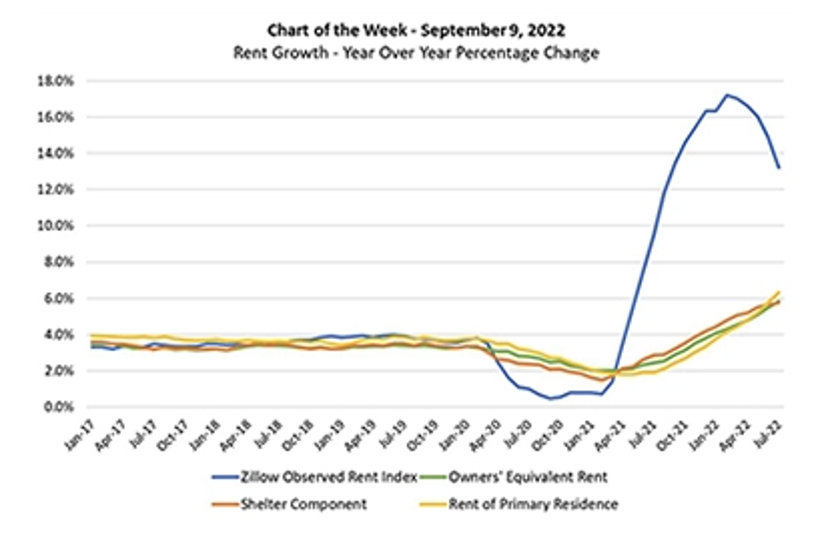

- The U.S. has a massive housing shortage. While rising interest rates will slow demand for housing, the U.S. faces a shortage of about 4 million homes. After the Great Recession, new home construction slowed dramatically, with fewer new homes being built in the 10 years ended 2018 than in any decade since the 1960s. That helps explain why home prices were rising at dramatic rates (through mid-year 2022, the year-over-year increase in home prices was 18%) until the recent dramatic runup in mortgage rates. The shortage, and regulations that helped create the shortage (the NIMBY, or “not in my backyard,” problem), is why rents have been rising so dramatically. Rising mortgage rates have slowed new construction, which will only exacerbate the problem. That is one inflation problem the Fed cannot solve via monetary policy alone – it’s a supply problem, not a demand problem. The result is that it seems likely that, in the absence of a serious recession, rents as reported in the CPI will likely continue to rise. Also, there is a significant lag in reporting because of the way the CPI is calculated (causing rents to lag the CPI by about 12-18 months).

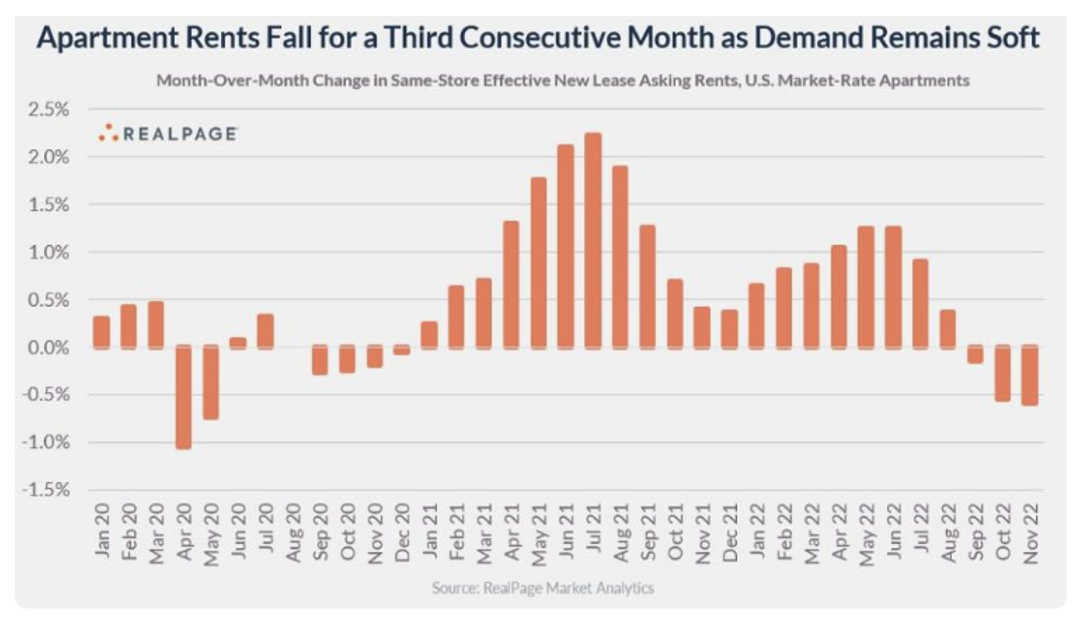

As the above chart makes clear, future increases in the rental component of the CPI are virtually guaranteed over the next year, though likely at a slower pace than in 2022. That will keep upward pressure on the core CPI. On the good news front, apartment rents across the U.S. dropped in November by the most in at least five years, a sign that a key cost tracked by the Federal Reserve could be easing up. A national index of rents fell by 1%. As seen in the chart below, it was the third straight month-over-month decline.

Similarly, a shortage of personnel will likely continue to drive medical costs up faster (rising rates don’t slow demand for health care). And medical costs are another key component of the core CPI.

- The COVID crisis led to massive fiscal stimulus. That produced a huge budget deficit that pushed our debt-to-GDP ratio to well above 100%, a level at which the empirical evidence demonstrates has had a negative impact on economic growth. The recently enacted Inflation Reduction Act will increase the deficit, as would the proposal to eliminate significant amounts of student debt. And the rise in interest rates already experienced exacerbates the problem, as each 1.0% increase in interest rates leads to an increase of about $250 billion in interest costs and the budget deficit.

- Debt ceiling. The debt ceiling must be raised by the end of September 2023. If it is not, there exists the possibility that the U.S. could default on its debt. And that could cause a financial crisis whose outcome no one can predict. It seems unlikely that a compromise will not be reached, although history suggests it will come at the last minute, as it did in 2011. Investors should never treat the unlikely as impossible.

- The wealth effect. Trillions of dollars have been lost in the cryptocurrency crash and stock and bond bear markets. That could put a damper on consumer spending.

The 14 risks that concern investors and markets are offset by some better news.

On the brighter side

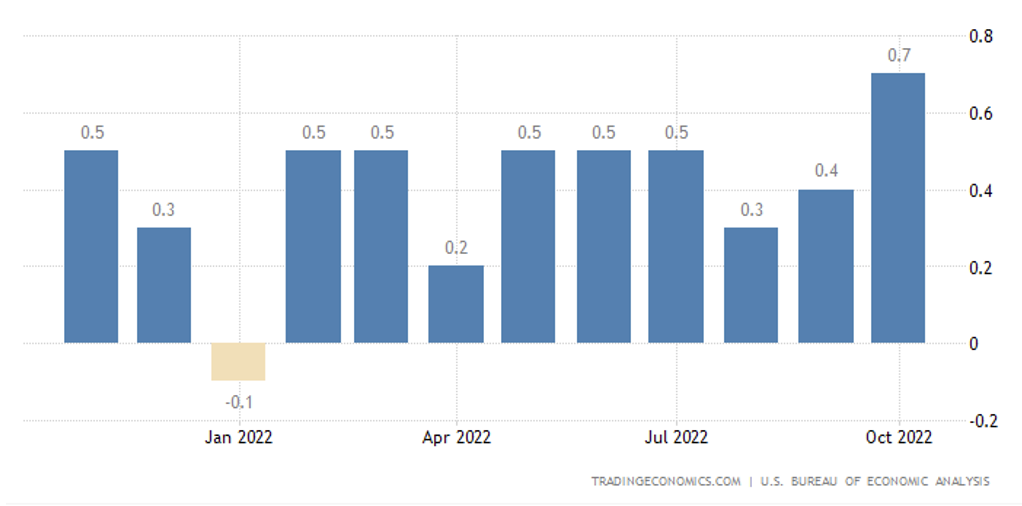

- The job market has remained quite strong despite two negative quarters of GDP growth (second and third quarters). Total nonfarm payroll employment increased by 263,000 in November, and the unemployment rate was unchanged at 3.7%. Over the first 11 months of 2022, monthly job growth averaged 392,000. Reflecting a strong labor market, November personal income increased 0.7%, the strongest reading since October of 2021, primarily reflecting increases in compensation and government social benefits. Average hourly earnings grew 5.1% from a year earlier, well above the pre-pandemic pace of about 3%.

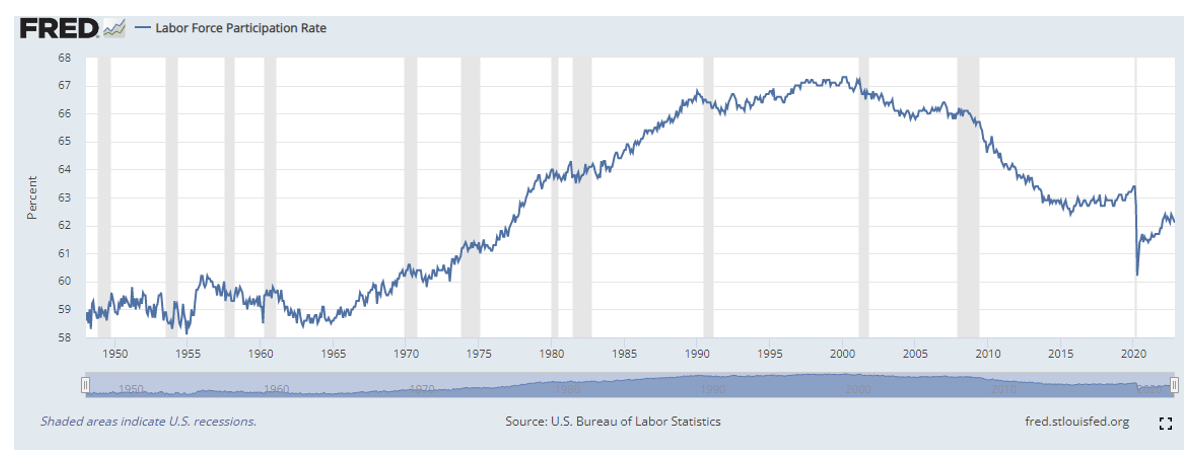

One reason employers might continue to raise wages briskly is that the labor participation rate remains below pre-pandemic levels, falling to 62.1 in October.

- Low unemployment and wage gains are helping fuel consumer spending. Personal income increased $155.3 billion (0.7%) in October; disposable personal income (DPI) increased $132.9 billion (0.7%); and personal consumption expenditures (PCE) increased $147.9 billion (0.8%).

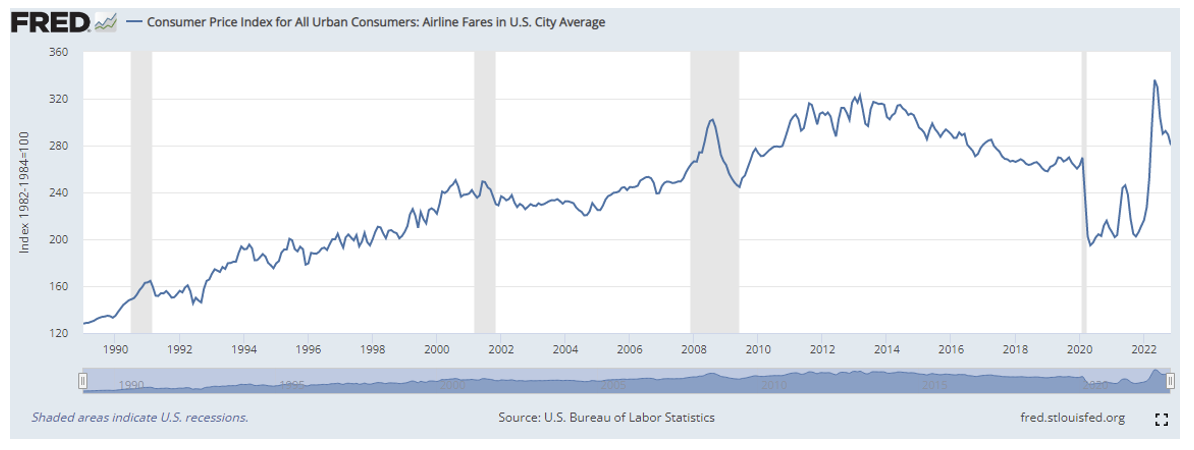

- Despite the ongoing war in Ukraine, the price of oil has fallen significantly, from above $120 a barrel earlier in the year to about $76, leading to lower prices at the pump. After peaking at over $5 dollar a gallon in June, the average national price fell to $3.25 by December 13. And, as can be seen in the following chart, airfares have fallen as well.

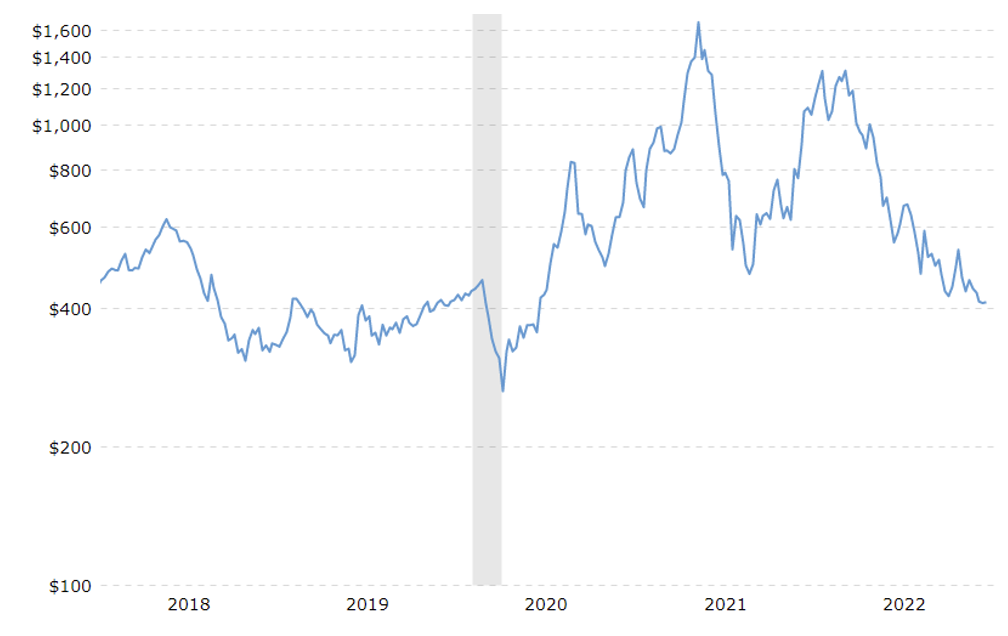

The chart below shows that thanks to the slowdown in housing, lumber prices have fallen about 75% from their peak in May 2021 (about $1,670) to about $412 per thousand board feet (about their pre-COVID levels).

In addition, the successful negotiations allowing the export of Ukrainian food supplies have slowed the increase in food prices.

- The global slowdown has reduced the need to rebuild inventories, reducing supply chain pressures, which should reduce inflation related to goods. In addition, container shipping costs have begun to fall sharply. As shown in the chart below, on December 15 the Baltic Dry Index, which measures the cost of shipping goods worldwide, had fallen to 1,401 from its peak of about 5,500 more than a year earlier, a drop of about 75% and back to about pre-COVID levels. That too should help bring goods inflation down.

- While the Fed has been raising rates, monetary policy is not yet very restrictive, as there are still negative real rates of interest on nominal bonds – rates are below both the annual rate of increase in the CPI and the core CPI. There is also some fiscal stimulus (just not as much as in 2020 and 2021), and both corporate and consumer balance sheets remain quite strong – not only have corporate profits been high, but corporations took advantage of historically low rates to refinance debt and lengthen maturities. And bank balance sheets are strong. Thus, systemic risks to the financial system are not there like they were in 2007. And there is no housing bubble to worry about.

- Perhaps most importantly, valuations are much lower, reflecting the heightened economic and geopolitical risks. For example, the Shiller CAPE 10 ended 2021 at 38.3 and was down to about 29 by December 12. Using current earnings, Morningstar shows the S&P 500 Index trading at a multiple of about 17, about its long-term historical average. And value stocks were trading as if we were already in a serious recession. As live examples, Avantis’ U.S. Small-Cap Value ETF (AVUV) was trading at only about eight times earnings, its International Small-Cap Value ETF (AVDV) was trading at a multiple of about 7, as was its Emerging Markets Value ETF (AVES). As good a predictor as we have of future real returns is the earnings yield (E/P). Remember that it doesn’t matter to markets whether the news is good or bad, only whether it is better or worse than expected. At least for value stocks, the markets seem to be expecting almost the worst possible outcomes, as valuations are near levels reached at the depth of the Great Recession.

- Following public protests of stringent COVID restrictions, China has begun to pare back control measures (such as scrapping a range of testing requirements), providing hope that it will open up its economy, the second largest in the world. That would improve growth prospects around the globe, particularly for Asian and emerging market countries. However, an improving Chinese economy would increase demand for energy and other commodities, making it more difficult for the Federal Reserve to achieve its inflation objective.

- The tight labor markets could make corporations reluctant to reduce their workforce if demand were to slow. While hurting corporate profits, that would reduce the risks of a recession.

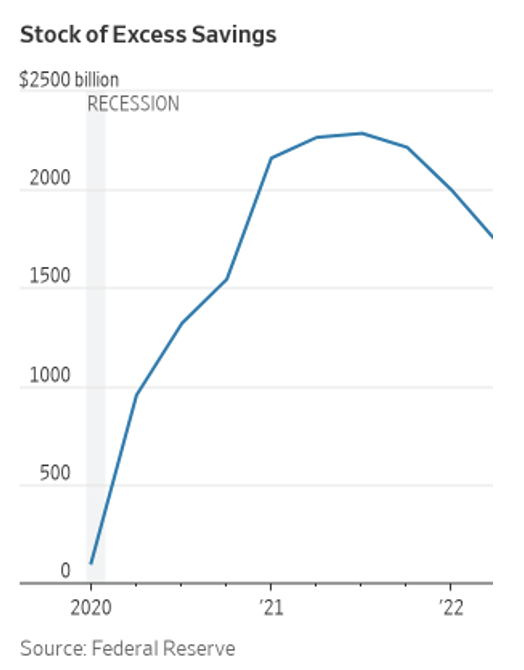

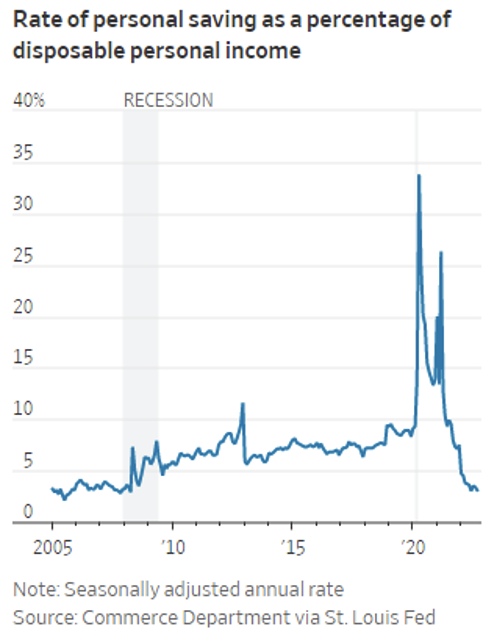

- Consumers still have a savings buffer provided by COVID relief spending. Consumers built up unprecedented savings buffers during the COVID-19 pandemic, thanks to government stimulus and fewer opportunities to spend. The extra cash helped households pay down debt, buy goods like new appliances and furniture during lockdowns, and take vacations once restrictions lifted. It gave businesses leeway to raise prices and hire more workers to meet stronger demand. Economists estimated that headed into the third quarter of this year, households still had about $1.2 trillion to $1.8 trillion in “excess savings” – the amount above what they would have saved had there been no pandemic. That buffer has helped consumers maintain spending in the face of rising inflation and rising mortgage rates.

U.S. retail sales posted their strongest gain in eight months in October. However, in 2021 the saving rate moderated to 11.8%, and it has fallen further during 2022. The rate has been below 4% for eight straight months and fell to just 2.3% in October, the lowest since 2005. This suggests that consumers are spending more and saving less of their monthly income than normal because inflation forces them to spend more on higher-priced goods and services.

Goldman Sachs economists estimated households have drawn down about 25% of excess savings and will have spent about 60% by the end of 2023: “The growth boost from strong balance sheets is probably mostly behind us but … elevated wealth levels will provide a backstop to spending for households that are hit with a negative economic shock.”

Outlook for the U.S. economy

All the above is well known by the market. Those factors are why stocks and bonds both performed poorly in 2022, and why valuations are lower and bond yields higher. However, they don’t tell us much about the future other than that there are heightened risks, and the dispersion of possible outcomes has widened. So, what do economists forecast for the U.S. economy?

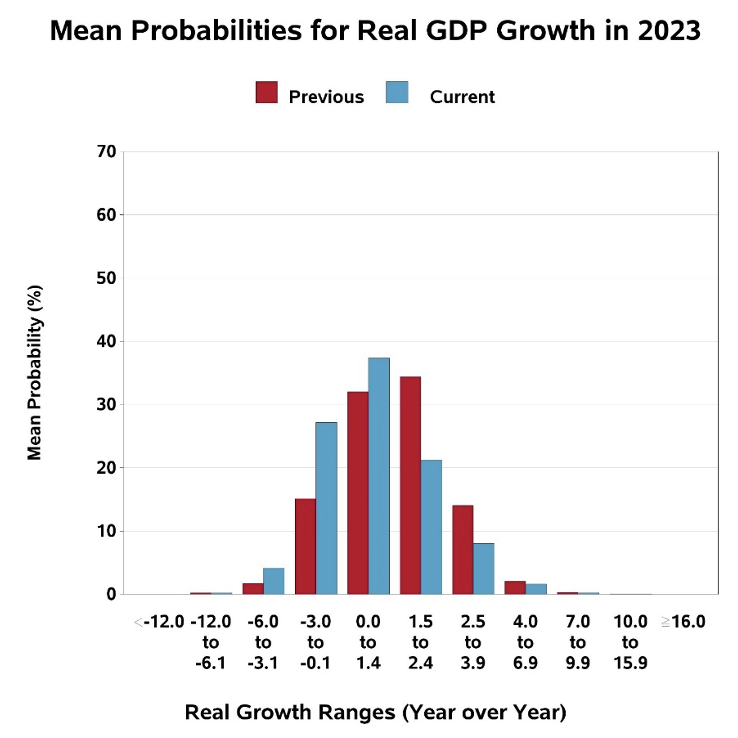

The Philly Fed’s Fourth Quarter 2022 Survey of Professional Forecasters, released in November, does not predict a recession (though with little margin for error) – calling for slow growth of just 0.2% in each of the first two quarters, followed by growth of 0.9% in the third quarter and 2.1% in the fourth quarter, putting year-over-year growth at 0.7%. The following chart shows the mean probabilities of real GDP growth in 2023. The consensus is that the risk of recession in 2023 has increased.

As the chart implies, the future unknowable. Thus, investors should treat the mean forecast of 0.7% growth in 2023 in a probabilistic, not deterministic, way.

The consensus forecast also calls for moderating inflation, though not sufficient to reach the Fed’s objective of 2%. The forecast for the CPI in 2023 increased slightly from the prior quarter’s forecast of 3.2%, to 3.4%. However, the forecast does call for inflation to fall from a fourth quarter 2022 forecast of 4.6%, to 3.7%, 3.2% and 2.8% over the following three quarters. Such a trend would likely cause the Fed to pause hiking rates, as the Fed funds rate would then be well above the CPI. However, that doesn’t mean they would pivot to cutting rates, as inflation would still be running hotter than its 2% target.

Uncertainty of forecasts: What could go wrong?

Smart investors know that investing is about managing risks, not returns, and that bear markets are a necessary evil (without them, there would be no risk and no equity risk premium). They accept that uncertainty of economic and geopolitical risks is the norm. And the evidence on the ability of active managers to outperform based on their forecasts is overwhelmingly against the strategy. That is why, for example, Warren Buffett ignores economic forecasts.

Instead of trying to manage returns, smart investors identify risks of concern and design portfolios that allow them to achieve their financial and life goals with the least amount of exposure to those risks. With that concept in mind, we will review some of risks we can identify (what could go wrong) and consider how they can be addressed, reducing them to an acceptable level.

- There are several forces at work that could lead to it being difficult to bring inflation to the Fed’s target. The tight labor market could keep wage demands at elevated levels, causing the Fed to keep rates higher for longer. While slower economic growth has resulted in goods price inflation coming down sharply, the tight labor market could keep the prices of services rising at faster rates, and services constitute about three quarters of the GDP. The labor shortage could be exacerbated by the trend toward deglobalization. Just as globalization helped hold inflation down, bringing jobs onshore, deglobalization, while helping the domestic economy, will put more pressure on wages and certainly will cause inflation to be higher than it would be otherwise (and be a negative for corporate profits as well). Third, the shortage of housing could keep rents increasing at a relative fast pace. Finally, a faster than expected reopening in China could put upward pressure on energy prices.

- The war in Ukraine drags on for a long period. Russia is the main supplier of gas to several European countries, creating greater risks for Germany and Italy in particular. Plans for rationing across Europe are already in place. If Russia completely cuts off gas shipments to Europe, that could have a significant negative impact on their economies, likely producing a deeper recession that would negatively impact global growth. There is also the risk of a nuclear incident due to Russia’s war with Ukraine.

- Government policies to discourage carbon-related energy production and distilling capacity, combined with the need to transition to greener forms of energy, have negatively impacted supplies, increasing inflationary pressures that could be long-lasting.

- The housing component of the CPI represents about one-third of the CPI and about 40% of the closely watched core CPI, and it has a significant lag because of the way it is calculated. Supply is limited and labor markets are strong. That could keep upward pressure on rents and the CPI.

- As to interest rate risks, the historical evidence is a guide to possible outcomes. Let’s assume you are an optimist and believe the Fed will achieve its goal of 2% inflation in the relatively near term. If the roughly 0.5% historical real return on T-bills and the historical term premium of 2% are added to that, it results in a 10-year Treasury yield of 4.5%, a level that would likely not be good for either stocks or bonds, as it is much higher than the market currently expects. And if you are a pessimist on the outlook for inflation, the yield could end up much higher.

- China could decide to go back to more restrictive COVID policies, slowing global economic growth, or it could take action against Taiwan.

- A colder than normal winter could create shortages of energy supplies around the globe. And a climate event, such as a major hurricane, could disrupt U.S. energy supplies. Such an event could create price spikes, as the Northeast has critically low supplies, down more than 60% from their five-year average. And there is always the risk of an unexpected “black swan” event (such as the COVID crisis).

- The Fed’s program of quantitative tightening (reducing the size of its balance sheet) has already reduced liquidity in the capital markets, creating risks that are difficult to foresee. The combination of the reduction in liquidity, the rise in interest rates and the strength of the dollar could lead to unforeseen consequences around the globe, putting pressure on emerging markets and high-yield debt markets and creating the risk of contagion. This risk should not be underestimated.

What should investors do?

Be prepared for more volatility, not only because of the potential risks, but also because the dramatic increase in the market share of passive investing has negatively impacted liquidity. And because of the regulatory changes made after the Great Recession (the Volcker rule), banks can no longer hold significant trading assets on their balance sheets. The result is that banks no longer act as significant providers of liquidity, which has led to increased bid-offer spreads and increased volatility.

Evidence of the reduction in liquidity was presented by Xavier Gabaix and Ralph Koijen in their March 2022 study, “In Search of the Origins of Financial Fluctuations: The Inelastic Markets Hypothesis.” They found that today, “Investing $1 in the stock market increases the market’s aggregate value by about $5.”

There are two ways to address the risks we have discussed. The first is to reduce exposure to both stocks and longer-term bonds and bonds with significant credit risk while increasing your exposure to shorter-term, relatively safe credit risks. By raising interest rates dramatically, the Fed has made that alternative more attractive than it has been in years. For example, for those concerned about inflation, the yield on five-year TIPS has increased from about -1.6% at the start of the year to 1.3% on December 13. And all shorter-term yields are significantly higher than they were a year ago.

Another way to address the risks is to diversify your exposure to risk assets to include other sources of risk that have low to no correlation with the economic cycle risk of stocks and/or the inflation risk of traditional bonds. The following are alternative assets that may provide diversification. Alternative funds carry their own risks; therefore, speak to your financial professional about your own circumstances prior to making any adjustments to your portfolio.

- Reinsurance. The asset class looks attractive, as losses in recent years have led to dramatic increases in premiums, and terms (such as deductibles) have become more favorable.

- Private middle market lending (specifically, senior, secured, sponsored corporate debt). This asset class also looks attractive, as base lending rates have risen sharply, credit spreads have widened, lender terms have been enhanced (upfront fees have gone up) and credit standards have tightened (stronger covenants).

- Consumer credit.

- Long-short factor funds.

- Commodities.

- Trend following (time-series momentum).

As Kevin Grogan and I demonstrated in our book, Reducing the Risk of Black Swans, adding unique risks has historically reduced the downside tail risk associated with conventional stock and bond portfolios. In general, while both traditional stock and bond portfolios produced large losses in 2022, those six asset categories provided positive returns.

The historical evidence is very clear that dramatic falls in prices lead to panicked selling as investors eventually reach their “Get me out!” (GMO) point. Investors have demonstrated the unfortunate tendency to sell well after market declines have occurred and buy well after rallies have begun. The result is that they dramatically underperform the very mutual funds in which they invest. That is why it is so important to understand that equity investing is always about uncertainty and why it is important to not choose an equity allocation that exceeds your risk tolerance. Avoiding those mistakes provide investors the greatest chance of making investment decisions with their heads, not their stomachs, which rarely make good decisions.

Larry Swedroe is the head of financial and economic research for Buckingham Wealth Partners.

For informational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed adequacy of this article. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Information from sources deemed reliable, but its accuracy cannot be guaranteed. Performance is historical and does not guarantee future results. All investments involve risk, including loss of principal. Mentions of specific securities are for informational purposes only and should not be construed as a recommendation of specific securities. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed here are their own and may not accurately reflect those of Buckingham Strategic Wealth® and its affliates. LSR-22-420.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All