Monetary and fiscal indicators continued to tighten significantly in the second quarter pointing towards a material slowdown in the U.S. economy.

Yields on 10-year Treasuries may fall as much as 150 basis points before the end of next year as the Federal Reserve cuts interest rates to bolster a slowing US economy, according to Jupiter Asset Management.

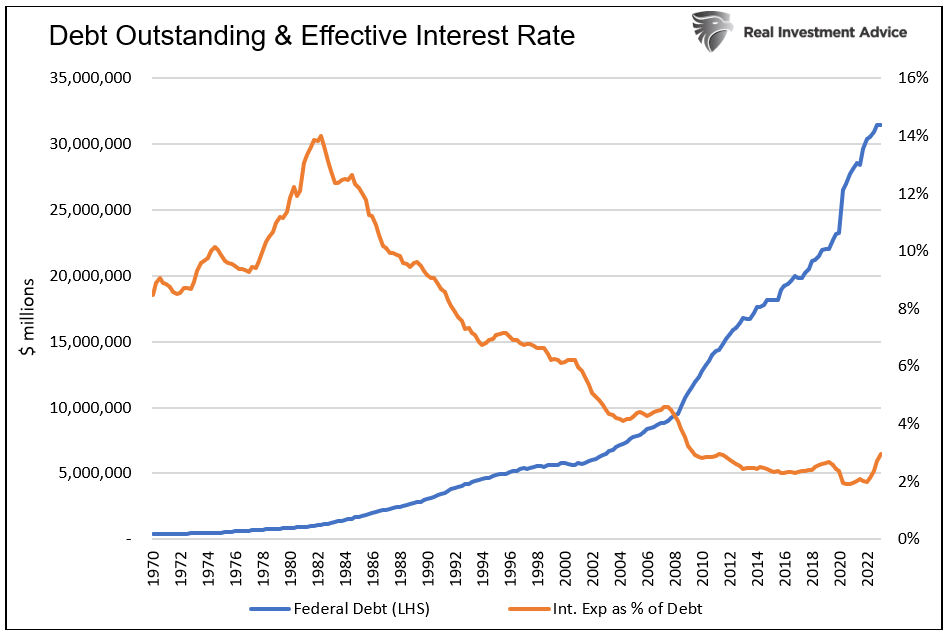

The Fed and government can ill afford to maintain today’s interest rates.

In what was a brutal 2022 for investors, there was at least one sure-fire, money-making proposition for much of the year.

Central banks are set to hike policy rates this week. Markets expect rate cuts to soon follow due to cooling inflation, whereas we see central banks holding tight.

A favorable inflation report is just one step in a long journey.

There are multiple factors to consider, including your tax rate.

There’s another side to power, reflecting a more nuanced view. It can improve communication, convert more prospects and deepen relationships with existing clients.

Markets should brace for a deep US recession that warrants a dramatic one percentage-point interest-rate cut by the Federal Reserve, warned DoubleLine Capital’s Jeffrey Sherman.

BlackRock Inc. is poised to become a bigger buyer of assets that banks unload to improve their capital and liquidity, after concluding that the industry faces years of upheaval brought on by high-interest rates, stringent new regulations and possible consolidation.

There is a particular “setup” that we’ve historically found to be associated with abrupt “air pockets” and “free falls” in the S&P 500. It combines hostile conditions in all three features most central to our investment discipline: rich valuations, unfavorable market internals, and extreme overextension.

High-quality fixed-income assets may offer the best return potential in more than a decade along with diversification benefits as a likely recession approaches.

With inflation falling and growth slowly grinding lower, time is running out on many global central bank tightening cycles – especially for the Federal Reserve (Fed) that meets next week.

Investors should consider diversifying their credit exposure with asset-backed lending strategies, which offer a fixed income allocation, a potential inflation hedge, and downside protection with collateralized assets.

Before you say “not me” to Matthews’ jewel of introspection, you should know that at some point(s) in your life you probably did – want to be someone else. So did I. As a matter of fact, since my early 20’s I’ve always dreamed of being a rock star.

It’s shaping up to be a pivotal week for global stocks, as companies with a combined $27 trillion market value gear up to report quarterly earnings. As Netflix Inc. and Tesla Inc. showed last week, the pressure is on — to deliver or face a sharp selloff.

Listen to Wall Street’s top economists and you’ll hear the same message again and again: The risk of a recession is fading fast. And yet, in the bond market, the traditional warning that a downturn is near — an inversion of the yield curve — keeps getting louder.

Housing is by far the biggest expense for most American households. Any inflation analysis that ignores housing misses not only the elephant in the room, but the room itself.

Despite persistent inflation and elevated short-term interest rates, the economy appears to be holding up well, and we believe the Fed may deliver the “soft landing” it has been trying to engineer.

El Niño will test the resilience of both infrastructure and food supply chains.

Head of Franklin Templeton Institute Stephen Dover recently moderated a panel of our leading economists and asked this key question: What’s in store for investors in the second half? Here’s a quick take on their answers.

Global corporate bond returns just hit their highest level this year on bets that the inflation crisis is coming to an end. Some investors say this may be as good as it gets, with dangers lurking in credit markets for the second half.

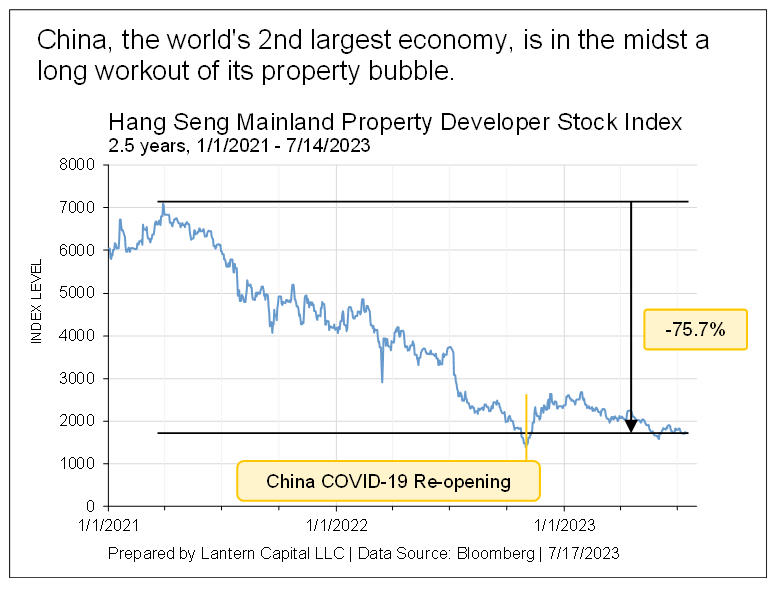

China’s ultra-long government bonds are seeing heated demand as the economy’s dire outlook and expectations for modest stimulus drive bets for further gains.

Home country bias means that investors may be overlooking international bonds. Certainly, the flows into U.S. fixed income ETFs dwarf the flows into international bond ETFs. That could be a missed opportunity.

Markets can present challenges for investors as volatility, direction, supply, outside influences, and future expectations are continuously changing.

Appealing yields and cautious markets.

We favor emerging market (EM) to developed market (DM) assets on a brighter macro backdrop. We get granular and harness mega forces, per our playbook.

The beginning of the banking and commercial real estate crisis this year has many parallels to the start of the residential real estate crisis in 2007.

Monetary policy infamously operates with long and variable lags, and successively navigating the impact monetary stimulus or withdrawal has on prices throughout the economy and financial markets requires a strategic mindset that is thinking and planning many moves ahead.

The economy has held up remarkably well despite the Fed’s tightening program, but with two more hikes likely in 2023, the risk of a slowdown remains elevated.

Bond yields well above implied and historical inflation rates are a great opportunity.

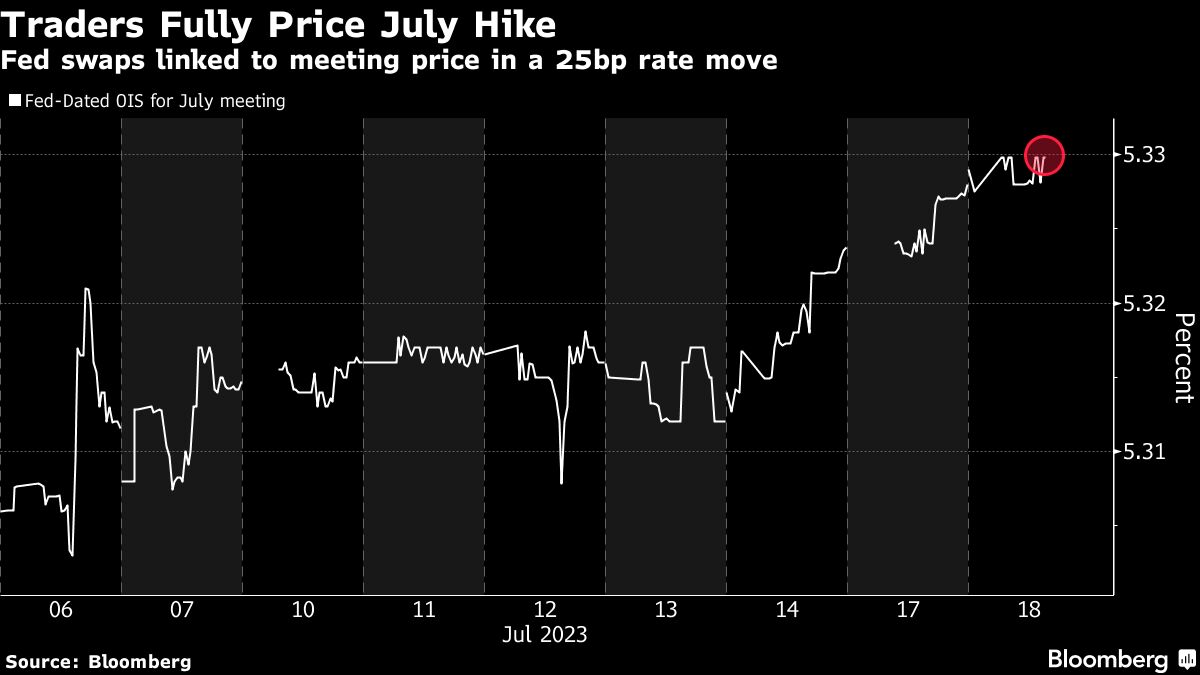

Traders now have no doubt: the Federal Reserve will start raising interest rates once again next week.

An improved income outlook for multi-asset investors, including higher yields, sharply contrasts with cloudy conditions at 2023’s start.

A high probability for an El Niño event in the second half of 2023 brings concerns of extreme weather, persistent inflation, supply chain disruptions, and market volatility.

The S&P 500 has generated double digit returns so far in 2023, but the gains have been narrowly focused. Heading into the second half, we will be watching to see whether the rally broadens or the market capitulates.

Investors with $250,000 or more to spend on municipal bonds are increasingly seeking opportunities to pick and choose what goes into their portfolios.

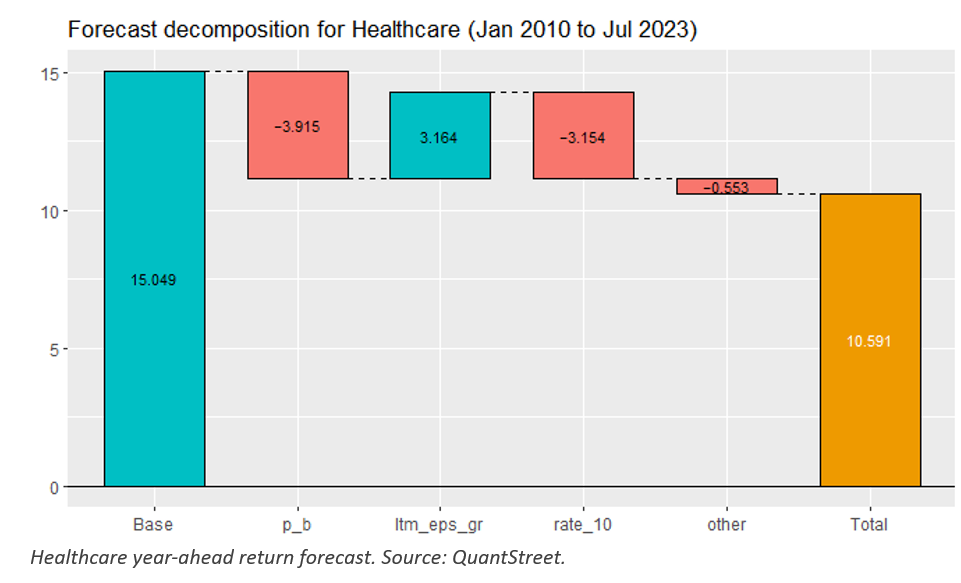

Healthcare stocks have been laggards on the back of cost pressures and punitive regulations. But the long-term trends are extremely favorable, making the sector a compelling opportunity.

While the deeply inverted yield curve has stoked anxiety among investors about the prospect of a recession, Goldman Sachs Group Inc. has a different message: stop worrying about it.

The continued rally in equity markets seems to be slowly reaching its crescendo. While the fundamentals have been screaming bearishly for some time now, there have been a number of structural factors at play driving markets higher in spite of these headwinds.

The second quarter was characterized by a debt ceiling showdown (which perversely provided a boost to liquidity) and by a big spurt in tech stocks.

Investors loading up on long-term bonds have a history at their back.

Nikko Asset Management presents an analysis of global market trends, offering insights into the surprising performance of equities and the resilience of the global economy to date.

With the highest yields in years, the muni bond market looks increasingly attractive.

As summer temperatures peak, inflation just won't completely cool down. The question is how much more the Federal Reserve should do about it.

Maybe it’s something about the dog days of summer — the record heat in the last few weeks has made everyone a little delirious — but the July-August period is proving particularly popular for “pivot” rallies in US financial markets.

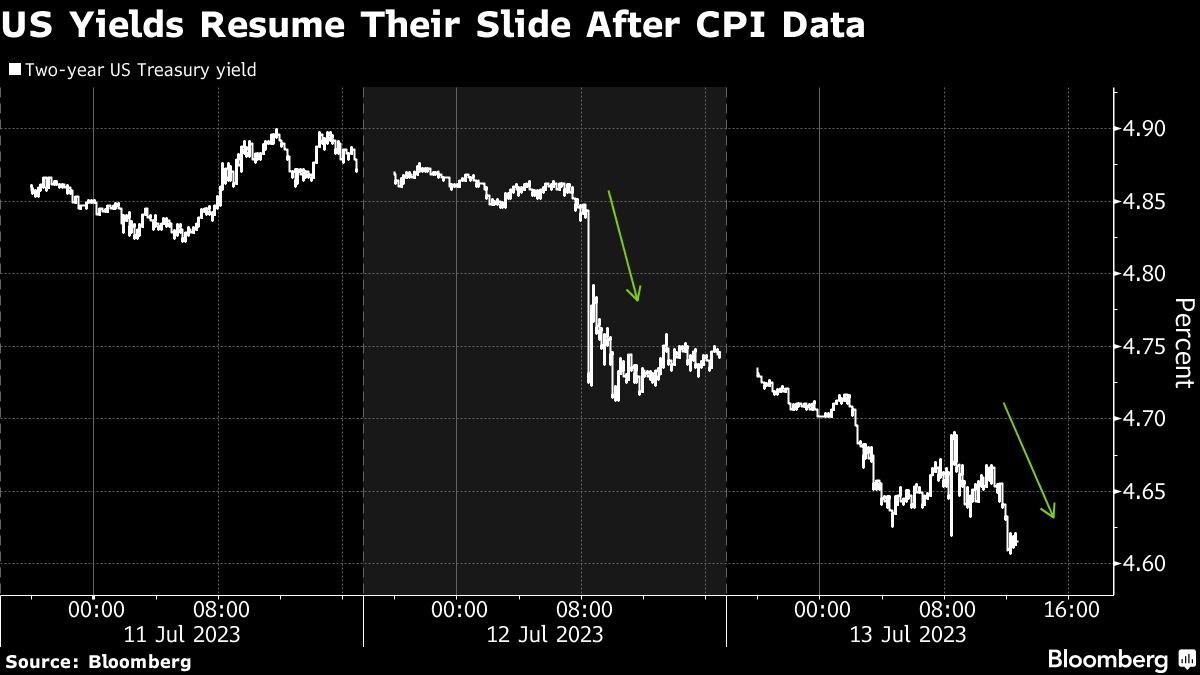

Bonds rallied for a second day as traders bet an aggressive streak of global interest-rate hikes is close to ending, bolstered by optimism that inflation in the world’s biggest economy will continue to slow.

While this is a market estimate and in no way guaranteed, let’s just pretend for a minute that there is a 100% chance of this coming true and the FOMC is going to raise the Fed Funds rate by an additional 50 basis points.

While we agree with the enthusiasm for AI that has helped the market rally, investors may be better served by patience than by chasing recent risk-on sentiment.

Now that short-term Treasury yields have reached 5%, further upside is likely to be limited.