2023 Rhymes with 2007

Membership required

Membership is now required to use this feature. To learn more:

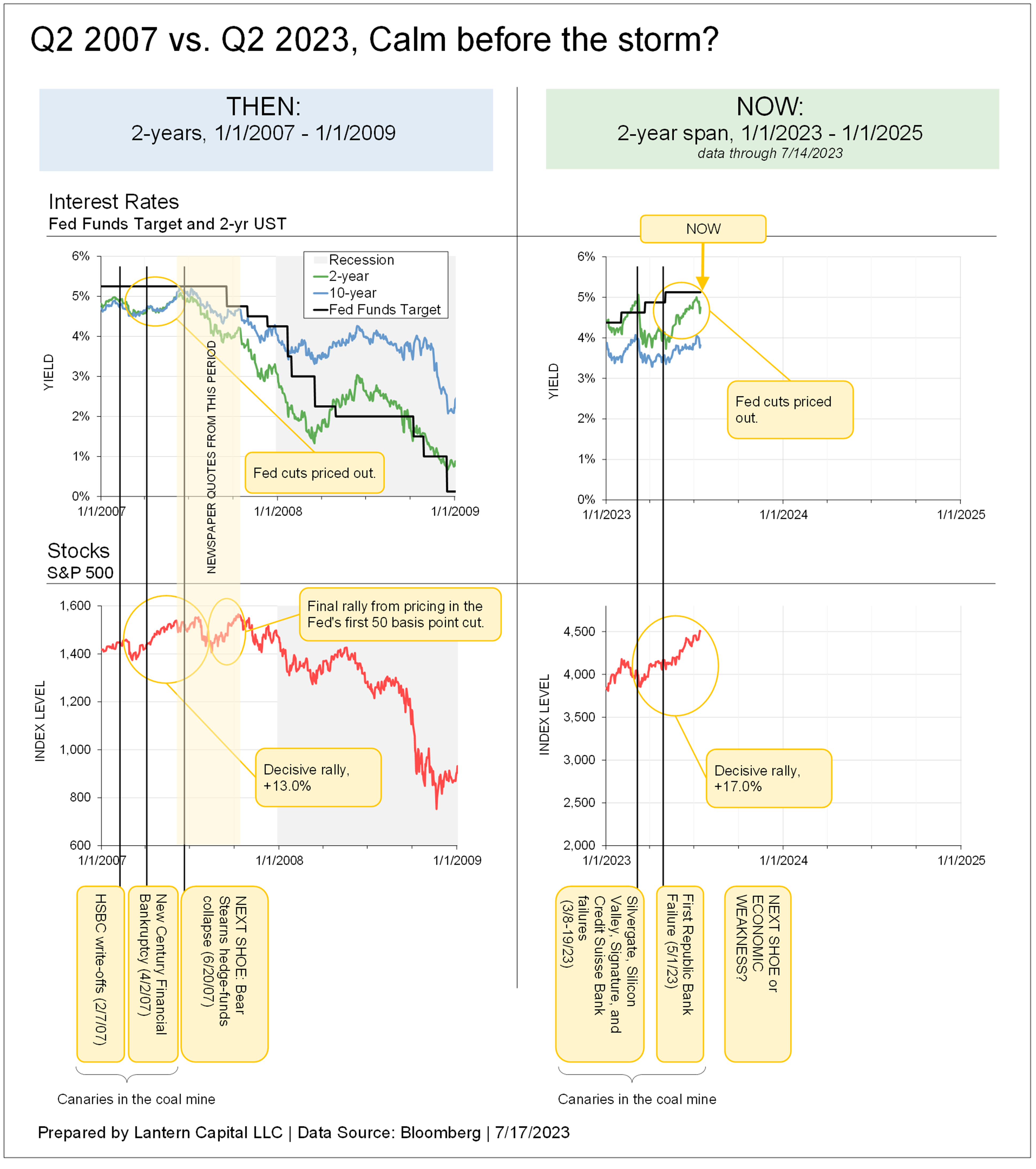

View Membership BenefitsSixteen years ago, in the second quarter of 2007, after the Federal Reserve had raised rates 4.25% and the first acute stress in subprime mortgages had been seen; U.S. Treasury yields and stocks bucked these early hints of what would become the Great Financial Crisis and rose dramatically (see charts, next page.)

HSBC’s “canary in the coal mine” subprime write-offs (2/7/2007) and New Century Financial’s bankruptcy (4/2/2007) had already happened, but because of residual strength in ISM surveys, labor, and consumer spending; markets and the Federal Reserve ran with the idea that the subprime problem was “contained.”

As we know now, it wasn’t. When two subprime Bear Stearns hedge funds collapsed in late June, interest rates began to fall, economic data began missing expectations in August, the Federal Reserve began cutting rates in September, stocks peaked in October, and the Great Recession began in December. By the end of the year, the 2-year U.S. Treasury had fallen to 3.05% from a 5.08% peak, the S&P 500 was down 9.8% from its high, and high-yield corporate bond spreads over U.S. Treasuries rose from 2.3% to 5.7%. In the second half of 2007, the mid-year hopeful narrative was supplanted by the whole economy crumbling.

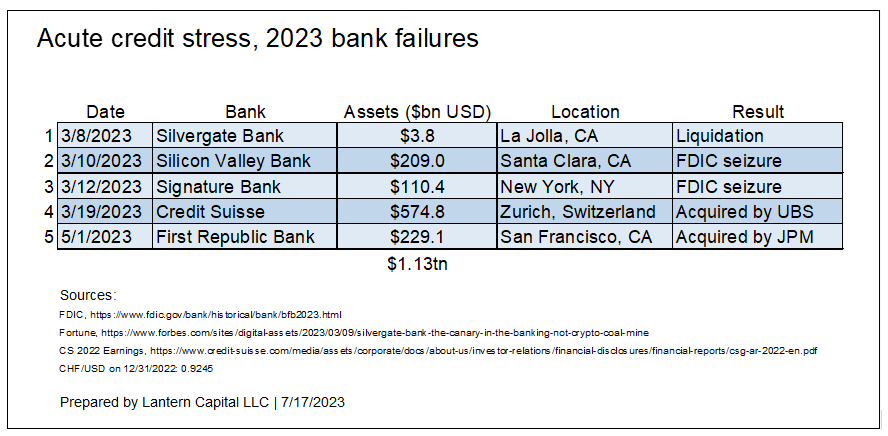

This year, while there is more yield volatility and inflation is higher, the similarities are striking. When four banks failed in March (see table below), the bond market priced-in several Fed interest rate cuts; predicting the Fed would lower to 3.85% by the end of the year. But in the ensuing months, from the combination of continued inflation, better-than-expected economic data, and a hawkish Federal Reserve; interest rates and stocks have risen significantly.

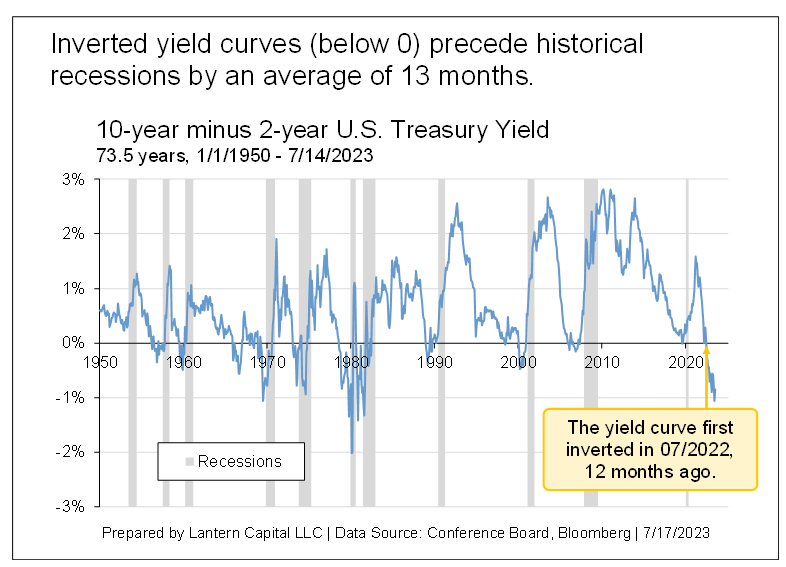

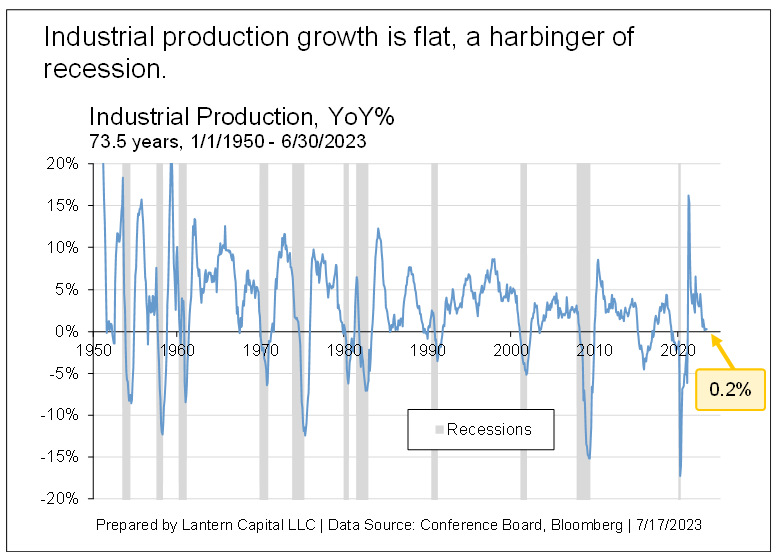

But also, just like 2007, cyclical macro-economic indicators are slowly weakening in the background. Labor is weakening, industrial production and retail sales have stalled, the yield curve has been inverted for a year, leading economic indicators have fallen dramatically, and the commercial real-estate crisis is still ahead. This is all amid a “super-bubble” or “everything bubble” that has been blown but not popped.

The charts below show stock and bond market similarities between 2007 and 2023.

Many economic and market conditions in mid-2007 were as strong or stronger than now:

The tone of the Fed and media in the Summer of 2007

The media and the Fed from June to October 2007, sounded a lot like now. Despite being directly ahead of the deepest recession since 1945, there was strong economic data, inflation fear, a hawkish Fed, and global central banks raising rates. The particulars were sometimes different, but the sentiment was the same. Links (URLs) require source subscriptions.

1. An optimistic Fed. Robinson, Gwen. “Fed minutes show concern on inflation”, Financial Times, 30 May 2007.

The minutes also show that nearly all Fed policymakers still saw inflation as “uncomfortably high” but were optimistic that the manufacturing inventory correction was largely over, and business investment would “most likely move higher in coming quarters”. They also expressed concern that growth overseas “could contribute to price pressures at home” with import price inflation also potentially fuelled by the dollar’s fall.

2. Strong economic data. Whitehouse, Mark. “Economy is Picking Up Speed”, Wall Street Journal, 2 June 2007.

The latest data show employment and manufacturing growing at a vigorous rate, suggesting the U.S. economy is regaining momentum after a slow start to 2007. The renewed strength, however, could raise inflation concerns for the Federal Reserve.

3. An optimistic Fed Chairman. Guha, Krishna. “Bernanke fuels hopes for US economy”, Financial Times, 5 June 2007.

Ben Bernanke on Tuesday fuelled market expectations of a vigorous bounce-back in US growth in the second quarter following very weak first-quarter growth.

The Federal Reserve chairman said first-quarter growth had been held down by factors such as an inventory adjustment, weak net exports and a slowdown in defence spending. These seemed likely to be at least partially reversed in the near term.

His analysis was reinforced by the latest Institute of Supply Management survey of activity in the service sector, which rose unexpectedly from 56.0 in April to 57.9 in May. The ISM’s May survey of manufacturing, published a few days ago, showed manufacturing activity up to 55.0, its highest level in 12 months.

4. Interest rates higher for longer. Connolly, Michael. “Inflationary Signals May Trigger Era of Higher Interest Rates”, Wall Street Journal, 6 June 2007.

With companies in many countries operating near full capacity after some of the strongest years of global growth in a generation, central banks are increasingly concerned that spare production capacity might soon run out. Those worries could push the banks to raise interest rates higher than they have in years -- and keep them there longer than most economists currently expect.

5. Global central banks raising rates. “Closing the Valve: Central Banks around the world still have some tightening to do”, The Economist, 14 June 2007.

To the surprise of no one who was watching, on June 14th the Swiss National Bank raised interest rates by a quarter point. Next week Sweden's central bank will probably do the same. Central banks almost everywhere are in a similar mood. Last week the European Central Bank (ECB) put rates up for the eighth time in 18months. The Bank of England refrained but will probably continue tightening policy this summer. And the Reserve Bank of New Zealand (RBNZ) lifted its official rate to no less than 8%.

America, where the federal funds rate has stood at 5.25% for almost a year, is an exception. But even there markets have gradually accepted that the Federal Reserve is not about to ease policy.

6. Inflation fear. Whitehouse, Mark. “Fear of Inflation Lurks in U.S. Recovery” Wall Street Journal, 2 July 2007.

Economists fret about inflation in part because the prices of food and energy have been rising so fast for so long. On average, forecasters expect overall U.S. consumer prices -- including food and energy -- to be up 3.1% in December 2007 from a year earlier, marking the fifth straight year in which the broadest measure of inflation has exceeded the core measure preferred by the Fed.

7. High consumer confidence. Willis, Bob. “U.S. Michigan Consumer Confidence Gains to 92.4”, Bloomberg, 13 July 2007.

Confidence among U.S. consumers unexpectedly jumped the most since October this month, helped by an unemployment rate close to its lowest in six years and gains in incomes.

8. Tight labor market. Reddy, Sudeep. “Fed Keeps Eye on a Tight Labor Market”, Wall Street Journal, 20 July 2007.

Federal Reserve Chairman Ben Bernanke suggested the Fed won't be convinced that the risk of higher inflation has subsided until the unemployment rate rises and businesses are operating farther from full capacity.

The labor market's tightness, especially for skilled workers, drew concern at the June meeting of Fed policy makers, according to minutes of the meeting released yesterday. "The continued tautness of labor markets was something of a puzzle in light of below-trend economic growth over recent quarters."

9. Out to October, on the day of the stock market peak from the Chief Economist at Bank of America. Levy, Mickey D. “No Recession in Sight”, Wall Street Journal, 9 October 2007.

Despite recent financial turmoil and a dismal housing market, there are key reasons why the economy will continue to expand, albeit at a modest pace, and not go into recession. Businesses are well poised to absorb a period of weaker product demand and are unlikely to significantly alter their hiring and investment behavior. Consumer spending is supported by rising incomes. Exports are strong. And monetary policy is consistent with sustained growth in domestic demand. Next year, we will look back and once again marvel at the flexibility and resilience of the economy.

10. Economists reducing recession probabilities. Izzo, Phil. “Economists’ Outlook Grows a Bit Rosier” Wall Street Journal, 12 October 2007.

The Federal Reserve may have stopped the economic bleeding caused by a summer credit crunch, the latest WSJ.com forecasting survey suggests, as economists turned more optimistic in the past month.

The survey, conducted Oct. 5-9, showed the average forecast for the chance of recession moved lower, to 34%. That was the first decrease since June and followed a forecast in the September survey of a 36% probability of recession.

The situation in 2023

In mid-2007, the residential housing crisis was directly ahead. In mid-2023, the commercial real estate (CRE) crisis is directly ahead. U.S. Commercial Real Estate is estimated to be worth a tremendous $23.8 trillion. Working from home and e-commerce has structurally upended its economics globally.

Upcoming CRE re-financing needs look insurmountable. Botros, Alena. “Morgan Stanley analysts are forecasting something ‘worse than in the Great Financial Crisis’ for commercial real estate” Fortune, 4 April 2023.

“More than 50% of the $2.9 trillion in commercial mortgages will need to be renegotiated in the next 24 months when new lending rates are likely to be up by 350 to 450 basis points,” Shalett writes. Alarmingly, Shalett notes that regional banks accounted for 70% to 80% of all new loan originations in the past cycle, with all eyes on the sector after the historic implosions of Silicon Valley Bank and Signature Bank last month. She said office properties were already facing “secular headwinds” from remote work, and she now sees a wipeout with vacancy rates close to a 20-year high: “MS & Co. analysts forecast a peak-to-trough CRE price decline of as much as 40%, worse than in the Great Financial Crisis.”

Bolstering concern of the issue, the Federal Reserve wrote about CRE in their May 8, 2023 Financial Stability Report,

The shift toward telework in many industries has dramatically reduced demand for office space, which could lead to a correction in the values of office buildings and downtown retail properties that largely depend on office workers. Moreover, the rise in interest rates over the past year increases the risk that CRE mortgage borrowers will not be able to refinance their loans when the loans reach the end of their term. With CRE valuations remaining elevated, the magnitude of a correction in property values could be sizable and therefore could lead to credit losses by holders of CRE debt.

No new CRE loan origination. Putzier, Konrad. “Interest-Only Loans Helped Commercial Property Boom. Now They’re Coming Due.” Wall Street Journal, 6 June 2023.

Many banks, fearful of losses and under pressure from regulators and shareholders to shore up their balance sheets, have mostly stopped issuing new loans for office buildings, brokers say. Office and some mall owners are facing falling demand for their buildings because of remote work and e-commerce. Interest rates have more than doubled for some types of commercial mortgages, analysts and property owners say.

The combination of these forces is weighing on building values, shrinking the amount owners can borrow against their properties and increasing the risk of defaults.

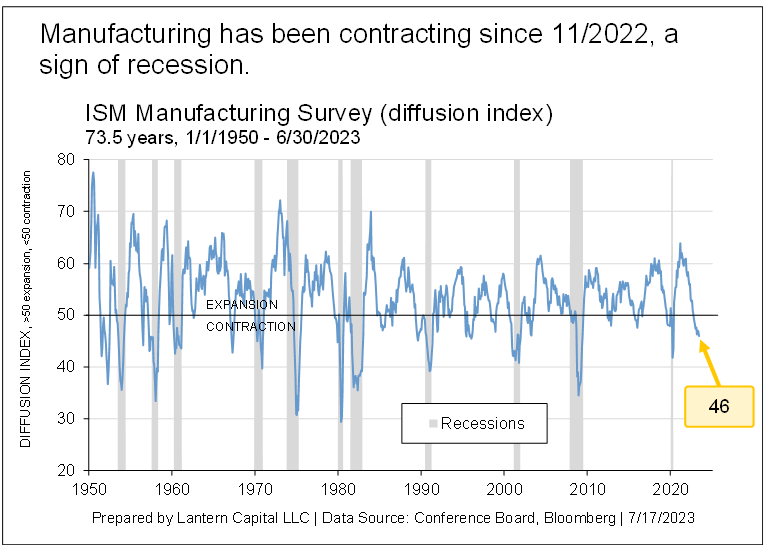

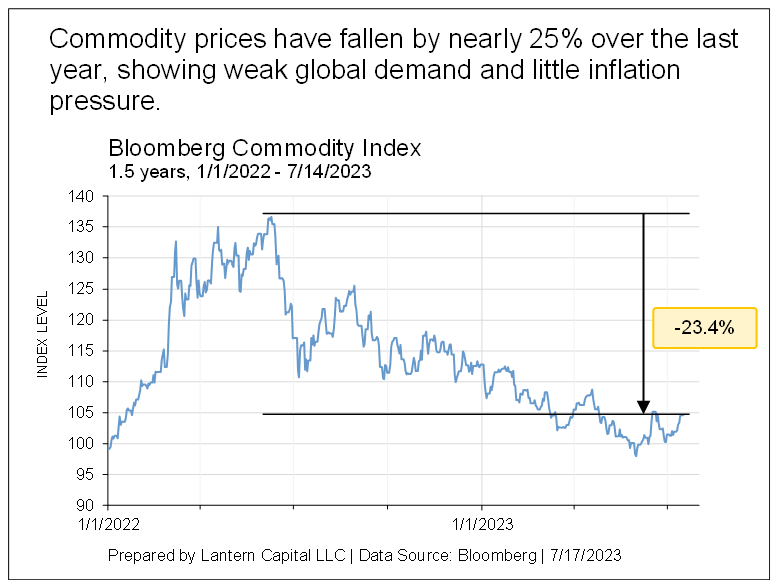

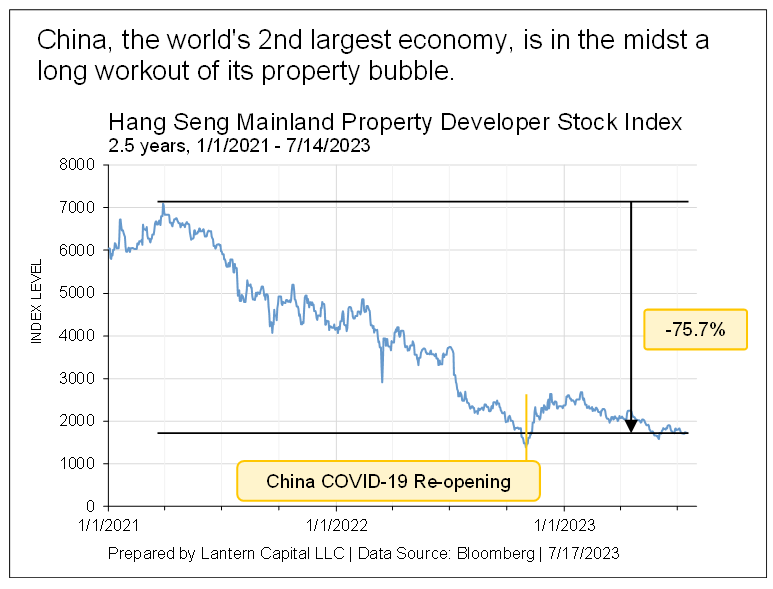

But aside from a coming commercial real estate crisis, several reliable economic indicators show proximity to a recession:

Conclusion

2023 is not 2007, but it is more similar than commonly known. 2023 has its own idiosyncrasies, and will have its own twists and turns, but at a minimum; the 2007 precedent shows that financial markets and the economy can look just like they do now and be directly ahead of a major recession. In other words, this situation of mixed signals isn’t new.

Despite recent strength in macro-economics and the stock market, there are too many signs of recession to not expect one. With regional banks and commercial real estate on the brink, the market narrative could flip suddenly. Market narratives rarely get resolved; they get replaced. Something will inevitably come along (another brick failing in Jeremy Grantham’s metaphorical dam) that changes the Fed and markets’ current focus on inflation.

A message from Advisor Perspectives and VettaFi: VettaFi’s Fixed Income Symposium is the biggest virtual event this summer. Register here and learn from experts and thought leaders how to navigate this unusual fixed income environment.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All