High-Yield and Bank Loan Outlook

Third Quarter 2023

Here are the key takeaways from our latest High-Yield and Bank Loan Outlook report:

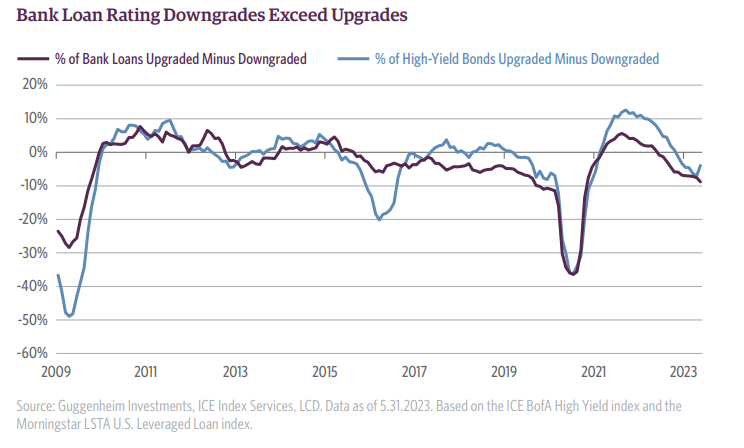

- The leveraged credit market is experiencing two contrasting trends: 1) aggregate credit fundamentals are in line or better versus historical levels, but 2) concern about the trajectory of fundamentals have led to downgrades outpacing upgrades at the fastest pace since 2020.

- This situation is giving rise to a process of capital rationing in the primary market, evidenced by large declines in debt issuance and shifts across industries and structures. Lack of issuance typically portends higher defaults.

- We anticipate the momentum of negative rating migration to persist.

- Investors should concentrate on stable opportunities and remain mindful of the potential risks associated with capital rationing and increasing defaults.

Summary

The leveraged credit market is experiencing two contrasting trends: on one hand, aggregate credit fundamentals like earnings growth, leverage ratios and balance sheet liquidity, are in line with or better than historical levels. On the other hand, concerns about the trajectory of fundamentals have led to downgrades outpacing upgrades at the fastest pace since 2020 as the impact of persistent inflation and rising borrowing costs weighs on outlooks. This situation is giving rise to a process of capital rationing in the primary market, evidenced by large declines in debt issuance and shifts across industries and structures.

Despite challenging credit conditions, risk premiums in leveraged credit have been relatively stable. Yields remain near decade highs, and limited net supply coupled with high coupons have supported year-to-date performance. Considering these dynamics, we believe that high-yield corporate bonds and bank loans continue to offer compelling opportunities that should not be easily disregarded. But navigating the current credit environment requires careful monitoring of credit quality, industry disparities, and the impact of tight monetary policy.

Highlights from the Report

- The 12-month issuer-weighted bank loan default rate more than doubled from 0.7 percent at the end of 2022 to 1.6 percent by the end of May. The high-yield corporate bond default rate increased from 1.5 percent to 2.3 percent. Both remain below historical averages.

- The loan sector experienced a higher proportion of downgrades (7.6 percent) compared to upgrades (2.7 percent), resulting in a net migration rate of -4.9 percent between March and May. In the corporate bond sector, bonds saw a net rating migration rate of -1.8 percent over the same period, with 7.6 percent downgraded and 5.8 percent upgraded.

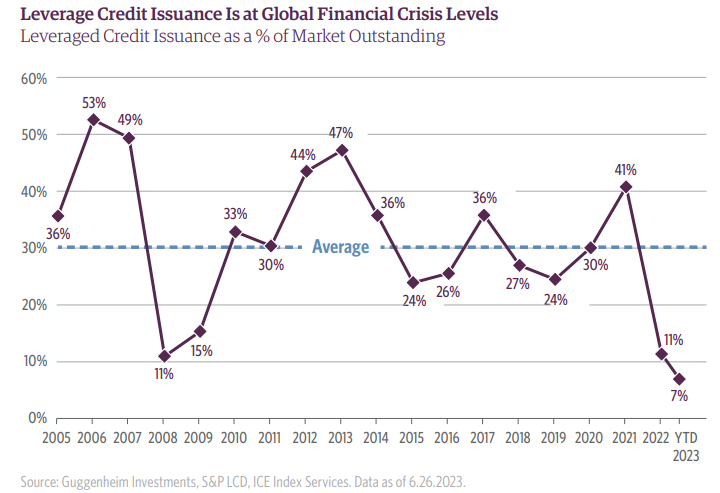

- While a healthy market typically sees leveraged credit primary market volume equal to at least 25 percent of the amount outstanding, this year it is tracking just 14 percent for the year.

- A lack of issuance, which is a feature of capital rationing, typically portends higher defaults. We believe we are on track to see the default rate in leveraged credit increase to 3.5 percent by year end.

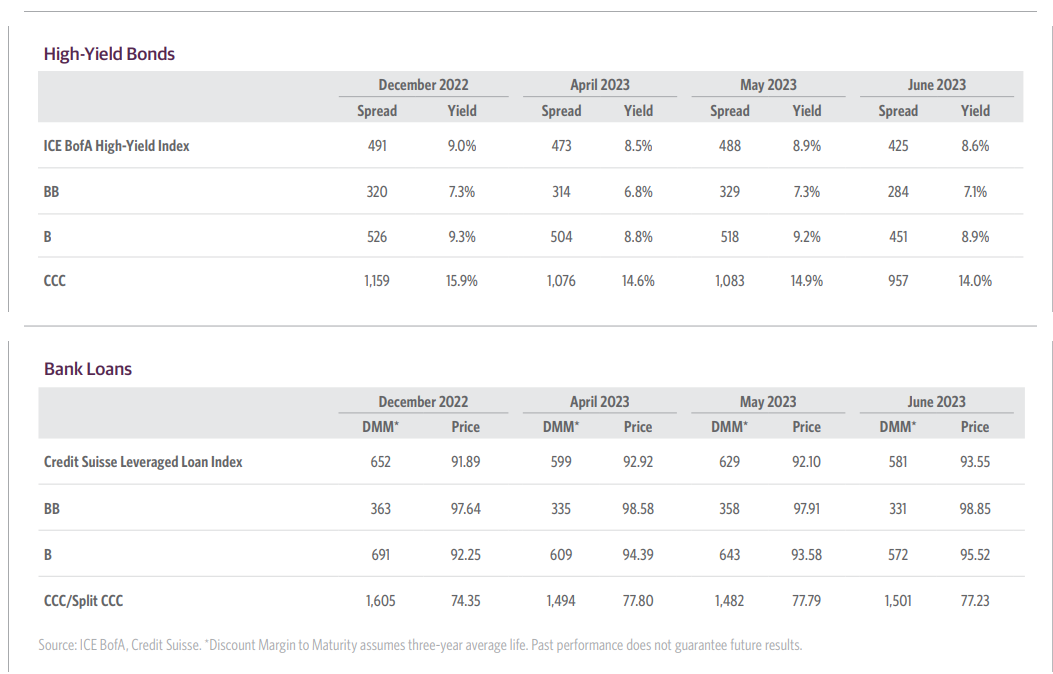

Leveraged Credit Scorecard

As of 6.30.2023

Macroeconomic Overview

The Fed Attempts a Hawkish Skip

While news cycles in April and May primarily focused on the potential downside risks of additional bank failures and the government debt ceiling, both of which fortunately did not reach worst-case scenarios, the U.S. economic data generally surprised to the upside. The third release of U.S. gross domestic product (GDP) growth for the first quarter came in at 2 percent compared to 1.1 percent in the advance release, and second quarter tracking estimates have increased to 1.5 percent from about -0.3 percent near the middle of April.

The housing market has been a notable source of positive surprises, with new home sales showing solid month-over-month increases of 9.6 percent in March, 4.1 percent in April, and 12.2 percent in May despite expectations of declines. Housing starts have experienced a surge, consistent with the recovery observed in the NAHB Homebuilder Survey. These data points indicate that interest-rate sensitive sectors of the economy are adapting to higher rates, and the worst of their negative impact on measures of broad economic activity may be behind us.

Amid a resilient economy, it has been encouraging to see inflationary pressures continue to ease. The headline Consumer Price Index (CPI) recorded a 3 percent year-over-year increase in June, the lowest since March 2021. Core CPI rose by 4.8 percent year over year, showing a meaningful decline from the previous report’s 5.3 percent. The path towards lower inflation is becoming clearer as shelter inflation cools, and the recent surge in used car prices is expected to reverse soon. Anticipation of these developments led the Federal Reserve (Fed) to keep interest rates unchanged during the June Federal Open Market Committee (FOMC) meeting, suggesting that skipping a meeting would allow it more time to observe the impact of previous rate hikes on the economic data.

The Fed made a cautious decision at the meeting, but their updated Summary of Economic Projections revealed a more aggressive stance, suggesting two more rate hikes this year. The diverging messages aim to manage expectations and prevent excessive easing in financial conditions and a resurgence in price pressures. But the market is increasingly pricing in the prospect of a soft landing, driven by the Fed’s characterization of the data and the growing optimism surrounding disinflationary trends. Paradoxically, the more the Fed presents a soft landing as feasible, the less likely it becomes as financial markets and economic conditions teeter toward overheating.

Concerns at the Fed are mounting regarding the potential resurgence of inflation in 2024. Inflation generally lags economic activity by several quarters, and the recent softening likely reflects only the initial impact of higher interest rates and the slowdown in activity at the end of 2022. Easing financial conditions, a resurgent housing market, and the economy’s adjustment to higher interest rates contribute to apprehensions over the path for inflation.

It is becoming increasingly likely that the Fed will need to maintain a tight monetary policy even as inflation prints decline over the next few months. This dynamic could eventually disrupt the optimism supporting credit spreads and equity valuations, given that a 2024 easing cycle is priced into expectations, judging by fed funds futures markets. Markets will have to recognize that lower inflation, easier Fed policy, and resilient economic growth are an unlikely equilibrium. In our view, growth will eventually need to give way to a recession to clear the path to the 2 percent inflation target.

Navigating Troubled Waters: Deteriorating Credit Ratings

The leveraged credit market is currently experiencing two contrasting fundamental trends: On one hand, aggregate credit fundamentals seem relatively stable, aligning with the recent positive surprises in U.S. economic activity. On the other hand, negative rating migration continues, and defaults have accelerated as the impact of persistent inflation and rising rates continues to weigh on issuers’ ability to cover fixed charges.

A few positive, top-down fundamentals that we have observed include the ongoing decline in leverage, stability in interest coverage, and strong earnings growth. The latest data through the first quarter reveals a decline in the leverage ratio among public bond and loan issuers to 4.7x, while interest coverage held at 4.2x. Although lower than last year’s peak, interest coverage remains robust compared to recent history.

Growth in earnings before interest, tax, depreciation, and amortization (EBITDA) has softened to 26 percent year-over-year on a last 12-month (LTM) basis, but remains in the double-digit range within commodity, consumer cyclical and non[1]cyclical, and business service sectors. Excluding commodities, EBITDA growth registered a 17 percent increase on a LTM basis, and expectations for 2023 have risen from 9 percent to 11 percent year-over-year growth since our last report.

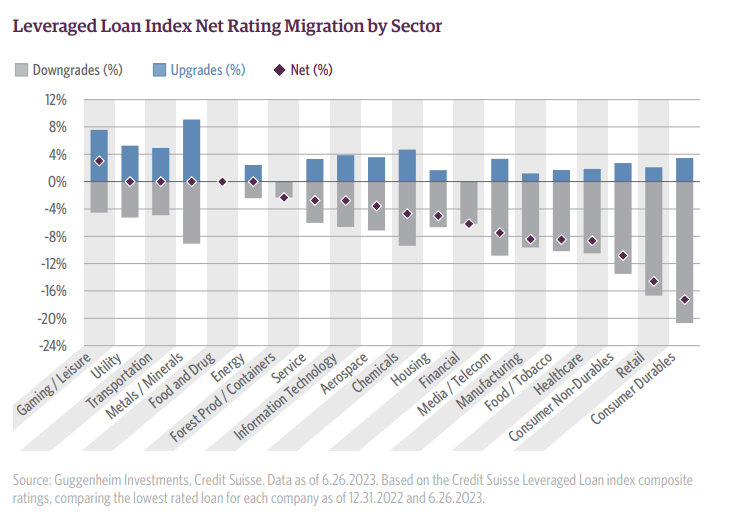

Despite these positive indicators, the loan segment experienced a higher proportion of downgrades (7.6 percent) compared to upgrades (2.7 percent) over the last three months, resulting in a net migration rate of -4.9 percent. This brings the last six months to a net migration rate of -10 percent. Most of the downgrades have been occurring in loans rated Single B or B minus, while BB-rated loans have accounted for only 11 percent of total downgrades despite representing 23 percent of the loan market by count.

In the corporate bond sector, bonds saw a net rating migration rate of -1.8 percent over the same period based on the ICE BofA High Yield index, with 7.6 percent downgraded and 5.8 percent upgraded, bringing the last six months to -5 percent. The high-yield corporate bond market continues to be comprised of nearly 50 percent BB-rated companies, providing the sector with a better starting point to weather headwinds related to downgrades.

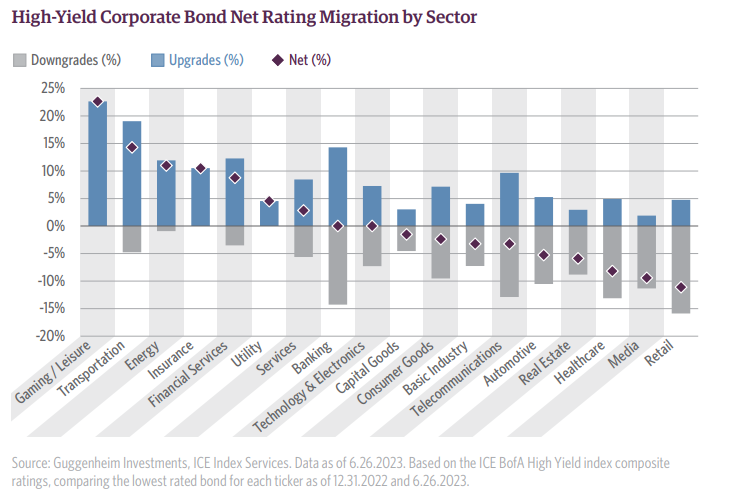

The rationale for downgrades varies, but include unsustainable capital structures, refinancing risk, and failures to meet de-leveraging or cash flow targets. It differs by issuer and industry. These contrasting trends underscore the need to focus on industry divergences, which as we show later, have implications for credit availability and defaults.

One sector experiencing positive migration has been gaming and leisure. Over 20 percent of gaming/leisure bonds in the high yield index have seen rating upgrades since the start of the year, and 8 percent in loans. This sector has enjoyed favorable conditions due to a tight labor market and the decline in gas prices from last year’s peak, which historically benefit consumer spending. We are somewhat cautious given headwinds growing for U.S. consumers, like the resumption of student loan payments this year, rising interest rates on credit cards and fading excess savings from COVID-related stimulus. But U.S. consumer fundamentals remain healthy, with low debt burdens relative to disposable income and strong wage growth.

Transportation has also seen net positive rating migration due to last year’s strong demand, large price increases, and the resulting financial performance. Spanning freight transporters to automotive parts providers and equipment rental, this sector has seen some natural deleveraging from strong earnings growth, while also taking steps to reduce debt outstanding. Cash flows have improved and maturities out to the middle of 2025 are practically non-existent (less than $4 billion). Demand is likely to soften going forward, but the recent decline in inputs prices, especially energy, may cushion some of the downside.

While the strength in consumer demand shows up clearly in services sectors, it’s not the case in goods, where retail, durables and non-durables have seen severely negative net rating migration in both bonds and bank loans. Frequently cited reasons for the downgrades include weak free cash flow, persistent revenue declines, inventory management issues, and unsustainably high leverage. Margin pressures are harder to combat with operators now hitting the end of price increases as consumer have sought lower-priced alternatives. Challenges here may persist if we do enter a recession, as goods sectors are historically impacted more severely than services.

The healthcare sector continues to face downward pressure on ratings, as we have noted in previous reports. Challenges include high costs, structural labor shortages, lack of pricing power and declining volumes. Additionally, the recent increase in interest rates has raised concerns about healthcare companies’ ability to generate sufficient operating cash flow in the future. Any maturities over the next two years add to the growing apprehensions, especially as this sector has struggled to access new capital, which we discuss later.

While there are both positive and negative aspects in credit rating migration, we anticipate further deterioration in coming months given fiscal and monetary policy outlook and high interest rates. This is a time to prioritize stability over stretching for small upside risks, so we continue to stress test credits for negative outcomes. One crucial aspect to consider when evaluating a credit is its capital needs, as the environment for securing new capital is increasingly constrained. We delve into this theme in the following section.

Lenders Ration Capital as Defaults Increase

Downward rating migration and limited capital availability are intertwined, creating a negative feedback loop. Credit downgrades we discussed in the previous section have influenced shifts in issuance, like a substantial drop from healthcare, but the rating agencies cite a forward-looking expectation of limited credit availability as a reason for downgrades, which then becomes self-fulfilling. There is a mutual reinforcement between these circumstances.

Many believe that Fed rate cuts will interrupt this negative loop and circumvent further pain, but we disagree. Based on futures prices, market participants expect the Fed to deliver over 100 basis points of rate cuts in 2024. Substantial rate cuts have always coincided with deteriorating economic and corporate earnings projections, more pullback in credit availability, and widening spreads. Furthermore, the effects of a capital withdrawal take several months to be felt, and an injection of liquidity in recessions also has a lagged impact. The dynamics we see in primary markets today are foreshadowing pain in credit markets several months from now, even if the Fed is easing at that time.

One of the dynamics that offer forward-looking signals is a shift in industry issuance within leveraged credit. Over the past five years, computers and electronics, services and leasing, and healthcare issuance have ranked in the top three by net volume. In 2023, the top three are services and leasing, chemicals, and manufacturing. Healthcare normally represents over 10 percent of net issuance, but this year is comprising just 2 percent. This is one example of how net rating migration and capital availability are mutually reinforcing dynamics.

Lenders have tightened the availability of credit but have not fully withdrawn it, which is a sign that they are rationing capital. A healthy primary market typically sees leveraged credit volume equal to at least 25 percent of the amount outstanding at the start of the year. Exuberant markets have seen issuance exceed 40 percent of outstanding, such as in 2007, 2013, and 2021. Issuance in these years was heavily skewed towards re-financings. Last year, leveraged credit issuance was just 11 percent of total outstanding, and this year it is tracking 14 percent for the year (7 percent year to date). This magnitude of pullback in issuance was last seen during the global financial crisis in 2008 and 2009. Pullbacks in capital availability have historically preceded increased defaults.

In such an environment, we typically see a return of less common strategies as borrowers seek to gain some flexibility. For example, a popular approach in loans this year has been amend-and-extend (A&E) activity. Through this method, borrowers and lenders revise the terms of an existing loan agreement before its maturity date. This gives borrowers the ability to extend the repayment period and make other modifications to certain provisions within the loan agreement, including interest rates and covenants. A&E activity has reached $88 billion of volume through the end of June and is poised to reach a new record at the current pace. Healthcare ranks in the top two industries taking this approach given challenges in raising new capital.

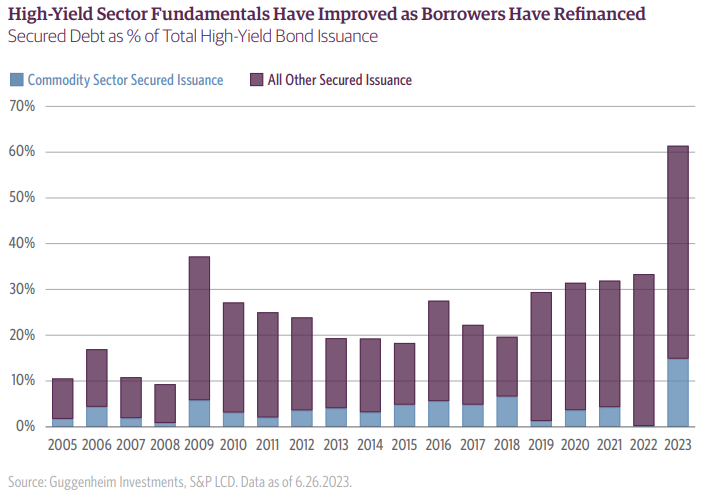

In the high-yield corporate bond market, a positive dynamic is that a record 61 percent share of debt issuance is secured. This is in part because certain loan issuers crossed over into the high-yield corporate bond space where terms are more favorable. Approximately 43 percent of secured debt issuance has been used, either partially or entirely, to refinance existing loans or revolving credit facilities. This positive trend means that the high-yield corporate bond sector is not only starting from a better credit rating profile of mostly BB-rated debt but is also increasingly secured, which bodes well for future recovery rates.

Defaults have increased as companies face the inability to cover interest expense and can no longer turn to primary markets to refinance high coupons. Sponsors have also taken preemptive measures in anticipation of possible future liquidity constraints. The 12-month issuer-weighted bank loan default rate increased from 0.7 percent at the end of 2022 to 1.6 percent by the end of May. The high-yield corporate bond default rate increased from 1.5 percent to 2.3 percent. Both remain below their historical averages.

A handful of defaults this year came from long struggling retail names that after years of repeat capital injections, asset sales, debt exchanges, and previous defaults, finally reached the end of the road, in bankruptcy. These include (but are not limited to) Party City, Serta Simmons Bedding, David’s Bridal, and Bed Bath & Beyond. An even larger volume of defaults this year are in the form of distressed exchanges, which has many similarities to A&E activity. These are debt exchanges that give the lender more time to repay debt, forgive some of the par amount due, or carry new terms like payment-in-kind coupon features.

Elevated healthcare default volume in this cycle has been noteworthy given that it is typically a defensive industry. However, we continue to see most of the default volume being credit-specific and broad based across industries and driven by higher input costs combined with unsustainable capital structures. The diverse nature of this default cycle highlights the importance of bottom-up credit analysis and diversification in this environment.

Investment Implications

The credit market is navigating a challenging landscape characterized by rating downgrades, but with relatively stable spreads and attractive yields. High-yield corporate bond yields ended the quarter at 8.8 percent, with a spread of 445 basis points over maturity-matched Treasurys. Bank loan yields stood at nearly 10 percent, reflecting a discount margin of 594 basis points. These yields continue to appeal to investors, despite more cautious market sentiment surrounding the hardest hit sectors.

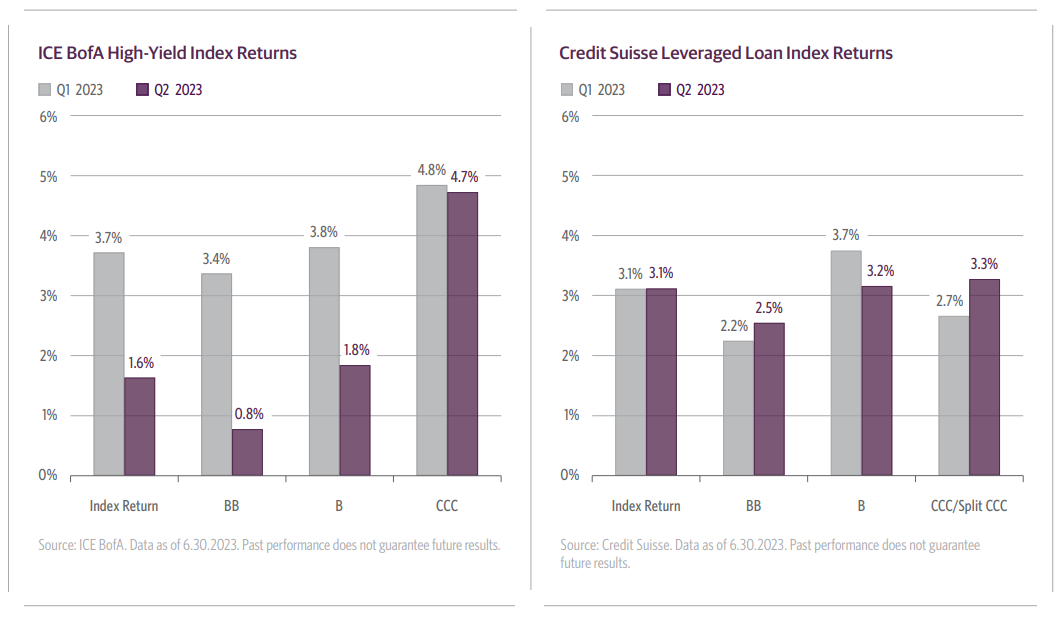

The performance of corporate bonds and bank loan markets in the first half of 2023 has been very strong, aided by more stable rates than in 2022, and some of the positive top-down fundamentals that we have highlighted. The ICE BofA High Yield Index returned 4.6 percent, its best first half performance since 2019, while the Credit Suisse Leveraged Loan Index delivered a 5.8 percent return, its best first half since 2009. Limited net new supply is keeping spreads contained, while high coupons and a milder headwind from higher interest rates (relative to last year) are supporting total returns.

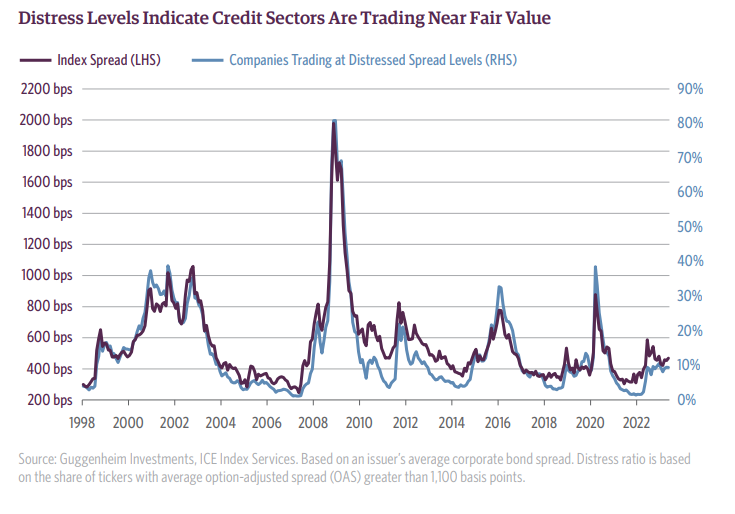

While the dynamics thus far have been beneficial to returns, contained spreads also create challenges for credit pickers. We worry that spreads have room to widen in both the high-yield bond and leveraged loan sectors later this year or in early 2024. In high-yield, spreads are 100 basis points tighter than the historical average and still near the 45th percentile of historical valuations. But measures of ticker level distress shows that the default cycle we expect is largely priced in. Companies with bonds trading on average over 1,100 basis points represent about 9 percent of the index. In loans, 13 percent have discount margins over this threshold, so we believe credit sectors are trading near fair value.

The challenge for investors lies in the potential volatility of spreads and prices as the Fed nears its 2 percent inflation target and the labor market weakens enough to support rate cuts. We believe that the transition from the tightening to an easing cycle, which may not happen for some time, could introduce significant spread volatility that will overshoot the level needed to compensate for the default cycle. This happens in every recession, with the share of companies trading at distressed levels typically reaching 25 percent or more. This volatility will present a valuable buying opportunity, making it sensible to maintain some dry powder for when the opportunity arises.

Investors should concentrate on stable opportunities and remain mindful of the potential risks associated with capital rationing and increasing defaults. Navigating the challenging environment in leveraged credit requires careful monitoring of credit quality, industry disparities, and the impact of monetary policy. We anticipate that the momentum of negative rating migration will persist until the Federal Reserve nears the end of its next easing cycle, at which point the headwinds facing the U.S. economy typically transform into favorable tailwinds due to the delayed impact of market liquidity injections.

Important Notices and Disclosures

INDEX AND OTHER DEFINITIONS

The referenced indices are unmanaged and not available for direct investment. Index performance does not reflect transaction costs, fees or expenses.

The Credit Suisse Leveraged Loan Index tracks the investable market of the U.S. dollar denominated leveraged loan market. It consists of issues rated “5B” or lower, meaning that the highest rated issues included in this index are Moody’s/S&P ratings of Baa1/BB+ or Ba1/ BBB+. All loans are funded term loans with a tenor of at least one year and are made by issuers domiciled in developed countries.

The ICE BofA U.S. High-Yield Index tracks the performance of US dollar denominated below investment grade corporate debt publicly issued in the US domestic market. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $250 million. In addition, qualifying securities must have risk exposure to countries that are members of the FX-G10, Western Europe or territories of the US and Western Europe. The FX-G10 includes all Euro members, the US, Japan, the UK, Canada, Australia, New Zealand, Switzerland, Norway and Sweden.

A basis point (bps) is a unit of measure used to describe the percentage change in the value or rate of an instrument. One basis point is equivalent to 0.01 percent.

AAA is the highest possible rating for a bond. Bonds rated BBB or higher are considered investment grade. BB, B, and CCC-rated bonds are considered below investment grade and carry a higher risk of default, but offer higher return potential. A split bond rating occurs when rating agencies differ in their assessment of a bond.

The three-year discount margin to maturity (DMM), also referred to as discount margin, is the yield-to-refunding of a loan facility less the current three-month Libor rate, assuming a three year average life for the loan.

Dry powder refers to highly liquid assets, such as cash or money market instruments, that can be invested when more attractive investment opportunities arise.

Spread is the difference in yield to a Treasury bond of comparable maturity.

RISK CONSIDERATIONS

Fixed-income investments are subject to credit, liquidity, interest rate and, depending on the instrument, counter-party risk. These risks may be increased to the extent fixed-income investments are concentrated in any one issuer, industry, region or country. The market value of fixed-income investments generally will fluctuate with, among other things, the financial condition of the obligors on the underlying debt obligations or, with respect to synthetic securities, of the obligors on or issuers of the reference obligations, general economic conditions, the condition of certain financial markets, political events, developments or trends in any particular industry. Fixed-income investments are subject to the possibility that interest rates could rise, causing their values to decline.

Bank loans are generally below investment grade and may become nonperforming or impaired for a variety of reasons. Nonperforming or impaired loans may require substantial workout negotiations or restructuring that may entail, among other things, a substantial reduction in the interest rate and/or a substantial write down of the principal of the loan. In addition, certain bank loans are highly customized and, thus, may not be purchased or sold as easily as publicly-traded securities. Any secondary trading market also may be limited, and there can be no assurance that an adequate degree of liquidity will be maintained. The transferability of certain bank loans may be restricted. Risks associated with bank loans include the fact that prepayments may generally occur at any time without premium or penalty.

High-yield debt securities have greater credit and liquidity risk than investment grade obligations. High-yield debt securities are generally unsecured and may be subordinated to certain other obligations of the issuer thereof. The lower rating of high-yield debt securities and below investment grade loans reflects a greater possibility that adverse changes in the financial condition of an issuer or in general economic conditions, or both, may impair the ability of the issuer thereof to make payments of principal or interest. Securities rated below investment grade are commonly referred to as “junk bonds.” Risks of high-yield debt securities may include (among others): (i) limited liquidity and secondary market support, (ii) substantial market place volatility resulting from changes in prevailing interest rates, (iii) the possibility that earnings of the high-yield debt security issuer may be insufficient to meet its debt service, and (iv) the declining creditworthiness and potential for insolvency of the issuer of such high-yield debt securities during periods of rising interest rates and/ or economic downturn. An economic downturn or an increase in interest rates could severely disrupt the market for high-yield debt securities and adversely affect the value of outstanding high-yield debt securities and the ability of the issuers thereof to repay principal and interest. Issuers of high-yield debt securities may be highly leveraged and may not have available to them more traditional methods of financing.

Investors in asset-backed securities, including mortgage-backed securities and collateralized loan obligations (“CLOs”), generally receive payments that are part interest and part return of principal. These payments may vary based on the rate loans are repaid. Some asset-backed securities may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices volatile and they are subject to liquidity and valuation risk. CLOs bear similar risks to investing in loans directly, such as credit, interest rate, counterparty, prepayment, liquidity, and valuation risks. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate.

This article is distributed for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This article is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This article contains opinions of the author but not necessarily those of Guggenheim Partners or its subsidiaries. The author’s opinions are subject to change without notice. Forward-looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

Applicable to United Kingdom investors: Where this material is distributed in the United Kingdom, it is done so by Guggenheim Investment Advisers (Europe) Ltd., a U.K. Company authorized and regulated by the Financial Conduct Authority (FRN 499798) and is directed only at persons who are professional clients or eligible counterparties for the purposes of the FCA’s Conduct of Business Sourcebook.

Applicable to European Investors: Where this material is distributed to existing investors and pre 1 January 2021 prospect relationships based in mainland Europe, it is done so by Guggenheim Investment Advisors (Europe) Ltd., a U.K. Company authorized and regulated by the Financial Conduct Authority (FRN 499798) and is directed only at persons who are professional clients or eligible counterparties for the purposes of the FCA’s Conduct of Business Sourcebook.

Applicable to Middle East investors: Contents of this report prepared by Guggenheim Partners Investment Management, LLC, a registered entity in their respective jurisdiction, and affiliate of Guggenheim Partners Middle East Limited, the Authorized Firm regulated by the Dubai Financial Services Authority. This report is intended for qualified investor use only as defined in the DFSA Conduct of Business Module. © 2023, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. Guggenheim Funds Distributors, LLC is an affiliate of Guggenheim Partners, LLC. For information, call 800.345.799 or 800.820.0888.

A message from Advisor Perspectives and VettaFi: VettaFi’s Fixed Income Symposium is the biggest virtual event this summer. Register here and learn from experts and thought leaders how to navigate this unusual fixed income environment.