There are two processes that we cannot escape: aging and math. This applies not only to human beings but also to large government social-insurance programs.

VettaFi’s core mission is to provide the index and distribution solutions that help asset managers build, grow, and navigate the markets with precision. Last week we took a massive, transformational step forward. TMX VettaFi signed a definitive agreement to acquire RAFI Indices from Research Affiliates, the undisputed pioneer of fundamental indexing and smart beta strategies.

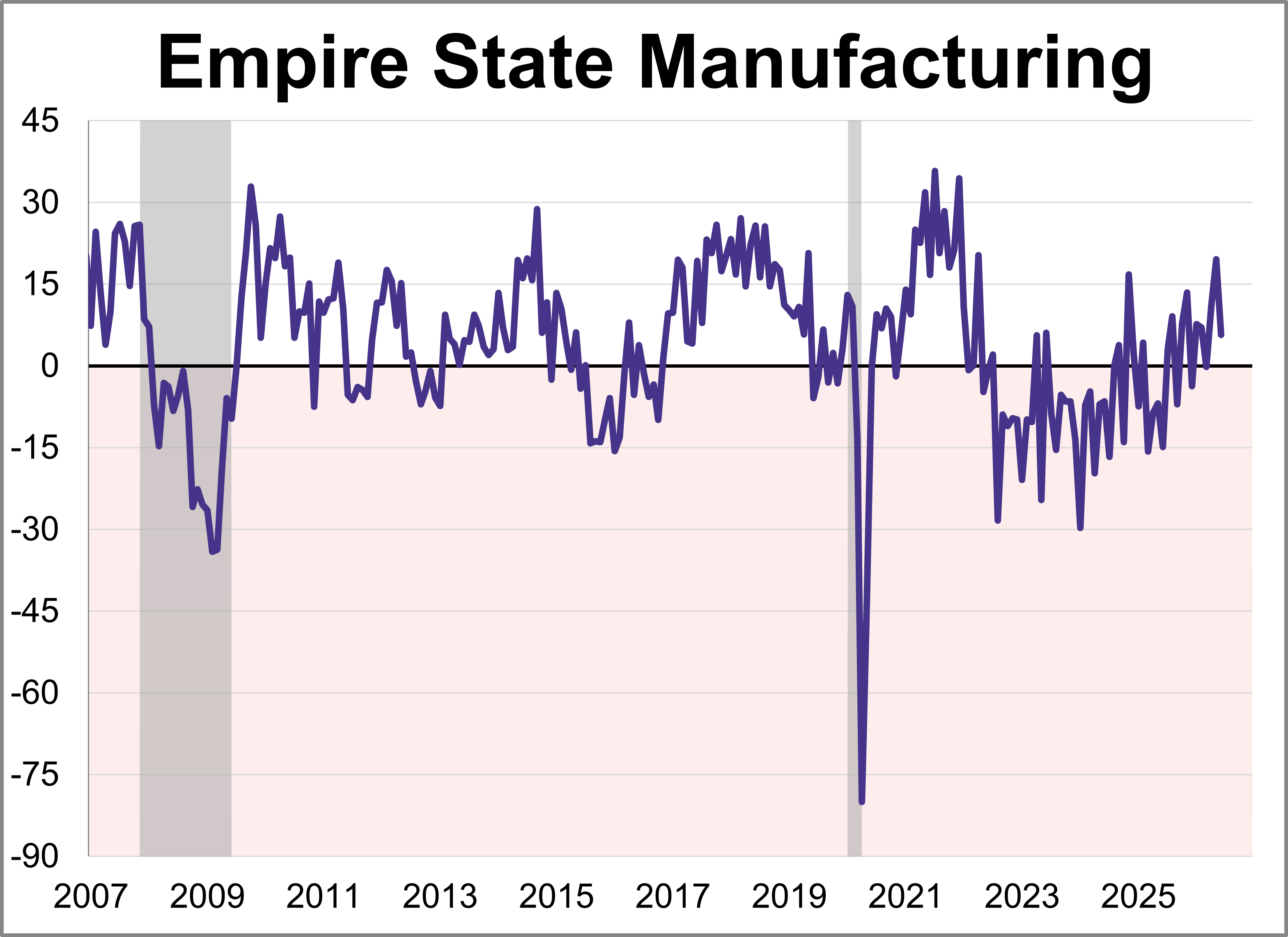

Manufacturing activity rose modestly in New York State, according to the Empire State Manufacturing June survey. The diffusion index for General Business Conditions remained positive but dropped 13.9 points to 5.7, falling short of the 13.2 forecast.

The K-shaped economy has become shorthand for a tidy story. The rich pull away while everyone else falls behind. It fits the mood, and it makes for a sharp headline. The problem is that it’s mostly wrong.

Despite everything we have seen in the economic data, which can be confusing, the US consumer has refused to crack. My friend Dr. Ed Yardeni, whom I have known since '98, has the most compelling explanation I have heard for why.

Companies are also looking for ways to cut workers’ costs by offering plans that charge workers less but restrict them to a narrower group of providers.

In this month’s Allocation Views, strong corporate fundamentals and resilient growth fuel our continued optimism toward equities into June, despite persistent inflation and more restrictive monetary policy.

For many registered investment advisors (RIAs), success has traditionally been measured in assets under management (AUM). As the industry evolves and consolidation accelerates, a broader question is emerging: are you building a practice or an enterprise?

The jury is still out on whether SpaceX is primarily a rocket company, as its name suggests, or actually more of a telecom provider or artificial intelligence play. Its expected valuation doesn’t help resolve the confusion.

After more than three years of underperformance, our prognosis for global health care stocks remains positive. The sector now offers a broader set of high-quality companies at valuations that appear increasingly disconnected from fair value.

Equity issuance is all the rage. The SpaceX (SPCX) IPO on Friday, Alphabet’s (GOOGL) up-sized secondary announced last week, and a slew of other major go-public names over the remainder of 2026 (Anthropic, OpenAI) buck the years-long trend of intense buybacks and shareholder-friendly activities by the world’s most valuable companies.

Begin with the print itself, because the headline flatters the internals only slightly. The bulk of May's gains came from leisure and hospitality, which added 70,000 jobs, nearly half of them in food services and drinking places; local government contributed 55,000, health care 35,000, and manufacturing a modest 7,000, while financial activities actually shed positions.

The biggest problem I find is that advisors don’t have the time they need to focus on growth. Sending out a mass invite via LinkedIn is fast and easy, but it doesn’t mean it is the most effective action you can take.

LPL Research analyzes bond markets as yields rise, exploring Fed policy expectations, inflation trends, and whether bad news is already priced into Treasuries.

Equity markets should remain supported by strong earnings and capital investment trends through 2026, but market concentration and macro risks leave less room for error.

In Part 1, we explored why Dollar Dominance Remains Alive and Well. Today, we will explore the stronger-dollar trade, the one macro trade that nobody is sized for.

Interactive Brokers Group Inc. is offering exchange-traded funds from BlackRock Inc. in savings plans in Europe, the latest platform to provide the booming product that’s become increasingly popular with mom-and-pop investors on the continent.

There is an old adage that the stock market climbs a wall of worry, which describes its ability to keep rising even amid negative economic news or events. This defies logic, yet I have watched it prove true time after time.

In case you’ve been living under a rock for the past few months, three of the world’s largest and most consequential private companies—SpaceX, Anthropic and OpenAI—are preparing to go public in the same year. Together, they could add nearly $4 trillion in market cap to public markets.

The world is not ending. It is restructuring. But restructuring, as I noted at the outset, comes with an asterisk. What is really happening is a replacement, of assumptions, of guarantees, of the architecture that held everything together for eighty years.

Our broad message for the second half of 2026 is this: Income still matters, but investors should be selective. Despite the recent rise in Treasury yields, we suggest investors favor a below-benchmark average duration with their bond holdings, favoring short- and intermediate-term maturities.

In the first phase of the generative AI boom, the winning strategy was straightforward: own the physical bottleneck. Alphabet’s plan announced this week to raise $80 billion suggests that the next phase may hinge on something else—the ability to finance AI capacity at scale without undermining returns.

While insurance coverage has broadly kept pace with rising catastrophe exposure, the protection gap — in absolute terms — has gone up as the value of exposed assets has grown, the Swiss Re Institute said on Wednesday.

LPL Research analyzes stock valuations, finding them fair given growth, rates, inflation, and AI-driven earnings outlook despite risks.

AI is a transformative technology with both near-term and long-term implications for the economy. For investors, while the debt-funded AI buildout has the potential to become a secular driver of risk premia, we believe any such shift would only play out through a multi-year adjustment and would not override the cyclical forces that affect markets.

Every family has a money story. It gets passed down quietly, invisibly, in the way families talk around the dinner table or on long walks together.

The market continues to demonstrate remarkable resilience. Lower oil prices, easing Treasury yields, and the relentless buildout of artificial intelligence infrastructure are still providing a favorable backdrop for risk assets.

If you’re not familiar with the name Leopold Aschenbrenner, you should be. A 24-year-old wunderkind, Aschenbrenner was hired by OpenAI in 2023 to work on the company’s “superalignment” team, essentially trying to figure out how to keep AI systems safe once they become smarter than the people building them.

Economies around the world aren’t just reliant on AI investments for growth. The appreciation of AI stocks has supported spending, which is following “K-shaped” patterns. A significant correction to the valuations of tech leaders would therefore be even more likely to result in recession.

The ETF landscape includes a wide variety of innovative, intriguing funds that look to meet investor goals. From equities to fixed income, all kinds of strategies offer intriguing spins on areas like income and dividends.

The essential feature of a useful alternative asset isn’t that it’s unusual or exotic, but that its returns aren’t tightly linked to the risks that already dominate the portfolio. The value of an alternative asset comes from the way it interacts with the other assets in the portfolio.

It’s not often that investors encounter something truly new in markets. But they will soon when Space Exploration Technologies Corp., OpenAI and Anthropic PBC go public with trillion-dollar valuations, or close to it. No company listed in the US has ever come to market so extravagantly priced — by a long shot.

The dollar is supposed to be dying. We’ve heard that argument for the better part of a decade, and it’s getting louder, not quieter. Dollar dominance isn’t fading. In fact, the events of late April 2026 just delivered the loudest counter-signal in years.

Equities extend gains as earnings and semiconductors lead markets higher. Consumer confidence remains subdued despite economic resilience. Inflation is easing gradually but remains above the Fed’s targey.

What is unusual about today, and I mean genuinely unusual, historically unusual, is that the people building the equivalent of Newcomen's engine today know exactly (or think they do) what they are building. They are not just pumping water. They “know” the vast potential.

The reality is, the American people wouldn’t accept the level of taxation necessary to maintain the warfare/welfare state. There would be a tax revolt. So, the government resorts to a less obvious tax.

If you want a blueprint for how countries can survive this era of great power rivalry, look no further than Vietnam.

Large asset managers are rolling out a wave of actively managed emerging-market ETFs, pitching them as alternatives to benchmarks increasingly dominated by AI stocks.

An unexpected rap on your front door is sometimes cause for anxiety. You are not sure who or what is out there, wanting to get in.

Contrary to what legal television series portray, verdicts rarely turn on a single moment of drama. They take shape gradually, as evidence accumulates and a broader narrative comes into focus.

After three decades of watching market cycles play out from both sides of the trade, I’ve come to a simple conclusion: Wall Street’s love of simple rules is one of the most dangerous aspects of investing.

Almost two-thirds of fund managers permit some level of “nuclear exposure,” with 34% allowing investments in nuclear weaponry, according to Jefferies Financial Group Inc.’s fourth-annual ESG and defense survey.

Despite these higher costs, a projected 45 million Americans are expected to travel at least 50 miles from home this weekend, setting a new record. Close to 40 million will drive while some 3.7 million will fly.

As more individuals turn to non-traditional financial advice — offered through social media, artificial intelligence, or other online services and platforms — advisors will be tasked with fostering a greater sense of trust with the public.

Since the post-COVID recovery began, U.S. nonfinancial corporations have generally managed capital conservatively. They have kept credit metrics stable and, in many cases, actively improved them. That discipline was not entirely voluntary: The sharp adjustment in funding costs triggered by the Federal Reserve’s 2022–2023 rate hiking cycle raised the bar for incremental borrowing and pushed management teams toward balance sheet restraint.

I have often written about one of the few indicators in economics that has earned its reputation over the years, and for good reason. It has preceded virtually every US recession since World War II. I’m talking about the inverted yield curve.

Elon Musk has bucked the trend of industrial conglomerate breakups, including such illustrious companies as General Electric and Honeywell International Inc., and decided to form a somewhat unwieldy company that makes rockets, spacecraft, satellites, antennas, modems and now computer chips. With SpaceX’s purchase of Musk’s xAI in February, the world’s leading space company was married to an AI startup and the X social media platform.

College costs continue to rise, and for many families, education is one of the most meaningful investments they will make. Preparing for those expenses often requires planning years, sometimes decades, in advance.

Global bond yields are reaching frightening levels due to the continued war in Iran and the effective closure of the Strait of Hormuz. Continued high oil prices and the threat of reverberating inflation are causing investors to demand higher yields on government bonds.

At Google’s developer conference, which is being held near its Mountain View, California, headquarters this week, Chief Executive Officer Sundar Pichai started his keynote by emphasizing the remarkable reach of Google’s services. Thirteen have more than a billion users, he said, and five of them have more than 3 billion.