There are two processes that we cannot escape: aging and math. This applies not only to human beings but also to large government social-insurance programs.

Last week the Social Security Administration released its annual trustees report, and the news was not good. Starting in the fourth quarter of 2032, one quarter earlier than previously projected, Social Security is set to pay only 78% of benefits. Such a broad cut is unlikely — Social Security is too popular, and the elderly rely on it too much. Even missing a cost-of-living increase is unthinkable. So something else has to happen.

The news is worse than expected because a lower fertility rate, less immigration, and provisions from last year’s budget and tax law are combining to decrease expected tax revenues. More generally, however, these negative shocks shouldn’t be a surprise, since at least two of those factors are deliberate policies.

The hard truth is that getting Social Security back on track will require both benefit cuts and tax increases. That means almost everyone will have to pay more and get less, including virtually everyone reading this (and writing it, for that matter).

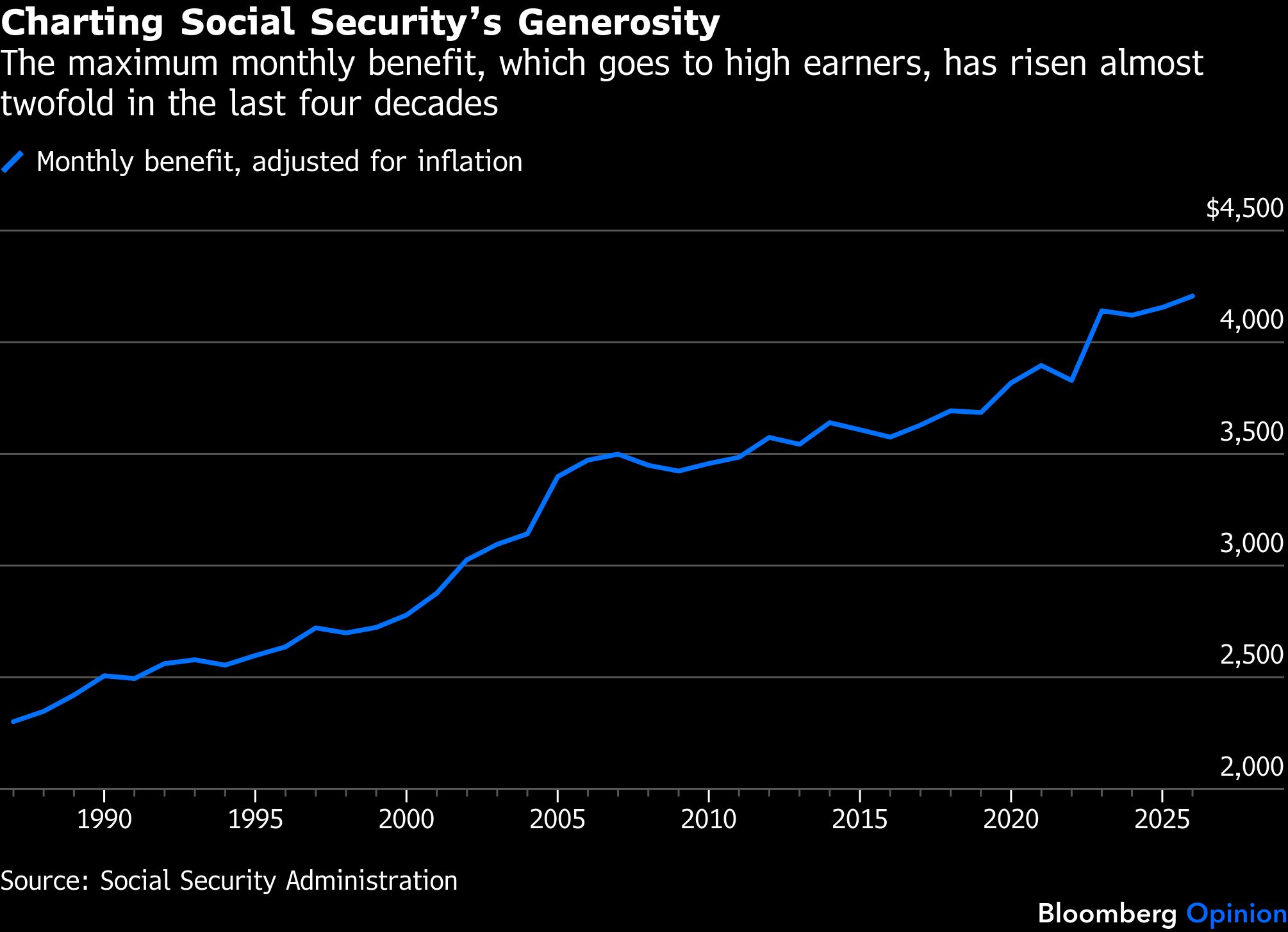

We will not grow our way out of it. Even if AI increases GDP, wages will likely increase with productivity — and while that will increase tax revenues, it will also increase liabilities. Part of the reason Social Security is becoming unsustainable is not only that society is aging, but also that benefits have become more generous. They are initially calculated by taking average lifetime earnings and indexing them to wage growth, instead of price inflation. Then once the benefit is calculated, it rises with price inflation. The idea is to ensure stable living standards.

But because wages generally grow faster than inflation, Social Security has become more generous over time. The figure below is the monthly benefit going to high earners, adjusted for inflation, based on year of retirement.

Despite these well-known financial challenges, which cause retirees so much uncertainty, it has become popular for politicians to say they won’t touch anyone’s benefits. This amounts to ignoring the problem. If they say anything, they tend to revert to their favorite promise: Someone else — generally the wealthy — will pay.

One common “solution” is just to lift the cap on earnings that are subject to Social Security taxes, currently $184,500. As if it is no big deal. But this amounts to an additional increase to the marginal tax rate of 12.4% on all income above this level. Someone earning $250,000 would face more than $8,000 in additional taxes. This would also put tax rates for high earners well above 60%, once state and local taxes are accounted for.

Maybe the US can get away with that level of taxation without harming the economy. But there is not much left to pay for anything else — more generous benefits for childcare, for example, or health benefits for working Americans. Seniors already have the lowest rates of poverty and more wealth; it is hard to justify spending any additional tax revenue only on them. Besides, even if Congress were to eliminate the cap and not increase the benefits going to higher earners, it would take care of only 67% of the shortfall, or 48% if their benefits were also increased.

The same goes for just filling the shortfall, about 1.06% of GDP, with general tax revenues, or asking future generations to pay by issuing more debt. The US is already running large and unsustainable structural deficits. With an aging population and higher interest rates, committing to even more debt to cover Social Security would be reckless — and would send another signal to bond markets that this country has no interest in getting its financial house in order.

That leaves the inevitable: benefit cuts or broad tax increases. Cutting benefits to the highest earners is one place to start, because they tend to have other income sources. There is also raising the retirement age, which is the equivalent of a benefit cut. Other ideas include using a different inflation adjustment each year, or using price inflation instead of wage inflation to calculate initial benefits. This can be paired with some combination of a broad tax increase — 1% or 2% on all covered wages — plus a small added tax on higher earners’ incomes.

The bottom line, again, is that the reality of math is catching up with the reality of aging. If the goal is fiscal responsibility, equity, and preserving the nature of Social Security, politicians need to drop the fiction that the program is not in trouble, or that high earners alone can bail it out. What the US needs is a compromise: benefit cuts and tax increases. All Americans have a stake in Social Security — and the sooner we take action to put the program on more sustainable footing, the less painful it will be.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Allison Schrager