Everybody is wondering how the stock market can be so high while the U.S. economy is so low. But you don’t hear the same rumbling concerns about the bond market – even though something very similar to ultra-high P/Es is going on in the fixed income side of your portfolio.

A brief monthly update on what's happening in the municipal bond market.

When it comes down to it, there are a few key macro variables that are highly correlated with the relative performance of value vs growth – most of them measuring the reflationary impulse in the system in different ways.

The price of gold had its first down week since early June, ending a spectacular nine-week rally. The yellow metal briefly fell below $1,900 an ounce on Wednesday as stocks neared their all-time closing high and the 10-year Treasury yield jumped on record supply.

Never before have I seen a market so highly valued in the face of overwhelming uncertainty. Yet today the U.S. stock market stands at nosebleed-inducing levels of multiple, whilst the fundamentals seem more uncertain than ever before. It appears as though the U.S. stock market has drunk from Dr. Pangloss’ Kool-Aid – where everything is for the best in the best of all possible worlds.

Although certain high-frequency data haven’t improved markedly, the threat of the virus has started to recede.

Whatever happens with Covid-19 and how we ultimately deal with it, be it a vaccine or medication or a change in behavior, we will adapt individually and together as a society.

Value often comes when good companies go out of favor, this is especially true in bull markets like we have been in the last several years. Almost by definition, when stocks are out of favor it further implies that their near-term performance may not be all that attractive.

In recent months, investment-grade debt has experienced a ferocious rally. What’s next?

Closed-end funds are known for leveraged income generation, but yields can come from a range of sources, strategies and products. John Cole Scott, founder of the Active Investment Company Alliance and chief investment officer of CEF Advisors, offers his perspective on the current CEF landscape and challenges presented by the coronavirus, not to mention the presidential election and recession recovery. Scott also shares his excitement about the AICA online CEF conference on Aug. 13, featuring the “best and brightest” minds in the CEF industry.

This week I did a complete re-read of Joel Greenblatt’s classic “The Little Book That Beats The Market.” For any of you that are not familiar with the book, Joel Greenblatt presents his magic formula for picking stocks that his research indicated will beat the market most of the time.

Growing challenges to banks have weighed on recovery hopes for value stocks. But our research of Japan’s experience and global value trends suggests value stocks don’t necessarily need financials to turn the corner.

We have a big economic calendar with reports on inflation, small business optimism, retail sales, consumer confidence, and unemployment claims. I expect the data to continue occupation of the back seat.

For the week, airlines stocks increased 9 percent, its best weekly performance since early June. Wheels up!

As I file this letter Friday morning, people are reacting to the July jobs report. My own reaction: The headline report is absurd.

Treasury Inflation-Protected Securities can help protect your portfolio against rising inflation, but there are nuances you should understand.

Russian stocks, as measured by the MOEX Russia Index, turned positive for the year on Tuesday of this week after plunging 30 percent due to the pandemic. This puts them slightly behind the S&P 500...

Government bond yields have tumbled globally but China’s yields have risen to pre-COVID-19 levels. The RMB hasn’t yet reacted to the favorable rate difference, and we think bond yields are likely to decline moving forward—a favorable landscape for China bonds.

Gold could extend gains as governments and central banks respond to slowing growth with vast amounts of stimulus.

America’s municipal bondholders have never been paid so little for taking on so much risk.

Several months into the Covid-19 era, Howard Marks takes a step back to consider the global health crisis, the economic fallout and the U.S.’s response to date. He also shines light on how one might – or might not – view the current circumstances in the framework of a market cycle.

There’s a small portion of the bond market that investors may have overlooked in the past, but should now consider—the taxable municipal bond market.

The U.S. economy contracted 9.5% through the second quarter, the worst single-quarter decline in gross domestic product (GDP) since the Commerce Department started tracking it in 1947. It was expected the report would show a dip, but it’s important to recognize what that dip represents.

Looking across the global opportunity set, we see potential for attractive yield, though uncertainties surrounding the global recovery suggest this is a time to be cautious.

The recent Treasury bond rally fits with our forecast that the recession has a second, more serious leg that will extend well into 2021, despite massive monetary and fiscal stimulus.

Two companies in the metals and mining space I’m looking forward to hearing from are Ivanhoe Mines and Franco-Nevada. Both are scheduled to report next week.

About two-thirds of this month’s comment is about COVID-19 and the risk of a second wave. This is not only for the sake of public health, which would be enough, and not only to contribute to a better understanding of the epidemic.

The U.S. dollar has fallen by about 7% against a broad basket of currencies since its mid-March peak. After a nearly decade-long bull market that saw it appreciate by more than 40%, we believe the dollar could be headed for a longer-term decline.

As you’re probably aware by now, spot gold is trading at an all-time high in nominal terms, having recently hit $1,977 an ounce. Futures touched $2,000 for the first time ever.

Americans are working longer for financial reasons – they can’t afford to retire. But what few realize are the enormous economic and social benefits that accrue to those workers and the companies they serve.

Thus far the market has shrugged off the recent rise in Covid cases, but the situation remains fluid. In our view, the best strategy is to invest in companies that are able to grow during this time of stress, either organically or by increasing market share as weaker competitors fall by the wayside.

Anyone still expecting the fixed interest payments from Treasuries, or even high-quality corporate bonds, to outpace inflation in the coming years is just setting themselves up for disappointment.

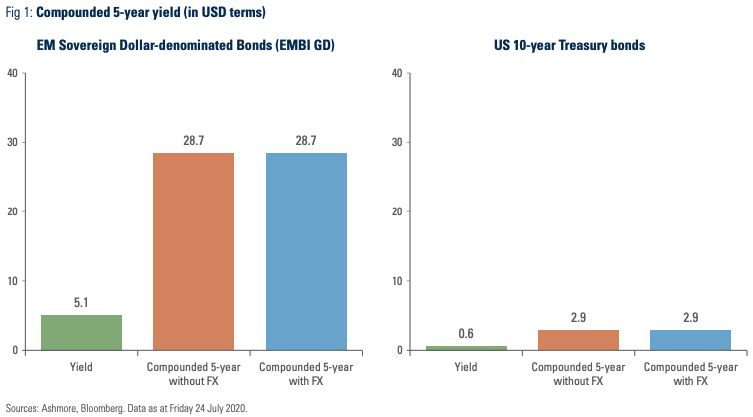

Does 9 times higher yield in EM than in US bonds make for an attractive investment proposition? We lay out the arguments.

We all know that past performance is no guarantee of future results, but you can see in the chart below that the white metal could possibly be setting up for another epic run-up. At this stage of the bull market, silver’s current price appreciation is ahead of any previous rally.

The U.S. and EU deliberate how to disburse aid, China’s recovery carries risks, and U.S. mortgage rates find a floor.

Investors must balance ongoing risks of the coronavirus against the extra yield the bonds provide.

Applying the definition of factor robustness that was established by our Research Affiliates colleagues in a 2016 award-winning paper, we determine ESG is not a factor. Nevertheless, the importance of ESG as an investing strategy is undeniable. We explore how greater clarity around defining ESG can quicken the pace of ESG integration in equity portfolios.

Investors have no chance of adding alpha by pursuing an “endowment” model. New research shows that even the most sophisticated institutions do worse when they increase exposure to alternative asset classes, and that investors would be better served with a passive, 60/40 allocation.

While we appear to have averted the worst pandemic outcomes so far, a resurgence in recently reopened states shows that we are not yet out of the woods. In our view, the economy will not fully recover until there is a vaccine or a reliable treatment.

Municipal bond investors will need to contend with the impact of monetary policy on market prices.

First quarter 2020 saw the U.S. economy in a tailspin; second quarter pulled out of it … but now is the recovery stalling?

Markets thus far in 2020 have been, to use an overused word, unprecedented. In a matter of months, we have witnessed economic and market moves that typically take an entire market cycle of many years to unfold. So, we truly do see 2020 as a year when investors are gaining “dog years” of experience.

The start to earnings season was not all that exciting as the banks were met with mixed reviews that saw the trading shops put up outsized profits thanks to the explosion of volatility in the quarter and the Fed backstopping the credit markets.

Zero yields could remove much or all of the "hedging value" of Treasuries in traditional bond allocations. Yet another concern for "traditional" bond allocations is less diversification potential (given compressed yields) going into a potential flight to quality. We believe a tactical approach—with a firm willingness to shift to defense...

Weeks before the S&P 500 bottomed, many millennial Robinhood investors began picking up coronavirus-impacted airline stocks. The buying spree continued even after Warren Buffett announced that he’d dumped his holdings.

U.S. stocks have been fairly resilient lately, even as coronavirus hotspots flare up around the country. Although consumers and businesses are increasingly worried about rolling shutdowns, major stock indexes generally have moved sideways. How long can this continue? Much depends on the shape of the economic recovery.

After an extremely eventful first half of the year, the key to managing through is understanding what has happened and why.

At LPL Research, we know the stock market is forward-looking: It focuses on what’s happening today and what it sees on the path ahead. Much of the real-time economic data we follow—such as transportation activity, home sales, and jobless claims—is showing tangible evidence that economic activity—while still depressed—has begun to make a comeback.

Recently, in the wake of the dramatic, catalyzing events associated with the COVID-19 pandemic, analysts have struggled to match the action in the Economy with that of the Financial System. Existing disparities of inequality and maldistribution have been dramatically exacerbated as the financial indices have soared.