The Trail to Recovery

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTHE TRAIL AHEAD

At the midpoint of 2020, we’re mindful that it’s been an extremely challenging year so far in the United States and around the globe. We’re in the midst of a pandemic that continues to impact all of us, our communities, and our economies.

Together we’re looking ahead for new ways to face these challenges and how we can prepare now for better times. We’ve been impressed by what we’ve seen so far: The resiliency and accelerated innovation among large and small US businesses; efforts by our national, state, and local governments to support our communities; and most of all, the dedication and unprecedented cooperation among our front-line health professionals, medical researchers, and everyday people to guide us through

At LPL Research, we know the stock market is forward-looking: It focuses on what’s happening today and what it sees on the path ahead. Much of the real-time economic data we follow—such as transportation activity, home sales, and jobless claims—is showing tangible evidence that economic activity—while still depressed—has begun to make a comeback.

Stocks already are pricing in a steady economic recovery beyond 2020 that may be supported if we receive breakthrough treatments to end the COVID-19 pandemic. However, the optimism we see reflected in the S&P 500 Index now may limit the size of the gains over the rest of the year.

It’s going to be a challenging environment with significant uncertainty that may lead to more volatility for the next few months. Still, we continue to encourage investors to focus on the fundamental drivers of investment returns and their long-term financial goals.

LPL Research’s Midyear Outlook 2020 provides our updated views of the pillars for investing—the economy, bonds, and stocks. As the headlines change daily, look to these pillars, or trail markers, and the Midyear Outlook 2020 to help provide perspective on facing these challenges now and preparing to move forward together.

Forecasts

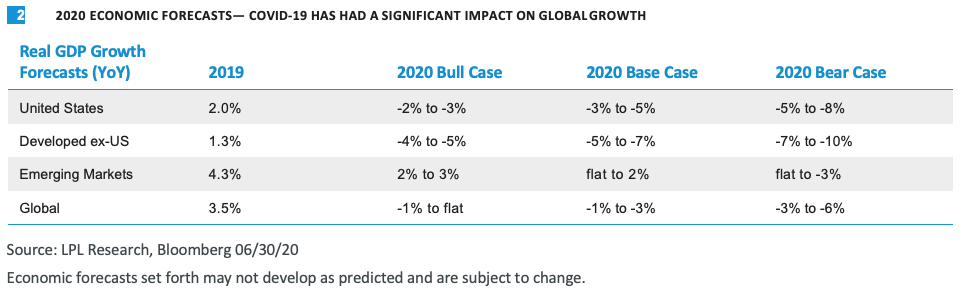

Domestic Economy: The trajectory of the economic recovery remains uncertain, but based on the depth of the contraction and a multi-staged recovery, our 2020 base case gross domestic product (GDP) forecast calls for a 3–5% contraction in GDP.

Global Economy: We expect economies in Europe to contract more than the United States or Japan in 2020. After the pandemic ends, deficits and populism may continue to weigh on Eurozone growth. So far, China has led the way out of the global crisis in terms of containing the virus and reopening its economy.

Recession: The US economy entered a recession in March 2020 as a result of the COVID-19 lockdowns and business closures. Although this recession may end up as one of the shortest on record, the eventual recovery may not be strong enough to get economic activity back to 2019 levels by the end of 2020.

Employment: Ongoing unemployment in industries that are more challenged because of social distancing may likely delay consumer spending’s return to 2019 levels until 2021.

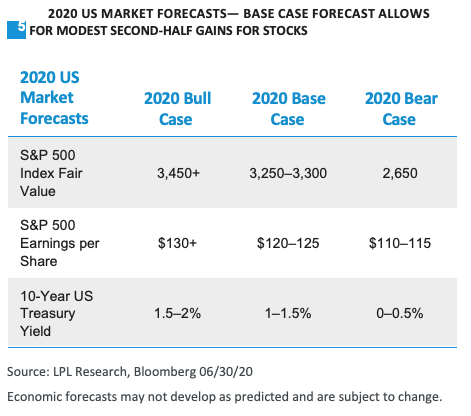

Stocks: We believe the optimistic economic recovery scenario reflected in stocks may limit their upside potential over the rest of the year. Our 2020 year-end S&P 500 Index target range is 3,250–3,300, based on a price-to-earnings ratio (PE) of just below 20 and a normalized earnings per share (EPS) number of $165.

Bonds: We expect interest rates to remain at historically low levels, but the direction may be higher over the rest of 2020. Our year-end base-case forecast for the 10-year US Treasury yield is 1–1.5%, which would be the lowest level to end a year on record if realized.

A contraction is a decline in national output as measured by GDP.

ECONOMY

The US economy entered a recession in March 2020, per the National Bureau of Economic Research, as a result

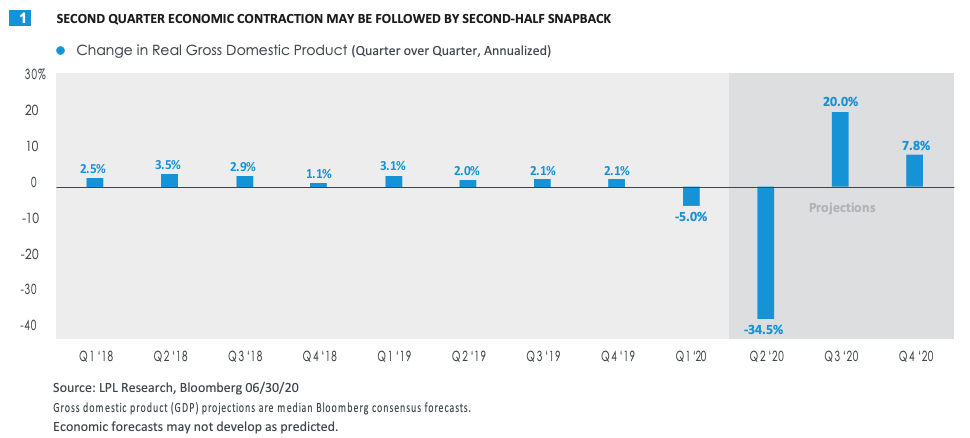

of the lockdowns and business closures to contain the COVID-19 pandemic. After GDP contracted by 5% during first quarter 2020 on an annualized basis, Bloomberg consensus expectations for the second quarter are calling for a mind-boggling 34.5% contraction on an annualized basis [Figure 1]. We see a strong second- half 2020 rebound in economic growth as more of the economy opens up, and this recession may end up as one of the shortest ever. However, the resulting recovery is unlikely to be strong enough to get economic activity back to 2019 levels by 2020 year-end.

The path of the economy over the rest of 2020 depends on whether COVID-19 infection rates and hospitalizations fall, facilitating more and faster business reopenings and a return to more normal consumer behavior. Alternatively, a potential second wave of the virus could lead to lockdowns being put back in place and consumers staying home. This recession has been led by consumers, and consumers—with help from the government and medical professionals—will have to lead us out.

ENCOURAGING SIGNS, BUT TOUGHER ROAD

Signs that the recovery is underway are encouraging. Policymakers have taken a potential depression off the table. Improvements in the timeliest data in recent weeks are encouraging, as most states have moved ahead with their reopening plans. We’ve seen increases in high-frequency data such as vehicle map requests, air travel, hotel occupancies, restaurant dining, public transportation use, and electricity consumption. Although the increases are coming off of depressed levels, there’s clearly some pent-up demand.

But a large portion of the US economy cannot be socially distanced easily, and this may limit the pace of the recovery by capping the amount of economic activity that can be recovered quickly. Capacity limits for restaurants and restrictions on large gatherings are two examples. More than 10% of US jobs are in the leisure and hospitality areas, according to US Bureau of Labor Statistics data, and unfortunately, some of those jobs won’t come back. More broadly, it will take time for stranded assets and affected employees to be retooled and redeployed. More economic disruption may occur as stimulus runs out.

Even with the surprisingly strong improvements in the May and June employment reports, the true unemployment rate remains stubbornly high and is likely one percentage point higher than June’s reported 11.1% rate, after adjusting for workers classified as “employed but absent from work.” For perspective, the unemployment rate peaked near 11% during the 2008–09 financial crisis.

SWOOSH-SHAPED RECOVERY

The trajectory of the economic rebound remains uncertain, but based on the depth of the contraction and a multi-staged recovery, our GDP forecast calls for a sizable contraction in 2020 [Figure 02]. Second-half growth headwinds that may linger well into 2021 suggest a swoosh-shaped recovery, or, if you prefer, a check mark: a quick, sharp decline and—after a small snapback—a gradual recovery over the next 12 to 18 months. We believe the square root symbol ( ) is too pessimistic because it implies a flat phase of recovery after the initial bounce, and a U-shape doesn’t capture the multiple stages of recovery. Our characterization assumes a COVID-19 vaccine will not be widely available for another year or so. Verifiable progress on an earlier arrival could help sustain the momentum of the initial rebound and move the economy closer to a V-shaped recovery.

CONSUMER OUTLOOK

Consumer spending comprises about two-thirds of US GDP, which makes jobs, incomes, and consumer confidence vitally important for economic recovery. With the highest unemployment rate since the Great Depression, and 22 million net jobs lost in March and April, it would be logical to expect a significant hit to consumers’ spending power to show up in recent economic data.

But stimulus efforts helped bridge the gap, including direct checks to individuals, unemployment benefits, and financial support for businesses to help them keep employees on their payrolls. We saw the impact of the stimulus in the 10.5% increase in consumer incomes in April and a record 33% consumer savings rate, according to the US Bureau of Economic Analysis, as well as the record-breaking 17.7% month-over-month spike in retail sales in May.

The stimulus has helped to bridge many consumers to the other side of the crisis, but structural unemployment in industries that are more challenged in a social- distancing society will likely delay consumer spending’s return to 2019 levels until 2021.

BUSINESS INVESTMENT

In this uncertain environment, businesses are pulling back on investing in future growth, but we’ve seen encouraging signs here as well. Small business confidence in the future has shown a solid rebound, according to the latest National Federation of Independent Business (NFIB) small business survey of expectations. The Institute for Supply Management (ISM) manufacturing survey for June returned to expansionary territory for the first time since the pandemic arrived in the United States, while the new orders component of the survey surged as businesses reopened. Still, economic output has a lot of ground to make up before returning to pre-pandemic levels.

The trail to recovery will be gradual, as businesses are thoughtful and deliberate about making long-term capital investment commitments. They’ll also need to learn more about how ongoing restrictions may impact their business until a vaccine arrives. Moreover, decisions for some industries could also be delayed until they have greater clarity on the post-election policy environment.

POLICY STIMULUS

Congressional policymakers prevented a deep recession from getting much deeper with an extraordinarily fast and bold response. The four stimulus packages already passed have totaled nearly $3 trillion, and a fifth package that could add more than $1 trillion to that total is in the works. Between what’s been implemented and what’s proposed, that’s potentially a total of over 17% of US GDP in fiscal stimulus support to bridge us to the other side of this crisis and help ensure a strong recovery. (2019 US nominal GDP was $21.4 trillion.)

The Federal Reserve (Fed) has been similarly bold, increasing its balancing sheet by about 13% of GDP, and signaling the central bank may hold its policy interest rates near zero through next year, and possibly through 2022.

INTERNATIONAL MARKETS

We expect economies in Europe to contract more than the United States or Japan in 2020, and post-pandemic conditions, deficits, and populism may continue to weigh on spending and capital investment in the Eurozone.

Movement toward a coordinated fiscal response to COVID-19 may introduce potential long-term upside, as does the possibility of continued US dollar weakness.

Bloomberg’s consensus forecasts for Japan 2020 GDP growth are calling for a smaller contraction than in Europe, supported by a very aggressive stimulus response. The latest fiscal proposal could increase the chances of a solid second-half recovery.

The US market, as measured by the S&P 500, is more growth-oriented, with a technology-and internet-heavy sector mix that has been well-equipped for the current environment. We expect US earnings to be more resilient than Europe’s in 2020, driven by improved economic growth and greater exposure to the growth sectors that have held up better during the pandemic.

China has led the way out of the global crisis in terms of containing the virus and reopening its economy. However, that hasn’t been enough to enable emerging market stocks to outperform the United States in 2020, based on the MSCI Emerging Market Index. Still, we find emerging markets attractive based on relative valuations and prospects for better economic growth in 2020, and likely well beyond. A potentially weak US dollar may provide a boost.

Our primary concerns are increasing US-China tensions, emerging markets’ inability to convert economic growth into profits and shareholder value in recent years, political instability, and Brazil’s inability to contain COVID-19.

We would recommend US-based long-term investors consider emphasizing domestic markets that are supported by massive fiscal and monetary stimulus, while carving out some exposure to Asia-focused emerging markets, where suitable. We believe active management is particularly well-positioned to outperform their benchmarks in these markets.

STOCK MARKET

Our expectations for a gradual economic recovery in the second half of 2020 appear to be in conflict with the S&P 500’s rapid ascent over the 12 weeks from March to June. On one hand, gains may appear appropriate based on the likelihood that the recession—officially declared on June 8—may be the shortest ever, aided by the massive stimulus response by policymakers and initial progress toward a vaccine.

On the other hand, the risk of a second wave of COVID-19 remains, particularly as some southern and western states have seen increases in infections and hospitalizations. In addition, some of the 20 million jobs lost in March and April, as reported by the US Department of Labor, will take a while to come back due to social-distancing constraints and the potential for lasting changes in consumer behavior.

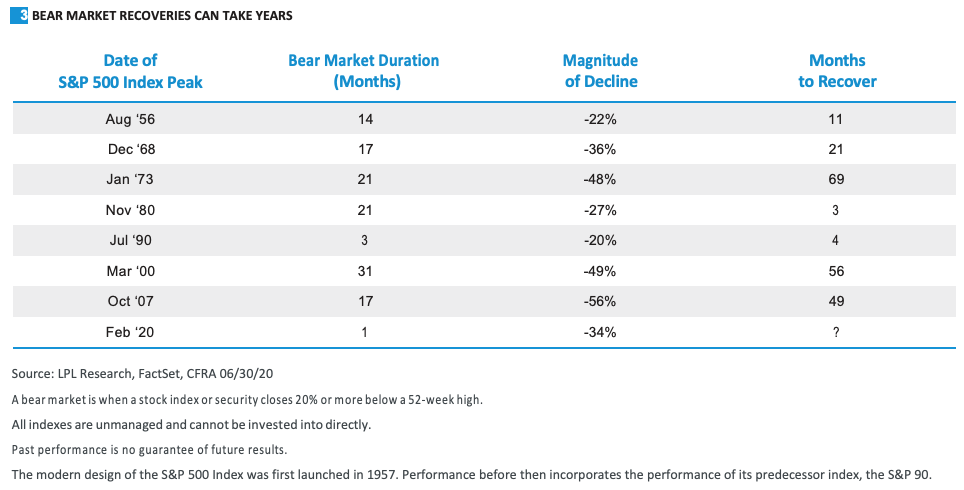

The uncertainty around these paths suggests stocks may have come too far, too fast. Although some recessions have seen stocks quickly recover bear market losses (1980, 1990), most of the time the journeys back to record highs have taken a year or more [Figure 03].

VALUATIONS MAY SLOW DOWN STOCKS

Stock market valuations have become more expensive because earnings have fallen, which may bring volatility if the recovery disappoints.

Using the 2021 consensus earnings estimate (source: FactSet) that we believe may be overly optimistic, the S&P 500’s PE ratio over 18 is above historical averages. However, low interest rates make bonds a less attractive alternative, while the absence of inflation, massive fiscal and monetary stimulus, and good prospects for a COVID-19 vaccine next year make these valuations tolerable. And we are hesitant to place too much emphasis on valuations given that historically they have not been good predictors of short-term stock market performance.

EARNINGS FACE LONG, UNCERTAIN ROAD BACK

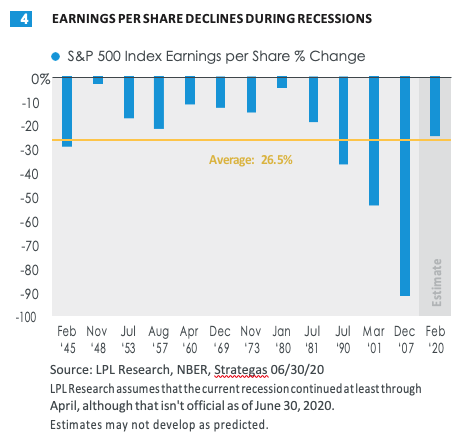

Our S&P 500 earnings forecast for 2020 is $120 to $125 per share. At the midpoint, earnings would drop about 25% from 2019’s level of $163, roughly in line with the average historical decline in recessions [Figure 04]. This forecast reflects: 1) the severity of the decline in economic activity in March and early April, 2) the initial snapback in activity after many states began to reopen beginning in mid-April, and 3) growth headwinds that will constrain the trajectory of the recovery later this year.

The severity of the recession and challenges for businesses incorporating social distancing introduce downside risk to this forecast. However, the encouraging progress to date in reopening the economy and reluctance to shut down again may limit the downside.

MARKETS LOOK TO 2021 AND BEYOND

We believe the optimistic economic recovery scenario reflected currently in stocks may limit their upside potential over the rest of the year. Our year-end target range for the S&P 500 is 3,250–3,300, based on a PE ratio of slightly below 20 and a normalized earnings figure of $165 [Figure 05].

An annual earnings run rate like that may not be achievable until well into 2021. But with interest rates so low and the possibility of a COVID-19 vaccine, we are comfortable using a longer-term earnings target to value stocks here.

Although we believe stocks may have come too far, too fast in the short term, for long-term investors, we continue to believe stocks may be more attractive than bonds. Historically, the early phases of bull markets have been accompanied by strong gains, which we think still leaves room for additional gains in the second half of 2020 and on into 2021. Our research dating back to 1950 shows that the historical average two-year gain for the S&P 500 coming off bear market lows has been 47%, leaving little room for additional upside. However, the bigger drawdowns have been followed by stronger two-year bounces, including the 96% bounce following the bear market in 2008–09, and 58% after the 2000–01 bear.

BEAR CASE

The potential for a second wave of COVID-19 introduces downside risk to our earnings and stock market forecasts on top of the uncertainty surrounding how quickly profits in some of the harder-hit areas of the economy can come back. Given what we’ve learned fighting this battle since March, including experiences in other countries that have successfully contained the virus, we’re optimistic that the economic and profit impact of a potential second wave may be more moderate than what we experienced earlier this year.

In a bear-case scenario, we would expect to see potential downside in S&P 500 earnings in 2020 of $110 per share and a possible downward move in the S&P 500 to 2,650. We would place a 10–15% probability on this scenario.

BULL CASE

Meaningful progress toward a COVID-19 vaccine could act as a market catalyst in the second half of 2020 and potentially enable a stronger snapback in economic activity and corporate profits than what we are currently anticipating. In that bull-case scenario, we would expect to see the S&P 500 break to new highs in the fall and propel S&P 500 earnings back to 2019 levels in 2021. We would place a 15–20% probability on this scenario, and we consider it may be slightly more likely than the bear case.

INVESTING FOR RECOVERY

We continue to favor large cap equities over small caps and US over developed international. Our style preference in the near term would be to lean toward growth in the still-challenging economic environment, though we would anticipate intermittent periods of value strength in the second half of 2020 as more evidence of a durable economic recovery emerges. Our favored sectors are communication services, healthcare, and technology, which we believe may offer the best combinations of strong balance sheets and earnings stability for the challenging near-term environment and growth potential beyond the recession. Consumer discretionary, financials, and industrials would be likely beneficiaries in the event that our bull-case scenario materializes.

Bear case is our forecast if we get a second wave of COVID-19 and economic conditions deteriorate more than we expect.

Bull case is our forecast if a COVID-19 vaccine arrives earlier than anticipated and the economy snaps back stronger than we anticipate.

BOND MARKET

We expect interest rates to remain at historically low levels, but the direction may be higher over the rest of 2020. Our year-end base-case forecast for the 10-year US Treasury yield is 1–1.5%, which would be the lowest level to end a year on record if realized.

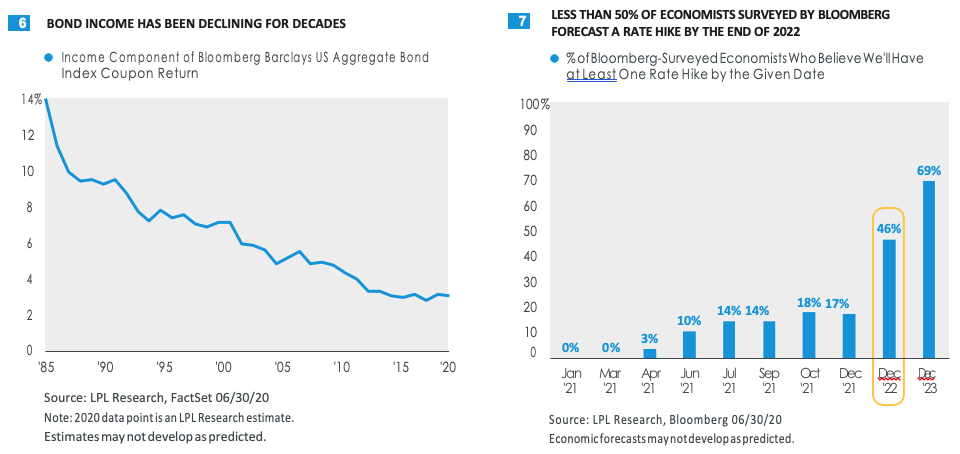

Rising Treasury yields contribute to bond prices falling, which can be offset by credit spreads tightening and the interest income that most bonds provide. With the credit spread for the Bloomberg Barclays US Aggregate Bond Index already near the average for the last cycle, and interest income at historically low levels [Figure 06], we would expect the index’s returns to be near flat over the rest of 2020 with some risk of losses; however, it would take a move above our target range to erase gains from the first half of the year.

Several factors limit the likelihood of bond yields rising significantly beyond our target range—even in the case of a more robust V-shaped recovery. Short-term Treasury yields will be well anchored by the Fed. Intermediate- to long-term yields may be pushed higher by improving growth, but inflationary pressures may be limited by slack in the labor market until the economy recovers more fully. Demand for Treasuries by international investors may also help to cap rate moves, as US yields continue to look attractive relative to other major developed market issuers like Germany and Japan.

THE FEDERAL RESERVE

The Fed is unlikely to hike (or cut) rates in 2020, and may not in 2021, even if the economic recovery is a little better than our baseline expectations [Figure 07]. Persistently low inflation during the last expansion should minimize any Fed concerns that it needs to raise rates preemptively to keep inflation under control. Consistent with its messaging, we expect the Fed to remain accommodative for some time, and raising rates probably won’t be on the table until after it ends its bond purchase program (known as quantitative easing). The Fed did not start raising rates in the last economic cycle until more than a year after its final round of bond purchases.

The Fed also has discussed the possibility of instituting some form of yield curve control to help support the economy. If this were to happen, the Fed would set a target cap for rates at maturities possibly as long as five years and buy enough Treasuries to keep rates below that threshold. Such a move would further help anchor rates for longer maturity bonds. For now, even the possibility of such a program has helped to keep rates lower at the shorter end of the curve.

BEAR CASE

Core bonds, particularly Treasuries, may benefit if a downside scenario emerges, such as a second wave of COVID-19 cases accompanied by renewed stock market volatility. In that case, the current 10-year Treasury yield of 0.65% (as of June 30, 2020) may be likely to fall at least below 0.5% and could even move toward zero. If that were to happen, Treasuries most likely would see further gains, supporting the broad Bloomberg Barclays US Aggregate Bond Index and helping it build on its positive return in the first half of 2020. While this is not our base- case scenario, it does highlight why suitable investors may consider the potential diversifying benefit of bonds.

INVESTING FOR RECOVERY

We would recommend that suitable investors consider positioning portfolios with below-benchmark interest-rate sensitivity and near-benchmark credit quality. We favor mortgage-backed securities (MBS) for their combination of interest income and limited rate sensitivity. We are neutral on investment-grade corporate bonds with valuations only slightly attractive and leverage increasing, but we still see incremental value for corporate bonds over Treasuries.

We continue to prefer stocks to the credit-sensitive bond sectors. Nevertheless, for those long-term investors seeking income, the credit-sensitive sectors may have a role to play in a well-diversified portfolio. Among those sectors, we favor a mix of dollar-denominated emerging market debt and high-yield bonds, with an underweight in equities to potentially help offset the added risk. We believe emerging market debt may likely benefit from the broadly supportive monetary policy environment, and valuations for high yield are still attractive, although the asset class leans away from some of the faster-growing sectors.

Municipal bond yields still appear attractive relative to Treasuries for tax-sensitive investors. We maintain a bias toward quality and are more cautious on high yield.

ELECTION 2020

Although all election years feel different, 2020 no doubt may be one of the most unique election years ever.

We have a pandemic, a deep recession, extremely heightened partisanship, a mail-in ballot controversy, an unpredictable president, and the oldest presidential candidate ever.

Amazingly, 1940 was the last time the S&P 500 was lower during an election year with an incumbent in the White House. Historically, when a president has been up for reelection, it has tended to boost stocks. Stocks were down big in 2008—but President George W. Bush had finished his two terms. It isn’t about Republican or Democrat—it’s about trying to boost the economy and stock prices by the time voters go to the polls. Some good news on the economy in the coming months, or progress toward a vaccine, could potentially get the S&P 500 all the way back to positive territory for the year, after being down 30% year to date in March, and that would possibly help President Donald Trump’s re-election chances.

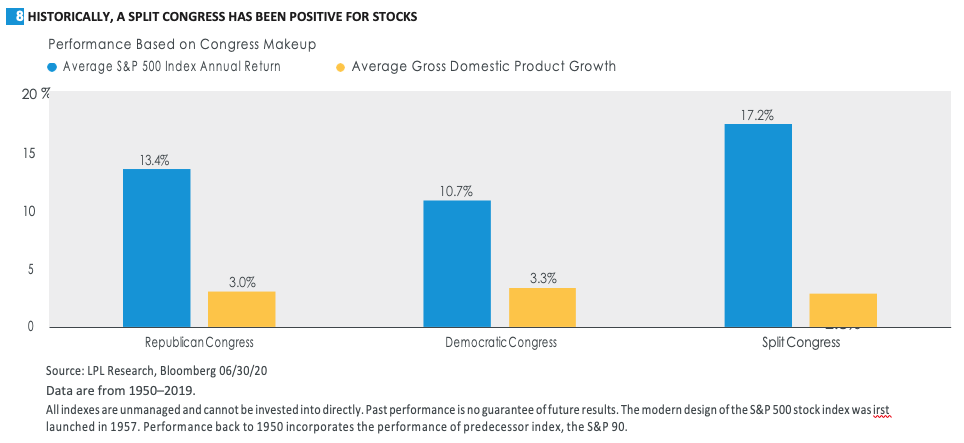

We’re often asked if stocks perform better under a Republican or Democratic president. We’d take a different angle and point out that stocks have tended to do their best when we have a split Congress. Markets tend to like checks and balances to make sure one party doesn’t have too much sway. When Republicans have controlled both chambers in Washington, DC, on average the S&P 500 has gained 13.4% per year and GDP has grown 3%. When Democrats have controlled both the House of Representatives and the Senate, the economy did a little better, with GDP growth of 3.3%, while the S&P 500 was up 10.7% on average. When we’ve had a split Congress, however, the average S&P 500 gain climbed to 17.2%, while GDP growth averaged 2.8%, again suggesting markets may prefer split power come November [Figure 08].

History shows that the US economy has major bearings on the presidential election outcomes. If there has been a recession during the year or two before the election, the incumbent president has tended to lose. If there were no recession during that time, the incumbent tended to win. In fact, the economy has incredibly predicted the winning president every year going back to President Calvin Coolidge, when he won despite a recession within two years of the election. But Coolidge inherited a recession when President Warren G. Harding passed away, and by the time people voted in November 1924, the Roaring ‘20s had started to take hold and the economy was strong again.

Markets tend to be volatile ahead of elections because of the uncertainty around possible policy changes. In this election, the stakes are particularly high for corporate America because a potential takeover of the Senate by Democrats and a possible Biden victory reportedly may lead to an increase in the corporate tax rate from 21% to 28% and unwind the corporate earnings boost the 2017 Tax Cut and Jobs Act delivered. Other areas to watch that could impact markets:

-

Financial regulation could tighten and potentially impact markets. Senator Elizabeth Warren is still in the running for vice president, which may be more negative for financials.

-

Healthcare should perform well regardless of the election outcome with “Medicare for All” off the table. Pressure to reduce drug prices is bipartisan.

-

Energy could be hurt by a potential Democratic sweep, but prices may get support from lower production and higher production costs. Green energy may be a priority.

Our analysis suggests the 2020 presidential race is still up in the air. If the economy continues to open up, a vaccine is on the way, and the massive stimulus continues to drive asset prices higher, President Trump’s chances may improve. A weak economy struggling to come out of recession and weaker markets would likely favor challenger former Vice President Joe Biden.

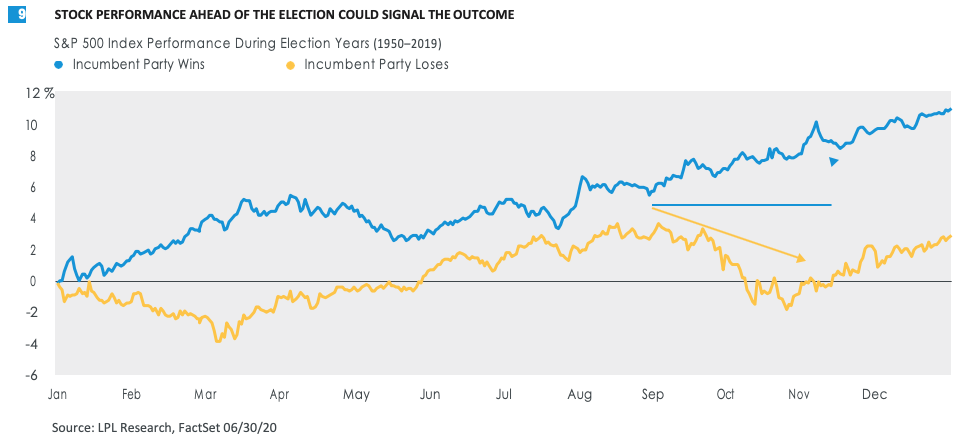

How stocks perform the three months ahead of the election has delivered a solid track record of deciding who will be in the White House the next January. The S&P 500 has predicted every presidential election winner since 1984, and 87% of the winners since 1928, with stocks favoring the incumbent party if stocks are higher in the three-month period before the election. As the chart shows, if stocks sell off ahead of the election, the opposition party has tended to win and the incumbent party has lost.

THE TRAIL AHEAD

The path of the economy and markets in the second half of 2020 may depend on how much progress we make against COVID-19. If recent evidence of potential economic recovery is a prelude of things to come, and stocks are accurately assessing a favorable growth outlook, then stocks may rally to new highs in the second half. Alternatively, in the event of a second wave of infections and renewed lockdowns, the economic recovery may stall, and stocks may be ripe for a correction following the strong gains off the March lows.

When uncertainty is high and markets are volatile, staying the course and focusing on the long term can be difficult. We would continue to view bouts of volatility as opportunities, when suitable, to rebalance portfolios toward long-term allocations.

This COVID-19 crisis has been one of the toughest we will ever face. By facing these challenges together with many heroes at our sides, taking advantage of opportunities in the markets, and focusing more on long- term objectives rather than bumps along the way, we can make decisions that may put us in better positions to seek our long-term goals.

GENERAL DISCLOSURES

The opinions, statements and forecasts presented herein are general information only and are not intended to provide specific investment advice or recommendations for any individual. It does not take into account the specific investment objectives, tax and financial condition, or particular needs of any specific person. There is no assurance that the strategies or techniques discussed are suitable for all investors or will be successful. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Any forward-looking statements including the economic forecasts herein may not develop as predicted and are subject to change based on future market and other conditions. All performance referenced is historical and is no guarantee of future results.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All index data from FactSet.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

GENERAL RISK DISCLOSURES:

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. Investing in foreign and emerging markets debt or securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

GENERAL DEFINITIONS:

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

EQUITY RISK:

Investing in stock includes numerous specific risks including the fluctuation of dividend, loss of principal and potential illiquidity of the investment in a falling market. Because of their narrow focus, sector investing will be subject to greater volatility than investing more broadly across many sectors and companies. Value investments can perform differently from the market as a whole. They can remain undervalued by the market for long periods of time. The prices of small and mid-cap stocks are generally more volatile than large cap stocks.

EQUITY DEFINITIONS:

Cyclical stocks typically relate to equity securities of companies whose price is affected by ups and downs in the overall economy and that sell discretionary items that consumers may buy more of during an economic expansion but cut back on during a recession. Counter-cyclical stocks tend to move in the opposite direction from the overall economy and with consumer staples which people continue to demand even during a downturn.

A growth stock is a share in a company that is anticipated to grow at a rate significantly above the average for the market due to capital appreciation. A value stock is anticipated to grow above the average for the market due to trading at a lower price relative to its fundamentals, such as dividends, earnings, or sales.

Large cap stocks are issued by corporations with a market capitalization of $10 billion or more, and small cap stocks are issued by corporations with a market capitalization between $250 million and $2 billion.

FIXED INCOME RISKS:

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. Bond yields are subject to change. Certain call or special redemption features may exist which could impact yield. Government bonds and Treasury bills are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate, and credit risk, as well as additional risks based on the quality of issuer, coupon rate, price, yield, maturity, and redemption features. Mortgage-backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

FIXED INCOME DEFINITIONS:

Credit quality is one of the principal criteria for judging the investment quality of a bond or bond mutual fund. As the term implies, credit quality informs investors of a bond or bond portfolio’s credit worthiness, or risk of default. Credit ratings are published rankings based on detailed financial analyses by a credit bureau specifically as it relates to the bond issue’s ability to meet debt obligations. The highest rating is AAA, and the lowest is D. Securities with credit ratings of BBB and above are considered investment grade. The credit spread is the yield on corporate bonds less the yield on comparable maturity Treasury debt. This is a market-based estimate of the amount of fear in the bond market. BBB-rated bonds are the lowest quality bonds that are considered investment-grade, rather than high-yield. They best reflect the stresses across the quality spectrum.

The Bloomberg Barclays Aggregate US Bond Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the US investment-grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

International debt securities involve special additional risks. These risks include, but are not limited to, currency risk, geopolitical and regulatory risk, and risk associated with varying settlement standards. These risks are often heightened for investments in emerging markets.

High yield/junk bonds (grade BB or below) are not investment-grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Municipal bonds are subject to availability and change in price. They are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply. If sold prior to maturity, capital gains tax could apply.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All