Opportunities and risk abound in the fixed income space as questions remain about whether or not the Fed will continue to tighten. With the long end of the curve starting to look appealing, but short end yields still being attractive, investors need to unpack how they are approaching the fixed income space. Join iMGP and VettaFi for a webcast that digs into how investors can capitalize on the return of fixed income.

Topics covered will include:

Top Silver Mining CEO: "On the demand side, it’s pretty phenomenal…"

The first step in winning the “war for talent” is understanding what your potential employees want.

As the debt ceiling fight in Washington heads down to the wire with the risk of a technical default looming, investors are growing nervous.

Rising rates in today's fixed-income markets have led to more attractive bond prices and higher yields, alleviating some of the challenges facing income investors.

Review the latest portfolio strategy commentary from Mike Gibbs.

What exactly does a trust company do to earn their fee that my family member or friend can’t do?

Over the last week, the market saw volatility pick up after approaching the upper end of what we believe is the near-term trading range.

How can advisors ensure that clients will keep their assets with you?

Tax-managed investing has gained in popularity in recent years. But what exactly is a tax-managed mutual fund? We do a deep dive into the concept.

Here are six compliance-friendly ways to incorporate social proof into your website to establish trust and capture new leads.

As interest rates show signs of peaking, gold prices are nearing new all-time highs.

Fears of bank runs precipitating a broader financial crisis helped spark a surge in bullion buying this week.

Review the latest portfolio strategy commentary from Mike Gibbs, managing director of Equity Portfolio and Technical Strategy.

We believe municipal bonds boast several key factors that position them as an attractive asset class in general, but especially so when markets are volatile.

Surveying your clients and prospects is essential, especially as we continue to confront a major shift in how we live our lives.

Northern Trust Asset Management (NTAM) is a leading global investment manager with $1 trillion in assets under management. It released “The Risk Report” late last year, which is an aggregated analysis of 280 institutional equity portfolios across the globe. The report revealed six common drivers of unintended investment results. As an investment manager that employs a quantitative risk-aware approach, NTAM regularly partners with investors and their consultants to provide them with a distinct analysis of underlying risk components impacting their portfolios’ ability to achieve intended outcomes. Of utmost importance to our Advisor Perspectives listeners and readers, the findings of the research are as applicable to portfolios managed by advisors for individual investors as they are to institutional investors. NTAM does indeed serve individual advisors through a number of offerings, including Northern Mutual Funds, FlexShares ETFs, and Diversified Strategist model portfolios. NTAM’s purpose in conducting the research behind the Risk Report was to help investors make needed adjustments consistent with NTAM’s core philosophy, which is that investors should get paid for the risks they take – in all market environments and in any investment strategy.

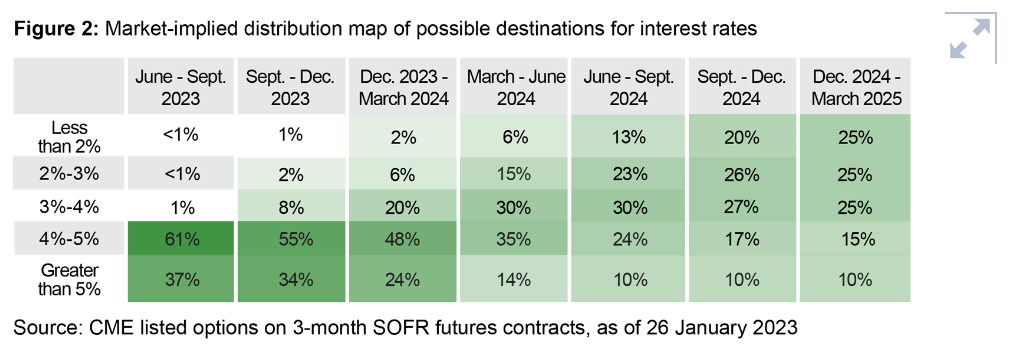

As investors seek to pinpoint market expectations for Federal Reserve policy, it’s critical to consider not just rate projections and derivatives pricing, but the degree of uncertainty and distribution of outcomes.

It is a challenge to design a website that addresses the needs and questions of multiple client types.

As investors hope for a Santa Claus rally in the days ahead, the Grinch is looking to steal their holiday cheer.

As warning signs for the economy mount, investors are cheering for more bad news. That's because they expect economic weakness will force the Federal Reserve to stop raising interest rates and eventually re-embrace loose monetary policy.

A hybrid model that combines sophisticated digital capabilities with human expertise and advice is not just today’s reality but will be a key differentiator for winning customer relationships.

Precious metals investors remain cautious following the Federal Reserve’s latest jumbo rate hike.

As investors weigh conflicting economic data and the prospects for a Fed pivot, precious metals markets are quietly basing out.

I cannot emphasize enough the importance of including a conversion page in a site build.

Is a recession lurking around the corner in 2023? If so, how might it impact defined benefit (DB) plan sponsors—and what steps, if any, should they consider taking?

As new inflation data pushes the Fed toward continuing with rate hikes, precious metals markets are struggling to make headway.

Precious metals markets are trying to tough this week despite another large rate hike by the Federal Reserve.

There are typically two approaches that I take for promoting a podcast on an advisor’s website.

Since the global financial crisis, assets in private credit have grown exponentially as investors search for yield while protecting against inflation and rising interest rates.

Since the global financial crisis, assets in private credit have grown exponentially as investors search for yield while protecting against inflation and rising interest rates. Once a small corner of the investment universe, private credit has boomed into a major asset class that does not show signs of slowing. Over the 2010-2020 period, assets grew by 12.8% annually. However, not all private credit is created equal. My guests today will explain how the private credit landscape is quite diverse relative to its publicly traded counterpart, and investors should take time to fully understand the differences within the space.

Your firm’s digital messaging and visual expression must all align with your ideal clients’ needs, goals and objectives. Here is how four top advisors achieved that goal.

Join us to discover why private credit is an attractive alternative for enhancing portfolio exposures and the role interval funds can play in accessing this coveted asset class.

From 2008 onward, U.S. market returns have been strong and consistent, and 2021 was no different, with the S&P 500 returning a solid 29%.

American families are feeling the financial squeeze of soaring inflation and a persistent pandemic as fractious Democrats return to Washington this week no closer to a deal on a tax and spending bill party leaders hoped would by now provide relief.

Ask yourself these questions when seeking a trust partner who not only is committed to a partnership service model, but can also deliver.

Here’s how advisors can maximize their event marketing ecosystem to drive more appointments from their in-person and digital events.

Given the inherent volatility of small capitalization stocks, even small differences in benchmarks can affect relative returns. Investors should be aware of the composition of the index used to define the opportunity set when comparing performance.

As the world becomes more digitally connected, cybersecurity’s role in business, technology, and society has become mission critical. Simply put, the modern world is built on cybersecurity. Without it, capital cannot flow freely, information cannot be stored safely, and businesses, governments and critical infrastructure cannot operate securely. Hear from CrowdStrike, a leading cybersecurity company, along with the Consumer Technology Association (CTA), and First Trust on noteworthy trends in cybersecurity as well as the importance of the cybersecurity investment theme. The Nasdaq CTA Cybersecurity Index (NQCYBR) is tracked by the world’s largest cybersecurity ETF, the First Trust Nasdaq Cybersecurity ETF (CIBR).

The index is comprised of cybersecurity companies, classified by the Consumer Technology Association (CTA), this index provides investors with a way of tracking and accessing this critical theme.

Meatpackers are in the crosshairs of U.S. lawmakers including traditional allies as ranchers complain that beef processors are abusing market power to gain out-sized margins at their expense.