The last 20 months have taught us to question everything. What is the future of work? Can American democracy survive? Will Baby Boomers keep consuming more than their fair share? And what comes after “trillion”? Howard Marks’s latest memo examines paradigm shifts that could reshape the economy, markets and the world for many years to come.

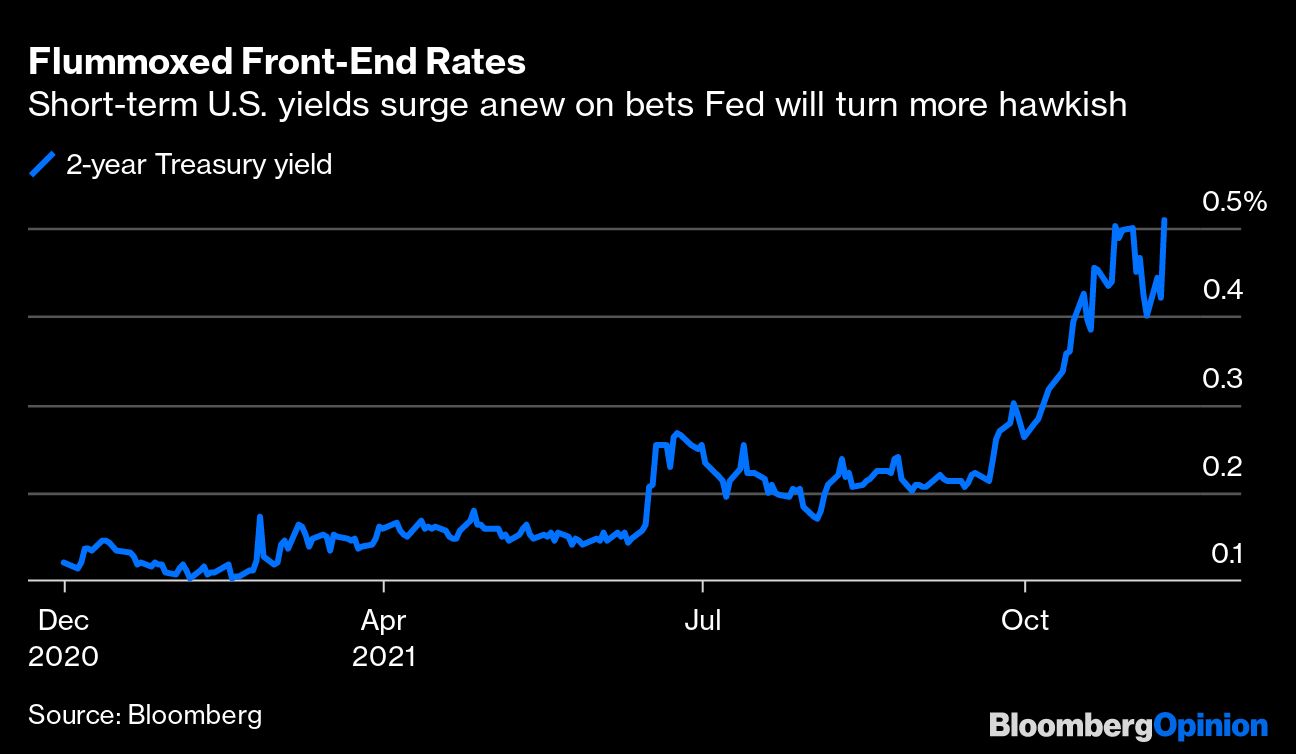

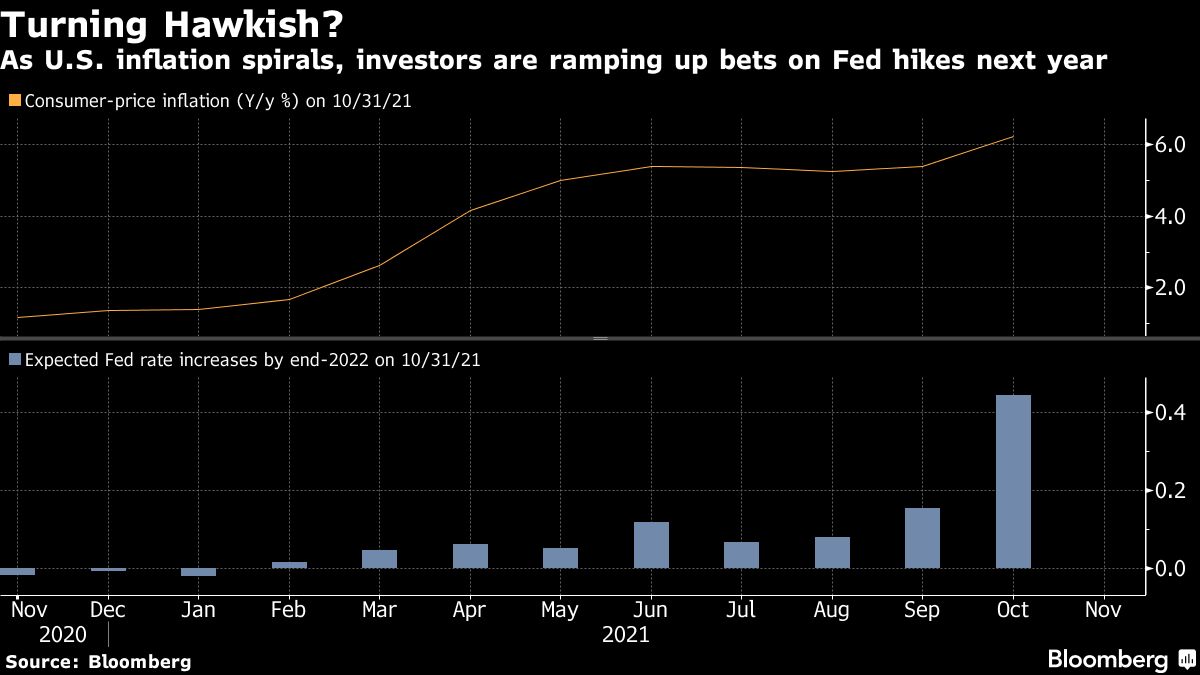

The surge in U.S. inflation is sending some of the biggest names on Wall Street into rethink mode, forcing them to recalibrate strategies that depended on bonds as a shock absorber against equity downturns.

Enjoy the latest Newsletter from Harold Evensky.

Bankers are repackaging everything from fast food franchises to fitness-center fees into bonds at the fastest clip since the global financial crisis as investors chase yield and inflation protection.

A high tide of growth, aided by a sea change in fiscal policy, is likely to help float the global economy safely over the rocks of risks in 2022, despite waves of worries emanating from COVID, inflation, shortages, and rate hikes.

Moderate inflation can be good, especially for some value stocks. Christian Correa breaks down why investors should not be afraid of the current inflationary or rising rate environments and explains how they can actually help some businesses and areas of the equity market.

Current low yields and tight spreads in the municipal bond market have made it difficult for investors to find opportunities to earn attractive interest income on their investments. We expect that to change in 2022.

It was another tough week in a brutal year for bears. Despite being right about many aspects of inflation, monetary policy and the persistence of the coronavirus, equity bears who were expecting anything to put a meaningful brake on the stock market were again denied.

There are certain features of valuation, investor psychology, and price behavior that emerge, to one degree or another, when the fear of missing out becomes particularly extreme and the focus of speculation becomes particularly narrow. We’ve suddenly hit a motherlode of those conditions. Emphatically, this is not a forecast. It's a statement about current, observable conditions.

In some simplistic economic theories, shortages never happen. Supply and demand for any particular good are always perfectly balanced in a given time and place. If you can’t get what you demand at that moment, you pay a higher price or you demand something else.

Thanksgiving is the time to reflect on all we are grateful for, and given the strides the economy and markets have made over the last year, we have a cornucopia of blessings to count! Between the economic expansion and the S&P 500 up 27% year-to-date, there is quite a long list.

Bill Zox and John McClain, portfolio managers with Brandywine Global, join Amer Hasan to discuss how current market and economic conditions could benefit high yield investors, the opportunities and risks right now, and why the asset class is often overlooked or misunderstood.

With major central banks likely to exercise patience in the face of price pressures, inflation-linked assets may be attractive allocations.

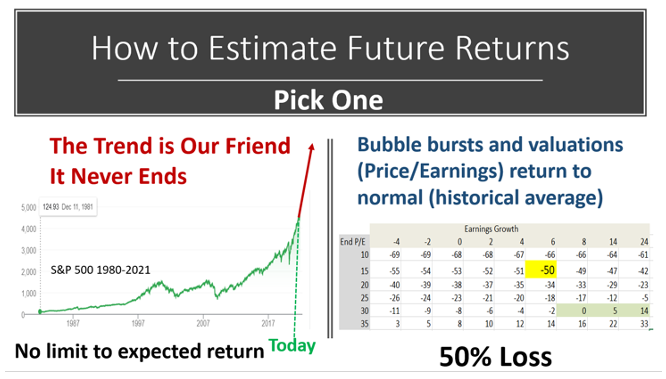

Inflation is why the 4% rule never made any sense.

Portfolio manager Michael Fredericks reflects on markets and investing to generate income while managing risk over the last decade.

With a new Prime Minister taking the helm in Japan, what does the future hold? Franklin Templeton Investment Solutions’ Gene Podkaminer and members of the research team take a look at both local and global trends influencing Japan—and why investors should pay more attention to the country.

With the right approach, advisors are well-positioned to identify the funds that will best suit their values-focused clients – even without standardized guidelines for what makes a sustainable fund sustainable.

Treasury Secretary Janet Yellen said she’ll be updating Congress “within the next day or two” on how long lawmakers have to raise or suspend the debt limit before the government runs out of cash.

In 2013, the mere mention by the US Federal Reserve (Fed) that the scaling back of asset purchases could be forthcoming caused significant short-term disruptions to the global financial markets. Currently, the Fed is once again poised to scale back its asset purchases as the US economy has recovered from the latest recession. Investors are concerned that a shift in Fed policy will have an outsized impact on markets.

In this webinar you'll learn:

A rule of thumb for how much U.S. retirees can “safely” withdraw each year without fear of outliving their savings just got a haircut.

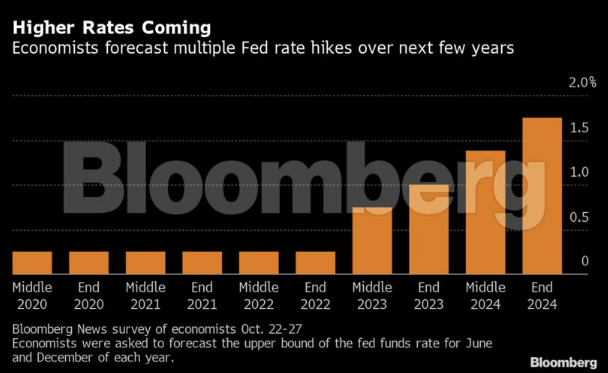

A growing chorus of market watchers is saying the Federal Reserve may have to speed up its reduction of asset purchases in light of the fastest inflation in 30 years.

Gold edged lower as investors assessed new economic data from China and the outlook for global inflation.

As investors and financial advisors approach the end of 2021 and consider their annual recalibration of portfolio mix for the coming year, they would be prudent to factor in some difficult economic realities that can no longer be ignored–that will alter stock and bond performance into and well past 2022.

The receding pandemic should continue to provide a tailwind. However, as economies begin to normalize, expectations for the future path of monetary and fiscal policies are shifting. And as markets adapt to a post-Covid economy, we expect increased volatility, more rotational markets, and leadership changes. The risk of a policy error has also increased at the margin, with future Federal Reserve leadership and policy more uncertain today than a month ago.

Expected returns are derived in two distinct ways: from Federal Reserve actions, since it is manipulating bond prices, and from momentum, which is driving stock prices. How long can both last?

New research shows that aggressively easy monetary policy has driven asset flows to high-yield corporate bonds. Those bonds now offer poor risk-adjusted returns and have made certain interval funds more attractive.

As much as last year centered around the Covid-19 pandemic and its impact on the economy, the major topic of discussion in the financial markets this year has been centered around inflation, and its prospective impact on monetary policy.

I am writing in the middle of a whirlwind week in New York. We are going to discuss what I’m learning, some takeaways from the conversations I’ve had, changes in my personal portfolio, and thoughts around the topic of the day: inflation. As well as a few random things that I have read this week. All delivered to you within my 3,000-word limit. Let’s jump in…

Gold performed as expected this week following a monster CPI report that showed inflation skyrocketing 6.2% in October. The yellow metal broke out of its downward trend going back to August 2020, when it hit its all-time high of $2,073.

A look at the predictive prowess of treasuries in gauging the stickiness of inflation.

The bonds that held market expectations and central bank policies closely together during the COVID-era are starting to break. BlackRock's quant bond experts discuss the latest developments in inflation dynamics, liquidity in the financial system, and changes in China's policy reaction.

For much of this year, rising inflation has been bad news for gold. Now it’s giving the metal a shot in the arm.

The Federal Reserve tried so hard to avoid a repeat of the 2013 “taper tantrum” — and was so successful in doing so — that it might just end up backfiring in a big way.

After U.S. prices climbed by the most in three decades, there’s even worse news ahead for households and policy makers: Inflation likely has further to rise before it peaks.

When the Federal Reserve released its semiannual financial stability report in May, I wrote that the central bank came as close as it could to saying “bubble.” So imagine what it could have said in its latest update, which was released on Monday.

Speculative psychology is the only thing standing between an hypervalued market that continues to advance and a hypervalued market that drops like a rock. Our best gauge of that psychology - the uniformity of market internals - remains divergent enough to keep market conditions in a trap-door situation.

Transitory or not, the current inflation rate has many investors concerned. A look back in history can put today’s situation in perspective.

Interest rates were mixed in October, as shorter maturity yields rose while longer maturity yields fell. The dramatic flattening in the yield curve reflects the market expectation that the Fed will begin tapering its bond purchase program imminently and has pulled forward expectations for rate hikes once the taper is completed.

Supply-chain jams are leading to congestion at ports around the world, keeping prices elevated.

There are at least three approaches that have been demonstrated effective in identifying skill in asset managers, offering investors the likelihood of superior future performance.

When rates are rising, investors need portfolio protection. But it’s no time to sit idly in cash and wait things out. Every day spent on the sidelines means income and opportunities lost. A passive, set-it-and-forget-it investing approach isn’t ideal either. Buy-and-hold laddered portfolios tend to lock in low yields that disappoint if the market begins to offer more.

This week Jerome Powell tossed the market a bone by hinting that the Fed would be patient in raising short-term interest rates due to the continued slack in the US labor market and inflation that would likely be “transitory”.

Inflation is looking less and less “transitory,” and make no mistake: Transitioning to a zero-carbon energy mix as quickly as climate scientists are urging will be highly inflationary.

The longest wait in the modern era for news about who will chair the Federal Reserve is triggering debate in financial markets about the impact of any unexpected replacement of Jerome Powell at the helm.

How annuities can help shoulder RMD burdens in a market drawdown.

The Federal Reserve navigated its tapering announcement without much market volatility, but faces the challenge of managing rate expectations amid elevated inflation risks.

Chair Jerome Powell and the Fed had been holding the market’s hand in the lead-up to the tapering decision, making it abundantly clear that a decision was imminent at today’s meeting and effectively pre-announcing all of the relevant details of the decision...

In March 2020 the Federal Reserve was able to use old and new tools to manage the unimaginable – a Pandemic. The Fed stabilized the Treasury bond market and the municipal bond market through its purchases and back stopped government loans to small and medium sized businesses to keep them from going under.

Federal Reserve Chair Jerome Powell said officials can be patient on raising interest rates -- after announcing a start to reducing their bond purchases -- but won’t flinch from action if warranted by inflation.

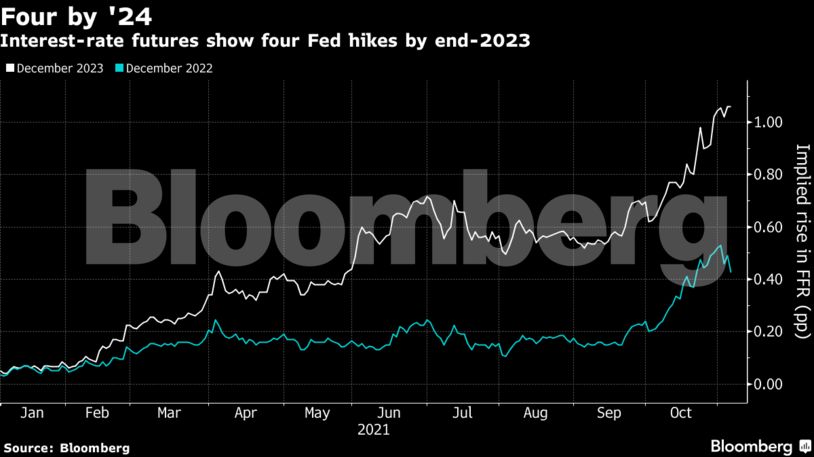

Investors are increasingly betting that the Federal Reserve will have to raise interest rates sooner than previously expected to keep inflation in check. A few months ago, futures prices implied that “liftoff” from the current near-zero level wouldn’t occur until 2023 or later; now they suggest it’ll happen near the middle of next year.