For American consumers wondering who's profiting from the run-up in food prices, it’s instructive to spend a few hours at Rob Tate’s Minnesota farm. Because he wants everyone to know that it sure isn’t him.

A high school reunion can be a revealing thing.

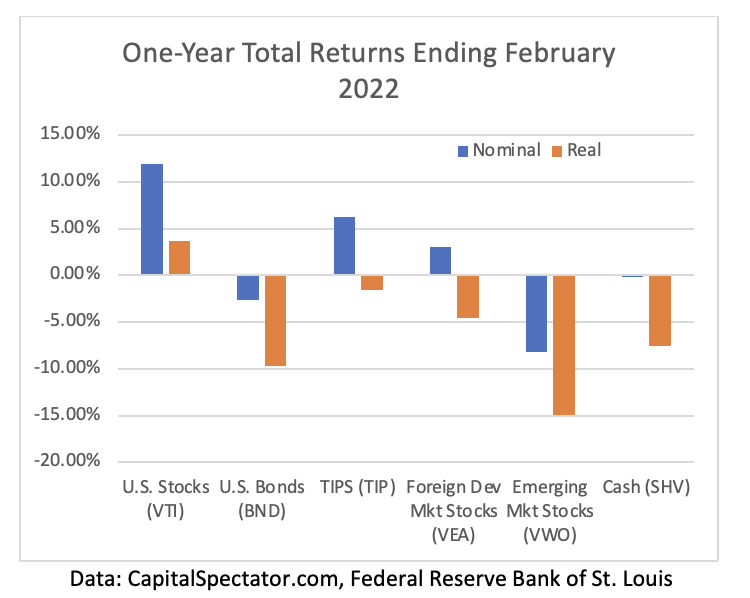

If higher inflation persists, at least two mechanisms represent an ongoing risk to achieving expected real portfolio returns: Inflation will erode nominal returns and it will inflict a tax drag on assets.

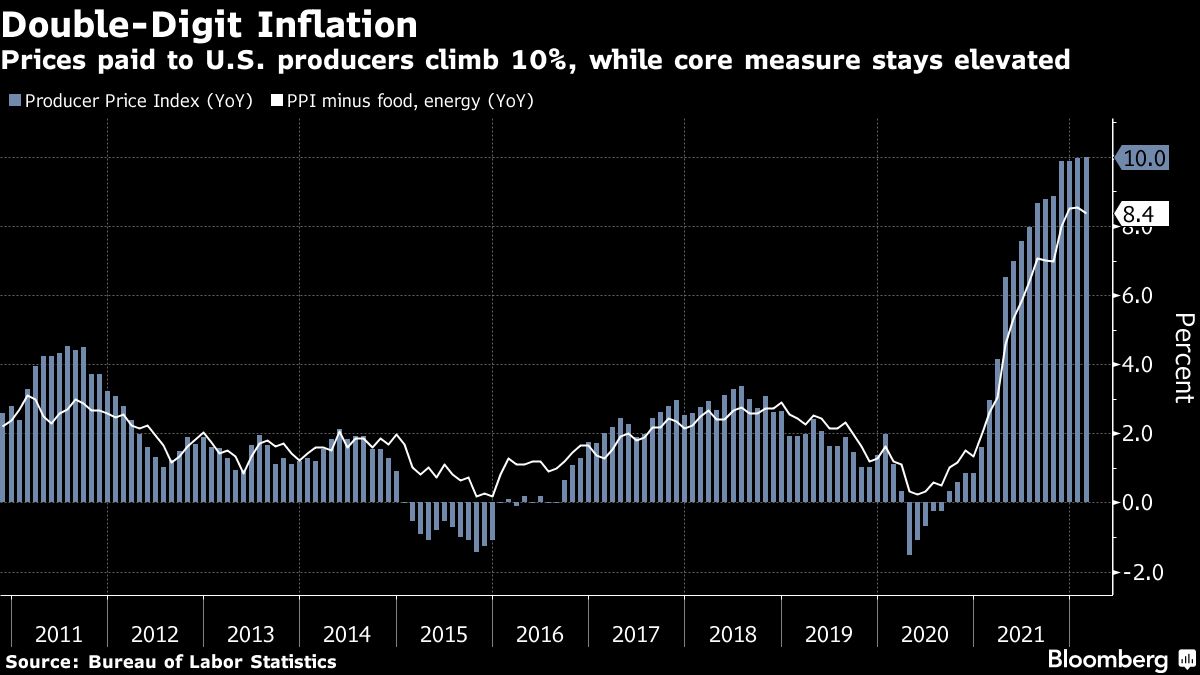

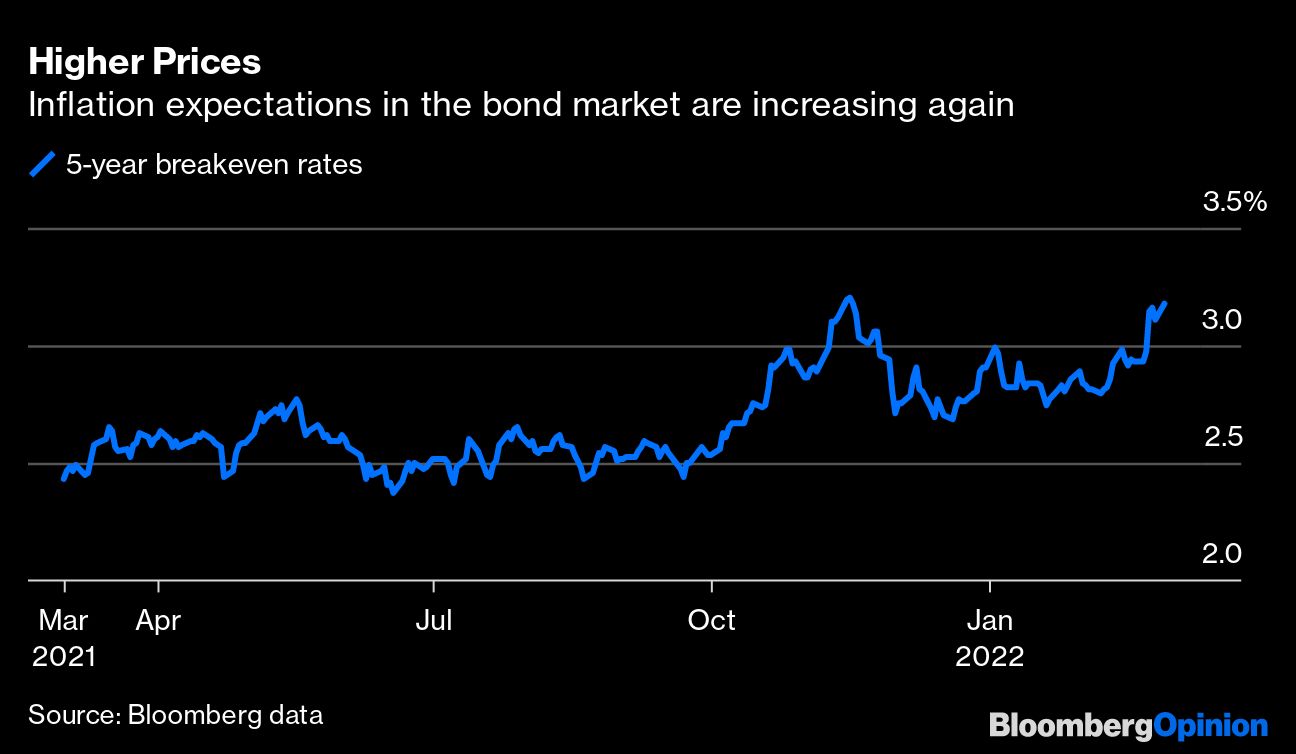

Prices paid to U.S. producers rose strongly in February on higher costs of goods, underscoring inflationary pressures that set the stage for a Federal Reserve rate hike this week. The producer price index for final demand increased 10% from February of last year and 0.8% from the prior month, Labor Department data showed Tuesday. That followed an upwardly revised 1.2% monthly gain in January.

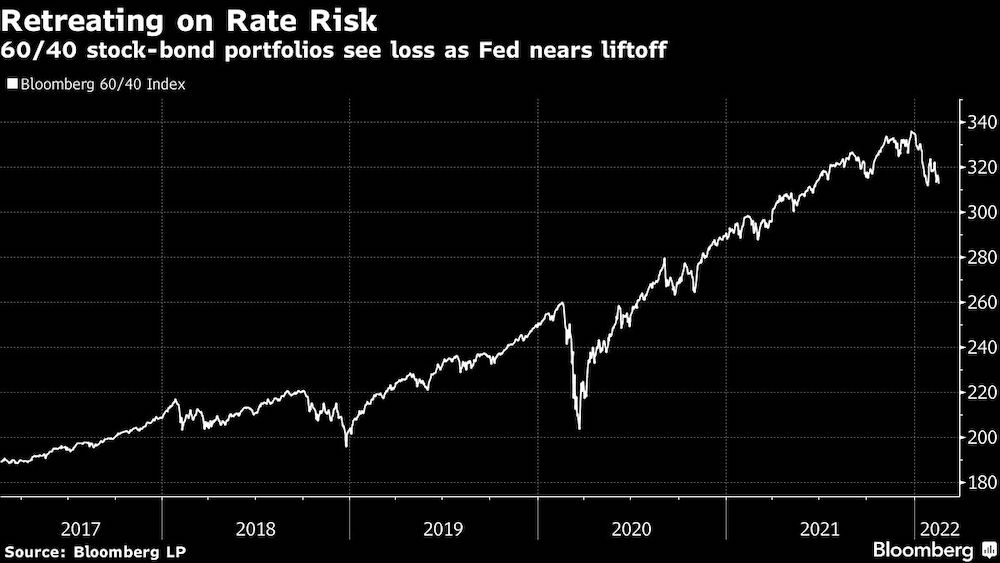

The classic 60/40 portfolio -- a strategy named for the share allocated to equities and high-grade debt, respectively -- is down more than 10% this year, leaving it on pace for the worst drubbing since the financial crisis of 2008.

The Russian invasion of Ukraine overturned a lot of assumptions about the near-term direction of the global economy.

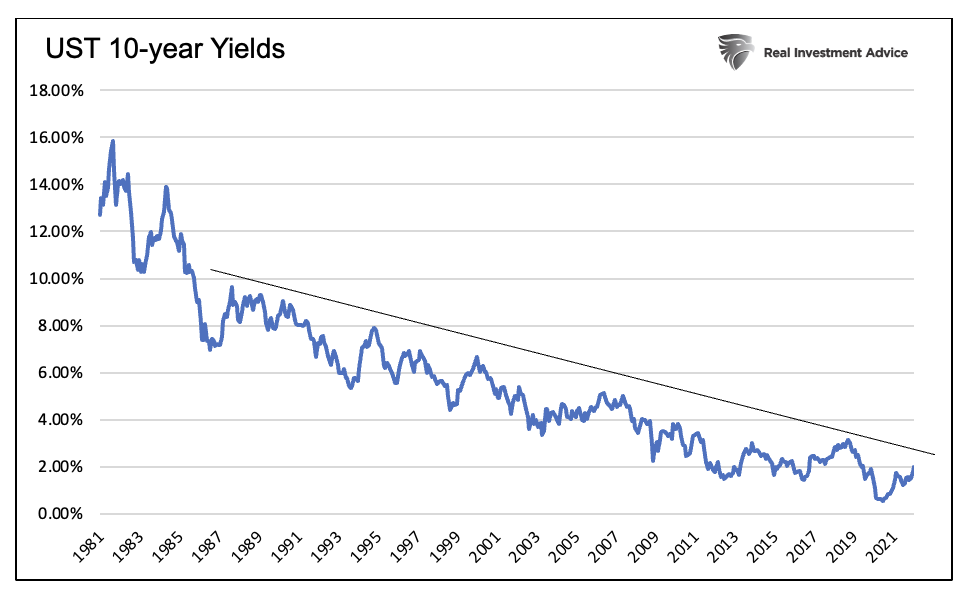

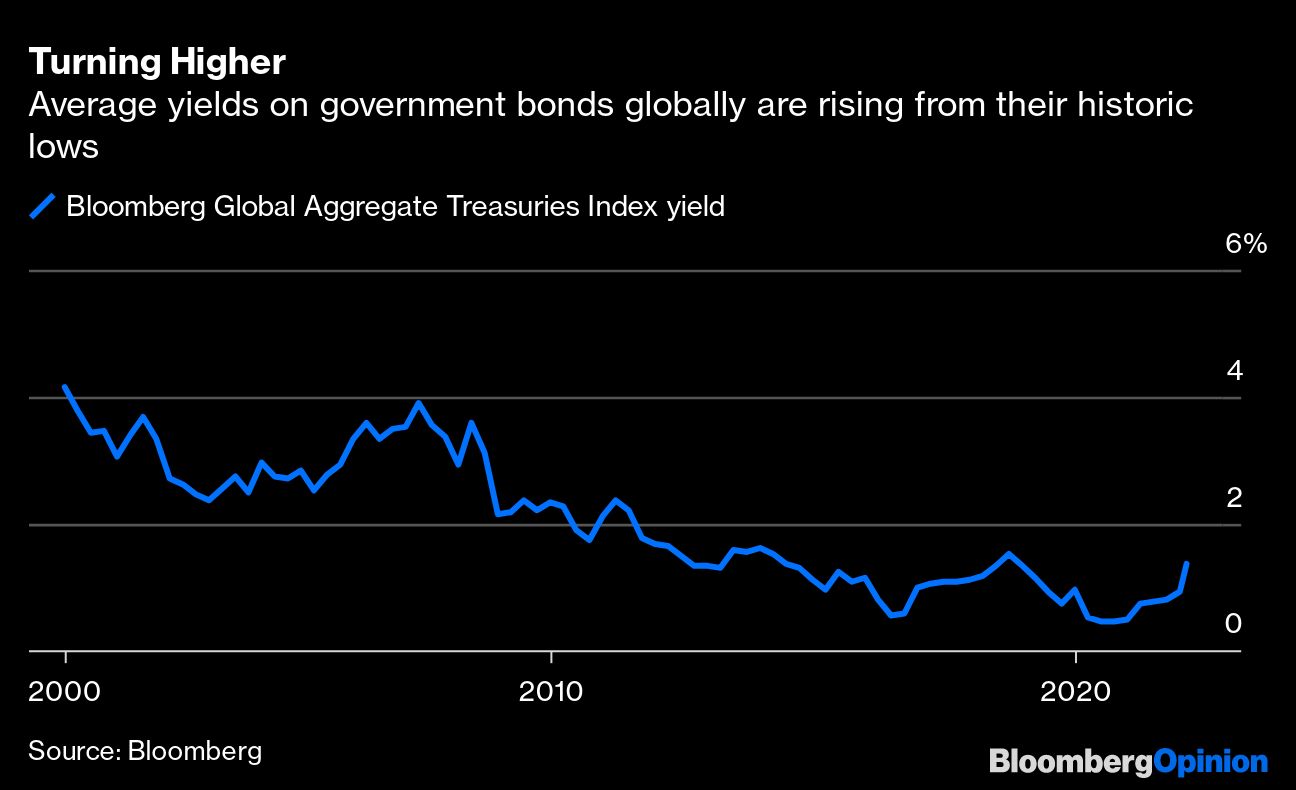

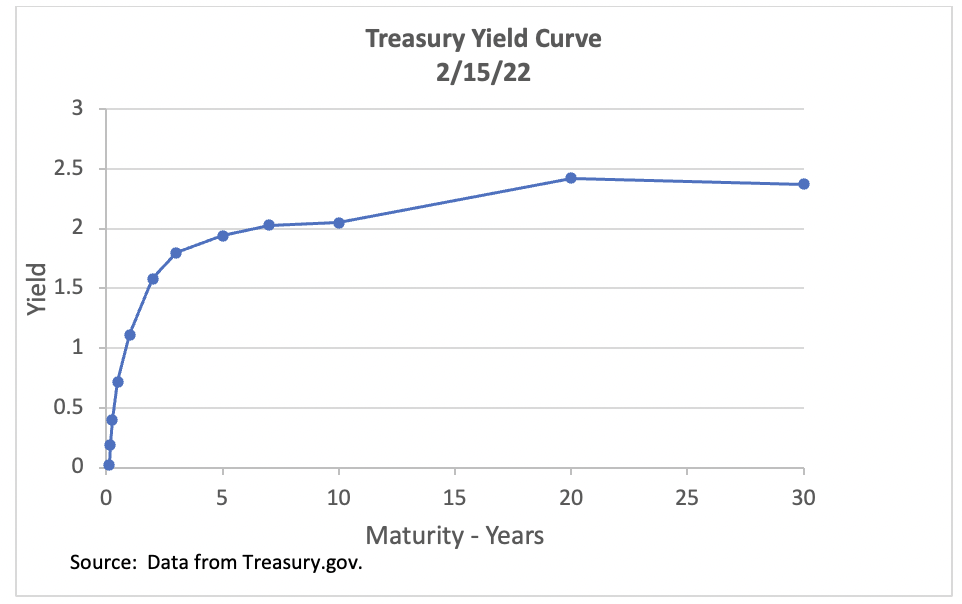

The surging volatility in the world’s biggest bond market is challenging traders trying to play both tighter global monetary policy and a war-induced commodity price shock that’s raising the specter of 1970s-style stagflation.

When market volatility goes up, investors increase their investments in volatility strategies that they deem as capable of yielding the most lucrative returns.

All geopolitical crises, including the current one, present three timeless lessons investors would be wise to heed.

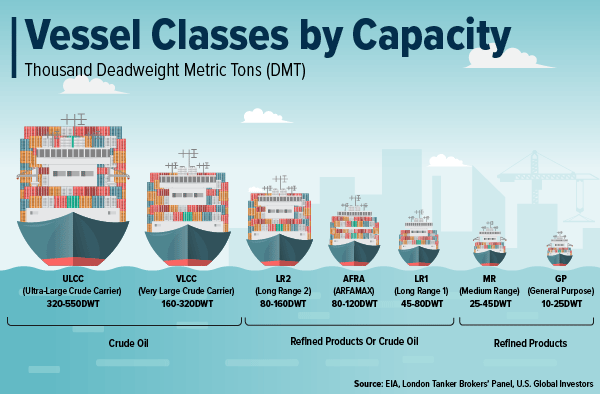

A provocative report by Credit Suisse’s Zoltan Pozsar that was making the rounds in certain corners of Twitter this week suggests that the Russia-Ukraine conflict could be a strong tailwind for shipping freight rates.

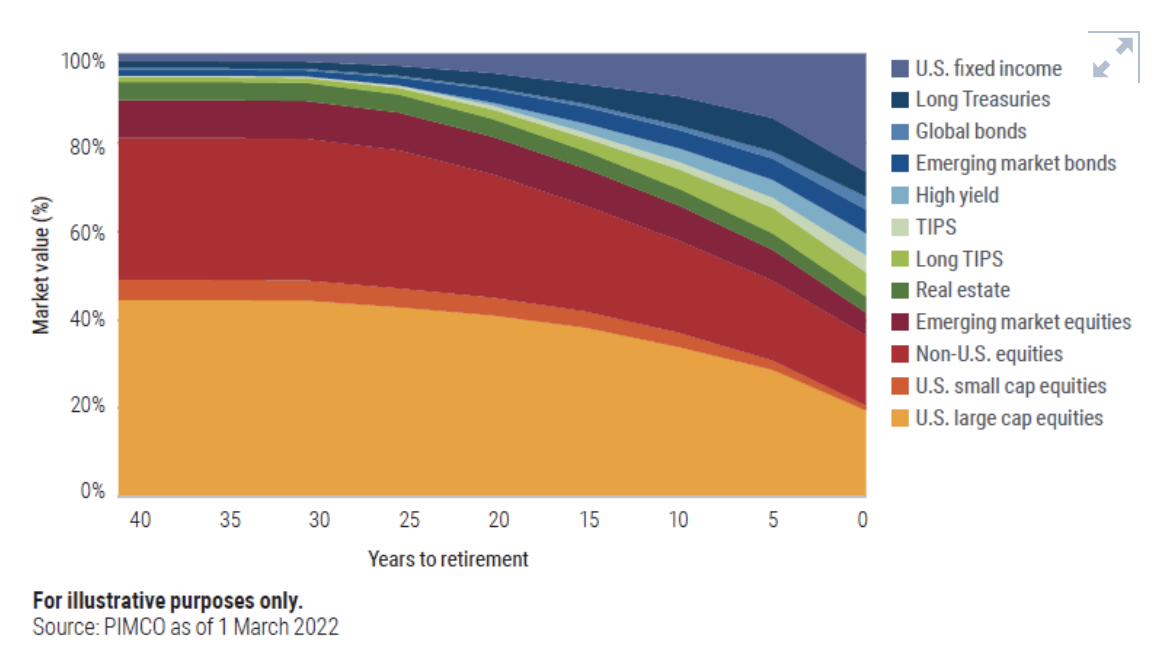

PIMCO’s glide path for target date funds expresses the firm’s collective view on age-appropriate asset allocation that can help prepare defined contribution (DC) plan participants for successful retirements.

In economics, “Guns or Butter” compares the impact of government spending on defense and non-defense categories. The Russia invasion of Ukraine has implications for investors and categories associated with defense, energy and industrials. Sectors deemed in the national interest should benefit from better appropriation, less regulation and bipartisan support.

What happens when you combine the tipping point of two deflationary forces—globalization and demographics—with a pandemic, epic supply-chain disruptions and an invasion in Europe? Inflation of a magnitude not seen since the 1970s. Some of the contributing factors may be transitory, but not all, and lingering inflation is likely to be higher than before. How should bond investors adapt?

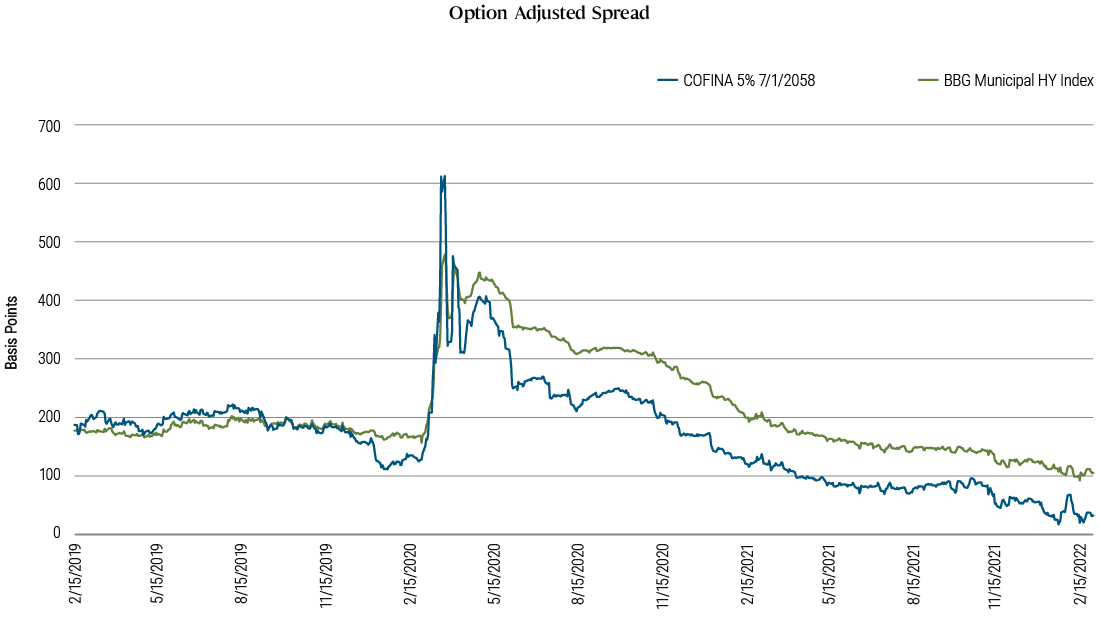

Restructured debt has often outperformed the broader municipal bond market as issuers emerge from bankruptcy with higher debt-servicing capacity.

Gold fell from near a 19-month high as risk sentiment improved, despite ongoing concerns that the fallout from Russia’s invasion of Ukraine will further fuel inflation and hurt economies.

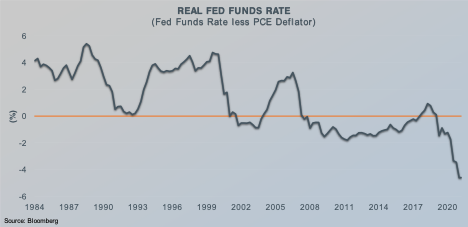

Headline inflation will breach 9% this year, according to Jeffrey Gundlach. That will force the Fed to aggressively raise the Fed funds rate.

Over the last 10+ years, U.S. equity outperformance has been caused by increased profit margins, the accretive impact of share buybacks, dollar weakness, and most significantly, an outsized expansion in equity multiples. There are risks to all of these sources of outperformance, suggesting that a neutral long-term strategic allocation to U.S. equities is now likely warranted.

The war between Russia and Ukraine—and subsequent economic and financial ripple effects—has exacerbated stress in global markets and ushered in an acute risk-off environment.

When an iceberg comes into view, investors must be wary of the danger, but Rick Rieder and team argue that it's also important to recall that calmer seas may lie beyond.

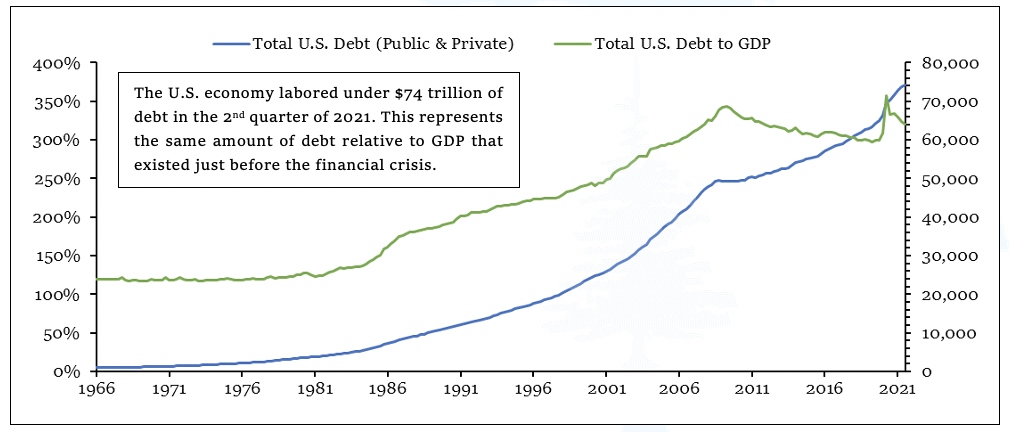

When it comes to the Federal Reserve and monetary policy, there are no shortages of talking heads who say the central bank can’t raise interest rates too much or else it would trigger a “debt bomb.”

The 60/40 stock/bond allocation is ubiquitous, but that’s stupid because it’s just not right for everyone, especially baby boomers.

I don’t believe the world has ever witnessed such a highly synchronized effort to ostracize a nation and isolate it from global markets. The steps have so far been deep and profound.

Today we’ll start what I’m sure will be a series of letters on Change2. I’ve said for some time the 2020s would be a turbulent period leading to a much better 2030s. I still believe that. I also believe the events we’re watching right now will define what that new order will be.

In this interview, Peter Essele, vice president, investment management and research, at Commonwealth Financial Network, explains why investors should view the volatility created by the pandemic and geopolitical events as an opportunity to add risk to their portfolios.

Given the war in the Ukraine, I thought it would be helpful to provide insights for advisors and investors to think about risk and what if any actions should be considered.

After living through more than two years of COVID-19, its variants, and the attendant supply-chain disruptions and inflation concerns, one thing is clear: Uncertainty is the only certainty.

“Geopolitical Risk” could well be a reason for the Fed to slow-roll tightening monetary policy in March.

Commodities appear attractive amid elevated inflation, lingering supply-demand imbalances and high roll yields.

Investors with short-term goals — such as buying a house in the next five years or paying college tuition — are generally advised against putting their funds in the stock market, since there might not be enough time for a portfolio to recover after a market sell-off. If you do have a significant chunk of your short-term savings in equities, you should be reviewing them with a view towards minimizing risk.

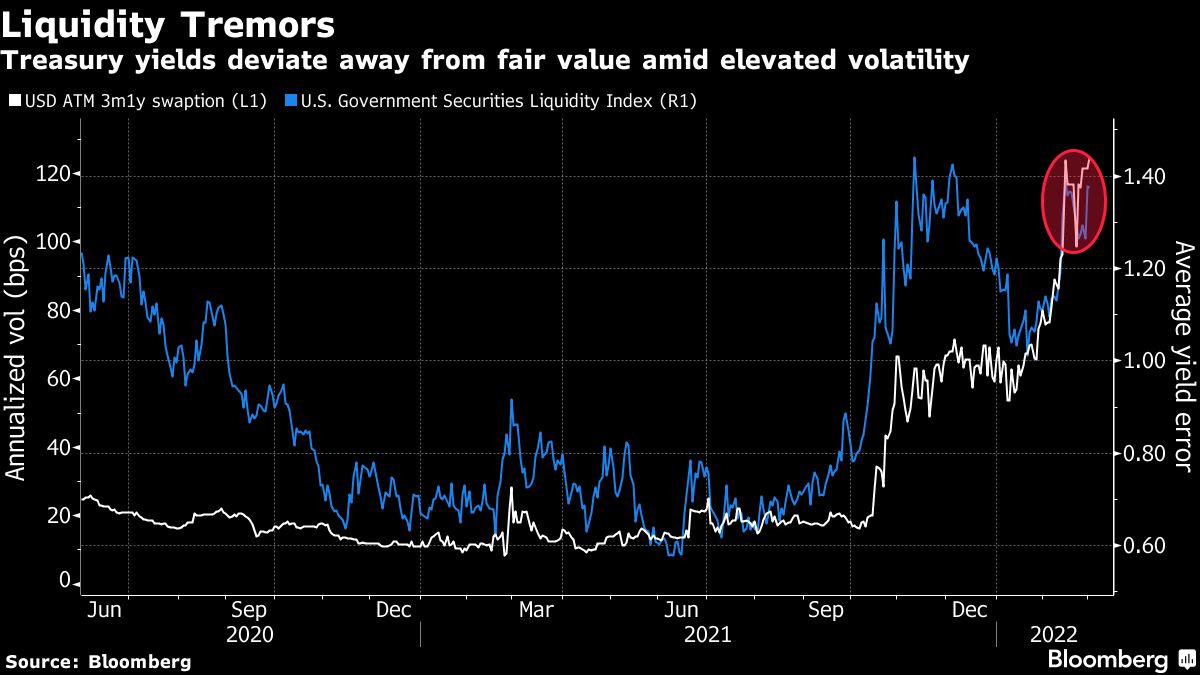

The rush into Treasuries sparked by Russia’s war in Ukraine has exposed fresh signs of weakness in the world’s biggest bond market, adding to pressure on U.S. regulators to detail a reform plan.

Finding attractively valued and high-yielding investments is difficult in the current market and economic environment.

The story of the Banque Royale and the Mississippi Bubble in the first issue of the Macro Value Monitor may sound like a tall tale of financial fiction, but those events did in fact occur three centuries ago in France.

The bond market is dialing back expectations for how quickly and steeply the Federal Reserve will raise interest rates as Russia’s war in Ukraine threatens to exert a drag on global economic growth.

This paper tracks the evolution of the emerging markets asset class and describes some of the resulting unique characteristics that make a value investing discipline attractive in these markets today.

The combination of high U.S. inflation and Russia’s invasion of Ukraine has discombobulated U.S. markets. From Friday to Monday, traders effectively reduced the number of expected rate increases by the Federal Reserve to six from seven by next February, even though, by most accounts, the inflation outlook has only worsened.

Here are some creative features to add to lazy, unappealing job postings so you can poach talent from your competitors.

The Rest of the Story was a radio show that aired from 1942-2008. Host Paul Harvey revealed little known facts that were previously not reported. The rest of the Federal Reserve story is that it is just pretending to be in control, and the rest of the Russian invasion story is about China and the U.S. dollar.

Yale Professor Robert Shiller’s Cyclically Adjusted Price-to-Earnings ratio (CAPE) is a respectable predictor of the future real return of the stock market, but it underwhelms when used on its own to set stock exposure. We examine a better way of using CAPE, with much better results.

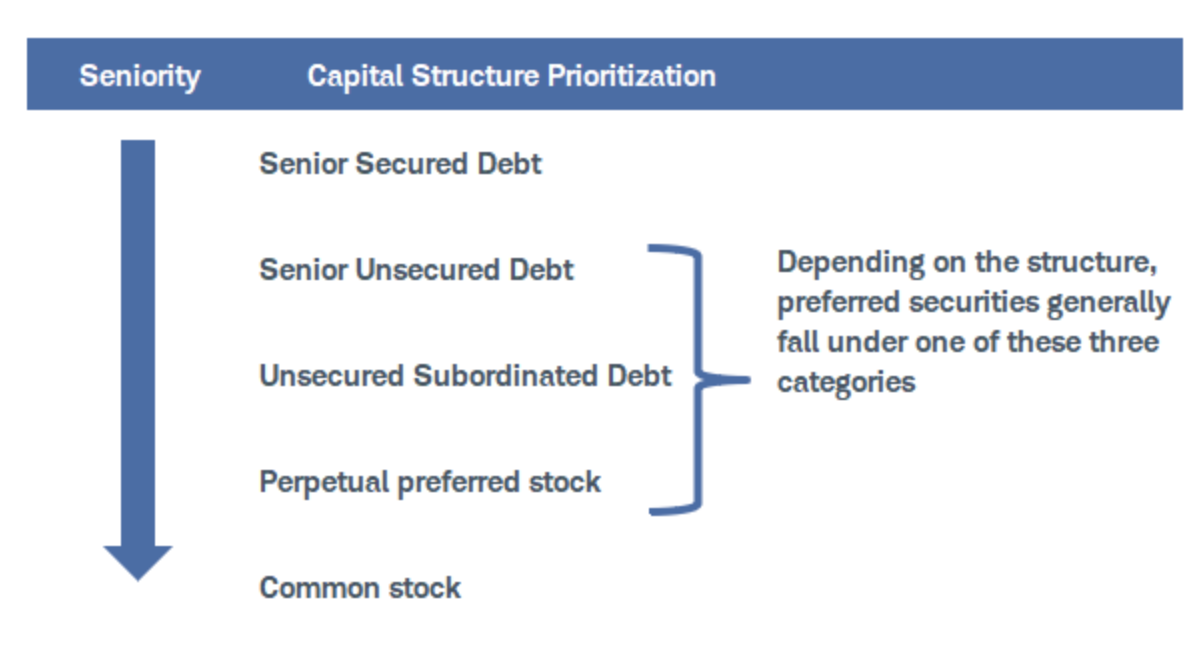

Preferred securities are a type of investment that generally offers higher yields than traditional fixed income securities, such as U.S. Treasury securities or investment-grade corporate bonds.

The 2022 investment year is now well underway and financial advisors and investors would be well advised to not, as the old saying goes, “fight the tape” of what is shaping up to be a difficult year for the stock market.

As we turn over the page to a new year, there are plenty of decisions that investors will need to make.

The “holy grail” of value investing is the only important “margin of safety.”

I propose a strategy that can produce larger price gains or losses than bonds and higher yields than traditional bond funds or ETFs. If yields decline soon, investors can expect double-digit returns in a relatively short period.

When it comes to investment returns, most people, including those who work in financial markets, only consider nominal numbers. For example, they look at the price of the S&P 500 Index now, where it was a year ago and work out what the total return was including dividends in that period.

Cryptocurrencies may be all the rage, but good luck figuring out how they fit in a portfolio.

Advisors can choose from five approaches to meet their clients’ income needs in retirement, each with its own merits and drawbacks. Those strategies attempt to solve for a central goal – ensuring that clients don’t run out of money – a risk that is illustrated by my wife’s catering business.

Advisors make seven predictably irrational mistakes when it comes to bonds, depleting their clients’ wealth and standard of living.

How much inflation is okay? People have different answers. I think it should be very low, but definitely positive to forestall deflation. Whatever your ideal may be, there’s a range of possibilities that would at least satisfy you. Political scientists call this range the “Overton Window,” a hypothetical box around the limits of acceptable policy. Anything outside the box is, by definition, unacceptable.

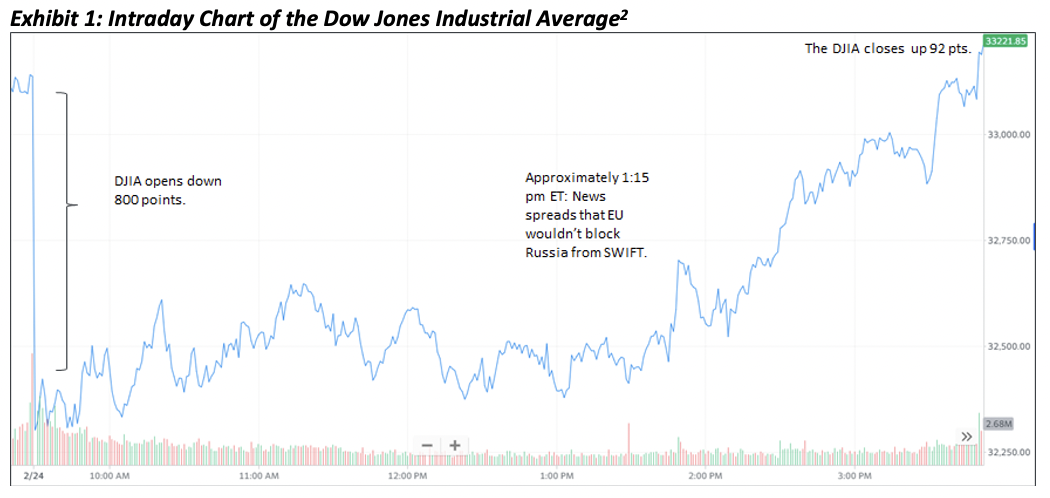

U.S. and global stocks fell sharply Thursday amid fear of a potential Russian invasion of Ukraine and ongoing concern about inflation.

There have been roughly 100,000 Russian troops on the border of Ukraine for about a year now. This is not a new development. What is Putin's main goal and how is all of this impacting equity markets?