The Five Strategies for Retirement Income

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisors can choose from five approaches to meet their clients’ income needs in retirement, each with its own merits and drawbacks. Those strategies attempt to solve for a central goal – ensuring that clients don’t run out of money – a risk that is illustrated by my wife’s catering business.

The thing that surprises me most about my wife’s business is how much food is leftover. I often ask, “Is there a better way to manage food costs?” and her answer is always the same: “Better to have food leftover than fall short.” She has the exceptional ability to estimate the amount of food each person will eat, but she can never be sure how many people will come and how much they will eat.

When planning for retirement, we also don’t want to “fall short.” To make sure, we must account for a multitude of factors:

1. How much income do I need?

2. How long will I need the income?

3. What will inflation be?

4. How much do I want to leave for beneficiaries?

Answering those questions is a daunting task that financial applications try to model. However, no matter how good we are at answering them, there is one question that is impossible to answer ahead of time: the sequence of investment returns we receive in retirement. It is one of the most important factors in determining retirement success.

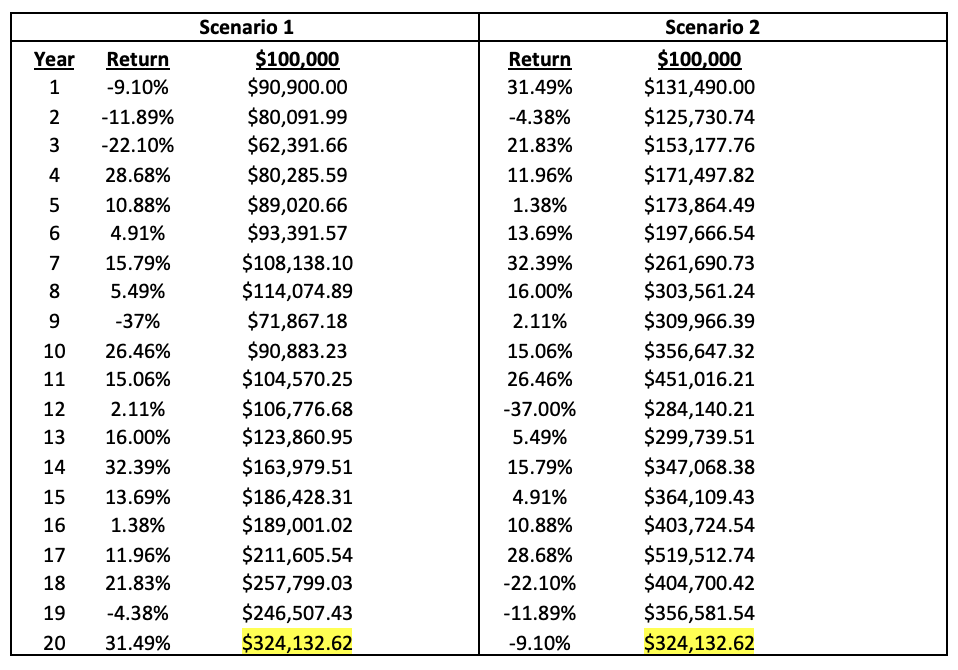

Sequence of returns is the order in which returns are realized. When we accumulate assets, the sequence of returns is of little consequence. To illustrate the point, let’s say you start out with $100,000 invested in stocks. In scenario 1, you experience negative returns at the beginning of your investment horizon, whereas in scenario 2 we flip the sequence so that the negative returns are at the end of the horizon.

For illustrative purposes only, not indicative of any specific investment product.

For illustrative purposes only, not indicative of any specific investment product.

Irrespective of which sequence we realize; the ending value is the same, with the average return in both scenarios being 6.05%.

But as we enter retirement, we must account for distributions, effectively changing the math. Using the same returns, let’s include a real income distribution of $50,000/year, assuming 2% inflation, from a starting nest egg of $1,000,000.

For illustrative purposes only, not indicative of any specific investment product.

For illustrative purposes only, not indicative of any specific investment product.

The “average” return in both scenarios is the same, but with vastly different outcomes. If we experience the negative returns upfront (scenario 1) we run out of money, a devastating situation in retirement. However, flipping the sequence (scenario 2) grows our nest egg to $1.6 million, begging the question, “Did we maximize income?”

This illustrates the importance of sequence of returns risk (SoRR) in retirement; the order of returns is more determinant than the “average” return. SoRR, longevity risk, and unexpected expenses are substantial factors in affecting a successful retirement. To address these factors a variety of strategies has been developed. They fall into five general categories, each with its own merits and shortcomings: certainty, static, bucket, variable, and insuring.

The certainty strategy

One strategy is to use a model that many institutions employ to fund their future liabilities, known as asset-liability management (ALM). You invest money today to meet a future liability with a high degree of certainty. For example, let’s assume one year from now we want $50,000 in income, and the current interest rate environment is 3%. Assuming the interest rate and principal are guaranteed, we could invest $48,545 ($50,000/1.03) today to meet that future obligation. However, this will not protect you from inflation. Alternatively, we could take $50,000 today and invest that into a one-year U.S. Treasury Inflation Protected (TIP) bond, thus covering the liability while also protecting it from inflation risk.

For all its certainty, there are drawbacks to this strategy. To make sure we don’t run out of money we would need to determine how many years to fund, an almost impossible task without having the foresight of our demise. Additionally, the strategy requires a very large upfront capital commitment, something most Americans are unable to accomplish.

The static strategy

If retirees lack the capital to fund the ALM strategy or are unable to calculate the duration of retirement, an alternative approach is to calculate a “safe” portfolio withdrawal rate. The seminal paper that discussed this strategy was William Bengen’s Determining Withdrawal Rates Using Historical Data. Using historical returns on a 50% stock/50% bond portfolio, he determined the optimal starting withdrawal rate to be 4%. Therefore, to sustain a real income of $50,000/year, you would need a starting nest egg of $1,250,000. Every year thereafter, you would adjust the previous year’s withdrawal for inflation.

As with any retirement income strategy, there are assumptions involved. In this case, Bengen assumed a 30-year retirement horizon and an annual rebalance back to the 50/50 portfolio. The challenge for retirees is rebalancing back into stocks after a large drawdown due to loss aversion, potentially derailing the strategy. Bengen’s “4%” withdrawal has been re-evaluated in follow-up papers and thus far has been shown to be an effective retirement strategy. However, with current elevated stock market valuations and low bond yields, some have recommended a slightly lower starting withdrawal rate.

The bucket strategy

To overcome the fear of rebalancing in a down market, retirees may prefer to deploy a bucket strategy. This strategy exploits the cognitive bias of mental accounting, our tendency to assign subjective values to different buckets of money (think of a Christmas account) regardless of fungibility. To implement the strategy, investors establish two (or more) buckets:

1. A cash like “short-term” bucket funded with two to three years of income needs.

2. A “long-term” diversified investment bucket with remaining retirement funds.

Retirees then pull income needs, year to year, from the short-term bucket. The long-term bucket replenishes the short-term bucket over specified intervals or balance thresholds. While this strategy will not eliminate the sequence-of-returns risk, it may allow retirees the flexibility to navigate market downturns. To mitigate losses, bear markets often compel retirees to rebalance to a more conservative allocation. Unfortunately, this will reduce the chance of recovering losses realized and/or increase future income. By physically and mentally segregating the buckets, retirees may be less prone to make irrational decisions; understanding current income will not be affected by market downturns while at the same time allowing the long-term bucket time to recover.

The variable strategy

Most static retirement income programs adjust your income distribution by inflation, keeping your real income the same regardless of need. But what if income needs change year-to-year? In data collected by Morningstar Investment Management, David Blanchett showed that spending doesn’t stay the same through retirement. He referred to the pattern as the “retirement spending smile.” He noted that spending is higher in the beginning years, declines through the middle years, and then starts to rise near the back end of the horizon.

Intuitively, a phased spending scenario makes sense. Retirees will typically spend most of their consumption and entertainment upfront, gradually reducing expenditures as health and mobility decline. The increase in spending near the end of retirement is attributed to healthcare expenses that by in large become a greater portion of spending. A retiree may deploy a variable spending schedule for retirement income. The most basic form would be to plan a higher initial income that gradually decreases over time while also accounting for future healthcare needs. This will typically yield a higher initial income but comes at the expense of some behavioral biases. Humans tend to be creatures of habit and accepting a lower income when the time comes presents a challenge for most. Additionally, it’s difficult to model just how much income reduction to plan for. Various retirement income models try to estimate this “retirement spending smile,” but when faced with the reality of a reduced income, follow-through becomes the hurdle.

The dynamic strategy

While a variable income strategy will typically define phases when income is needed, a dynamic strategy will adjust according to market conditions. One form of dynamic income planning uses Monte Carlo1 analysis. A Monte Carlo simulation runs thousands of possible scenarios to determine the probability of distribution success. Retirees then increase or decrease income based on the probability they deem satisfactory. For example, if 85% is deemed a successful threshold and the Monte Carlo simulation calculates 95% distribution success, the distribution could be increased. Alternatively, if the simulation shows a 75% probability, distributions would need to be decreased. A success rate of 100% is ideal, but undoubtedly there will be circumstances when that is not possible. Therefore the biggest hurdle to the strategy is determining what level of confidence is satisfactory. Once you have determined the acceptable threshold, you can run the Monte Carlo simulation at pre-defined intervals (annually, bi-annually, etc.) to increase or decrease income. As in the variable income option, it assumes that a retiree is willing and able to moderate income in the positive and negative direction.

The insuring strategy

Ultimately, the retirement nest egg is used to generate income and most of the strategies I discussed require or assume a retirement horizon. Unfortunately, without the benefit of hindsight, we can never be truly sure of the required duration. One way to eliminate longevity risk (the risk of outliving your assets) is by insuring the retirement income stream. In this scenario, a retiree works with an insurance company to provide income over a single or joint lifetime in exchange for a lump sum. To evaluate the strategy, one must balance the comfort of receiving an income regardless of market performance or longevity against the costs. Principal accessibility, beneficiary payouts, creditworthiness, and costs are but a few factors to consider.

Alex Murguia and Wade Pfau, two prominent retirement thought leaders, have written, “Constructing an appropriate strategy is a process, and there is no single right answer. No one approach or retirement income product works best for everyone.”

The strategies outlined are not exhaustive and are a framework retirees can use to understand different approaches. Which strategy or strategies to employ will be a function of personal preferences and other variables. For instance, is a retiree more satisfied with a stable or variable income, and if variable, would they prefer higher income now or later? Even if we can answer some of those subjective questions, we can never be sure of the sequence of returns, time horizon, and biases that may derail a particular plan.

Ultimately, a retirement plan will require balancing the desires of life with making sure we don’t “fall short.” It is the role of an advisor to determine which strategy or strategies best fits these objectives.

Krisna Patel, CFA, is an Investment Advisor Representative of Woodbury Financial Services, Inc., at 11001 W. 120th Ave. Suite 400, Broomfield, CO 80021. Krisna may be reached by phone at (317) 489-3505 or by email at [email protected]

1The projections or other information generated by Monte Carlo analysis tools regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. Results may vary with each use and over time.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All