Advisors make seven predictably irrational mistakes when it comes to bonds, depleting their clients’ wealth and standard of living.

Advisors make seven predictably irrational mistakes when it comes to bonds, depleting their clients’ wealth and standard of living.

1. Predicting interest rates. One person recently told me, “I don’t want bonds. I’m guaranteed to lose as interest rates continue to rise.” While it’s true that the Federal Reserve has announced that it will begin increasing the Fed funds rate, remember that is the shortest of the short-term rates – in fact it’s an overnight rate.

Roughly a decade ago in 2011, the then chief economist from Wells Fargo told me “interest rates will definitely rise.” I shared with him a study on the dismal track record of economists’ interest rate predictions showing similar results to this study by the New York Times. In fact, the 10-year Treasury Bond interest rate plunged that year from 3.30% to 1.89%. When rates continued to decrease through 2020, forecasts from economists showed similarly dismal results with predictions of increasing rates. Though rates did tick up in 2021 and this year, we don’t know if this will continue.

Why is it so hard to predict intermediate and long-term interest rates? The Federal Reserve conducts regular auctions for Treasury Bonds and Bills. If the buyers believed in the forecasts of those economists, they would bid a lower amount to get that higher return. Thus rates already would have increased.

I tell clients the best estimate of future intermediate and longer-term interest rates is today’s rates. I too have overestimated interest rates, but at least I’ve known for some time I can’t predict rates.

2. Hoarding cash or staying ultra-short. Because many think they know what will happen to interest rates (that they will increase), they want to keep cash or a combination of cash and ultra-short-term bonds. Even with the recent so-called plunge in bond prices, a Bloomberg Barclays Aggregate Bond Index fund like the iShares Core US Aggregate Bond ETF (AGG) earned 2.62% a year for the five years ending February 15, 2022. Those willing to take a little interest rate risk earned 13.8% while those in cash got virtually nothing. Ultra-short bond funds with the same high credit quality earned far less.

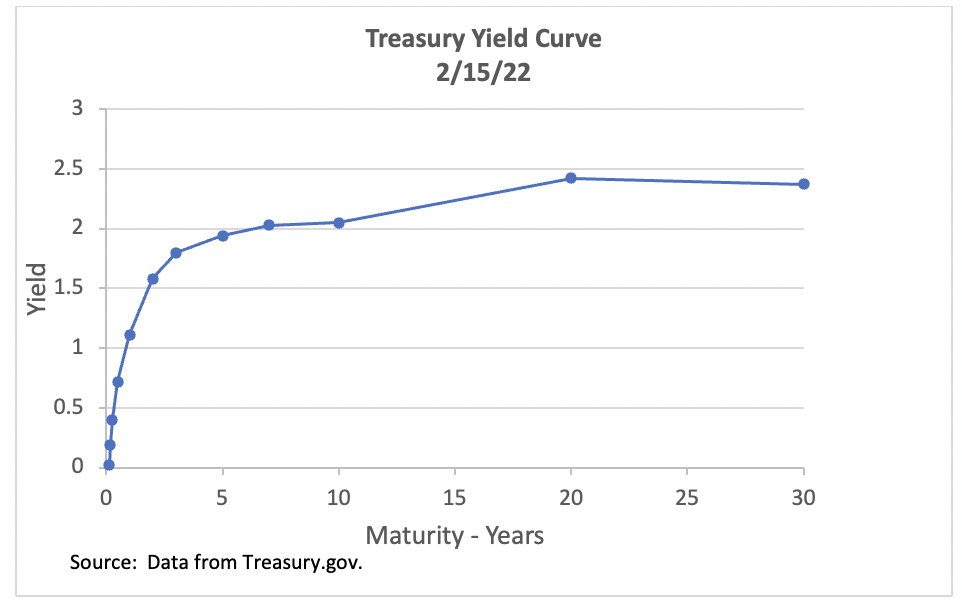

3. Going long. Knowing that we don’t know what will happen to interest rates cuts both ways. Looking at the recent yield curve, you are being compensated the most for taking about five to seven years of interest rate risk. Beyond that, there is little to no compensation for taking on term risk. But if rates rise, those going long will pay a large price.

4. Chasing yield. With nominal interest rates so low, many are taking risks to earn a bit more. Why settle for the 1.95% yield of AGG when the SPDR® High Yield Bond ETF (SPHY) has a 5.24% SEC yield? One of the few Wall Street terms that is accurate is “junk” for high yield, which is below BBB credit quality. Junk tanks when stocks do and doesn’t serve the role of the portfolio stabilizer. Advisors have overallocated to junk, as shown by this Vanguard survey.

5. Expecting high yields and safe returns. I frequently see floating rate funds in portfolios. Clients or advisors often think getting high yields and protection from rising rates is bullet proof. What could go wrong since higher interest rates would lead to higher yields? Plenty. Companies with high credit quality can lock rates in and don’t have to issue variable rate notes. It is the lower credit quality companies whose debt you will find in floating rate funds.

Let’s look at the SPDR Blackstone Senior Loan ETF (SRLN) yielding an attractive 4.38%. The average credit quality is B and 15% is below B or not rated. Any guesses what happens to this fund when stocks tank?

6. Finding alternatives to bonds. Why even own bonds when there are so many so-called safe alternatives for income? I see clients with preferred stocks, dividend stocks, and private REITs. Years ago, I would see master limited partnerships touted as safe alternatives to bonds because the pipelines were “monopolistic toll roads” that the oil must flow through.

Well, holders of preferred stocks found they got little back in a bankruptcy (far less than bond holders). “Safe” dividend stocks like GM, Eastman Kodak, and more recently GE, weren’t safe. Private REITs cut their teaser rates, and those master limited partnerships were highly levered and lost more than half their principal.

7. Avoiding bonds altogether. I often hear, “I’m a long-term investor and stocks always recover.” It turns out that those are the people who call me after a stock plunge wondering what they should do. It took more than three decades for Japanese stocks to recover back to their 1989 level. The three bear markets the U.S. has had since 1999 were just teddy bears, and the next one could be a grizzly bear.

Bonds are an important part of a client portfolio. The less risk clients need to take, the more they need bonds to protect the financial independence they have worked so hard to a achieve. Keep credit quality high with an intermediate duration. One recovers from interest rate risk since yields increase over time when interest rates increase. One does not recover from default risk. Consider TIPS for part of the fixed income, though rates are near a record low real yield at about a negative 1.2%. TIPS are also more volatile than fixed rate Treasury bonds.

Sometimes a client has attractive choices for high-quality fixed income that may not fit into your platform. CD rates can be way above bond rates (not currently) and, while these are small amounts, I Bonds are yielding 7.12%, federal tax-deferred and state tax-free. Some client 401K plans have legacy stable value choices with attractive rates offered through insurance companies.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

Read more articles by Allan Roth

Advisors make seven predictably irrational mistakes when it comes to bonds, depleting their clients’ wealth and standard of living.

Advisors make seven predictably irrational mistakes when it comes to bonds, depleting their clients’ wealth and standard of living.