Data from Vanguard shows that advisors have increased allocations to passive, low-cost investment products. But they also increased allocations to commodities and timed markets poorly, particularly after the March 2020 crash.

Data from Vanguard shows that advisors have increased allocations to passive, low-cost investment products. But they also increased allocations to commodities and timed markets poorly, particularly after the March 2020 crash.

Last month, Ryan Barksdale gave a fascinating presentation at the AP Thought Leader Summit. He is the head of portfolio analytics and consulting at Vanguard. The presentation, “Portfolio Insights: Effective investment strategies in the current market,” provided those and other riveting insights. A few of these trends were very encouraging, while others were downright frightening. I interviewed Ryan about his presentation.

Ryan aggregated approximately 15,000 portfolios using a Vanguard diagnostic tool and analyzed data on services Vanguard provides to advisors. He told me the purpose of sharing this data was to help advisors have a more objective view of portfolio construction trends and compare their strategies to other advisors to inform portfolio decisions.

My first question to Ryan was how representative of advisors overall was the data presented? I suspect advisors using Vanguard funds are more concerned with costs and more likely to use market-cap-weighted funds. Advisors using smart-beta strategies or high-cost products would be less likely to use Vanguard services. Ryan said he, “agreed that this data includes advisors using Vanguard’s portfolio construction tools and consulting services (not necessarily Vanguard investment products) and more cost conscious and more benchmark-oriented (i.e., less dramatic factor / sector exposures).”

First, the wonderful trends:

Embracing “dumb beta”

A decade ago, “smart beta” was the craze and it was viewed by many advisors as a free lunch. Some told me it was behavioral in that investors chased growing companies and shunned value-oriented stocks. Soon over 500 smart-beta factor strategies were discovered that “worked” in the past.

However, I embraced market-cap weighting and named it “dumb beta.”

I was pleasantly surprised to see that advisors were very close to market-cap weighting in value, growth and size. I would have loved to see the allocation of those same advisors a decade ago before small-cap, value and other factor investing badly underperformed.

Getting more cost conscious

The average expense ratio is 0.33% annually. While this number has an extra digit more than what I recommend, it’s a large decrease from the 0.44% average expense ratio in Q1 2020. This is an encouraging sign since we know that costs are the best predictors of relative performance. I suspect this isn’t representative of advisors in general because, as previously noted, advisors using Vanguard would tend to be more cost conscious.

Continuing to move to indexing

Related to falling expense ratios, advisors are using more passive index funds. More than 60% of equity funds used by advisors are passive, though fewer than 40% of fixed income is passive. Advisors are increasingly passive for both asset classes. Overall, indexing accounts for more than half of U.S. stock funds and advisors are part of that trend. Fixed income has a smaller share in passive and that’s likely due to taking on more credit risk, which I’ll review shortly.

Simplifying

The average number of funds used by advisors is 14. While I argue a diversified portfolio can be built with three to five funds, I can rarely do this for clients as tax ramifications prevent this simplification. Still, advisors aren’t constructing mind-numbingly complex portfolios that take 100 pages to list on a statement and have far less diversification than broad index funds.

Next, the trends that concern me:

Taking a lot of risk

While I don’t know the average age of the clients or how much risk they need to take, the asset allocation to risky stocks and hybrids/alternatives at 65% is aggressive. This is particularly so given that the fixed income is tilted toward lower credit quality, which I’ll discuss later. I put this in the “concerned” category and not as frightening as the next two trends.

What I fear is going on is a déjà vu of what advisors did during the financial crisis. Then, TD Ameritrade released data showing advisors timed the market poorly.

- On 10/9/07, after five years of bull markets, when U.S. stocks doubled and international stocks tripled, advisors had only 26% of assets in cash and fixed income.

- On 3/9/09, at the bottom of the bear market and just before the raging bull started, advisors nearly doubled their allocation to conservative assets at 51%.

- In 2010, after stocks had recovered, they reduced cash and fixed-income allocations.

Stocks have been on a tear since 2009 with the briefest bear market in history in March 2020. That, combined with interest rates near nominal lows, had driven advisors and clients to allocate to riskier stocks. While no one knows when this raging bull will end, it’s quite likely that advisors will get more conservative after stocks plunge. That, of course, is predictably irrational.

Underweighting international stocks

Ryan referred to this as home-country bias (i.e., preference of investors to invest more in their home country relative to global market cap). I pressed him on this matter, noting it could also be recency bias in that international stocks have badly lagged the U.S. over the last dozen or so years. Ryan did not have reliable data going back many years, and there is no way to test the hypothesis that advisors had a greater international stock allocation in 2007, after international stocks had trounced U.S. stocks over the prior five years. More detail on home country bias and Vanguard’s perspective can be found in this piece: Vanguard’s framework for constructing globally diversified portfolios.

I believe in overweighting stocks in one’s home country. That’s because there is foreign currency risk in international stocks. But, most importantly, I tell clients to pick an asset allocation and stick to it. The human tendency of investors and advisors is to chase past performance. Ryan told me, “It takes discipline to sell U.S. equities and buy non-U.S. stocks after performances over the past decade. Vanguard believes maintaining discipline is one of the keys to successful long-term investing, in addition to setting goals, maintaining balance, and focusing on costs.” I agree.

Three trends that scare the heck out of me:

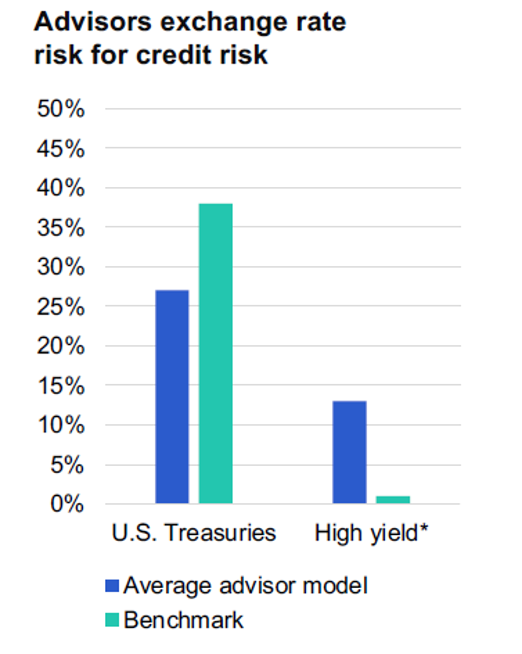

Taking on way too much credit risk

Advisors have about 13% of their clients’ fixed income in junk or non-rated fixed income, which is many times that of the entire market. Conversely, advisors have far less fixed income backed by the U.S. Treasury than the overall bond market.

Ryan said investors are hungry for yield. He also noted, “There is less conviction in certain areas of the fixed income markets given the yield environment. We’d encourage advisors to revisit the role of bonds in their portfolio; we believe high-quality fixed income remains an important component given the opportunity to serve as a buffer for equity market volatility (i.e., provides balance).”

Junk is highly positively correlated with stocks and, to a lesser extent, investment-grade corporate bonds, especially A and BBB rated bonds. The common belief that rates are near an all-time low is misguided. What matters most is one’s after-tax real return. Sure, it felt wonderful to earn 12% in 1981. Unfortunately, after taxes and inflation, investors lost about 4% of their spending power, which is far worse than today.

What I suspect is going on is that AUM advisors are concerned clients may think advisors are taking too much of the pie. With the Bloomberg Barclays aggregate (AGG) bond funds yielding about 1.30% and five-year Treasury bond yielding 0.88%, clients object to the advisor taking 0.50 to 1.00% in a management fee. Thus, advisors take on more credit risk as well as an equity-heavy portfolio. According to Ryan, “Advisors are paying a valuation premium for high-quality in equities and overweighting lower quality for fixed income at a time of relatively low yields and tight spreads. I understand it given the low-yield environment, but lower credit quality fixed income may lead to unintended risk, and volatility levels similar to equities.”

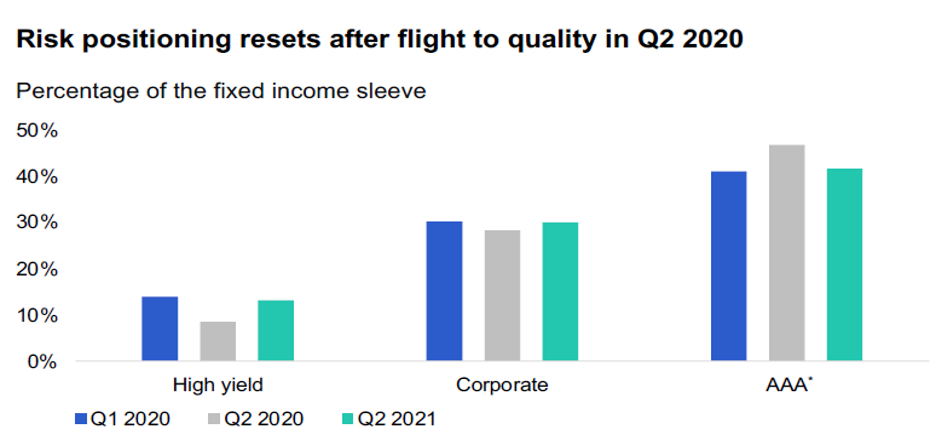

Continuing poor timing

Earlier, I showed advisors timed markets poorly during the 2008-2009 real-estate/financial bubble. While I don’t have data on how they behaved during the 33 days beginning February 19, when stocks dropped 35%, advisors performed horribly with fixed income.

In the first quarter of last year, advisors were heavy in junk and corporate and light on high-credit-quality (mostly U.S. government debt). Then, predictably, after junk and corporate bonds sank along with their stock portfolios, advisors got out just before they recovered and went to high-quality fixed income. After lower credit quality bonds recovered, advisors went back to get more yield. Again, this is predictably irrational. Ryan explained, “It’s a tough strategy to be successful in timing (e.g., U.S. versus International), which is why we reinforce timeless investment principles (goals, balance, costs, discipline).”

To a lesser extent, advisors timed equities poorly as well. Ryan says: “In short, we see a similar risk-on to off to on trend from an asset class perspective during the period in question (i.e., advisors’ equity exposure began at 63% then moved to below 60% and then back up to 62.3%). This could be that advisors didn’t rebalance rather than selling after the decline.”

Increasing commodity exposure

Ryan showed that advisors increased commodity holdings by 50% in the second quarter of this year versus the previous quarter. No investment firm holds the actual commodities. They use futures, and, in the aggregate and before fees, not a penny has ever been made in the futures market. Perhaps that’s why Vanguard shows the Bloomberg Commodity Index (benchmark) losing 4.67% annually over the last decade ending August 31, 2021. Futures are important risk mitigators for corporations like airlines and oil companies to stabilize revenues and expenses, but they are pure gambling for individuals.

What drove this increase? I suspect it’s the nearly 38% increase in valuations over the past year. Performance chasing and gambling are alive and well.

Conclusion

It’s always interesting to see how other advisors are investing, which is why this presentation was so fascinating. Though it feels safer to invest like our peers, choose which trends you follow wisely. Lower fees and greater diversification are wonderful trends I’m happy to embrace. Others, like performance chasing and holding low-quality fixed income, are trends I’m happy to avoid.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion dollar companies and has consulted with many others while at McKinsey & Company.

Read more articles by Allan Roth

Data from Vanguard shows that advisors have increased allocations to passive, low-cost investment products. But they also increased allocations to commodities and timed markets poorly, particularly after the March 2020 crash.

Data from Vanguard shows that advisors have increased allocations to passive, low-cost investment products. But they also increased allocations to commodities and timed markets poorly, particularly after the March 2020 crash.