Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

With Russia’s invasion of Ukraine on February 24, the post-Cold War order – one founded on peace, security, and the encouragement and proliferation of global trade and capital flows – came to a screeching halt. As global markets and economies digest the impact of this new world order, many investors are left searching for what it all means for their portfolios. All geopolitical crises, including the current one, present three timeless lessons investors would be wise to heed.

1. Markets respond quickly to new information

Markets responded immediately when news of the invasion broke. In response, Western nations announced a heavy barrage of long-threatened sanctions on Russia aimed at crippling the Russian economy, punishing Russian oligarchs, and isolating Russia from the global economy. The Dow Jones sold off early on the news and was down more than 800 points when it first opened. However, around 1:13pm ET news broke that the European Union had decided against excluding Russia from SWIFT – the global telecommunications network that connects the world’s banks – a decision that effectively watered down the immediate and harshest impacts of any economic sanctions.1 The market subsequently rallied more than 800 points to finish the day up 92 points.

Exhibit 1: Intraday Chart of the Dow Jones Industrial Average2

The rapidity with which markets responded to new information was not isolated to the Dow Jones. On the first day of the invasion (February 24), the Russian stock market cratered nearly 40%. A week later, the MSCI Russia Index was down nearly 50%; at the time of writing, the Russian ruble is down approximately 30% in value against the US dollar.3 Similarly, the yield on the U.S. 10-year Treasury opened down nearly 10 basis points from its prior-day close – before nearly fully recovering by day’s end. A close analysis of the tick data shows yields began to rise at precisely the same time news broke of the EU’s decision to not exclude Russia from participation in SWIFT (around 1:13 PM EST).4

The takeaway for investors is that markets respond quickly to new information; any hopes we might harbor of trading on such information to earn short-term profits should be set aside. In most cases, markets are highly efficient when it comes to rapidly incorporating new information and our ability to capture excess profits by trading on such information is almost always little more than wishful thinking.

2. Investors should diversify not because of what they expect but to protect against what they don’t

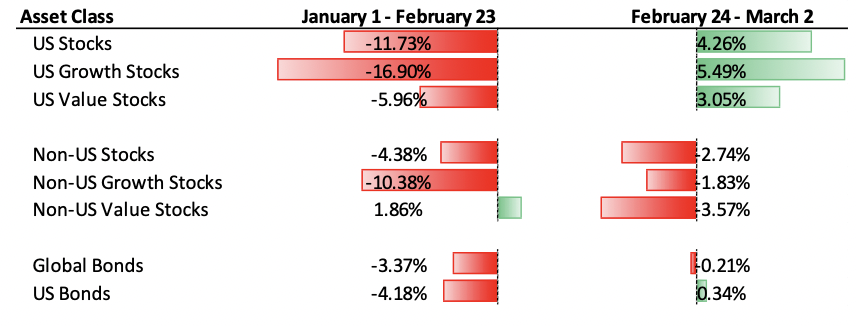

Humility is by far the most important asset to include in any portfolio. Investors would be wise to keep their overconfidence biases in check. Coming into the year, nearly every market pundit predicted higher interest rates in the year ahead. As recently as a week ago, the market was pricing in seven rate hikes, with as much as a 50-basis point hike in March. Subsequently, most financial advisors recommended investors lower fixed income durations, reduce allocations to growth, and overweight value and non-U.S. stocks within their portfolios. Based on market expectations, these were absolutely the right calls.

Yet, it’s our expectations – no matter how sound our reasoning – that lead to overconfidence, a dangerous state of mind that mischievously deludes us into foregoing valuable diversification. Too many investors heavily overweight portfolios based on experts’ market forecasts. It was precisely those asset classes that we expected to underperform this year – for example, fixed income and U.S. growth socks (especially relative to non-U.S. and value stocks) – that have thus far outperformed handsomely since the crisis began. Prior to the crisis, the pundits’ thesis was accurate – value stocks outperformed growth, both at home and abroad. Similarly, fixed income – while still a powerful diversifier to equities – struggled in the face of inflation and the promise of higher rates. However, in the week since the invasion began, we’ve seen a reversal of those pre-February 24 trends.

Investors would be wise to maintain globally well-diversified portfolios across major asset classes – and resist significantly departing from a broad, cap-weighted asset allocation.

Exhibit 2: Strong relative returns for value and non-US stocks prior to the crisis rapidly reversed when the unexpected happened.5

It’s important to diversify across asset classes and within them. Far too often investors have poor intra-asset class diversification. Let’s go back in time and consider the case of an investor who, in hopes of capitalizing on an expected rise in energy prices due to the crisis, decides to add an energy sector allocation to his portfolio when the market closes on February 23. He knows he wants to be diversified so he decides to add not one but two stocks to his new energy sector allocation. He spends several days reading through piles of company financials on his Bloomberg terminal and, being from Texas, he settles on dividing his energy sector allocation between two companies: a 50/50 allocation to Irving-based ExxonMobil (XOM) and Houston-based Marathon Oil (MPC). Yet, despite our hypothetical investor’s best efforts, his portfolio wasn’t diversified enough to offset the company-specific risk associated with owning just two companies. He would’ve done better had he simply invested in a more diversified energy sector ETF like XLE.

Exhibit 3: Diversifying within asset classes is just as important as diversifying across asset classes.

Don’t fixate on short-term market returns. The unexpected can happen at any time. Indeed, if markets have taught us anything over the years, it’s that the unexpected has a curious way of happening with a high degree of frequency. And the best approach to protecting against the unexpected is through the maintenance of a disciplined, globally diversified portfolio that is well-diversified both across and within asset classes.

3. Geopolitical selloffs are typically short-lived

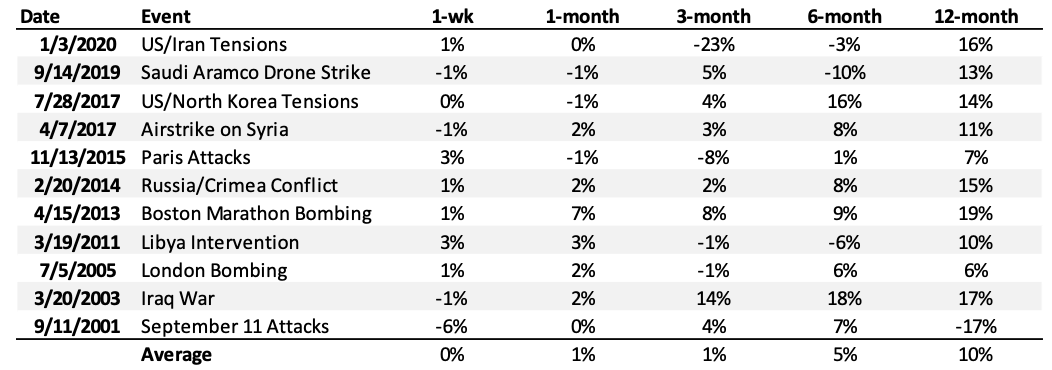

Market history includes a staggering abundance of geopolitical, financial, and economic crises. Geopolitical selloffs have typically been short-lived. A recent study by Vanguard showed that, beginning with the Suez crisis of 1956, U.S. equities returned on average 5% within six months of an initial geopolitical selloff and 9% within one year.6 Even the 1962 Cuban missile crisis – arguably the most serious geopolitical crisis since the end of the second World War – saw U.S. equities initially decline a relatively mild 5% and then go on to return 21% six months later.7 More recent history has similarly seen no lack of geopolitical crises; and when we look at the data, what we see is that geopolitical crises have tended to be relatively short-lived and that, over time, markets have gone on to reward disciplined investors.

Exhibit 4: Geopolitical self-offs have been relatively mild and short-lived.8

Conclusion

None of this is to overlook or in any way minimize the unspeakable human tragedy that is unfolding in Ukraine. War is always and everywhere a horrible, and are typically negative-sum game with no winners. However, the takeaways for investors are that markets, over time, reward those who resist (1) market timing; (2) remain diversified, both within and across asset classes; and (3) remain disciplined in the face of geopolitical crises.

Don Calcagni is the chief investment officer for Mercer Advisors.

1“Kyiv furious as EU fails to block Russia from SWIFT payment system”, The Guardian, Thursday, February 24, 2022 13:15pm EST.

2Chart courtesy of Yahoo!Finance.

3Source: FactSet, Inc.

4Source: FactSet, Inc.

5Source: YCharts, Inc. US stocks = Russell 3000; Non-US Stocks = MSCI ACWI Ex-USA; US Value Stocks = Russell 3000 Value; US Growth Socks = Russell 3000 Growth; Global Bonds = Barclays Global Aggregate; and US Bonds = Barclays US Aggregate.

6https://www.vanguard.com.au/personal/education-centre/en/insights-article/geopolitical-sell-offs

7Ibid.

8Source: BMO, as quoted by CNBC on February 24, 2022. https://www.cnbc.com/2022/02/24/geopolitical-shocks-to-the-stock-market-tend-to-be-fleeting-says-bmos-belski.html

Read more articles by Donald Calcagni

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.