When it comes to investment returns, most people, including those who work in financial markets, only consider nominal numbers. For example, they look at the price of the S&P 500 Index now, where it was a year ago and work out what the total return was including dividends in that period. They do the same calculation for bonds, substituting interest payments for dividends. By those measures, the S&P 500 returned about 14% and 10-year U.S. Treasury notes lost about 5%.

But what investors should be looking at are real numbers, which take into account the effect of inflation. This is not an abstruse, academic distinction. Good investments are ones that should, at the very least, maintain your ability to buy the things you want and need to buy in the future. In periods of low inflation, there isn’t much difference between nominal and real returns in the short term. When inflation is high and rising, good nominal returns become more modest ones, modest returns turn into bad ones and bad returns turn into woeful ones. In the examples above, the real returns have been roughly 7.7% for the S&P 500 and minus 12.5% for 10-year Treasuries given that the consumer price index surged 7.5% in the period. The Russell 2000 Index of small cap stocks lost 16% in real terms and, measured in dollars, emerging markets some 20%.

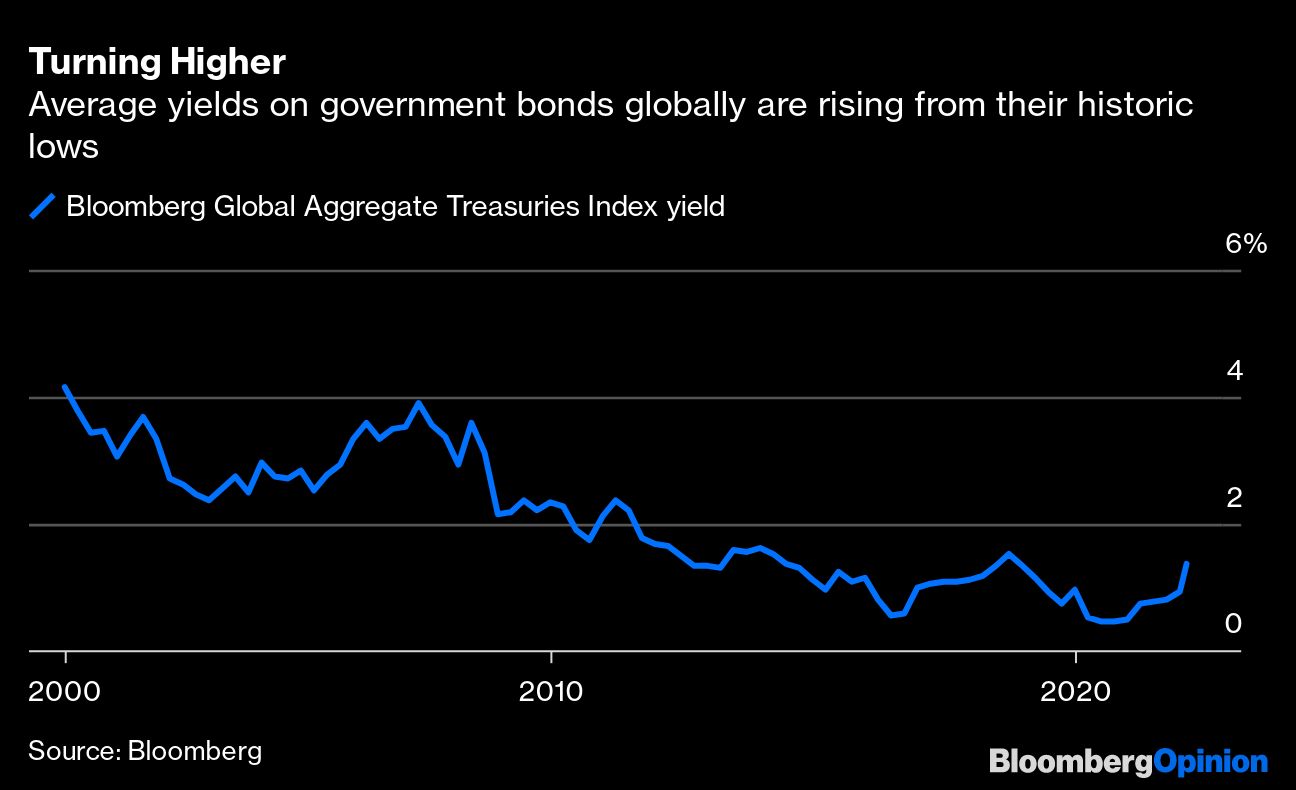

And with central banks set to rein in inflation, albeit very reluctantly, more obvious nominal losses will be added to less visible real losses. That is what happens when the risk premiums demanded by investors in almost every asset class are miniscule – as is still the case even after the recent turbulence in markets. Government bonds are a decent proxy for extremely slim risk premiums. The overwhelming consensus in markets is that inflation will rapidly drop, capping the rise in short-term interest rates and bond yields and thus supporting all types of riskier assets.

Central banks have said they are on the case. Some of them have even promised to push short rates up a bit to combat inflation. The rise in bond yields over the last six months has helped drive real yields — the yield offered by inflation-linked bonds before inflation is added in — higher. The yield on five-year Treasury Inflation-Protected Securities, for example, has jumped by a percentage point since mid-November. It is that rise in real yields that has unsettled other markets.

But the real yield on five-year TIPS is still below zero at minus 1%, and it is not clear what that number means. Indeed, the concept of future real yields is so fuzzy as to be almost meaningless. For very short-term rates, the real yield calculation is fairly straightforward: It is the official interest rate minus the inflation rate. The federal funds rate, for example, is about zero, so the real rate given the latest consumer price index reading is minus 7.5%. Future real rates, though, are a residual. They are merely the result of subtracting the expected inflation rate over the next five years from current nominal bond yields. But what markets expect and what they get are not the same thing. Inflation that is higher than markets expect means that actual real yields end up lower than forecast and vice versa.

If you’re confused about this, you’re not alone. I’m probably being generous in saying so are 95% of people who work in financial markets. For clarity, understand that two things, both guesses, dominate the current calculation of future real yields.

The first is that the market thinks the U.S. rate of inflation as measured by the CPI will fall to less than 3.5% over the next couple of years. The second is the main driver, which is that markets expect energy prices to fall. The spot price for West Texas Intermediate crude is roughly $92 a barrel. It’s price for the first quarter of next year in the futures market is about $80. But both the forward energy market and the forward inflation market have been consistently and spectacularly wrong for almost two years. If they continue to be wrong -- and the chances are high because, among other reasons, fossil-fuel investment has plummeted in recent years but demand continues to grow -- then inflation and inflation expectations will ratchet up further. And, all things equal, bond yields will have to rise a lot further to keep real yields from dropping.

The problem is that despite the rise in nominal bond yields in the past year, they remain so low that they reward investors even less than the expected rate of inflation over the life of the bond. Yet those expectations forecast a huge drop in the inflation rate. But if inflation slows more modestly, or stays where it is, the only way for investors not to lose money in real terms is to demand much higher nominal yields on bonds. That means even more losses for investors on top of those they have already suffered on their fixed-income assets.

Efforts by central banks to contain inflation will just mean that investors lose money more obviously. That’s not just in government bonds, but increasingly in credit and equities as well. It’s a sort of lightbulb moment, but not in a good way.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Richard Cookson