Oak Associates

Dieting is Hard

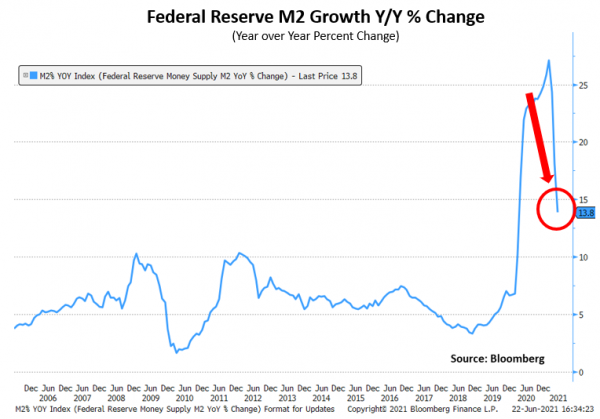

Investors are grappling with the reality of a new monetary backdrop in the US.

The Debate Over Guns or Butter Returns

In economics, “Guns or Butter” compares the impact of government spending on defense and non-defense categories. The Russia invasion of Ukraine has implications for investors and categories associated with defense, energy and industrials. Sectors deemed in the national interest should benefit from better appropriation, less regulation and bipartisan support.

Q3 2021 Market Commentary Answers to Our Most Recent Client Questions

US stocks, as seen by the S&P 500, ended the third quarter unchanged, having shed over 4% in September as fears over the debt ceiling and the Fed’s options erased the summer’s progress. Certainly, the market environment has changed a lot over the past 18 months. Valuations are up, economic data is varied, and the prospects of potential Fed action are growing.

Play Ball

Baseball fans returning to ballparks has been a definitive symbol of the optimism emanating from the reopening of the US economy. While the enthusiasm from consumers and investors alike is warranted, Jeff uses his version of the old-western movie title ‘The Good, The Bad, and The Ugly’ to describe Oak’s current view of the investment landscape.

Light at the End of a Long Tunnel

We have all endured the Covid-19 pandemic for over a year now.

The Heavy Lifting

Wall Street and Main Street are two different zip codes. In 2020, one neighborhood struggled with rising economic uncertainty, while the other posted strong gains underscored by a loose fiscal and monetary environment. In 2021, we expect the neighborhood's economic fortunes to converge.

The Calm After the Storms

We have stated many times over the past decade how well the stock market does overlooking the prominent headlines of the day and remaining focused on the underlying economy and its outlook. The third quarter of 2017 was no exception.

What Keeps Us Awake at Night

The US stock market, as seen by the S&P 500, rose an impressive 3.8% during the third quarter of 2016.