Could a disruptive cash crunch ensue, along the lines of what happened in money markets a few years ago?

Gold steadied after a two-day decline as traders eyed the soaring dollar and a surge in Treasury yields amid expectations of further monetary tightening by the Federal Reserve.

Investors naturally gravitate toward higher-income segments as a way to boost traditional core bond yields.

Investors who might be looking for the world’s biggest bond market to rally back soon from its worst losses in decades appear doomed to disappointment.

Stocks started the month on an upswing but ended with volatility.

US employers added a healthy number of jobs in August and a steady stream of people entering the labor force pushed the unemployment rate higher, consistent with a job market that is coming more into balance and offering mixed implications for the Federal Reserve.

"Without Italy, there is no Europe, but outside of Europe, there is even less Italy." -Mario Draghi

The second half of August has been bruising for technology stocks, but those hoping for a respite from the declines shouldn’t relax just yet: September is just around the corner.

Corporate junk bonds in the US are paying investors a paltry premium for the risk of holding them into a looming recession.

Some of Wall Street’s biggest banks expect a lengthy period of higher interest rates to further pressure Corporate America’s profit engine, threatening equity gains as companies grapple with elevated financing costs and margin-shredding inflation.

In Jackson Hole, Federal Reserve officials unequivocally emphasized their commitment to bringing inflation under control – even as the U.S. economy slows.

U.S. stocks ended the day in the red, continuing last week's sharp drop following comments from Fed Chairman Jerome Powell last Friday that heightened inflationary concerns.

Global bonds sold off as investors responded to central bankers signaling they will increase interest rates as much as necessary to bring down inflation.

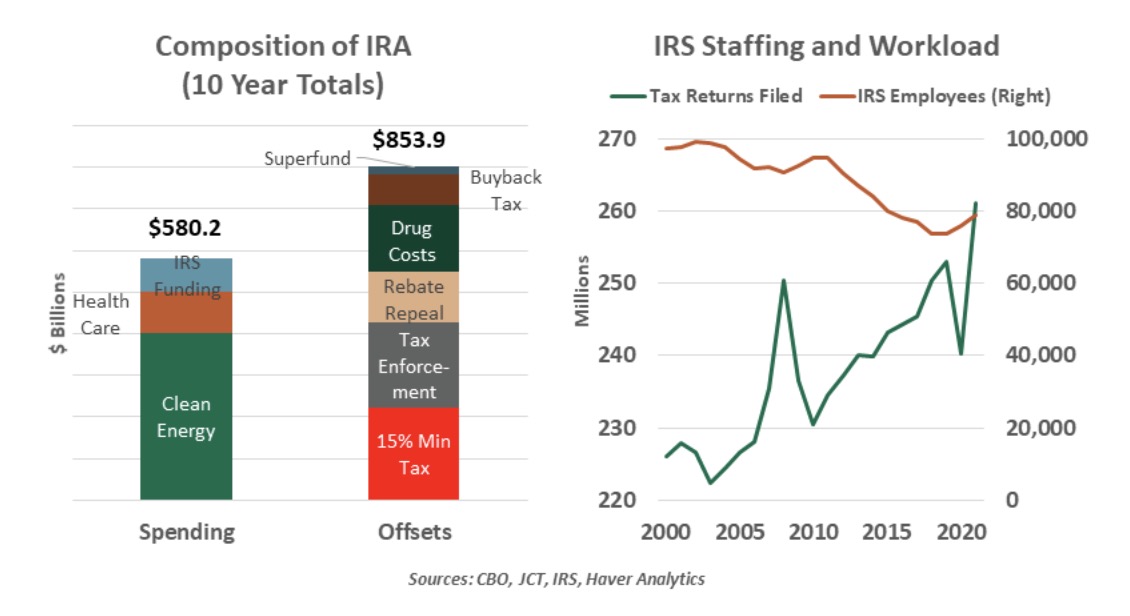

A long negotiation cycle yields green investment, a smaller deficit and higher corporate taxes.

With the recent increases in interest rates, the carry trade has had a sudden resurgence in performance, which could make it a tempting strategy for investors.

Two-year Treasury yields. rose as investors digested the remarks, pushed as high as 3.44% while the 2- to 10-year yield curve resumed its flattening. Equities were lower.

Professional stock pickers are beating the market in a scale not seen in more than a decade.

Even elite money managers are struggling to pick winners in this year’s vicious market.

Federal Reserve Chair Jerome Powell’s message to investors was short and blunt: The central bank will likely keep raising interest rates and leave them elevated for some time to battle inflation.

Mortgage rates in the US surged to the highest since June, turning up the pressure in a housing market where demand has fallen sharply from its pandemic-era peak.

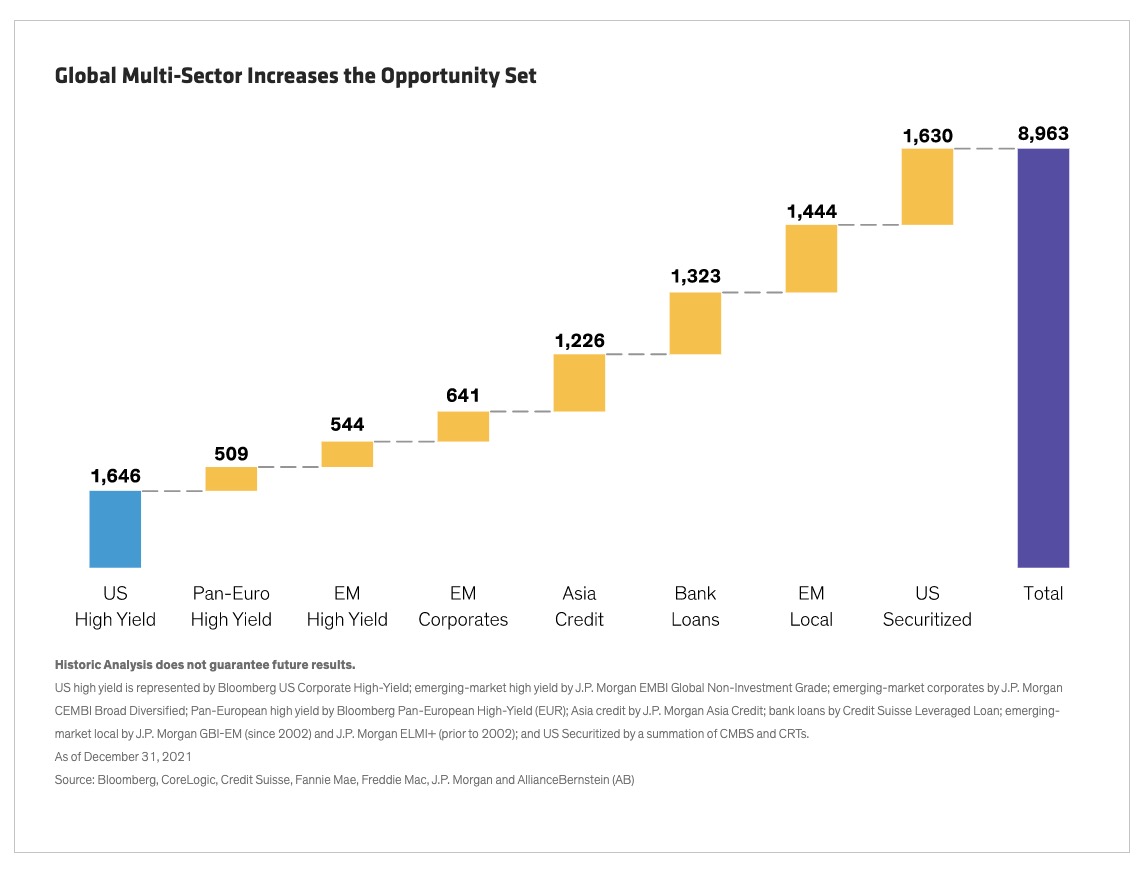

You might think these headwinds would be broadly negative for EM debt, but we see bright spots within the EM sovereign and corporate landscape.

Signposts for credit investors as the next recession approaches.

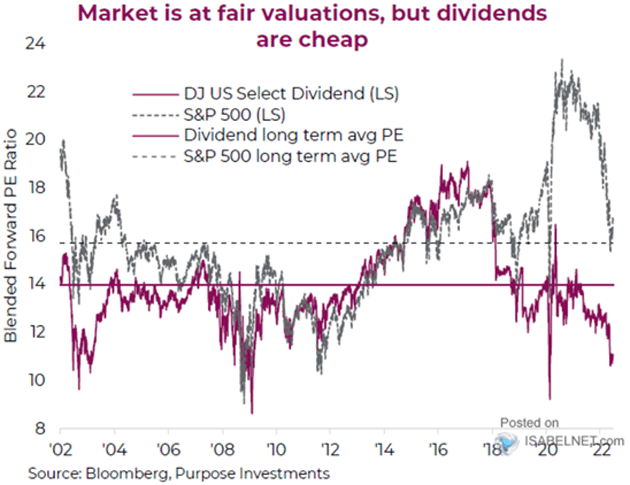

One of the most popular and reliable touchstones of investment strategy is value.

When Federal Reserve Chair Jay Powell speaks in Jackson Hole later this week, he will have no shortage of critics lying in wait to vivisect his every remark.

Cathie Wood’s flagship ETF, Bitcoin, meme stocks, profitless tech firms. The risk assets that powered this quarter’s $7 trillion rally all took a pounding Monday.

Some of the world’s biggest bond investors say the market is wrong to expect central banks to score a long-term win in the war against inflation.

Over our decades of involvement in emerging country debt markets, we’ve witnessed many ups and downs.

Equity markets have clearly taken notice of rising inflation—and not in a good way.

Corporate debt offers attractive yields, particularly through an interval fund with limited liquidity. I compare one such fund, CCLFX, to more traditional, liquid mutual funds.

Hedge funds are unleashing record bets that the Federal Reserve will stick to its hawkish script as they rapidly position for higher interest rates in a key corner of the derivatives market.

The Federal Reserve’s forward guidance program has been a disaster, so much so that it has strained the central bank’s credibility.

We normally start our letters on a positive note.

This is part 1 of Volume I Issue VI of the Macro Value Monitor, a publication focusing on Monetary History, Market Myths, Investing Legends, and Real Global Value.

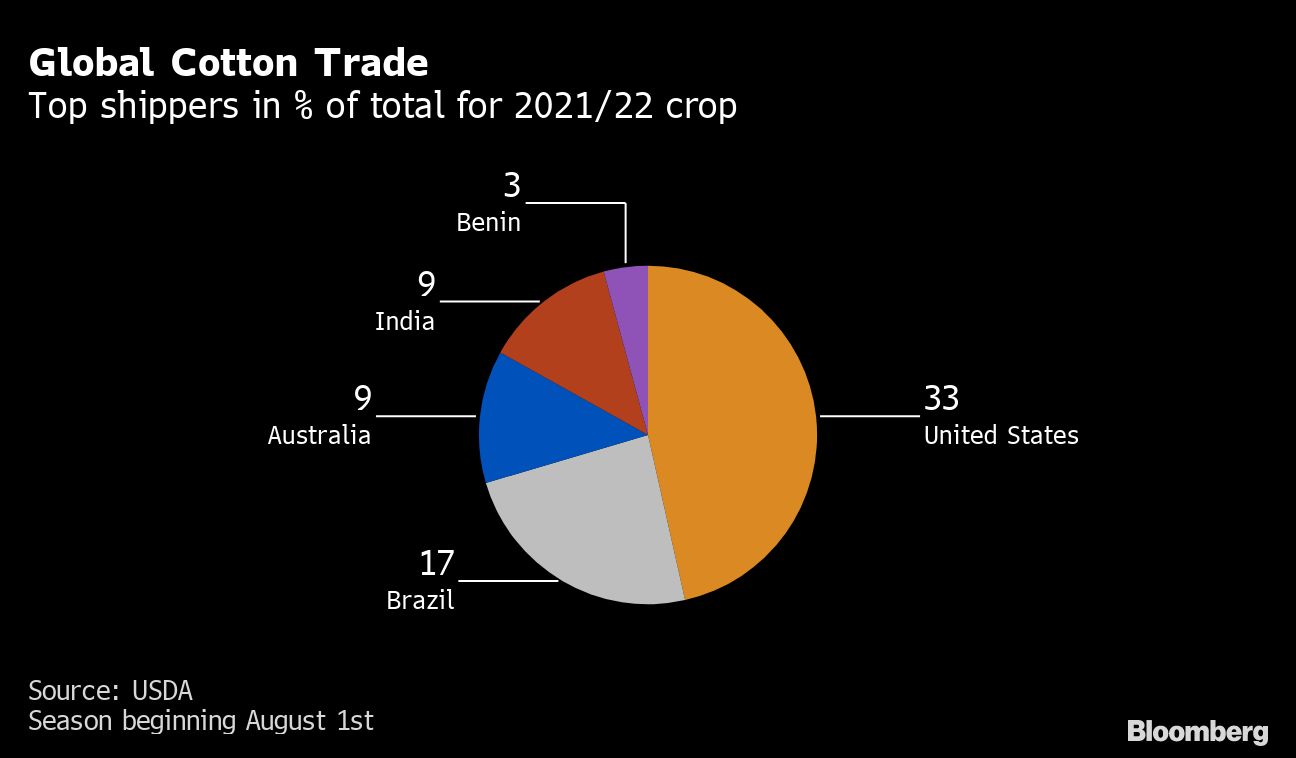

Extreme weather is wreaking havoc upon virtually all of the world’s largest cotton suppliers.

Cryptocurrencies suffered a sharp selloff as global markets retreated after US Federal Reserve officials reiterated their resolve to keep raising interest rates until inflation is contained.

Winter is coming for Europe, and energy prices are soaring as international sanctions on Russia curb the supply of natural gas, on which many European Union (EU) countries have increasingly become dependent.

Our own government cannot afford a short end of the curve much higher than it is now, and our own fiscal and monetary decisions have held down the long end of the curve in what I believe is a multi-decade period ahead that is best referred to as “Japanification”

“The Godfather” has a quote for everything. Maybe, just maybe, it was Putin all along. Or perhaps its was Nikolai Kondratiev.

In the face of what was the largest first half decline in the S&P 500 since 1970 and the worst ever start to a year for high yield bonds, short duration credit was not immune

If Wall Street is right, the big revival in value investing in the post-lockdown era is in danger of falling apart all thanks to the resurgent bond market.

U.S. stocks are subdued following yesterday’s release of the minutes from the Fed’s July monetary policy meeting.

It is my belief that the bear market is over.

The market contraction presents better opportunities than we’ve seen in years to generate income, which we balance against the need for resilience in the face of a potential recession.

Most advisors and practices get defensive during bear markets and recessions and look inward to protect what they have. They wait for the external climate to change to return to offense and growth.

The S&P 500 could be close to 3,500 by year-end if the Fed follows through with its QT plans.

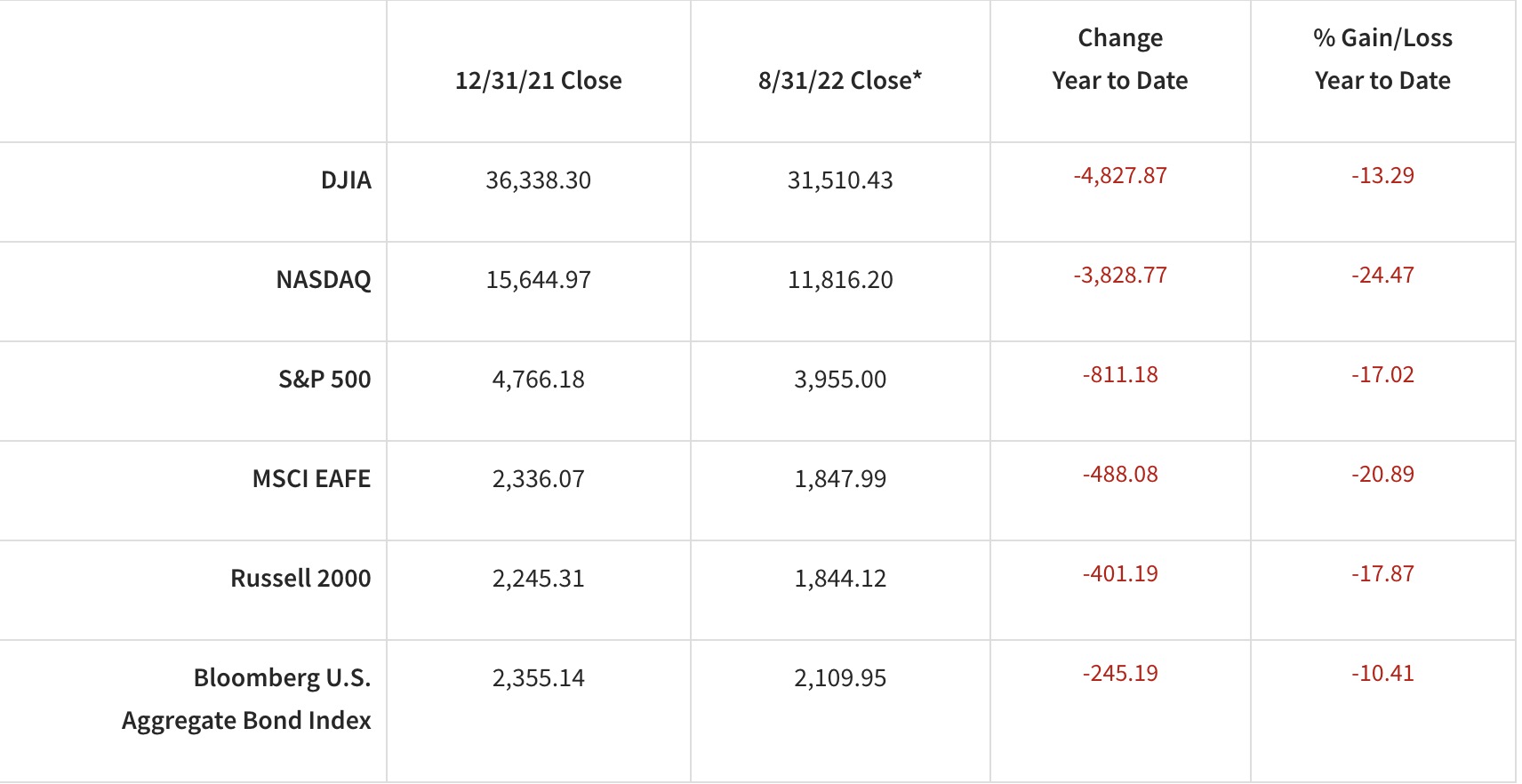

It’s been a tough first half of the year, with the MSCI All Country World Index down by 21.7% and the Bloomberg Global Treasury benchmark losing about 9% as of June 17.

After more than 40 years of work in the financial markets, studying all the data I could get my hands on, I’ve found it to be universally true that those who argue “history doesn’t matter” have never actually studied history.

After German troops were defeated in a pivotal battle at El Alamein in 1942, he commented that it was “not the end, not even the beginning of the end but, possibly, the end of the beginning.”

U.S. stocks have come off the worst levels of the day and are threatening a move into positive territory.

If you wanted evidence that the worst of inflation might be over, the last two days have offered quite a litany.