Inflation cooled in October by more than what was forecast, suggesting that one of the biggest headwinds facing tech could be easing.

An astounding $200 million dollars per day, every day, is spent gambling in Las Vegas casinos.

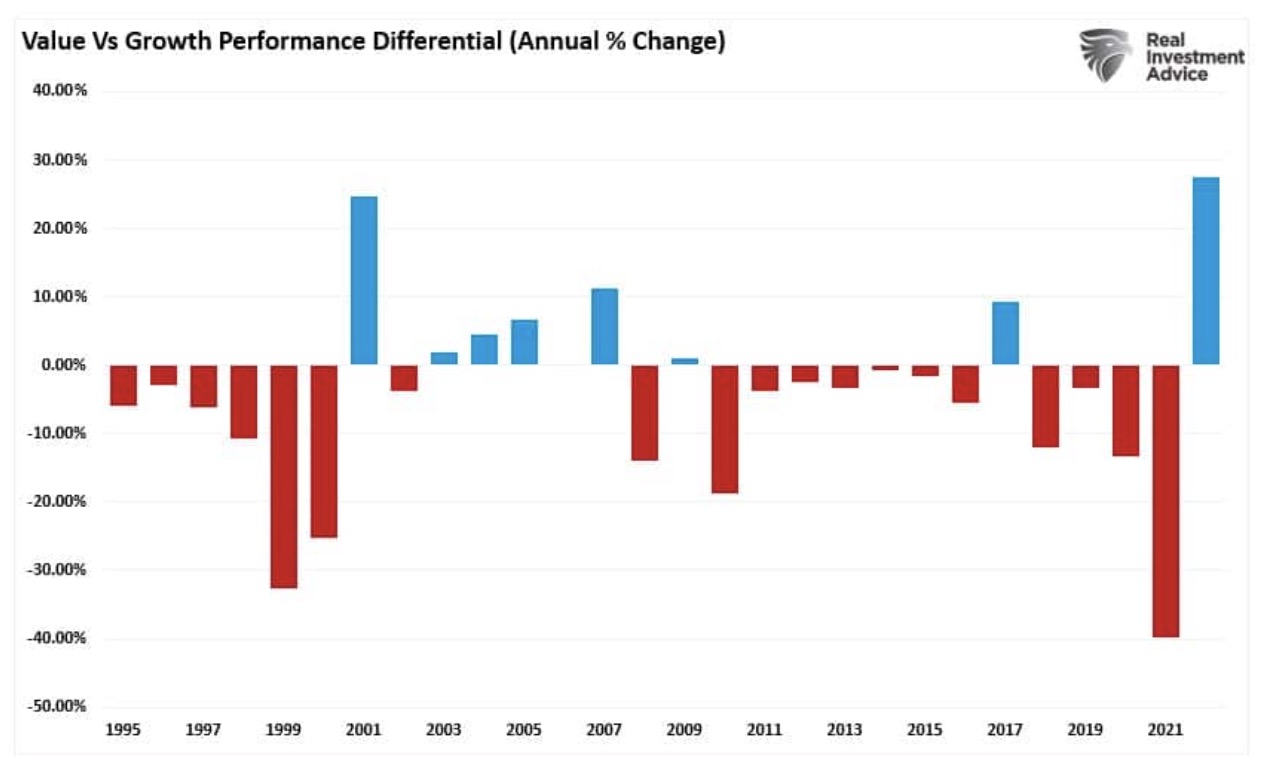

Are the FANG stocks dead?

It’s been a rough year for investors, and the credit market has been no exception. Rates have surged, ending a multi-decade bond bull market. How can investors generate alpha as credit yields become more attractive?

U.S. equities are lower as the global markets await the final results of the U.S. midterm elections as the control of the Congress remains undetermined.

It’s not as if volatility markets have needed extra juice this year.

Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

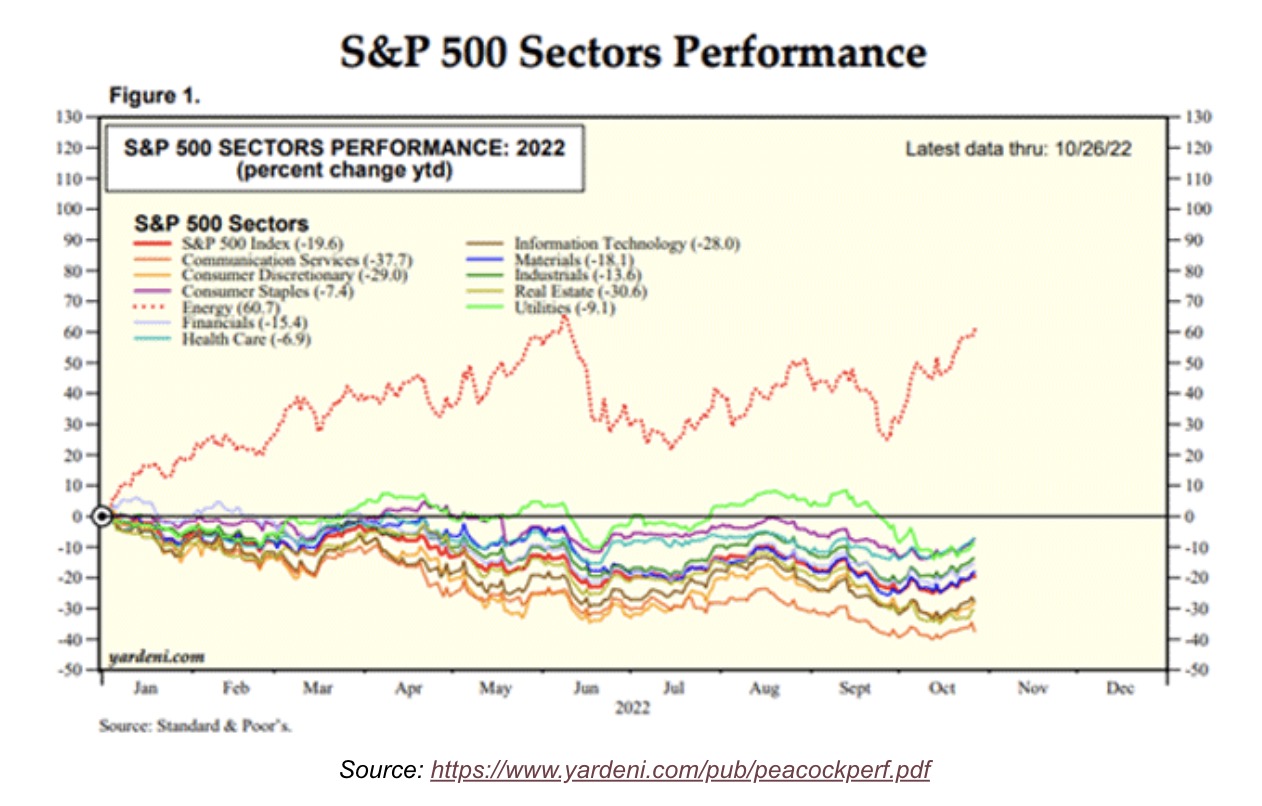

October started strong and then slid to new lows but managed to rally back toward the month’s end.

All bets appear to be off on how high yields can rise in the world’s biggest bond market.

For traditional fixed-income investors seeking higher yield and/or inflation protection, private, senior secured, sponsored debt provides an attractive alternative.

It took 16 months to pay off my husband’s student loans after we got married.

As I see it, decentralized assets have never looked more attractive than they do now.

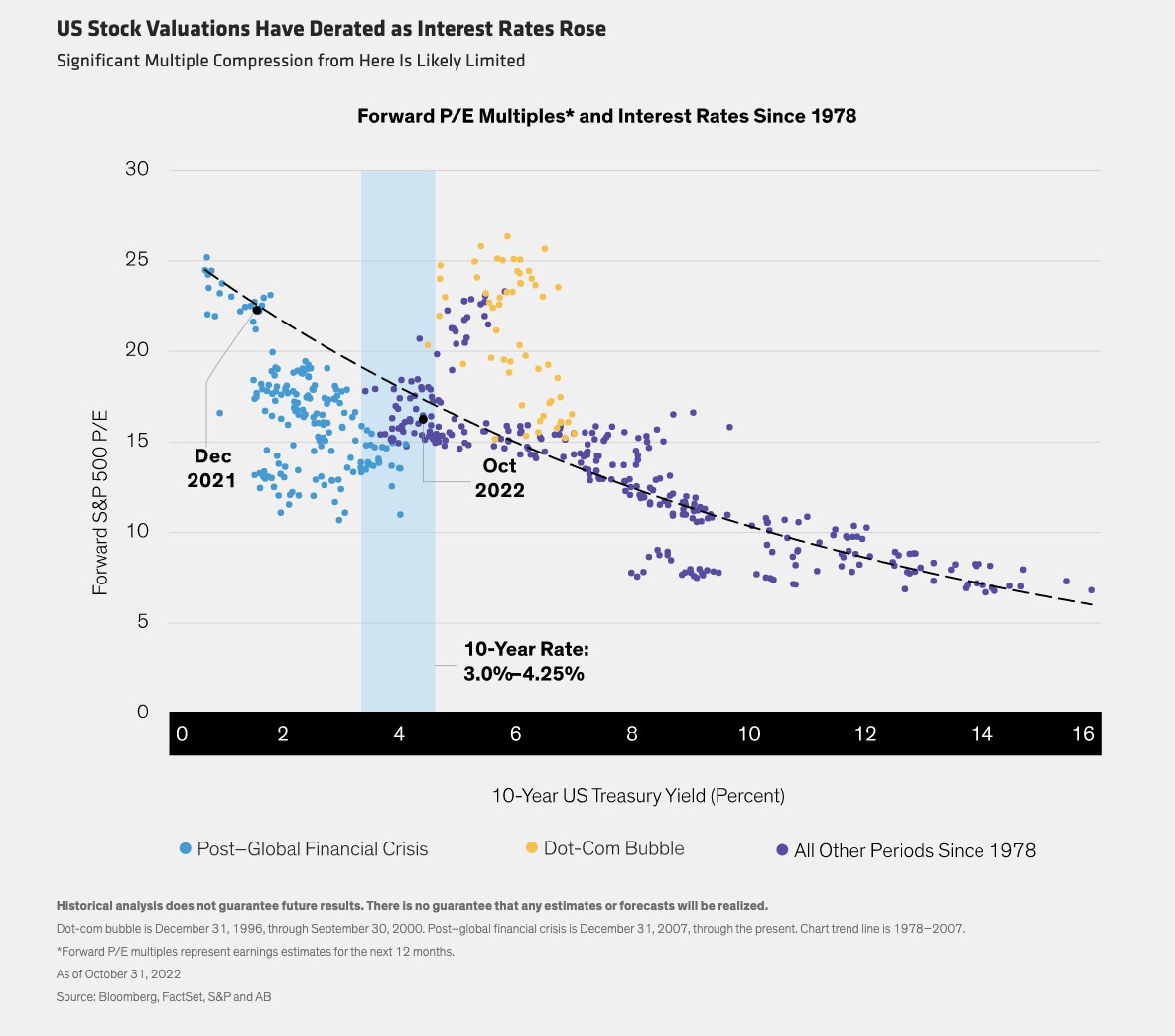

Equity valuations have fallen substantially as central banks hike interest rates to combat inflation.

The Federal Reserve’s November statement included dovish language, but Fed Chair Powell warned investors not to expect the Fed to stray from its full focus on fighting inflation.

Review the latest portfolio strategy commentary from Mike Gibbs, managing director of Equity Portfolio and Technical Strategy.

What are the implications of strategic asset allocation, the dynamics of public and private credit, tech-driven megatrends, and more?

Wall Street money managers looking to pile back into Treasuries after months of losses will have to contend with a Federal Reserve that stands ready to raise the stakes every step of the way.

About 90% of this year’s S&P 500 loss was attributable to higher interest rates.

Markets hoped for a dovish Federal Reserve “pivot,” but got a hawkish surprise instead.

Wall Street had already come to terms with prospects that the Fed would again raise interest rates by 75 basis points.

Jerome Powell’s Federal Reserve did something Wednesday it hadn’t done for months: say something dovish. Investors had all of 30 minutes to celebrate.

U.S. equities finished lower with the Dow whipsawing within a more than 900-point range following the Fed's monetary policy decision.

Federal Reserve officials signaled their aggressive campaign to curb inflation could be entering its final phase even as they delivered their fourth straight 75 basis-point interest-rate increase.

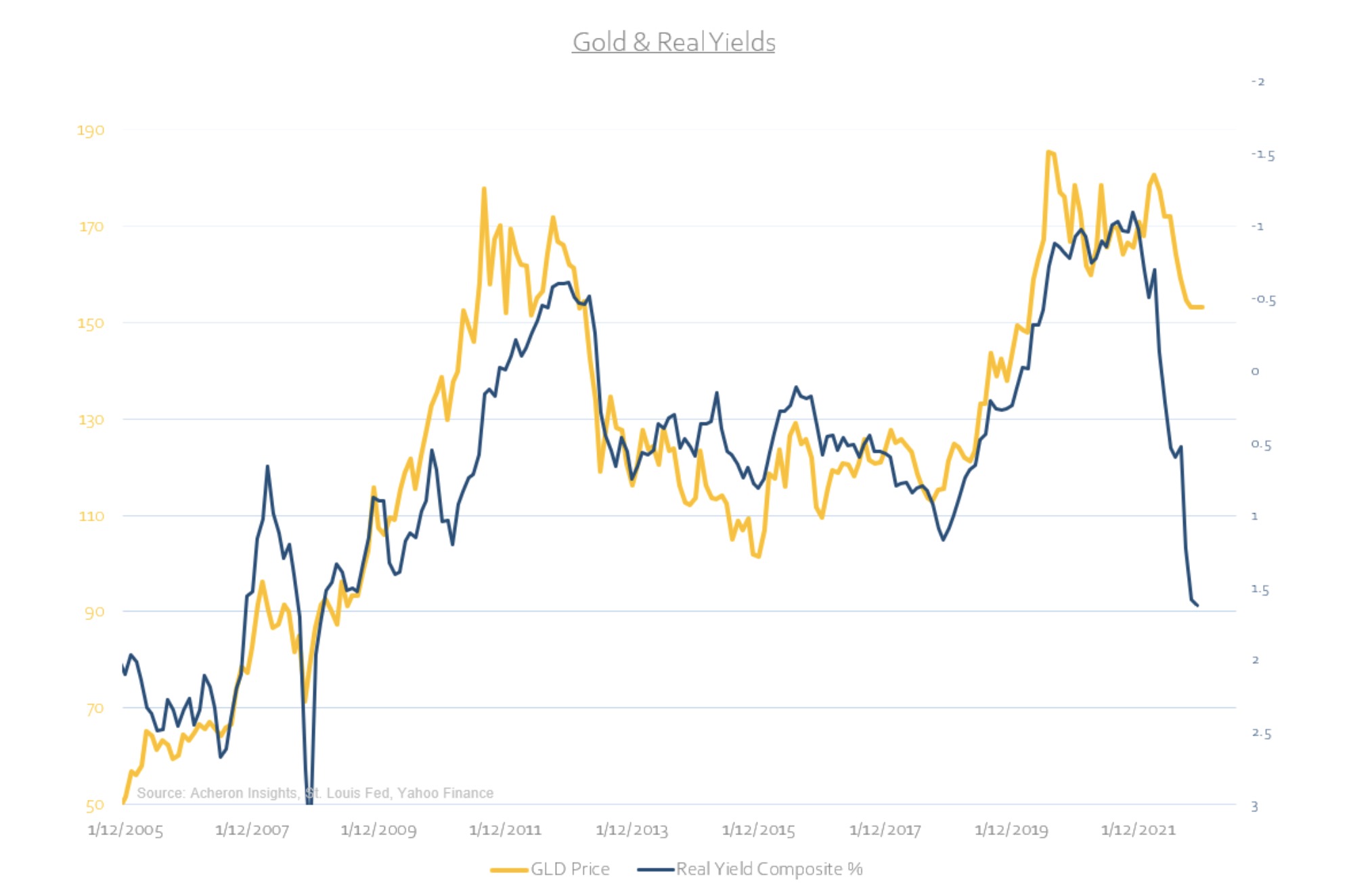

Rising and positive real yields continue to be a major headwind for gold over the short-term.

When you have radiotherapy for prostate cancer, you need to drink a lot of water so that your bladder is “comfortably full.

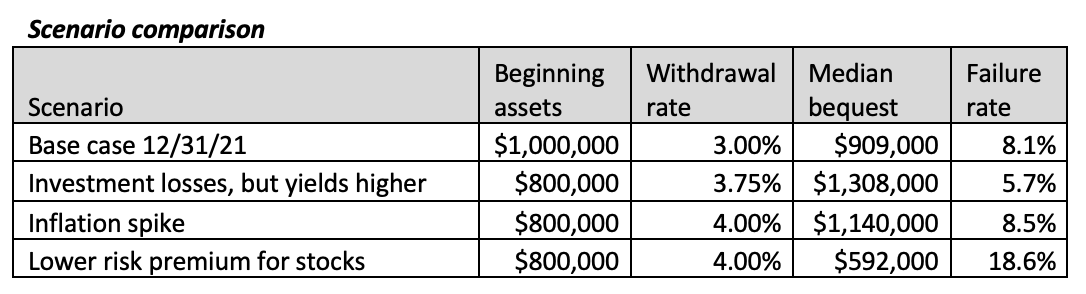

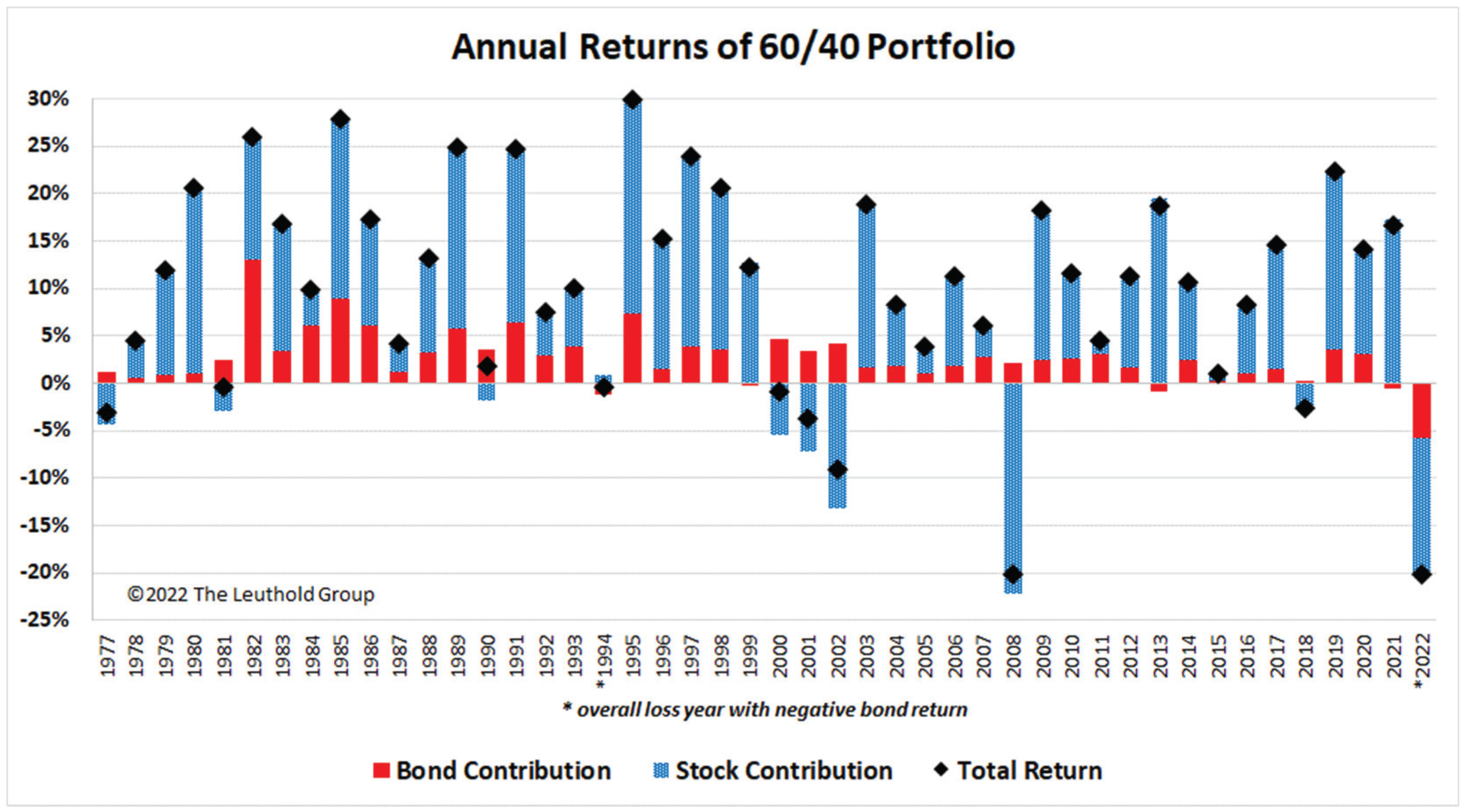

This year has been disastrous for stock and bond investors. But things are not as grim when viewed in a financial planning context that considers how the assets will be used, i.e., the liability or expense side of the household balance sheet.

We see central banks on a path to overtighten policy.

The final day to get Series I savings bonds at a record 9.62% yield has come and gone.

U.S. equities are declining, struggling to continue the past two week’s positive momentum.

It seems 2023 is arriving early. The race to raise interest rates to levels that have a hope of quelling inflation is entering a less punishing phase.

Governments will have to resist the temptation to address stagflation with stimulus.

The optimism that has crept into the US bond market is about to be put to the test.

Was it good or bad this week when Alphabet Inc. told investors that advertising demand that helped swell its top line 50% in two years is starting to soften?

Russ Koesterich, CFA, JD, Managing Director and Portfolio Manager, of the Global Allocation team discusses whether markets have bottomed or not.

A heap of distressed debt is expanding in the US corporate bond market and investors worry that a burst of defaults will follow.

It is unlikely that US corporate defined benefit (DB) pensions will have to face liquidity issues like those UK DB pensions recently witnessed, primarily because of their different approach to valuing liabilities, varying use of derivatives/leverage, and therefore a different investment style of liability-driven investing (LDI), according to Franklin Templeton Fixed Income’s Tom Meyers.

It was supposed to be the silver lining to a year of brutal losses. As bond-fund managers watched the market value of their portfolio decline rate hike after rate hike, one thing was certain: companies would soon have to return to the market offering juicier yields.

In this Global Macro Update, we discuss the trifecta of trends that caused the current inflationary environment… why an economic slowdown won’t cure inflation... the three sectors every investor should own today… and much more.

Short-term bonds currently offer higher yields than longer-term ones, but there are risks in holding only short-term bonds.

In these tumultuous times on Wall Street, at least one investing trend is proving remarkably consistent: Dividend ETFs are notching relentless inflows as traders take refuge in the stock-market storm.

The latest bear-market rally in US stocks has brought investors off the sidelines and provided a welcome reprieve from three quarters of gloom. But traders now need to ask themselves whether the risks continue to justify the potential returns.

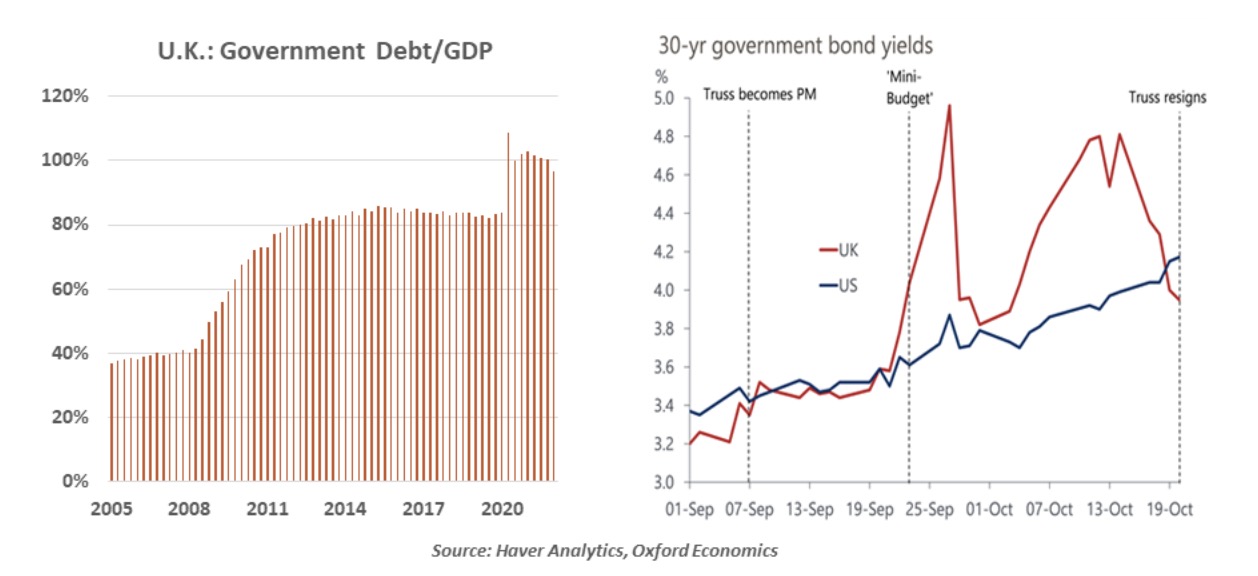

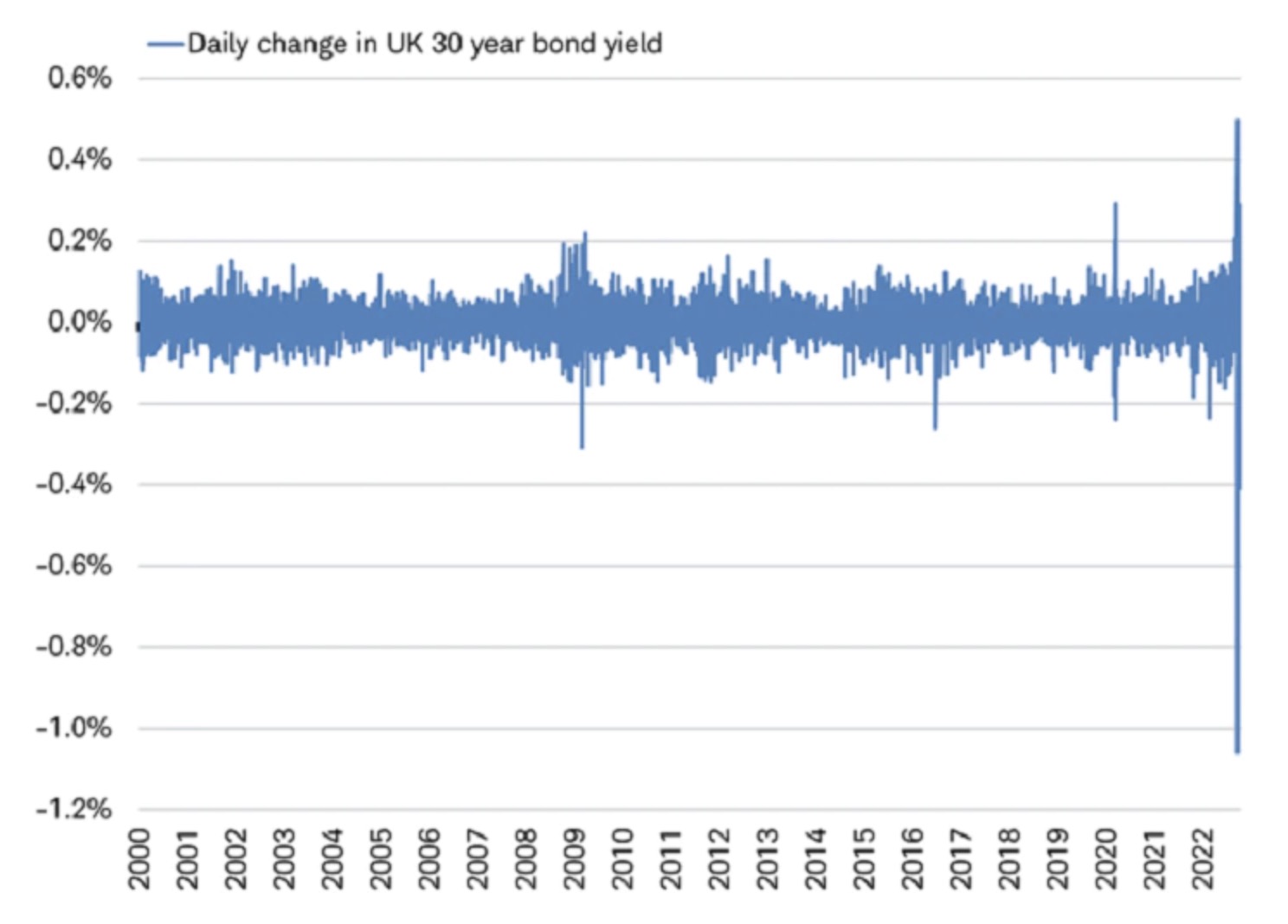

Markets can have more sway over policymakers than vice versa, as demonstrated in the U.K. recently.

The balanced portfolio strategy of allocating 60% to equities and 40% to fixed income generated a highly satisfactory 7.9% annualized return over the last 30 years.

A classic recession warning is flashing in the US Treasury market, where the 10-year note’s yield fell below the three-month bill’s, a rare occurrence that signals investors anticipate dire economic consequences of the Federal Reserve’s campaign against inflation.

In this piece, we update our valuation charts and commentary, with additional details on our methodology available upon request.

Bond yields may keep rising, but a significant driver of yields is done selling.

It is difficult to convince yourself that if things are going a certain way they will not continue down the same path indefinitely.

U.S. stocks are trading mixed in pre-market action.

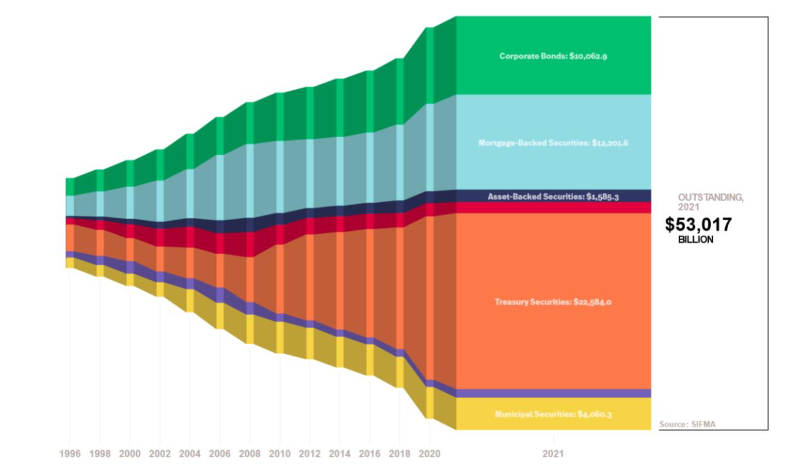

There are lots of “total return” bond funds these days, almost a half century since I innovated the concept in 1987.

I built a 4.36% real (inflation-adjusted) systematic withdrawal portfolio using a 30-Year TIPS ladder.