I built a 4.36% real (inflation-adjusted) systematic withdrawal portfolio using a 30-Year TIPS ladder.

I built a 4.36% real (inflation-adjusted) systematic withdrawal portfolio using a 30-Year TIPS ladder.

In June, I wrote about safe spend rates and concluded that a balanced portfolio could only support a 3.3% real withdrawal rate for a 30 year period with a 90% chance of success. There are differing opinions on what a safe spend rate should be. For instance, Mark Hulbert recently wrote in Barron’s that a 1.9% withdrawal is more appropriate.

At the suggestion of Bob Huebscher, the editor of this publication, I decided to try something different. I built a strategy backed by the U.S. government with Treasury Inflation Protected Securities (TIPS) that supports a reasonably level real 4.3% withdrawal rate for 30 years. It’s not perfect, but it was good enough for me to put my money behind it. I implemented such a portfolio with just under $100,000 of my own family’s nest egg.

First a little background and then I’ll get to the specifics of what I did and how you can do it too.

Background

A couple of weeks ago, I wrote about six good things in this horrible market. One was that TIPS suddenly had attractive positive real yields rather than the negative rates for the past few years. Bob sent me an email stating that this could guarantee a 4% safe withdrawal rate. It took me a little time to digest, but I started playing with the math.

At the time, 30-year TIPS had a real 1.73% yield. I plugged it into a spreadsheet and got a 4.23% real safe withdrawal rate for 30 years before it was exhausted. Of course, this is theoretical as the volatility of 30-year TIPS is considerable so we can’t count on selling some every year at a fixed price. For example, the PIMCO 15+ Year US TIPS ETF LTPZ was down nearly 35% YTD as of October 19, 2022. And, of course, fees take from the return.

For the strategy to work, one would have to build it with individual TIPS maturing each year to be assured of a certain real amount. I had only bought TIPS through funds and buying individual TIPS in the secondary market was harder than I thought.

I knew the basics of Individual TIPS. They have a fixed real yield plus an adjustment of principal based on the CPI-U. The IRS taxes both the distribution and the increase in principal; the latter is known as phantom income. They are state tax-exempt. Building it in an IRA solves the phantom income tax issue but loses out on the state tax-exemption.

One complication is that there are no TIPS that mature between 2033 and 2039 so I know I’d have to do a work-around of buying a few years in both 2032 and 2040. Much like the nominal yield curve, the TIPS yield curve was flat with attractive short-term yields making it a great time to build such a ladder to get a higher safe withdrawal rate.

Building the TIPS ladder

There are a total of 50 TIPS maturities issued by the U.S. government outstanding. I started building a spreadsheet but then discovered eyebonds.info and an easily downloadable and free spreadsheet that did the heavy lifting for me. It was written by Bob Hinkley, a retired corporate financial analyst and computer programmer and well respected contributor in the Bogleheads forum. I kicked the tires and compared outputs to my own spreadsheet until I felt reasonably comfortable. I was able to use this spreadsheet to back into an average annual real amount I could receive with roughly a $100,000 investment. The spreadsheet even told me which bonds to buy and in which quantity.

At this point, I’m still dallying in the land of theory. Buying the individual TIPS is another matter. The pricing on the eyebonds.info spreadsheet was a couple of weeks old, and the spreads are much larger buying tiny quantities of 2-4 bonds in the secondary market. Each bond is $1,000 par plus the accumulated increase in principal from the CPI-U adjustments. Would anyone even be willing to sell me a few bonds?

It wasn’t easy. I built the bond ladder on the Fidelity platform. I had to find bond lots where the seller was willing to sell lots as small as one bond and often found that the order didn’t execute even though I met the seller’s ask price and quantity. Some orders had to be placed multiple times and it took two calls to the bond desk. But it worked and below are the results.

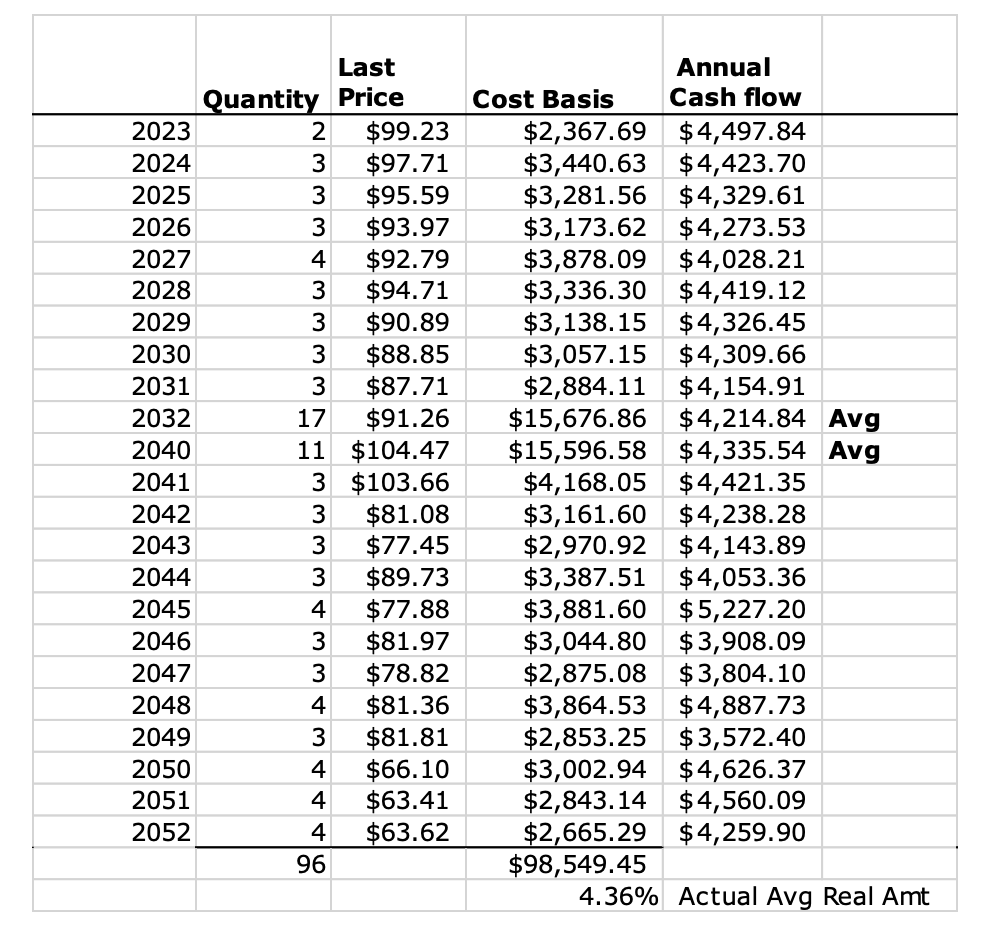

I spent $98,549 to produce an average cash flow of $4,296 annually, which equates to a 4.36% real average annual withdrawal rate. I’ll get back a total of $128,882 in today’s dollars or a real annualized return of 1.83%.

Because no TIPS mature between 2033 and 2039, I bought five years’ worth of bonds that mature in 2032 to last until 2036, and four years’ worth of bonds maturing in 2040 knowing they will be short-term in 2037, and later with far less volatility than long-term TIPS. I consider the risk of those few years minimal.

The average cash received each year is a real $4,296, but there is variation with a low of $3,572 and a high of $5,227. Had I bought larger amounts (like building a $1 million ladder), the annual cash flow would have been far more consistent.

Finally, after purchasing the bonds, I shared my results with Bob Hinkley who concurred with the results of the TIPS ladder I built from his eyebonds.info spreadsheet. The theory was successfully implemented and I’m likely to do more.

Conclusion

While this strategy isn’t perfect, it produced a safe 4.3% annualized real withdrawal rate for 30 years with no risk (except for the bonds between 2033 and 2039). Think of it as a 30-year period-certain inflation-adjusted portfolio. One large difference between this strategy and the 3.3% real withdrawal rate from a balanced portfolio is that there is a 90% probability that the latter will leave money after 30 years. I wouldn’t rely entirely on a TIPS ladder even though it’s inflation protected and backed by the U.S. government.

This strategy protects against inflation, which is justifiably on many clients’ minds and provides comfort knowing that a calculated specific real amount of spending power will be available each year. This is a very attractive strategy for someone wanting a guaranteed inflation-adjusted cash flow in addition to Social Security.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

Read more articles by Allan Roth

I built a 4.36% real (inflation-adjusted) systematic withdrawal portfolio using a 30-Year TIPS ladder.

I built a 4.36% real (inflation-adjusted) systematic withdrawal portfolio using a 30-Year TIPS ladder.