This year has been disastrous for stock and bond investors. But things are not as grim when viewed in a financial planning context that considers how the assets will be used, i.e., the liability or expense side of the household balance sheet. Interest rates have increased a lot, which means the present value of future spending declines. I’ll use an example of someone at retirement age to illustrate the impacts.

This year has been disastrous for stock and bond investors. But things are not as grim when viewed in a financial planning context that considers how the assets will be used, i.e., the liability or expense side of the household balance sheet. Interest rates have increased a lot, which means the present value of future spending declines. I’ll use an example of someone at retirement age to illustrate the impacts.

Interest rates

Year-to-date through mid-October, the 10-year Treasury yield increased from 1.52% to 3.67%, and the 30-year went from 1.90% to 3.73%. There have been similar increases in real yields – 10-year inflation protected securities (TIPS) have gone from yielding a negative 1.04% to a positive 1.43%, and the 30-year has risen from -0.44% to +1.58%. Real yields have very quickly moved much closer to the long-term average of 2% or a bit more, after being negative or close-to-zero since the great financial crisis.

It’s straightforward math to demonstrate how interest rate increases result in market value losses for bonds and bond funds. For example, if we put the cash flows from a 20-year, 2% bond into a spread sheet, and calculate the present value at 4%, it comes to about 73% of the par value, equivalent to a market value decrease of 27%. By way of illustration, the Vanguard long-term Treasury fund, similar in duration to this 2% bond example, is showing a YTD loss of 30% through mid-October.

There are also indications that stock market losses reflect the increase in interest rates, although the math is not as direct as with bonds. The market value of a stock can be thought of as the present value of the future cash flows from owning the stock (dividends, buybacks, and future sale price). Of course, the timing and amounts of these future flows are much less certain than for bonds, but those flows get discounted more when interest rates increase. U.S. stocks are down about 25% through mid-October, and my assessment is that much of that decline for both bonds and stocks was from the increase in interest rates.

Future expenses

We can now turn to the expense or liability side of the household balance sheet. For example, if have a new retiree who plans to utilize their savings to spend $30,000 per year (with annual inflation increases) and we assume a 30-year retirement, we can calculate present values using TIPS yields, because the future spending is in real dollars. If we use a TIPS yield of -0.5%, from the beginning of 2022, the present value comes out to $974,000. Because the assumed TIPS yield is negative, this amount exceeds the total future cash flow of $900,000 in real dollars. If we then raise the TIPS yield to the present-day positive 1.5% and redo the PV calculation, we get $720,000

The present value of future expenses decreased by 26%.

If we assume a new retiree invested in 60% Vanguard Total Stock Market Index (-24% YTD) and 40% Vanguard Intermediate Term Treasury (-12% YTD) they would be down 20% for the year on the asset side, but down 26% on the liability or future expense side. They would be ahead of the game. That’s quite a different picture than their quarterly investment statements have been showing.

Although this result might seem to involve finance sleight of hand, the explanation is quite straightforward. In bond-math terms, this is a case where the duration of the expenses exceeds the duration of the assets, so there is a greater impact on the PV of future expenses.

Retirement-planning model

To connect this example to retirement planning, I’ll run some examples using a Monte Carlo retirement simulation model. This will better illustrate the underlying assumptions built into the model, and I will expand this to include the impact of higher inflation – a negative in terms of retirement viability.

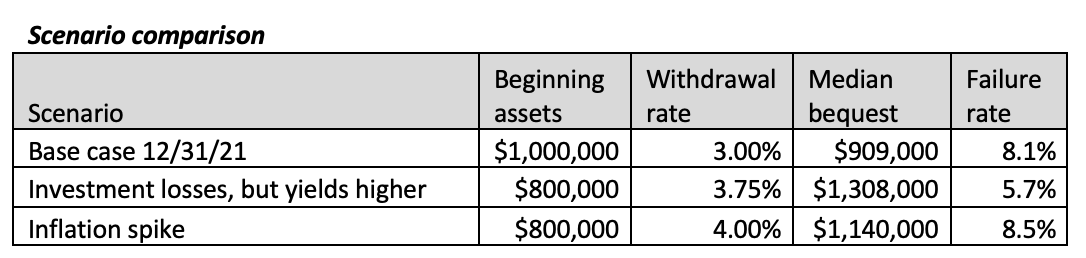

The base case for this analysis is a 30-year retirement scenario for an individual with $1 million in savings split 60/40 stock/bond, and an investment environment reflective of year-end 2021. The average investment return for the bond portion is assumed to be 2% nominal and -.5% real, reflecting 2.5% future inflation. I assume an expected equity premium of 7% based on the long-term historical average, so the arithmetic average stock return assumption is 9% nominal, 6.5% real. Standard deviations are 7% for bonds and 20% for stocks based on long-term history.

I assume annual withdrawals of $30,000 increasing each year based on 2.5% inflation. I’ve chosen this 3% withdrawal rate (less than the classic 4%) to reflect lower-than-historical investment returns that tie in with the lower-than-historical bond yields at the beginning of this year.

The chart below is based on 5,000 Monte Carlo retirement simulations using the above assumptions. For key performance measures, I show the median bequest remaining at the end of the 30-year retirement and the failure rate – the percentage of the 5,000 simulations that deplete savings before the end of 30 years.

For our starting base case, we generate a median bequest of $909,000 in real 2022 dollars, and 8.1% of the simulations fail.

Next I change the scenario to reflect what has happened so far in 2022. Based on the 60/40 Vanguard scenario discussed earlier, beginning assets are reduced by 20% to $800,000. We now need a 3.75% withdrawal rate to generate the $30,000 in annual real withdraws1. But, on the positive side, bond interest rates have increased by 2% to 4% or 1.5% real. I assume the same risk premium for investing in stocks, so the average stock return assumption also increases by 2%. The chart below compares the results for this scenario with the base case.

The perhaps surprising result is that both the median bequest and failure rate improves, even though we start off with a 20% hit to savings and need to increase the withdrawal rate. This result mimics the analysis in the previous section that showed a 26% reduction in the present value of future spending compared to a 20% asset loss based on a 60/40 Vanguard portfolio.

Inflation

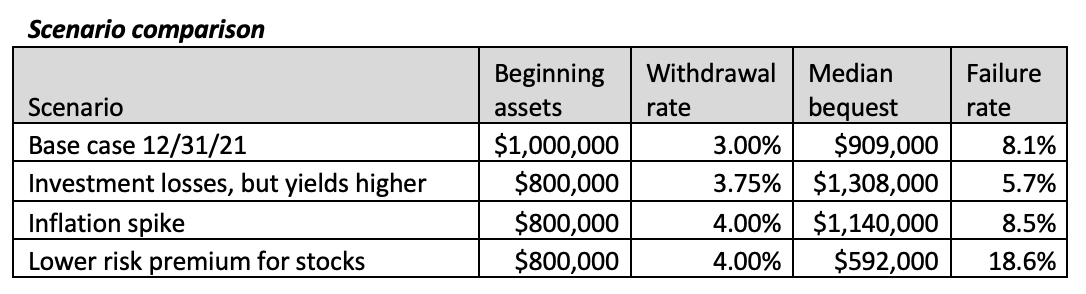

Bouts of high inflation pose a serious problem for retirement plans because they ratchet up the amount of spending needed to maintain purchasing power, and that impact carries through for the remainder of retirement, even after inflation drops back to more normal levels. To model such an inflation scenario, I’ve assumed starting off with 8% inflation for 2022, and 4% for 2023 before dropping back to a base level of 2.5% annually, and I’ve added this to the above case where assets drop by 20%. To continue to generate $30,000 of real withdrawals, we now have to raise the withdrawal rate to 4%.

The chart below adds a line for this result, and we see that we are now pushed back closer to the original scenario in terms of median bequest and failure rate. But the good news is that the retirement plan has withstood both a significant drop in assets and a spike in inflation.

Return assumptions

The key assumption underlying good news is that we can achieve higher returns after experiencing losses. For bond returns things are quite straightforward – current yields are a reliable indicator of long-term returns and current bond yields have increased a lot. And they are still a bit below long-term averages, so there is no compelling reason to expect a sudden drop.

However, for stocks things are more uncertain. There is the general uncertainty about future stock returns. Even if expected returns increase, there is a wide range for future actual returns. There is no anchor like there is for bonds. But to make projections, it is necessary to make assumptions, and it is reasonable to assume that investors will demand the same premium for taking stock market risk as they did before interest rates increased. Therefore, I assumed no change in the risk premium for stocks. For this analysis of before-and-after impacts, the level of risk premium assumed is not as important as the assumption about whether the risk premium changes.

To highlight the importance of this risk premium assumption, I’ve added a line to that chart to show what would happen if the stock return assumption didn’t change, so the risk premium dropped by 2%. However, my own view is that an unchanged risk premium for stocks is a more reasonable assumption.

Discussion

What’s important in this analysis are not the numbers I have chosen, as much as the general concept of looking beyond investment statements when assessing the impacts on financial plans. Be cognizant of both sides of the financial planning balance sheet. There will always be challenges in communicating with clients, because it’s only natural that market values on investment statements will be seen as facts and attempts to forecast potential futures may be viewed as fiction – all dependent on the assumptions. But advisors need to be more aware of the full picture.

Joe Tomlinson is an actuary and financial planner, and his work mostly focuses on research related to retirement planning. He previously ran Tomlinson Financial Planning, LLC in Greenville, Maine, but now resides in West Yorkshire, England.

1In an article last week, Allan Roth demonstrated that a 30-year TIPS ladder can support 4.36% risk-free withdrawals, further emphasizing the financial planning benefits that are a consequence of higher real rates.

This year has been disastrous for stock and bond investors. But things are not as grim when viewed in a financial planning context that considers how the assets will be used, i.e., the liability or expense side of the household balance sheet. Interest rates have increased a lot, which means the present value of future spending declines. I’ll use an example of someone at retirement age to illustrate the impacts.

This year has been disastrous for stock and bond investors. But things are not as grim when viewed in a financial planning context that considers how the assets will be used, i.e., the liability or expense side of the household balance sheet. Interest rates have increased a lot, which means the present value of future spending declines. I’ll use an example of someone at retirement age to illustrate the impacts.