Who knew that the subject of US Treasury bond yields could inspire such passion? When, in late June, I argued that they were likely to move considerably higher than the then-prevailing 3.75%, I attracted some vehement pushback.

Interest rates are at 20-yr highs, yet unemployment is at 50-yr lows, core-PCE is near 30-yr highs, and Wall Street (and Fed) economic forecasts continue improving. What explains the disconnect between these unexpected outcomes and those expected by mainstream economic textbooks?

Whereas the U.S. is investing in new airport infrastructure and modernizing facilities to meet ambitious climate goals, European airports are choosing to combat emissions by restricting the number of flights.

If they’d been offered today’s economy a year ago – with inflation downgraded from emergency to mere headache, still-low unemployment, and growth that’s slowed without stalling – the world’s top central bankers would’ve taken it like a shot.

Over the past 12-24 months of rate hikes, short-term and ultra-short-term bond ETFs have served income-seeking investors well. But as interest rates continue to rise, exposures farther out on the curve have begun to offer attractive yields, too.

Recent data and policy developments have fallen firmly in the soft-landing camp, and market performance has reflected this shift. Notwithstanding recent stronger-than-expected economic activity, we continue to believe a downturn is in the pipeline.

Equity traders reeling from the market’s worst stretch since February face some pivotal events in the days ahead, and a closely watched speech by Federal Reserve Chair Jerome Powell may not even be the biggest test of all.

Convinced a recession in the US was near, some of the world’s most prominent money managers loaded up on government bonds this year in a bold bet that would atone for the punishing losses suffered in 2022.

Government bonds or stocks? If you were picking an asset class to outperform over the next 18-24 months, which would you choose?

My last three letters reviewed Neil Howe’s new book about the Fourth Turning. Today we’ll look at another set of patterns observed by my friend George Friedman in the geopolitical realm. George’s view of how patterns shape countries is different but not inconsistent with Neil’s generational cycles.

Progress toward a sustainable world would be hamstrung without the backing of global banks and their sponsorship of green and sustainable bonds.

We expect inflation and rates to remain higher than the last decade. We favor tech within growth and cyclicals within value.

European banks are rightly being criticized for failing to pass on interest-rate increases to customers. But is it any wonder they’re so unafraid of losing business? Compared to their US counterparts, European financial institutions often face less competition from alternative cash-like investments.

All around the world, bond traders are finally coming to the realization that the rock-bottom yields of recent history might be gone for good.

The fresh boom in stock options that expire within 24 hours has grabbed all the attention on Wall Street trading desks — spurring a Goldman Sachs Group Inc. warning that the activity is fueling the recent market selloff.

Today was a disaster for Chinese economic data. In the table below, we can see that every single data point missed consensus expectations in the wrong direction. Activity undershot expectations across the board.

With so much uncertainty remaining around the Fed’s rate cycle and the potential for recession, many investors are beginning to look toward international equity markets for the means to build income. Yields continue to look attractive for international dividend ETFs, in particular.

Federal Reserve officials at their policy meeting in July largely remained concerned that inflation would fail to recede and that further interest-rate increases would be needed. At the same time, cracks in that consensus were also becoming more apparent.

What if I told you that CPI is effectively at 2% now? Would the Fed's policy stance remain the same?

U.S. corporate earnings have stagnated for a year, but Q2 beat a low bar. Expectations of improving margins look rosy. We stay selective in equities.

JPMorgan Chase & Co. and Western Asset Management are among those saying this month’s jump in bond yields represents a buying opportunity, given central banks are getting close to the end of their rate-hike cycles.

It’s been an interesting first half of the year. Markets performed very well in the face of continued Fed tightening, calls for an imminent recession, a regional banking crisis, debt ceiling debate, and drama around an 11th-hour deal to avoid a default on U.S. debt.

The Agg is supposed to be to bonds what the S&P 500 Index is to equities. But it is an insufficient gauge for measuring the bond universe.

Investors are bailing out of the biggest exchange-traded fund devoted to Treasuries at the fastest pace since markets were hammered during the early months of the pandemic.

The yield on the 10-year note ended August 11, 2023, at 4.16%, the two-year note ended at 4.89%, and the 30-year at 4.24%.

We maintain a neutral-duration posture overall. We prefer an up-in-quality bias and have become increasingly selective in non-investment grades.

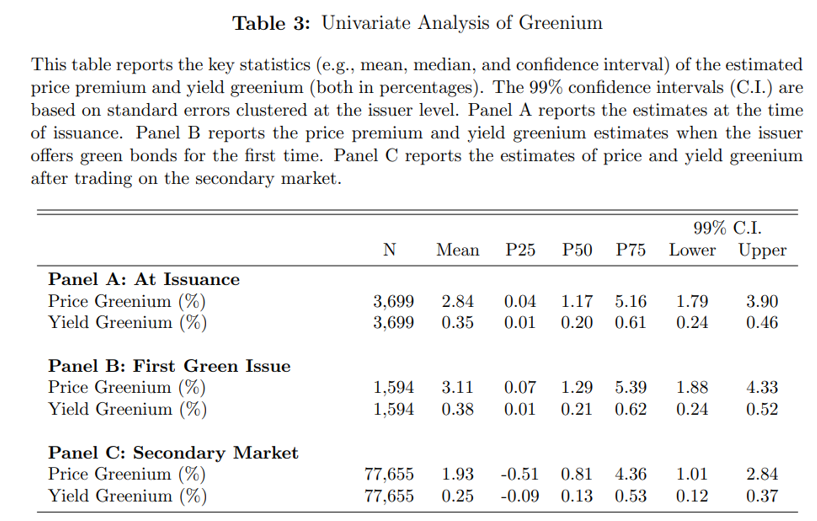

I’ve written previously about how positive (“green”) ESG metrics have increased the prices of stocks, reducing their expected returns. New research examines a similar effect in bonds, where a “greenium” (lower yield on green bonds versus non-green equivalents) reduces returns for investors.

Bankers are warning that tougher capital rules being proposed by the Federal Reserve and other US regulators will push more risks out of well-regulated lenders and into markets.

The old playbook of selling emerging-market bonds when Treasury yields spike is being upended by the positive dynamics favoring developing-nation debt.

Across Wall Street, there’s growing relief that the Federal Reserve — at long last — may be done raising interest rates. But that doesn’t mean turbulence in the bond market will soon become a thing of the past.

Given the current economic backdrop, where can investment opportunities be found, particularly within the fixed income asset class? Head of Franklin Templeton Institute Stephen Dover shares his key takeaways from a panel discussion that he moderated with fixed income experts within the company.

For the years following the Lehman crisis, the Fed put was the norm. Exceptionally loose monetary policy ensured risk assets had a safety net. But central banks were unable to rehabilitate the real economy while governments kept their belts tight.

Will the economy roll into a formal recession, or is a recovery underway? It's a close call.

A team of scientists claimed to have created a breakthrough material that could superconduct electricity at room temperatures and ambient pressure. But then people started trying to replicate the experiment.

For the better part of the last century, the largest companies in the world were those that produced physical property – traditional transportation machines, the energy that powered them, or the capital that financed them.

All of a sudden, the short-volatility trade is back on Wall Street as billions of dollars pour into options-selling ETFs like never before.

The potential for a Fed pause presents an opportunity for investors to consider adding duration back into their portfolios.

Inflation concerns are threatening to keep US Treasury yields higher for longer, worsening a slide in Asia stocks as investors sell chip shares after their recent rally.

Bond investors who have repeatedly gotten burned buying 20-year Treasuries since the US government reintroduced them in 2020 appear willing to conclude that this time will be different.

A key measure of US consumer prices rose only modestly for a second month, bolstering hopes that the Federal Reserve can tame inflation without sparking a recession.

This article takes a look at a long-term perspective on Treasury yields as of the July 31, 2023 close. The chart below shows the 10-year constant-maturity yield since 1962 along with the Fed funds rate (FFR) and inflation.

Do high-yield bonds still make sense for income investors at this stage of the credit cycle? We think so.

We see compelling value in high-quality, liquid fixed income assets that may offer potential resiliency if the economy weakens.

We see emerging markets better withstanding volatility and benefiting as supply chains rewire. We switch our EM debt preference to hard currency from local.

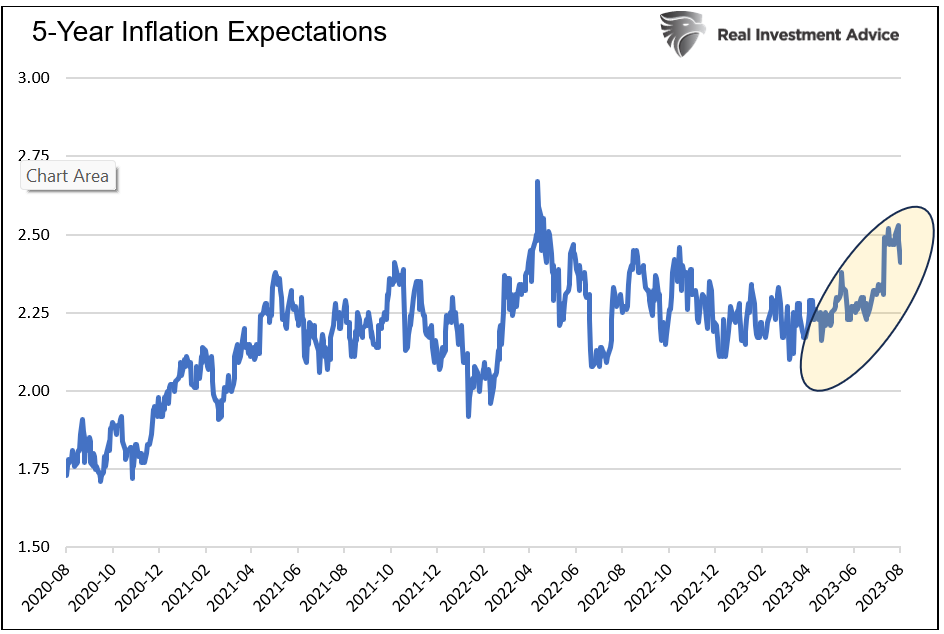

A closely watched bond market gauge of expected US inflation is rising back toward a nine-year high, signaling concern the Federal Reserve may continue to wrestle with elevated price pressures for years.

Bulging sales of US Treasuries are about to deliver a major test of investor demand and determine whether a selloff has room to run, as the market braces for the biggest round of refunding auctions since last year.

Coming into the year, over 60% of economists expected the economy to enter a recession in 2023. But the economy’s resilience, particularly in the wake of aggressive rate hikes, has surprised the market and supported better than expected earnings growth and the equity rally year-to-date.

Earnings season has thus far been a mixed bag, and despite a notable increase in the beat rate, the market is rightfully shifting focus to guidance for the rest of the year.

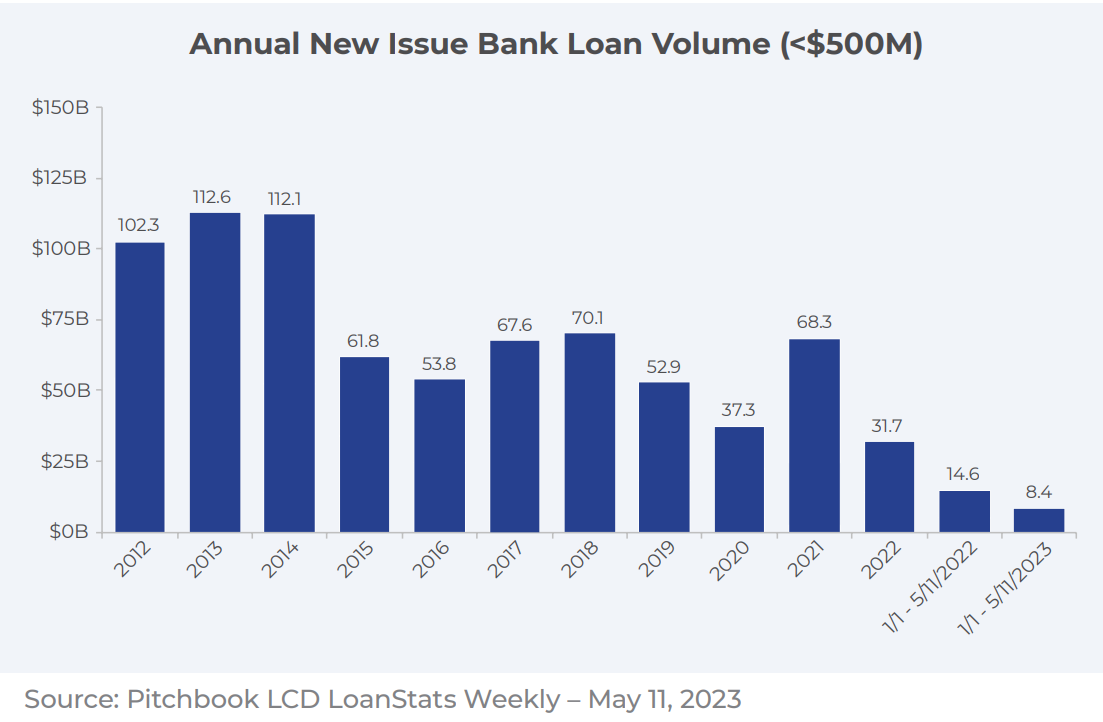

As the Fed tightens and banks accelerate their pullback from middle-market lending, private credit’s stability, strong downside protection and floating rate yields make it an attractive fixed income alternative.

Investors planning for retirement are facing seven significant challenges.