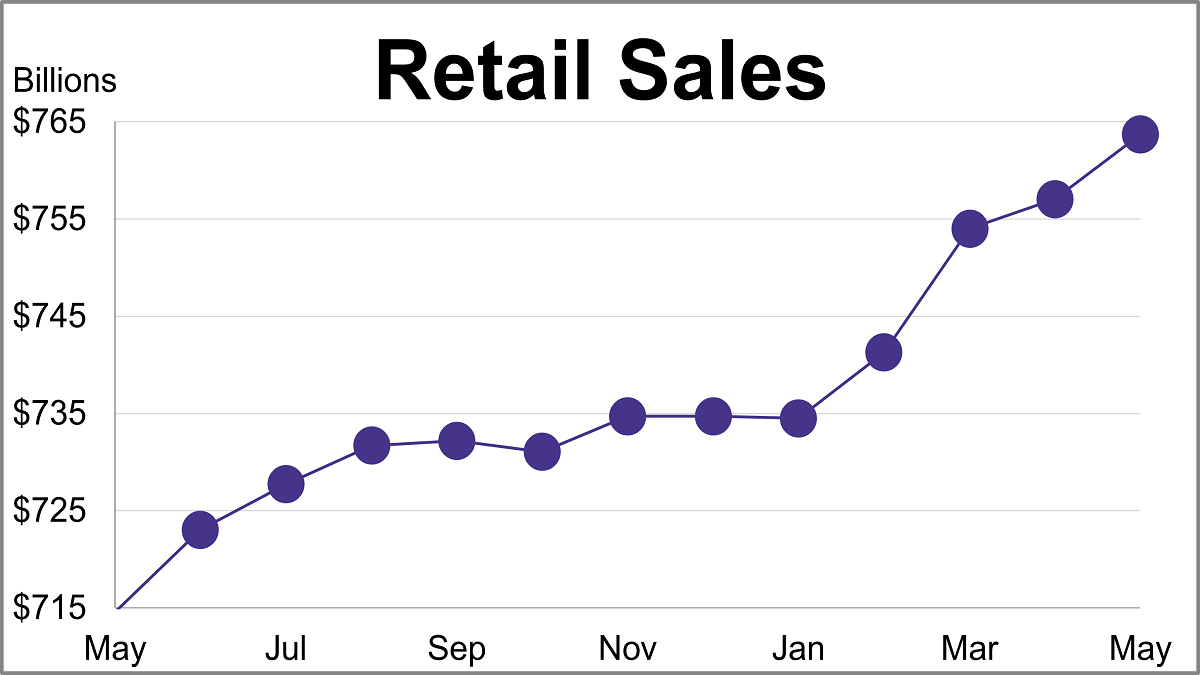

According to the Census Bureau’s Advance Retail Sales Report, consumer spending climbed for the fourth straight month in May. Headline sales rose 0.9%, almost double the projected 0.5% growth and marking an acceleration from April's 0.4% rise.

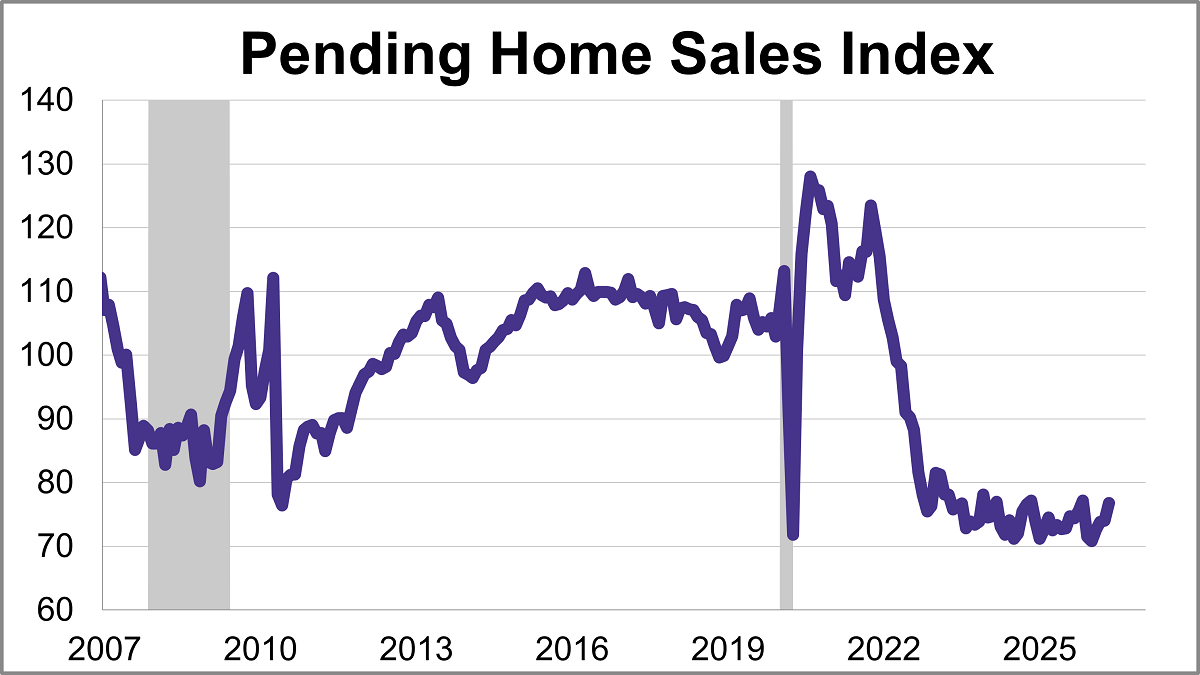

The National Association of Realtors® (NAR) pending home sales index jumped 3.8% in May to 76.8, marking its fourth consecutive monthly gain and highest level in six months.

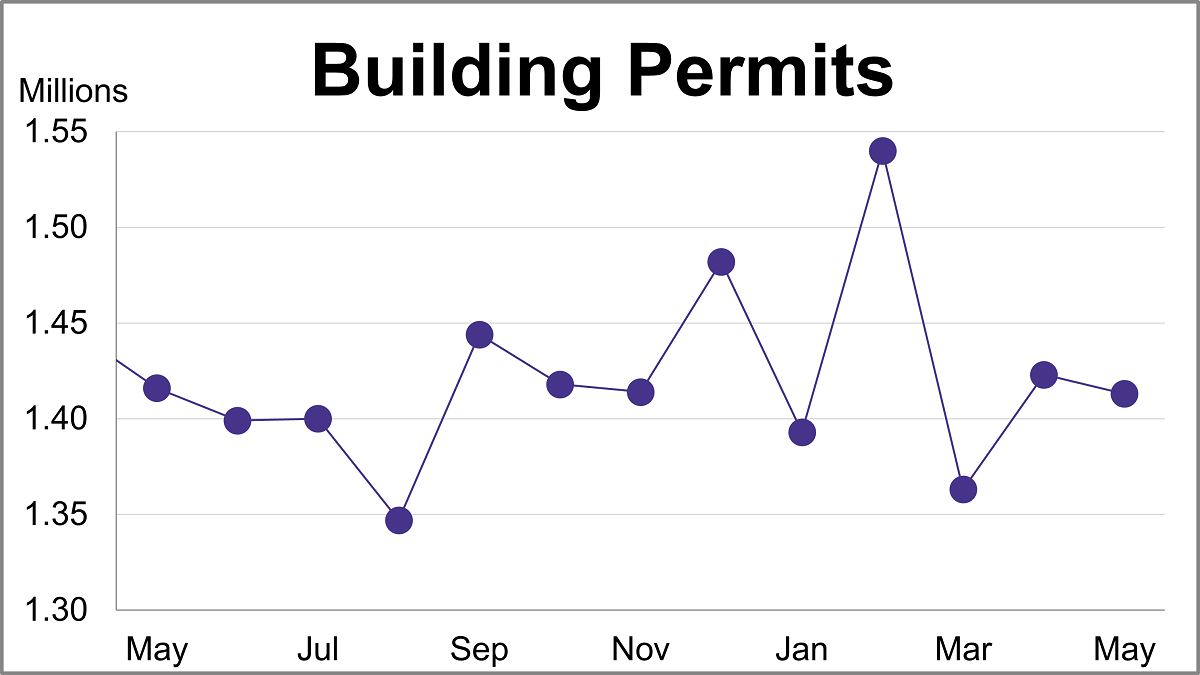

Building permits inched down 0.7% to a seasonally adjusted annual rate of 1.413 million in May. The latest reading missed the forecast of 1.420 million.

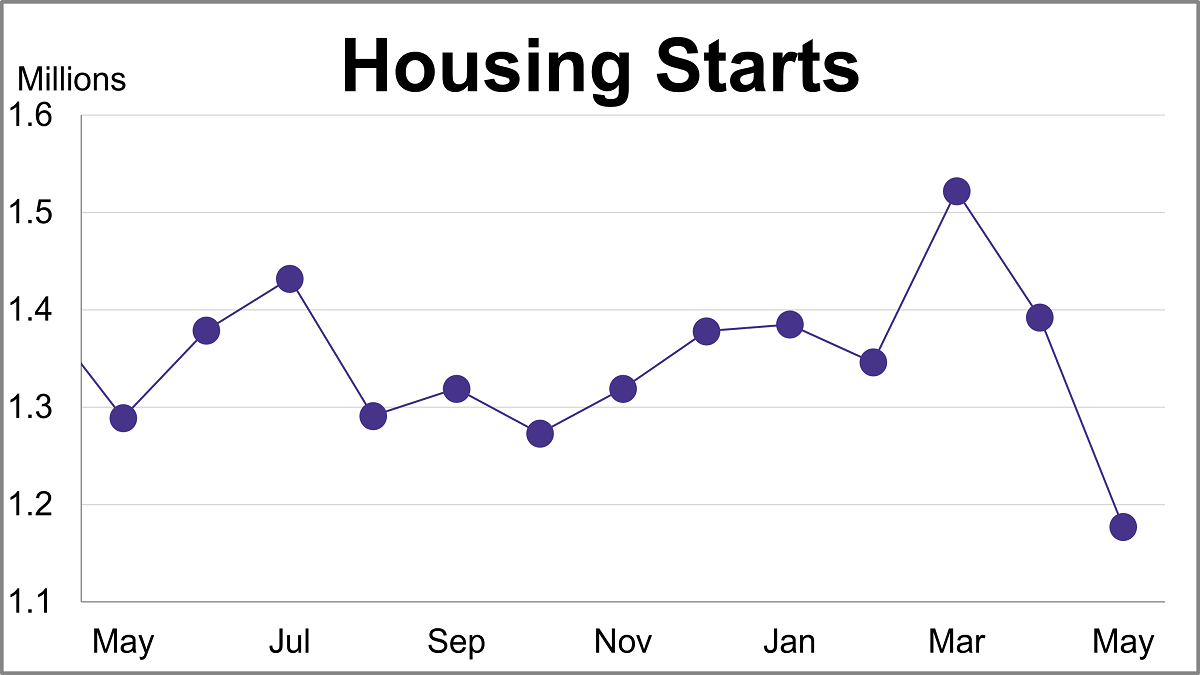

Housing starts sank 15.4% in May to a seasonally adjusted annual rate of 1.177 million, the lowest level in six years. The latest reading was significantly lower than the projected 1.430 million.

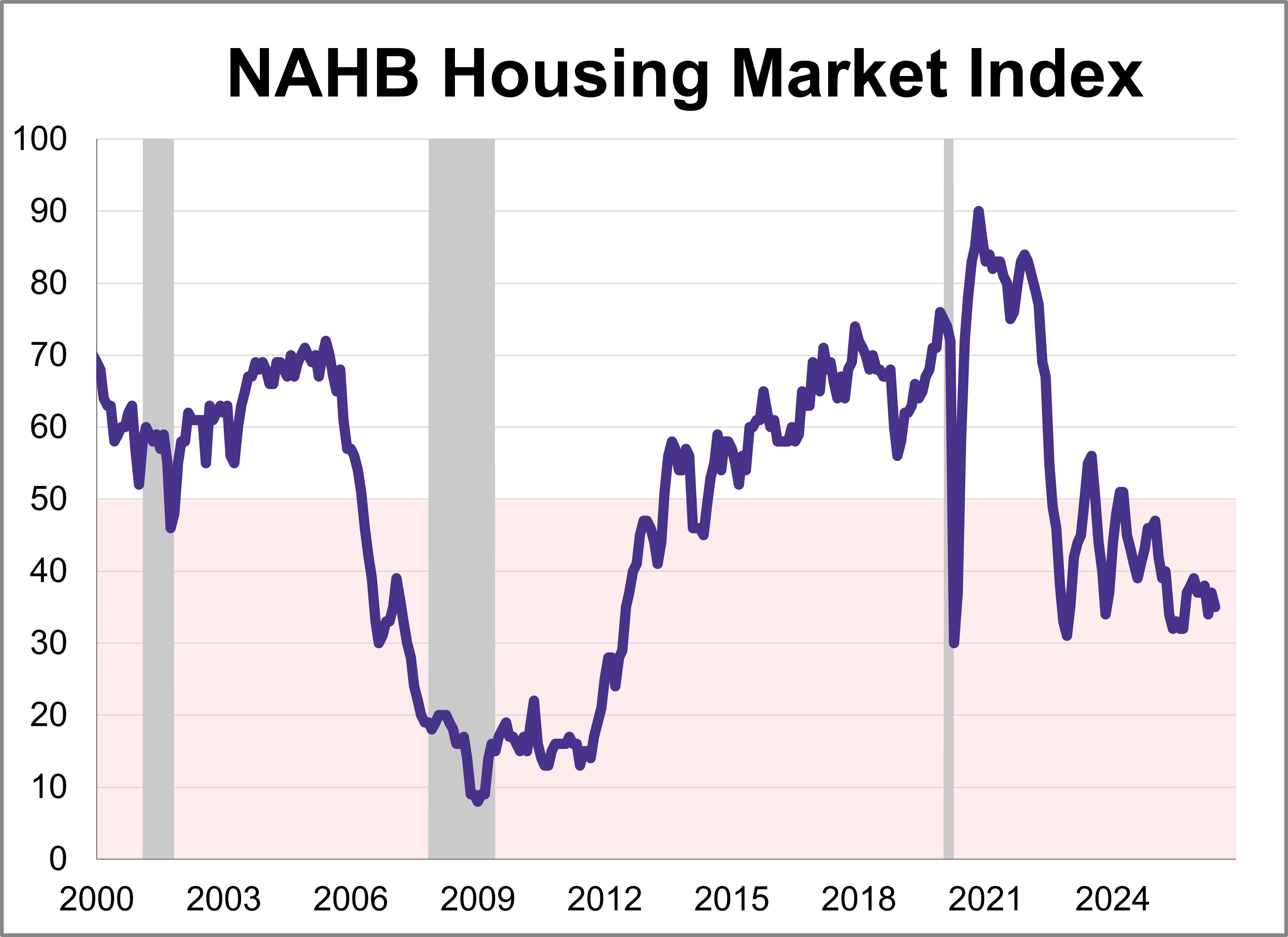

Builder confidence edged lower in June as ongoing affordability challenges continue to affect the housing market. The National Association of Home Builders (NAHB) Housing Market Index (HMI) fell 2 points from May to 35 this month, marking the 26th consecutive negative reading.

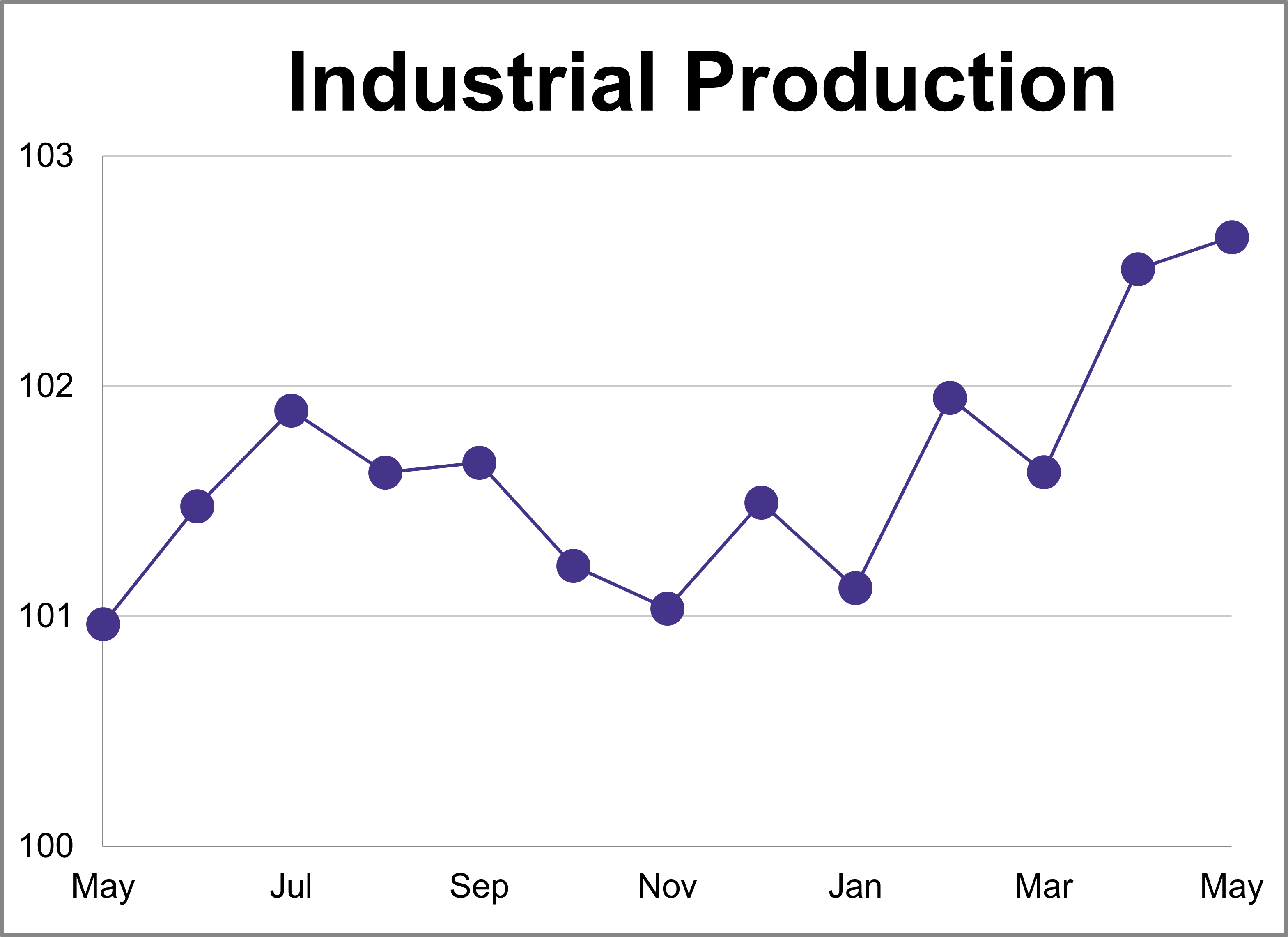

Industrial production rose less than expected in May, increasing 0.1% after a 0.9% jump in April. This was lower than the expected 0.3% growth and marks a 1.7% increase compared to one year ago.

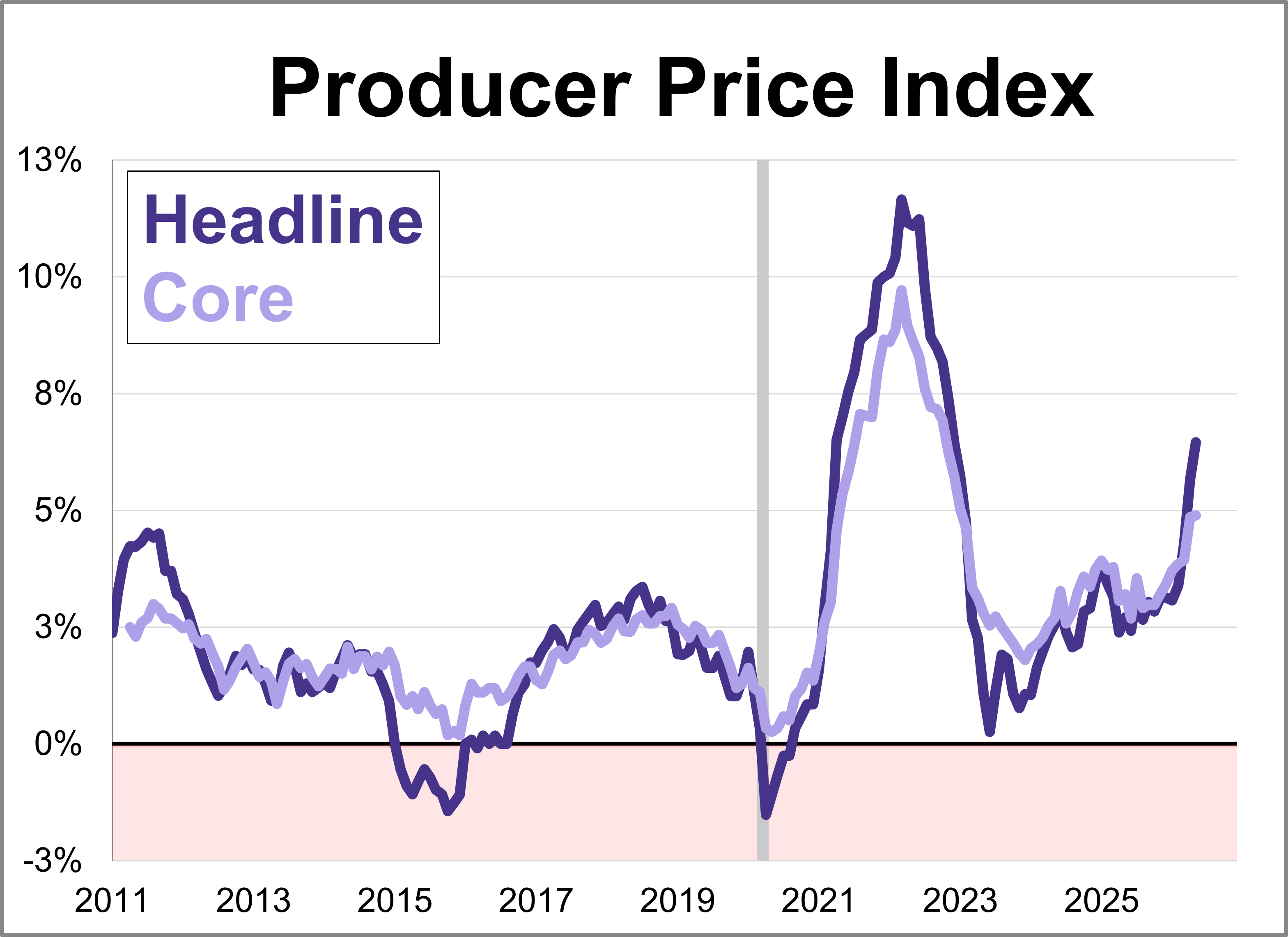

May's Producer Price Index (PPI) data delivered another blow to inflation watchers, as wholesale price growth came in hotter than expected.

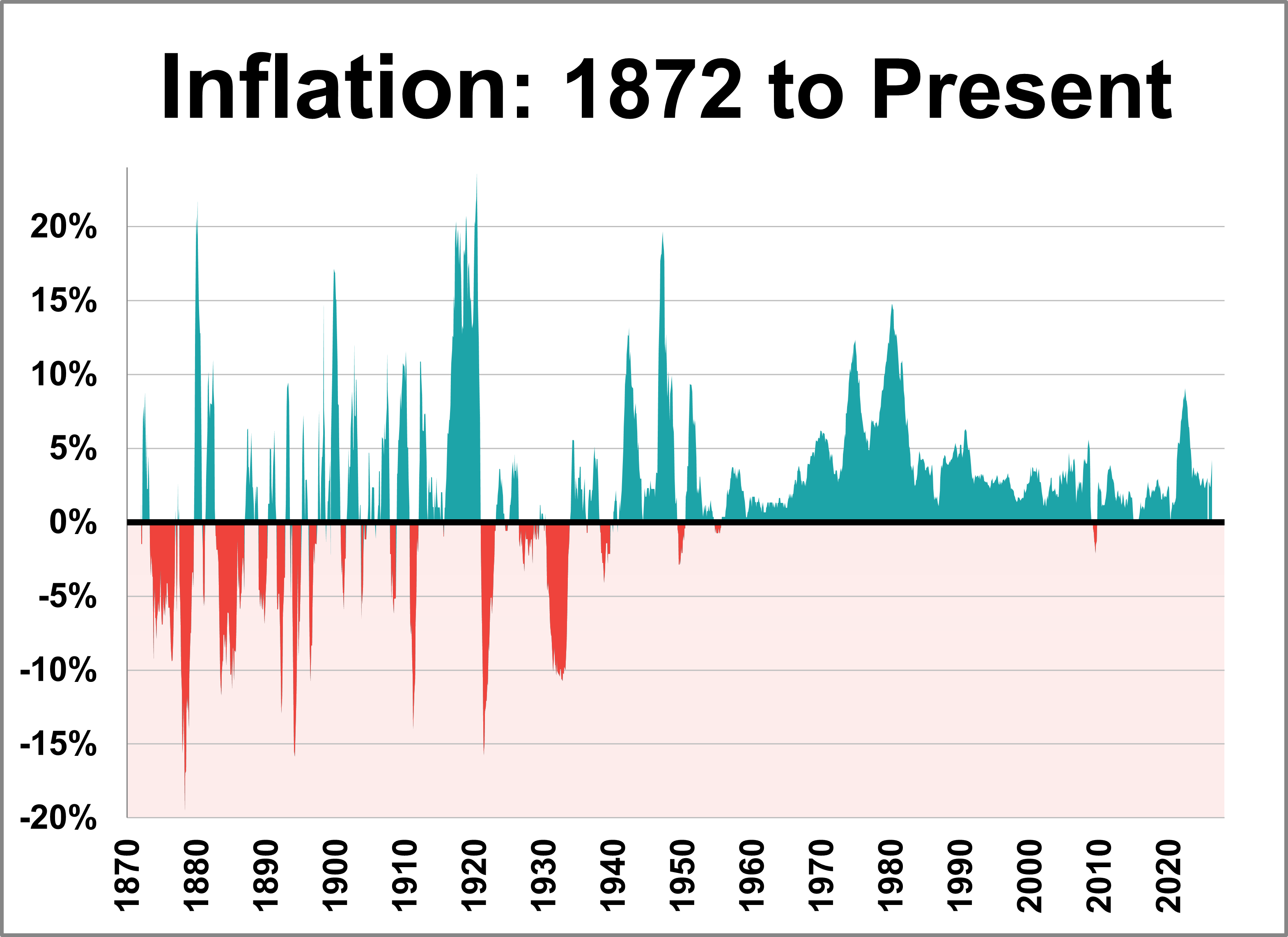

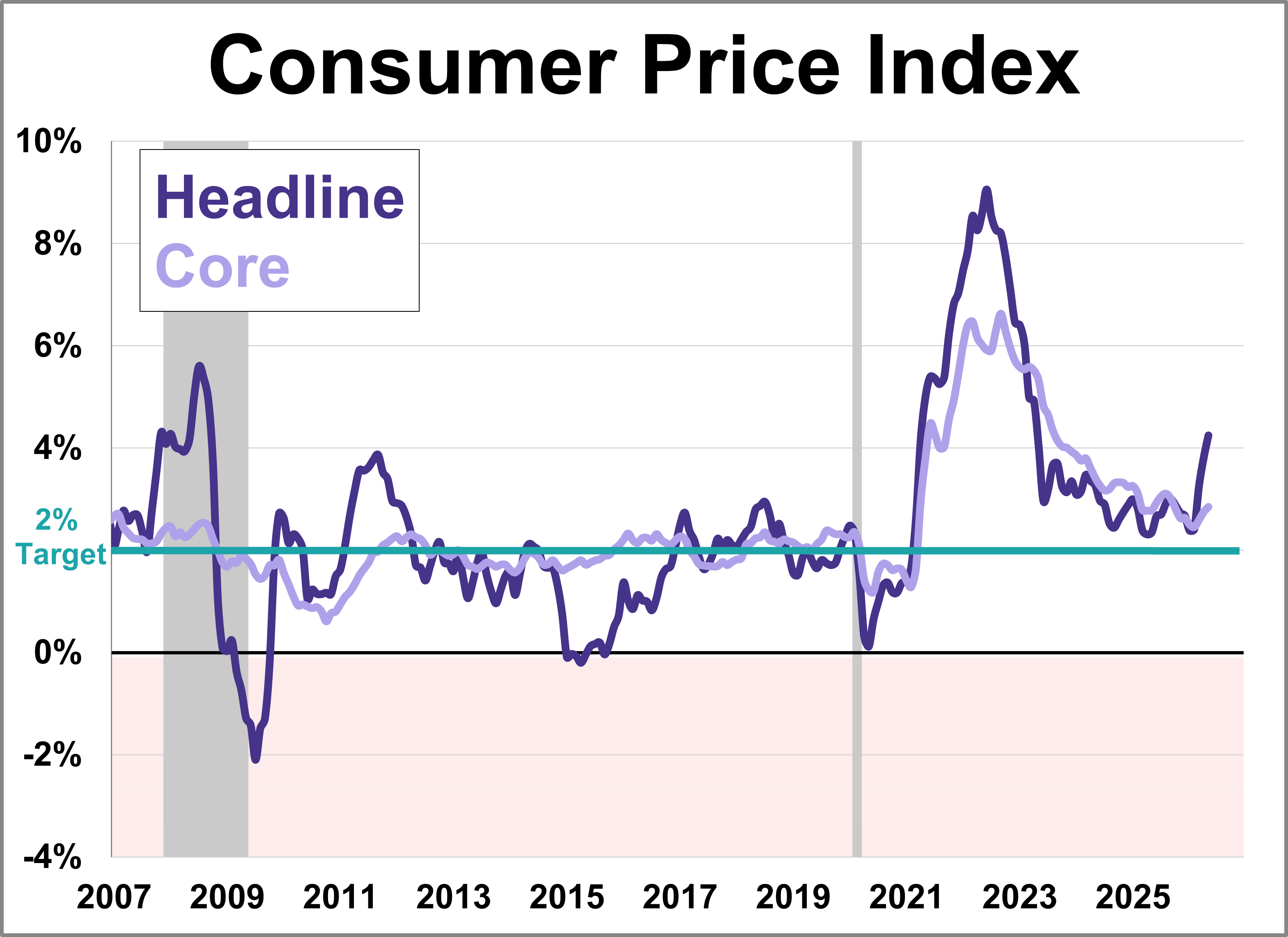

The May release of the Consumer Price Index for Urban Consumers (CPI-U) places the year-over-year inflation rate at 4.25%, its highest level in over three years. This keeps inflation above the post-WWII average of 3.72% for a second straight month and marks the third consecutive month that the current rate is above the 10-year moving average, which currently sits at 3.27%.

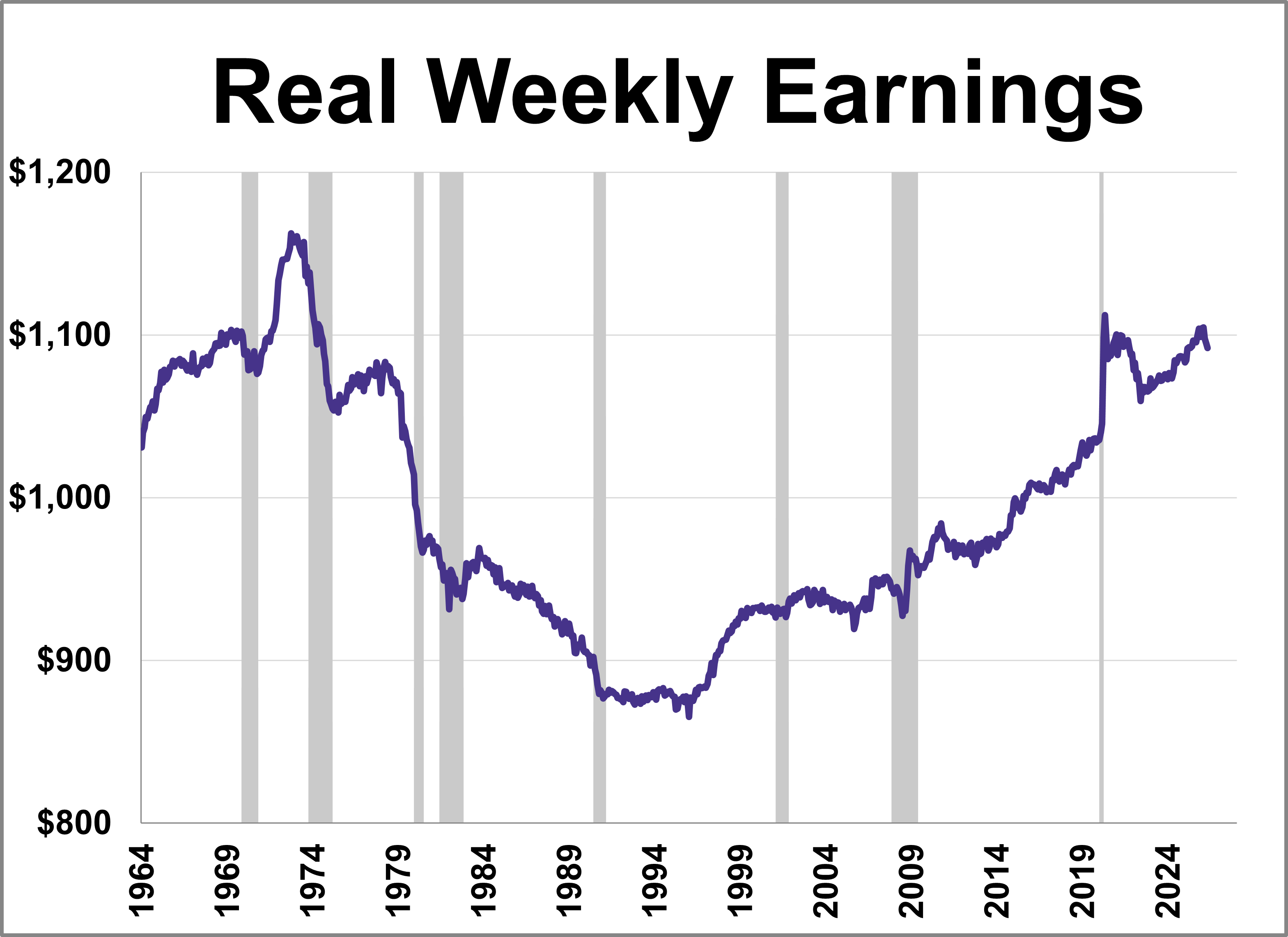

This series has been updated to include the May release of the consumer price index as the deflator and the monthly employment update. The latest hypothetical real (inflation-adjusted) annual earnings are at $54,604, down 6.1% from over 50 years ago.

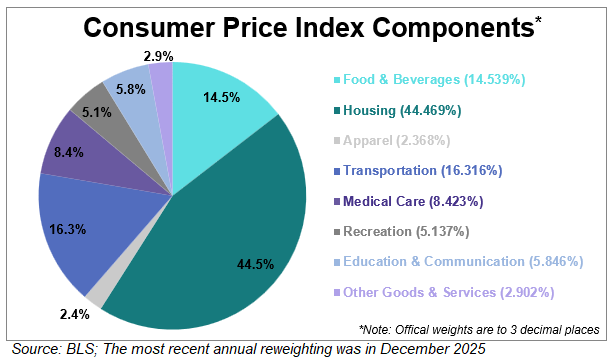

Inflation affects everything from grocery bills to rent, making the Consumer Price Index (CPI) one of the most closely watched economic indicators. The Bureau of Labor Statistics (BLS) tracks this by categorizing spending into eight categories, each weighted by its relative importance.

Inflation surged to 4.2% year-over-year in May, hitting its highest level in over three years. The headline figure for the Consumer Price Index (CPI) was consistent with the forecast, driven primarily by cost increases in energy, shelter, and food.

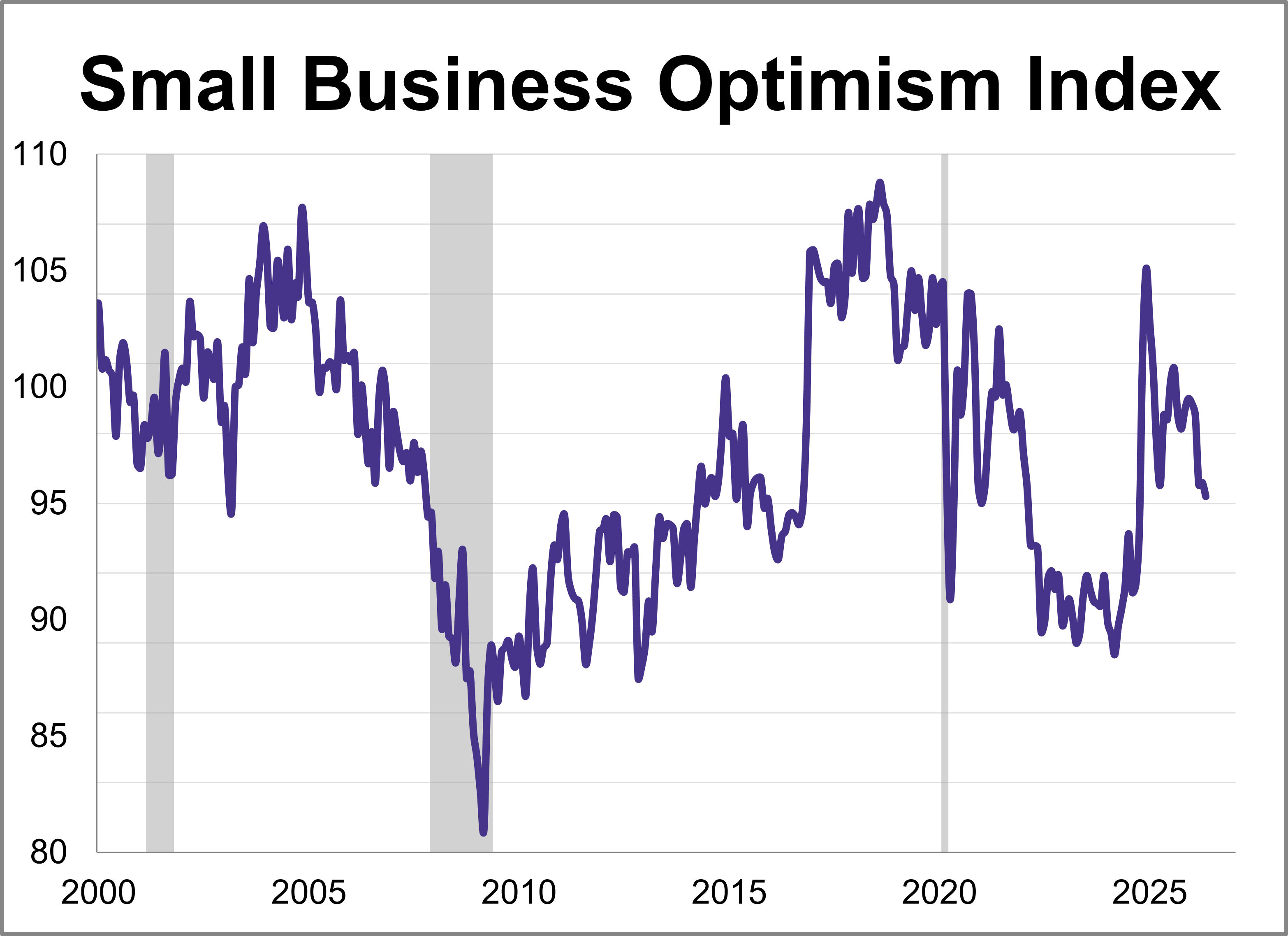

The NFIB Small Business Optimism Index dropped 0.6 points to 95.3, reaching its lowest level since October 2024. The index remains below its historical average for a third straight month.

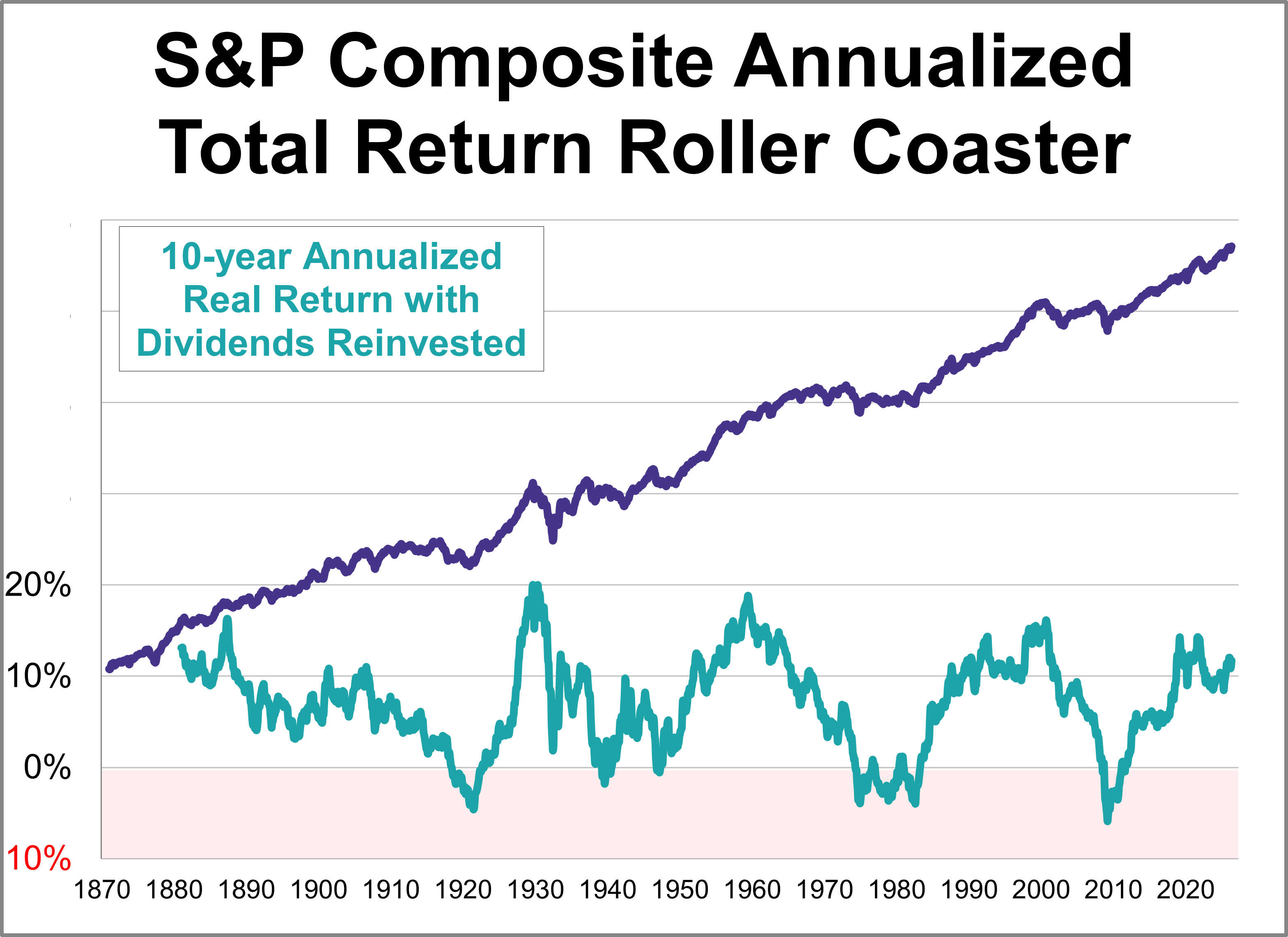

Here's an interesting set of charts that will especially resonate with those of us who follow economic and market cycles. Imagine that five years ago you invested $10,000 in the S&P 500. How much would it be worth today, with dividends reinvested but adjusted for inflation?

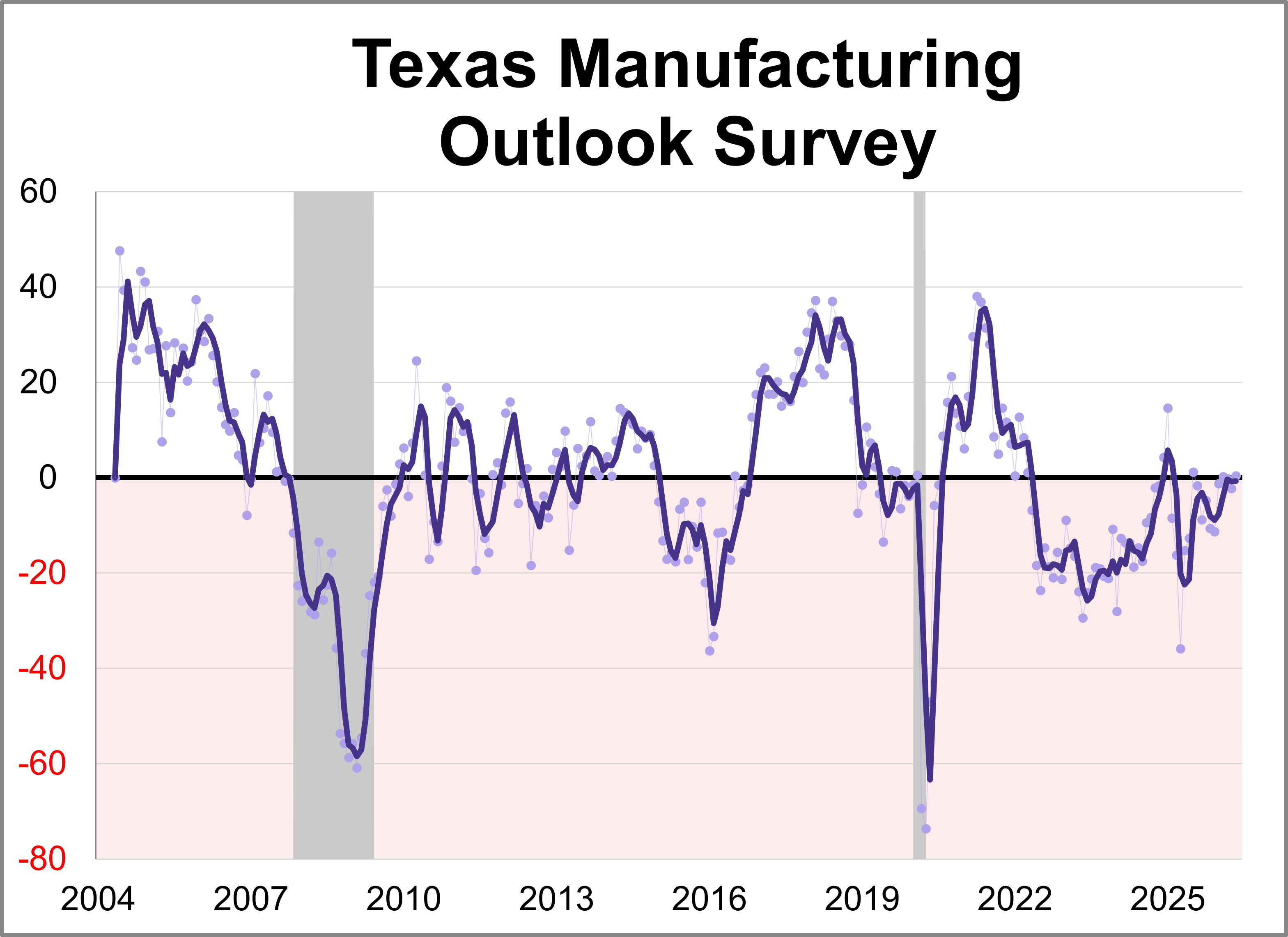

The Dallas Fed released its Texas Manufacturing Outlook Survey (TMOS) for May. The general business activity index rose 2.7 points to 0.4, indicating slower growth of manufacturing activity and stable business conditions perceptions.

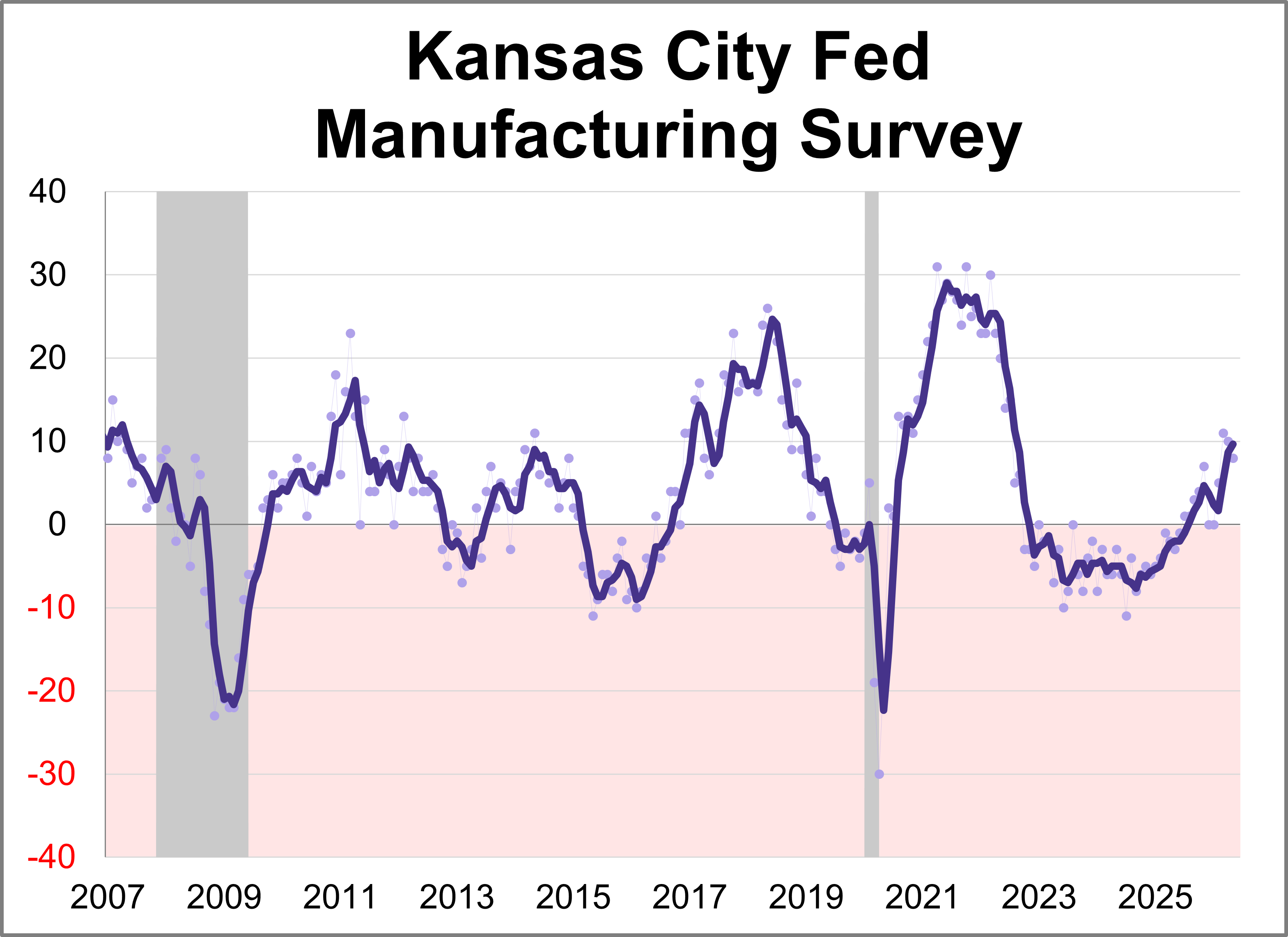

The Kansas City Fed Manufacturing Survey revealed regional activity continued to increase in May. The composite index came in at 8 this month, down slightly from 10 in April but still indicating continued expansion.

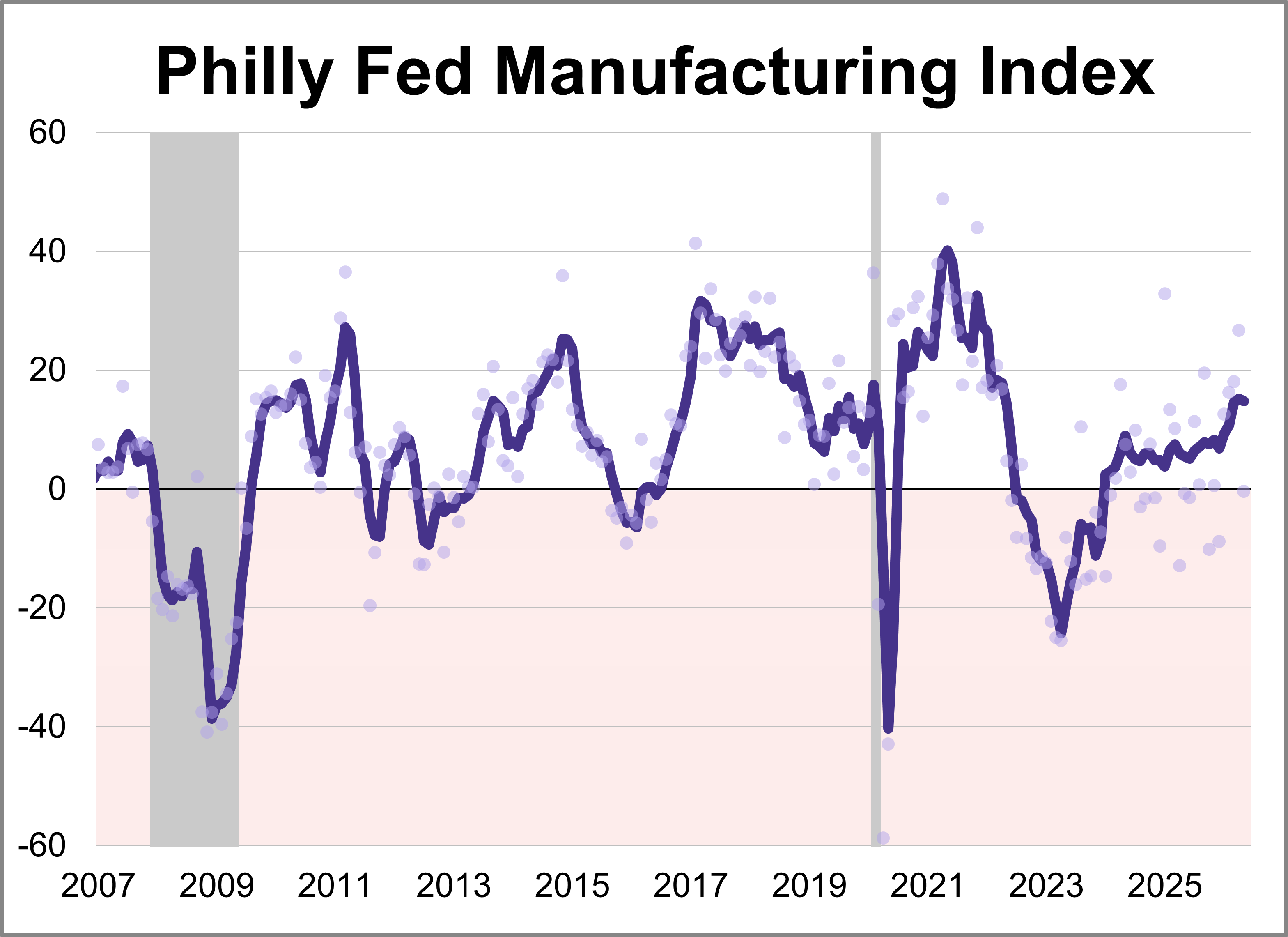

The latest Philadelphia Fed manufacturing index showed activity weakened in May, with the index sinking 27.1 points to -0.4. The latest reading marked the lowest level for the index this year and was worse than the forecast of 17.6.

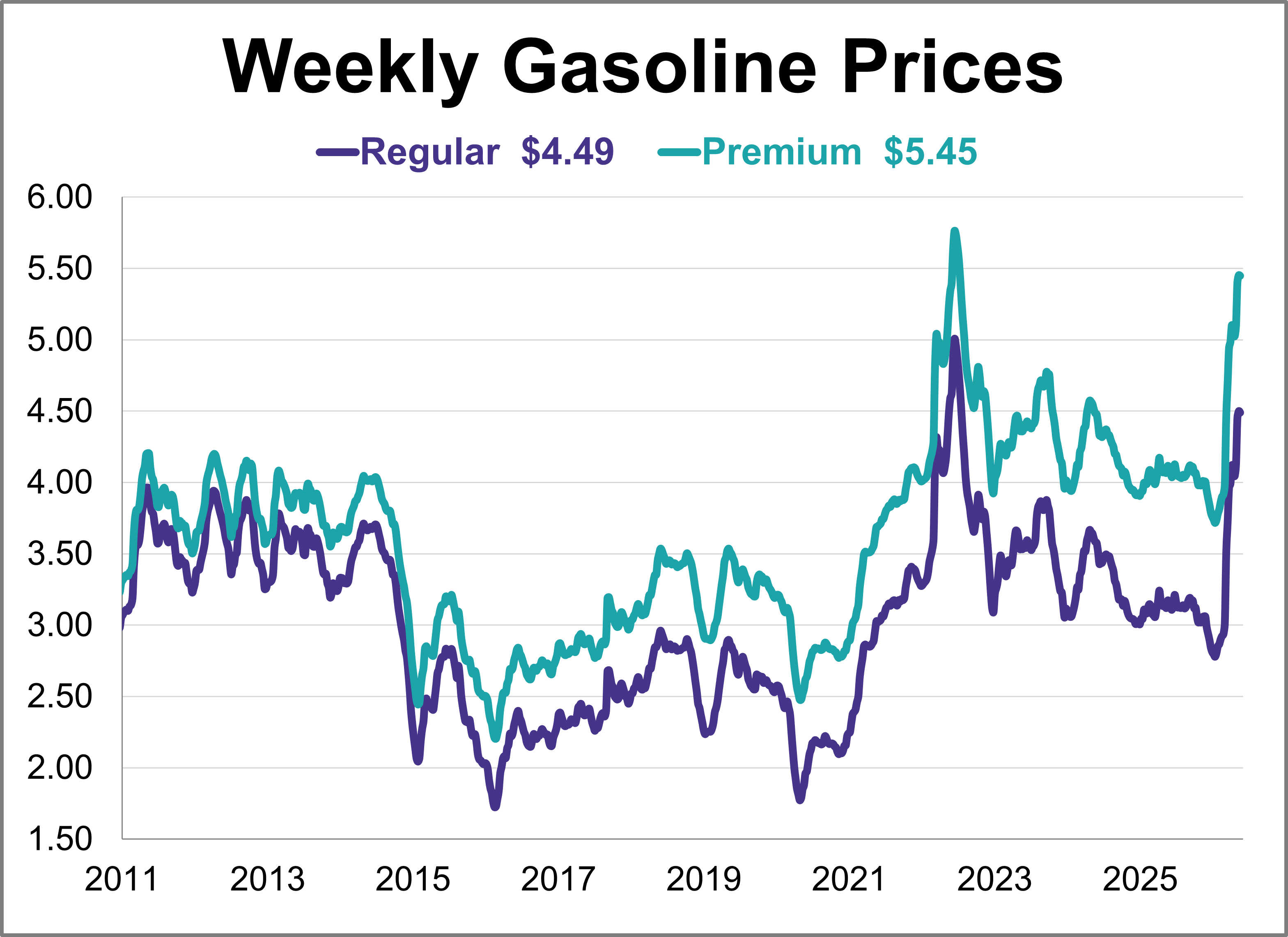

Gas prices were relatively flat this week, remaining at their highest level in nearly four years. As of May 18th, weekly prices were down 1 cent for regular and were unchanged for premium.

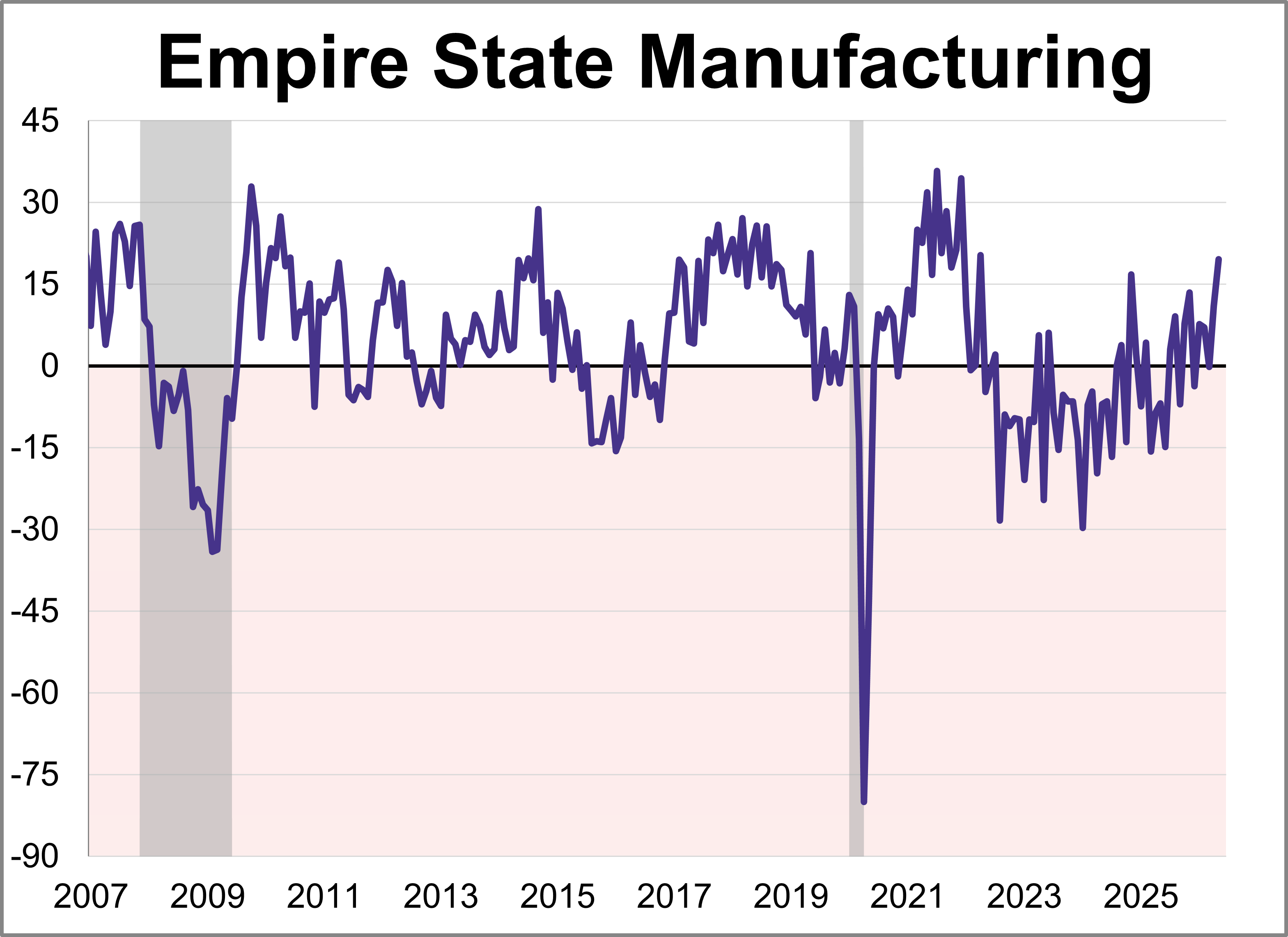

Manufacturing activity grew strongly in New York State, according to the Empire State Manufacturing May survey. The diffusion index for General Business Conditions rose 8.6 points to 19.6, its highest level in over four years.

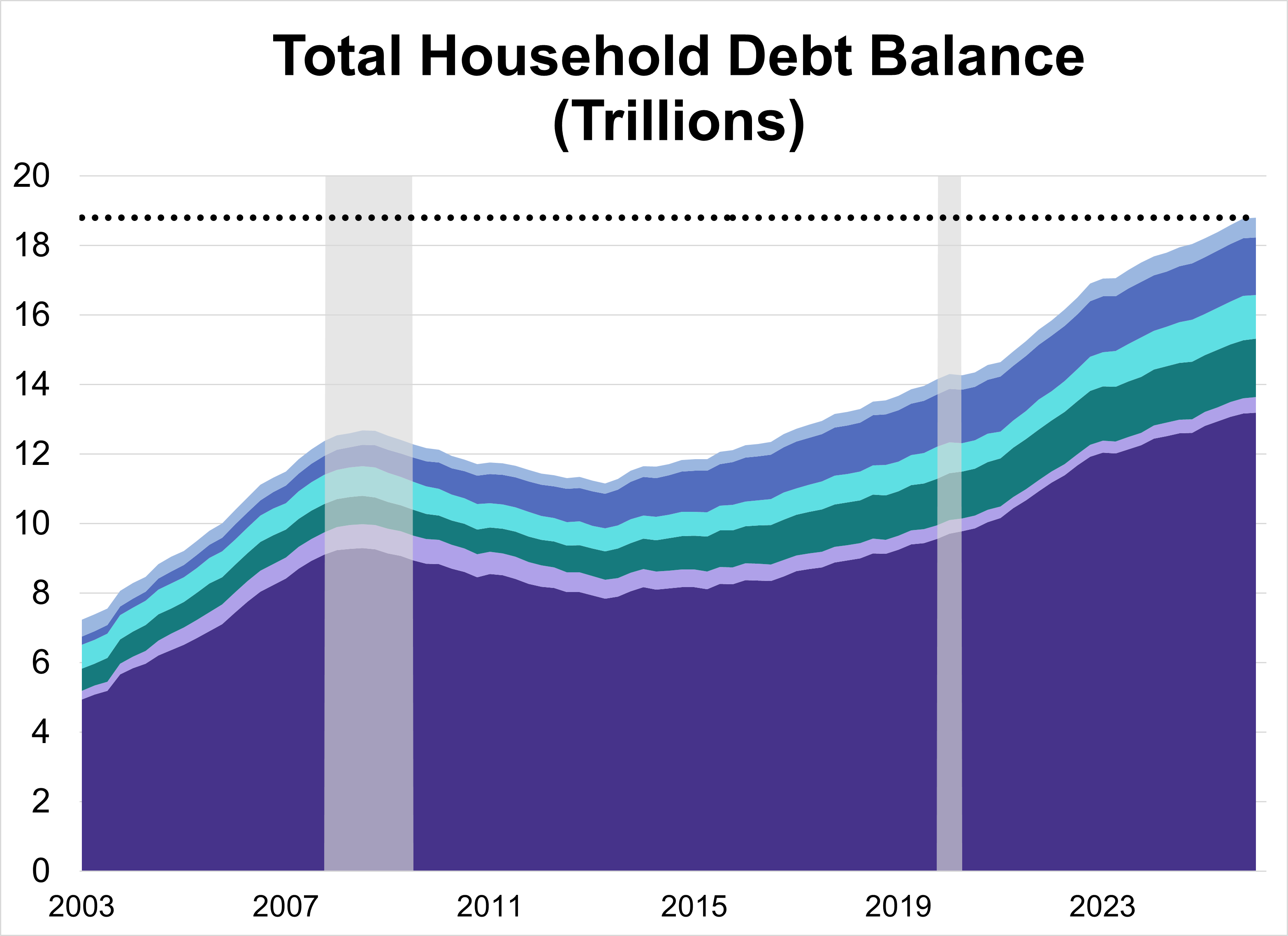

Total U.S. household debt climbed to a record $18.79 trillion in Q1 2026, a modest 0.1% ($18 billion) increase from the previous quarter. The overall rise was driven by increases across a handful of categories, specifically mortgage and auto loan balances.

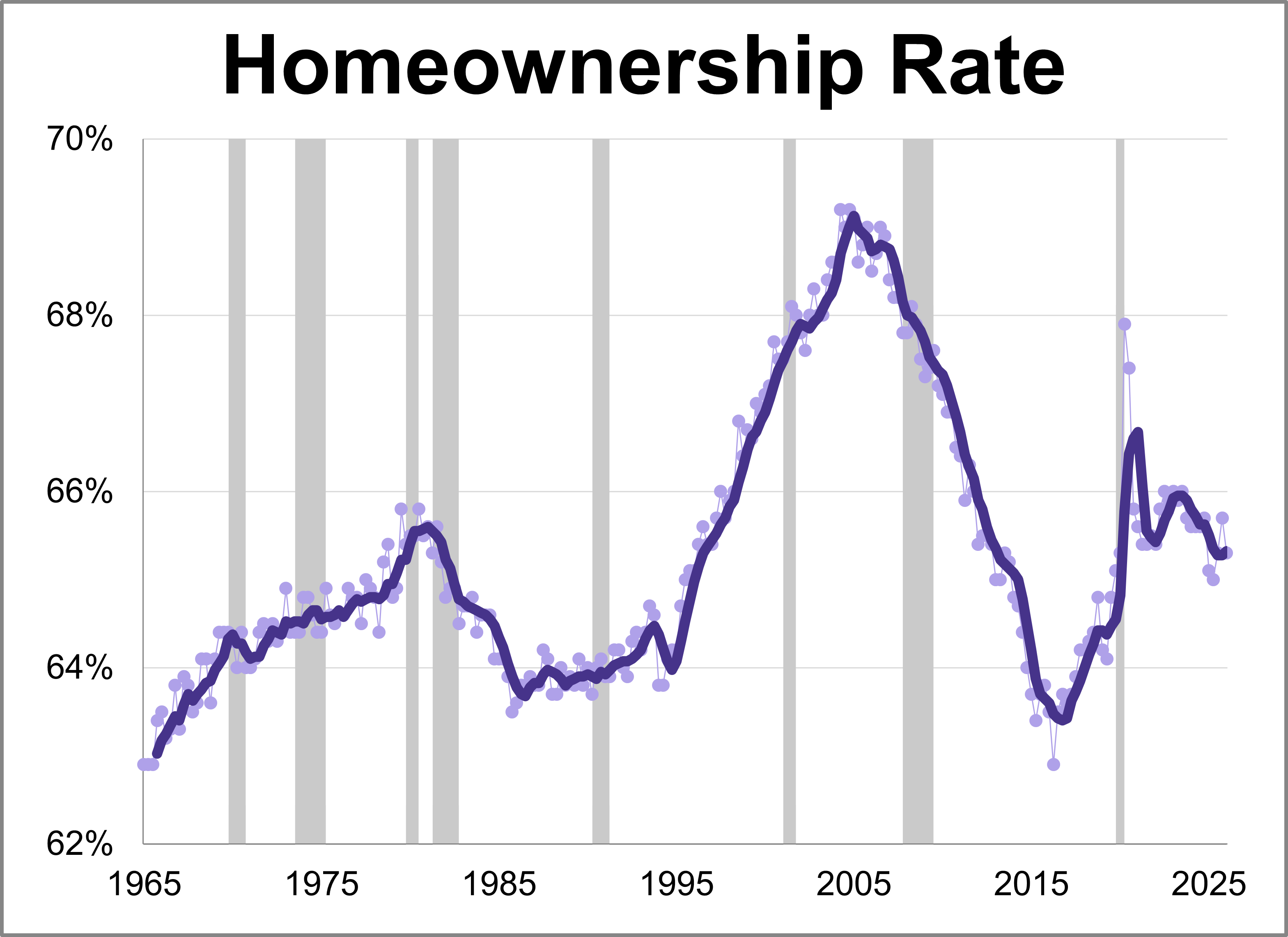

The Census Bureau released its latest quarterly report for Q1 2026 showing the latest homeownership rate is at 65.3%.

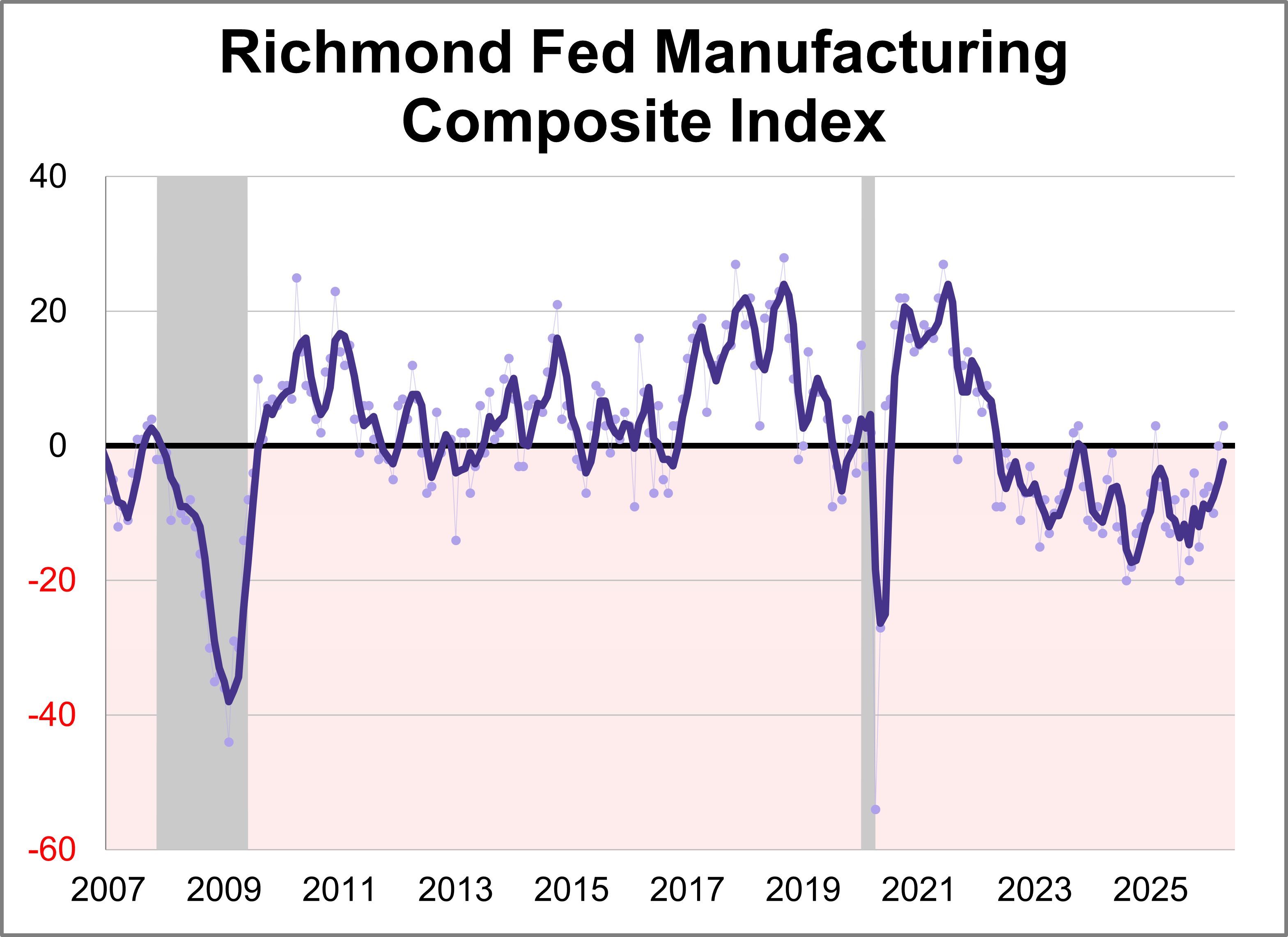

Fifth district manufacturing activity increased in April according to the most recent survey from the Federal Reserve Bank of Richmond. The composite manufacturing index rose three points points to 3, marking the highest level for the index in 20 months. This month's reading was above the forecast of 2.

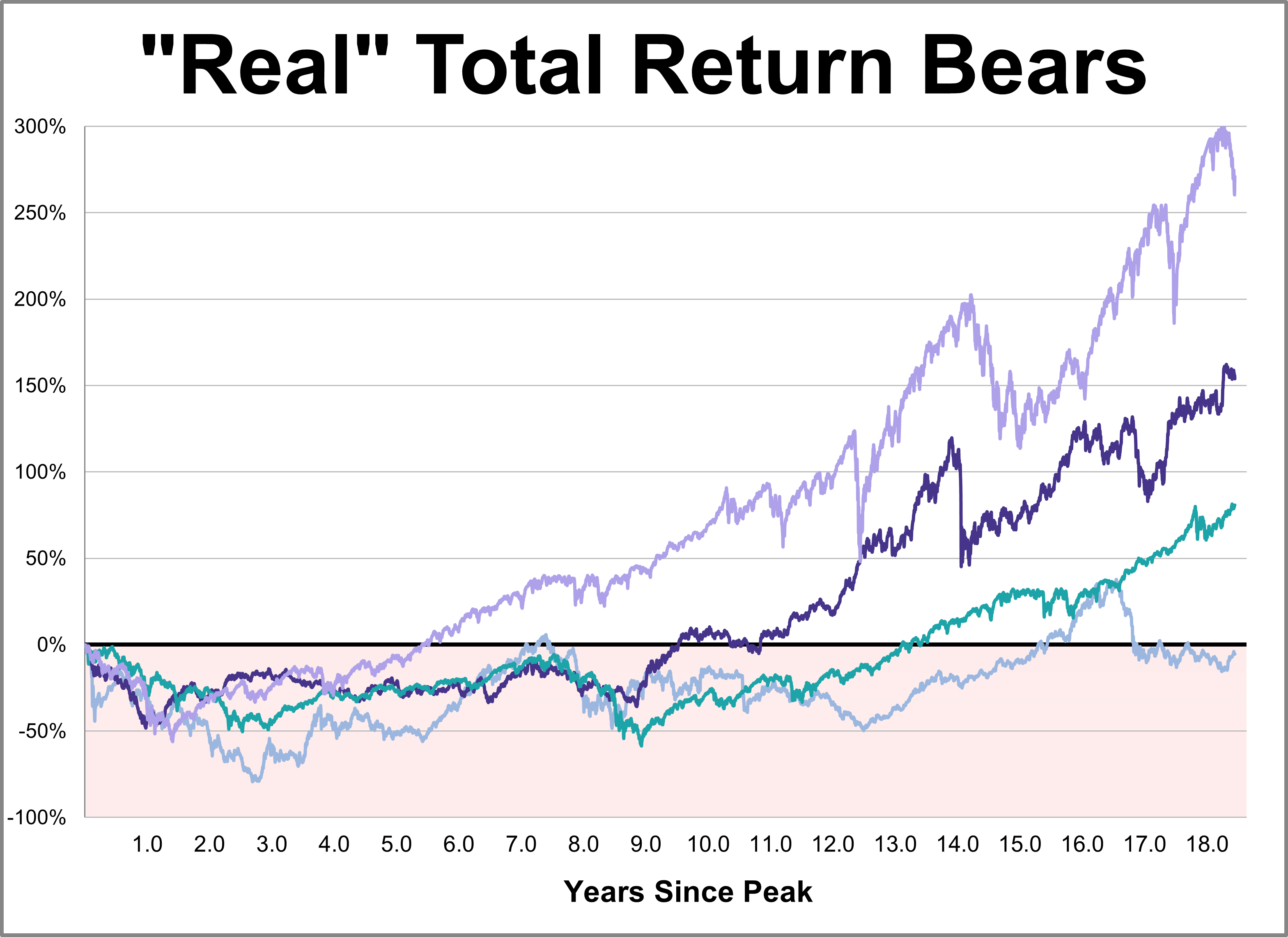

While every market downturn is unique, history offers a crucial lens for understanding recovery. This chart series provides a comprehensive overlay of the Four Bad Bears in U.S. history since the 1929 peak, comparing their recovery paths through the S&P 500's close on March 31, 2026.

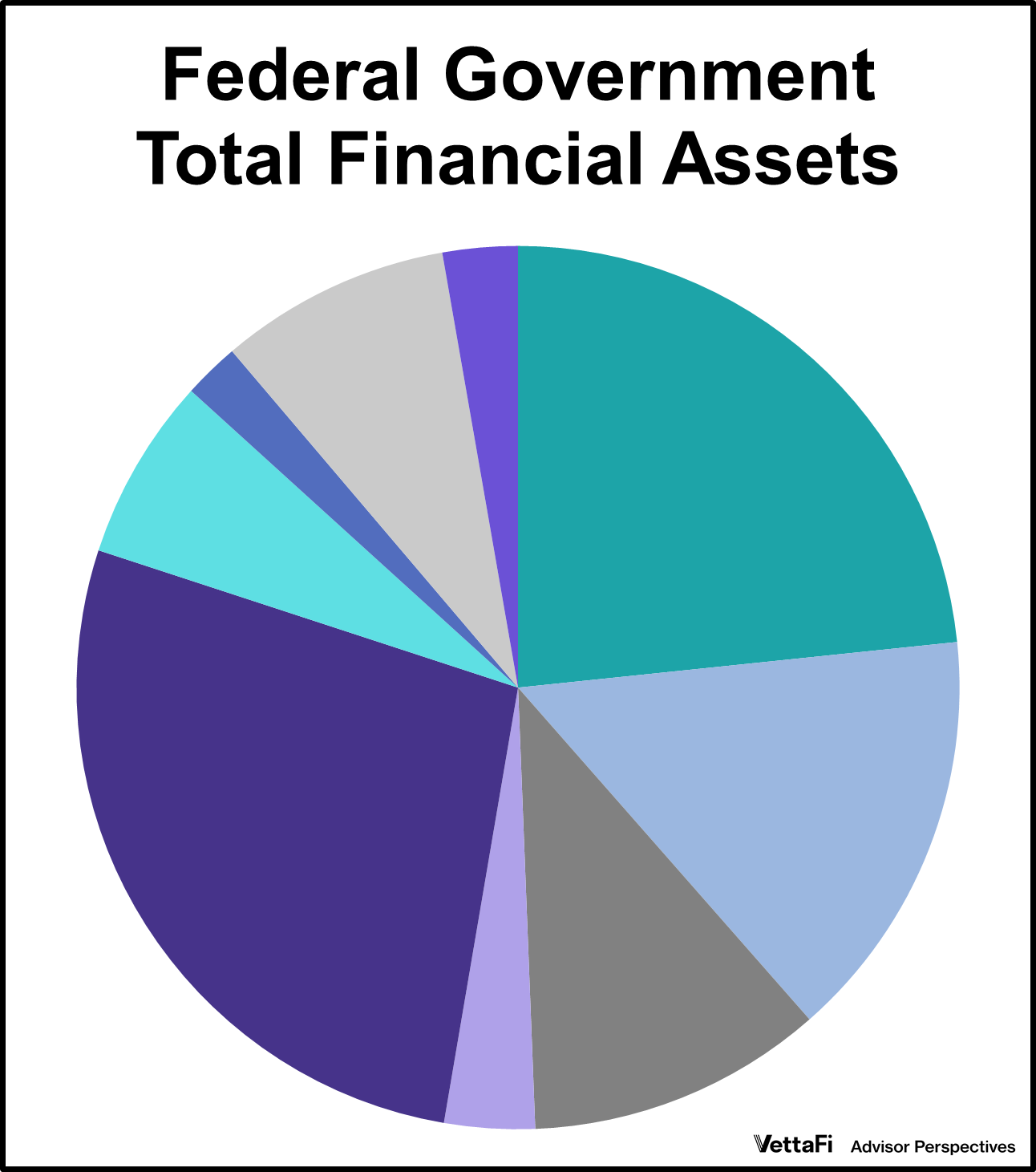

When we think of the U.S. government's finances, we often focus on the massive debt. But what about the assets? What does Uncle Sam actually own, and which asset is the largest?

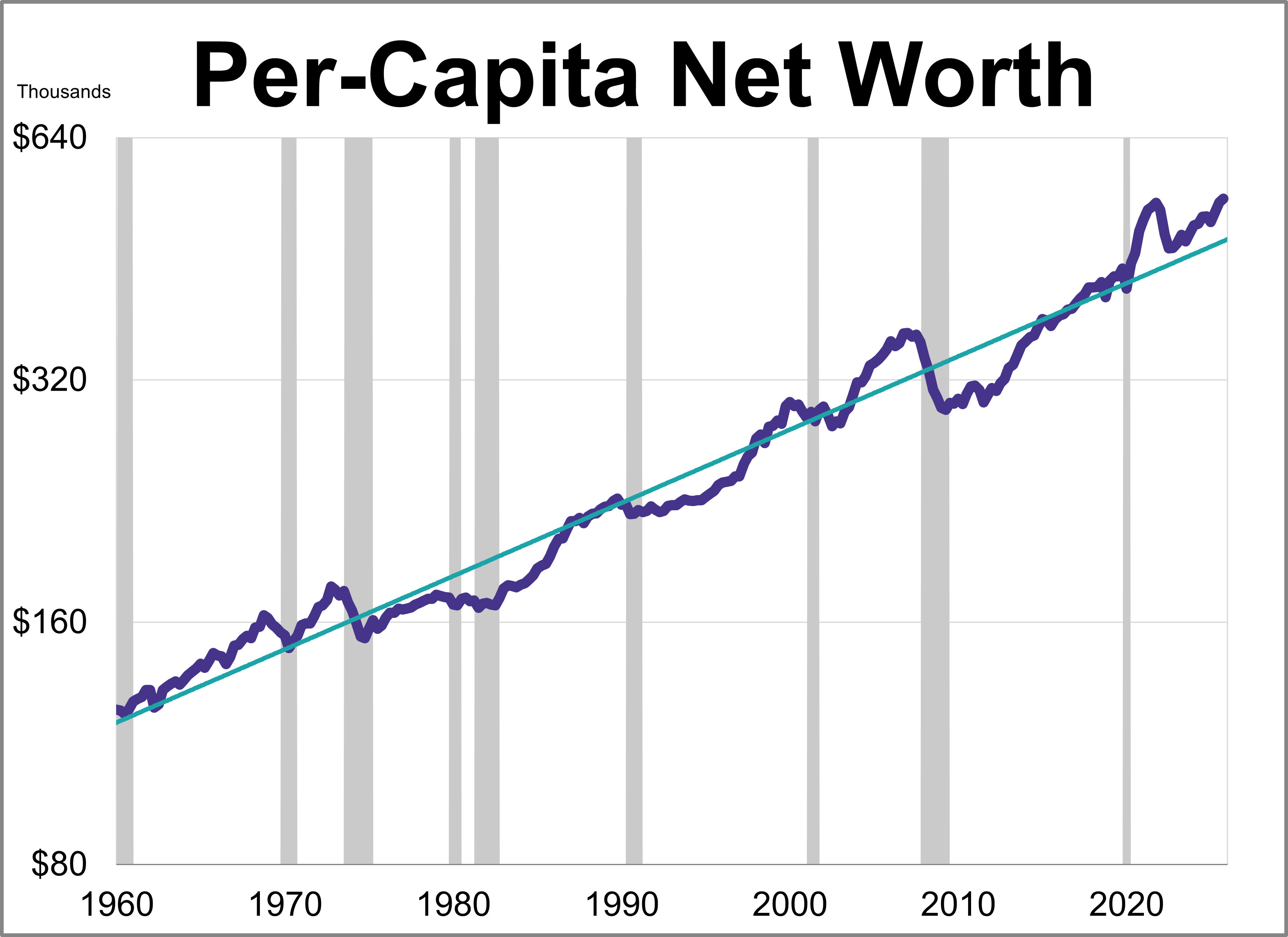

How much wealthier are Americans since the Great Recession? While a look at the headlines shows a staggering 211% increase in household net worth since 2009, adjusting for inflation tells a much different story.

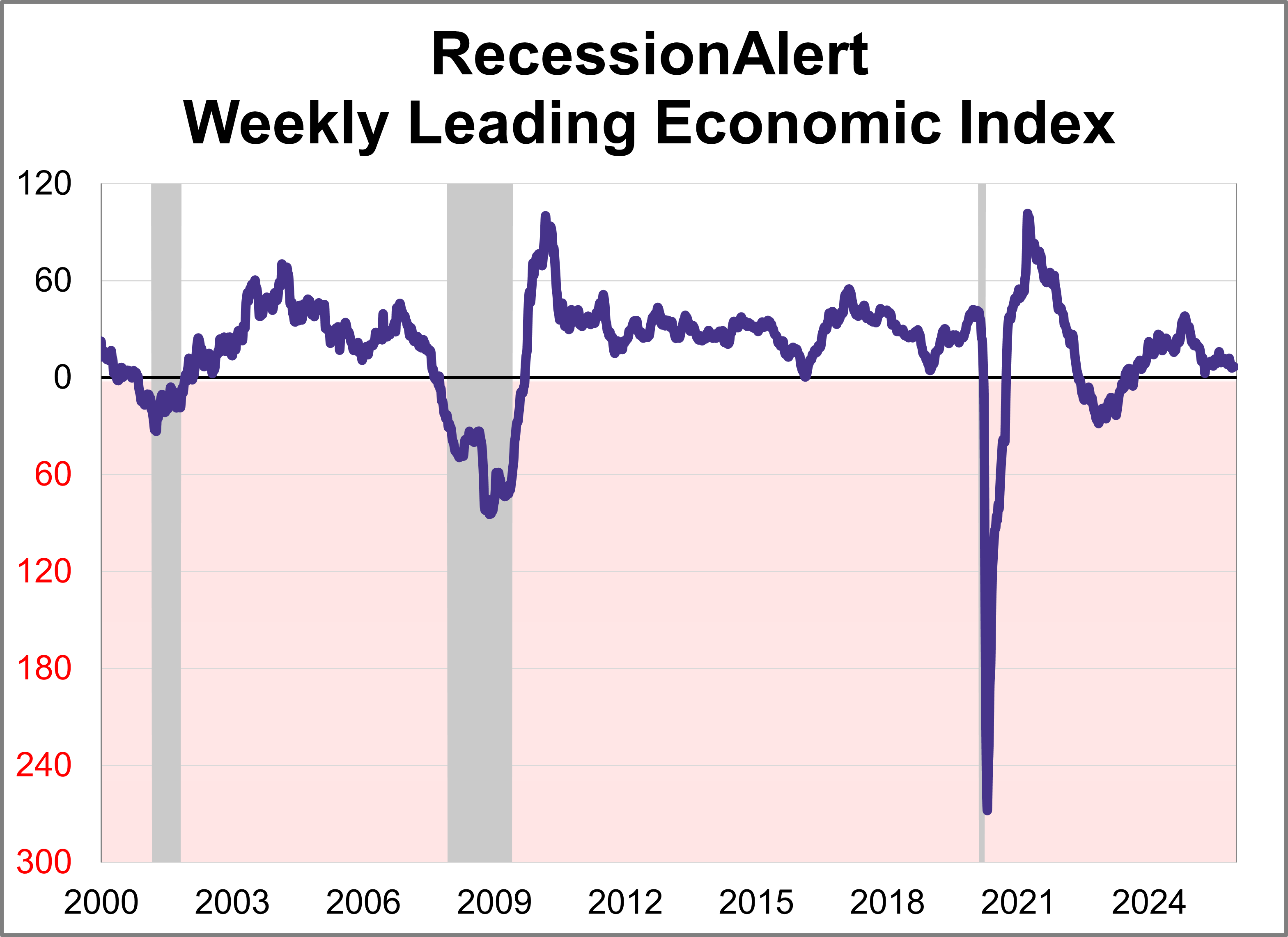

The weekly leading economic index (WLEI) is a composite for the U.S economy that draws from over 20 time-series and groups them into the following six broad categories which are then used to construct an equally weighted average. As of December 12th, the index was at 6.71 with 3 of the 6 components in expansion territory.

Our monthly workforce recovery analysis has been updated to include the latest employment report for November. The unemployment rate inched up to 4.6%, its highest level since 2021. Additionally, the number of new non-farm jobs (a relatively volatile number subject to extensive revisions) came in at 64,000.

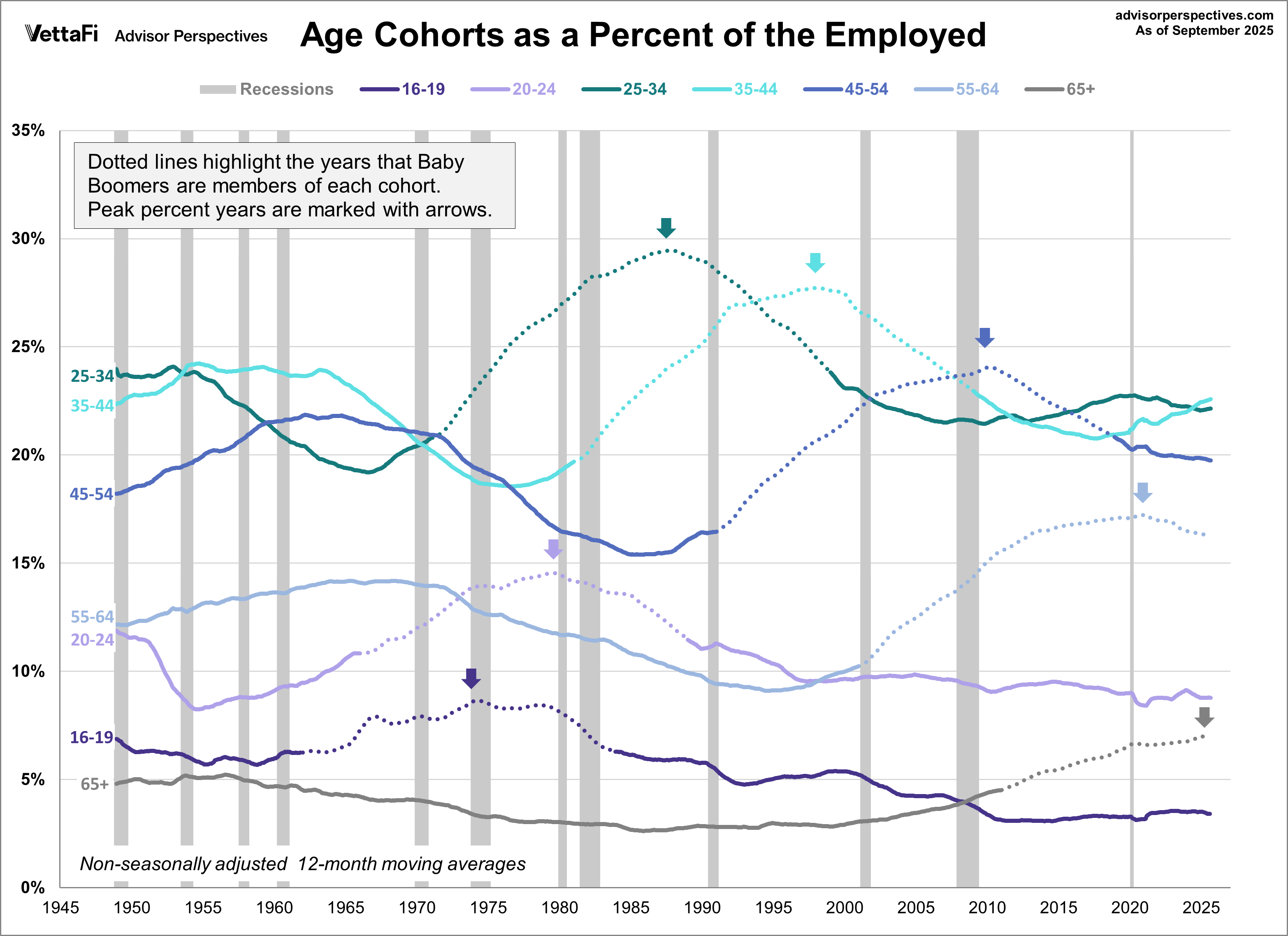

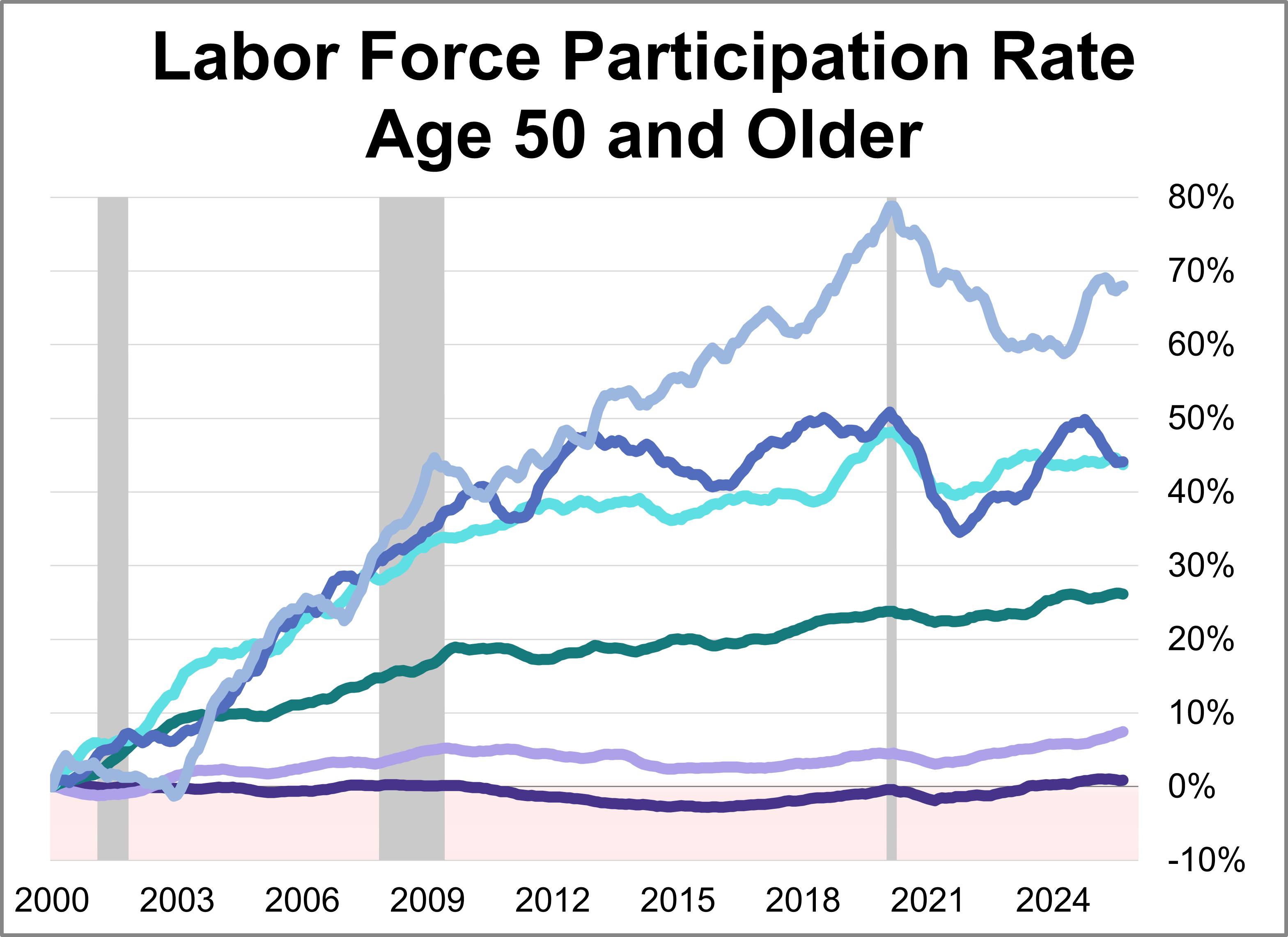

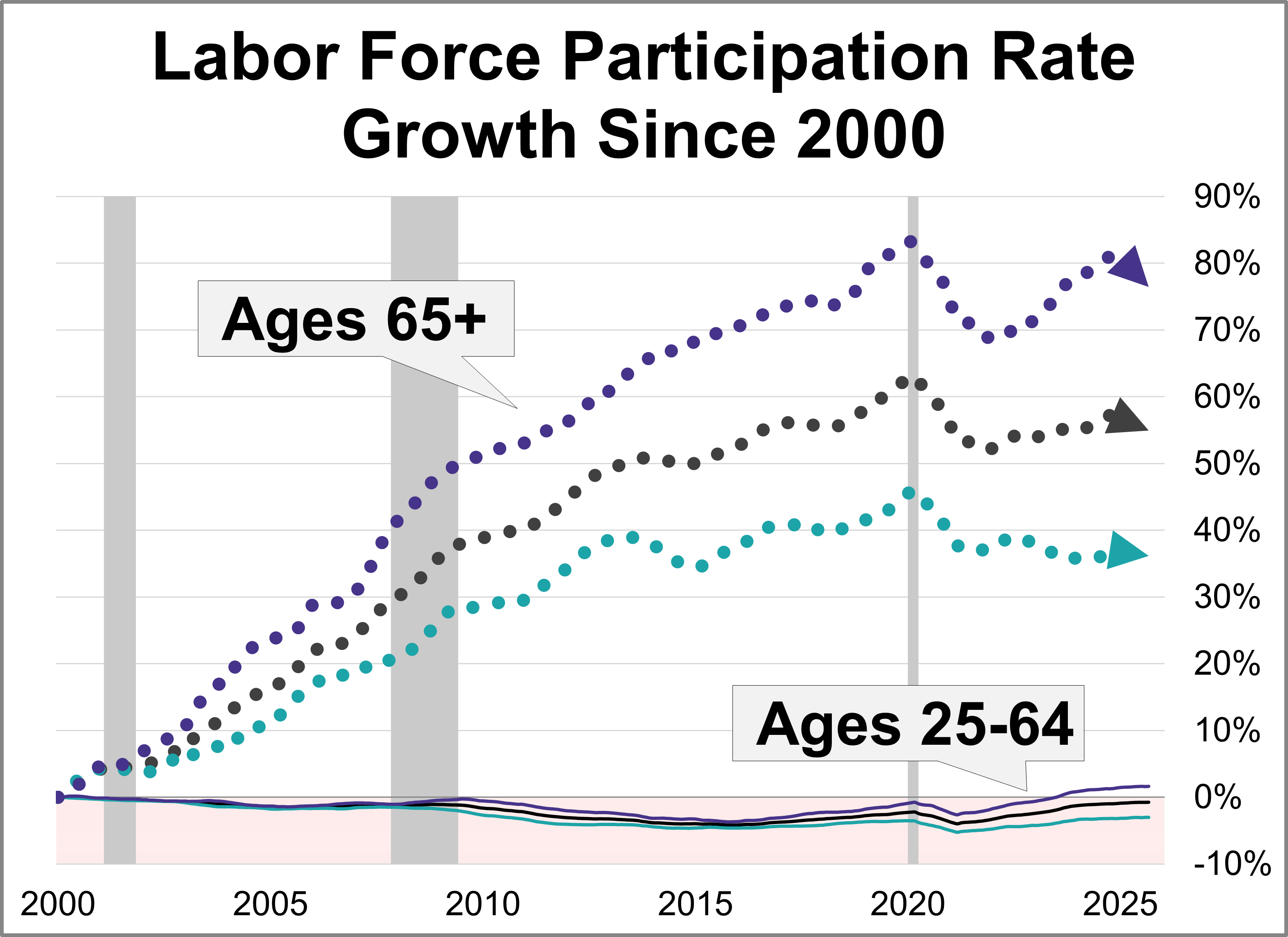

The 20th century Baby Boom was one of the most powerful demographic events in the history of the United States. We've created a series of charts to show seven age cohorts of the employed population from 1948 to the present.

Today, one in three of the 65-69 cohort, one in five of the 70-74 cohort, and one in ten of the 75+ cohort are in the labor force.

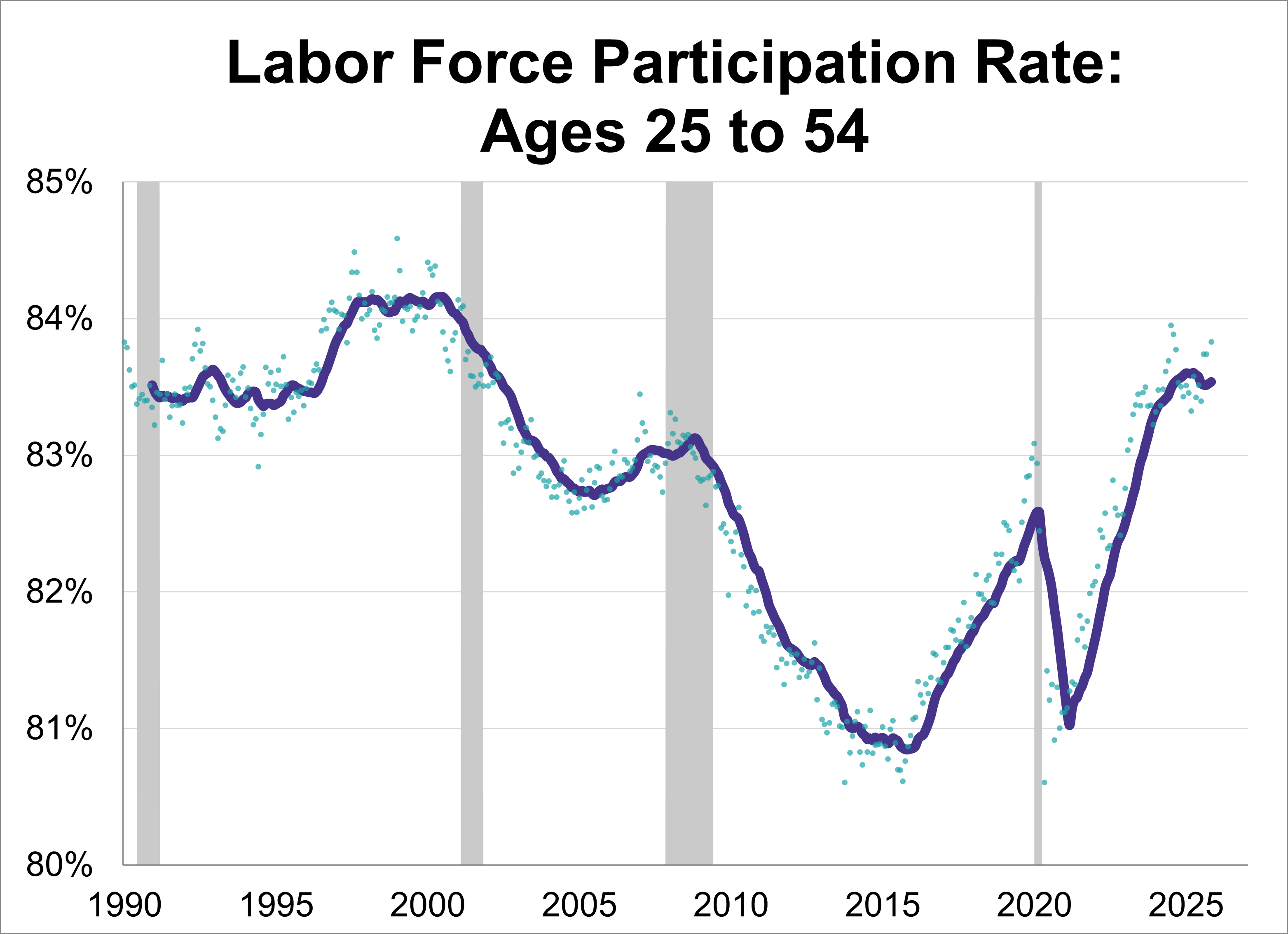

The labor force participation rate (LFPR) is a simple computation: You take the civilian labor force (people aged 16 and over employed or seeking employment) and divide it by the civilian non-institutional population (those 16 and over not in the military and or committed to an institution). As of September, the labor force participation rate is at 62.4%, up from 62.3% the previous month.

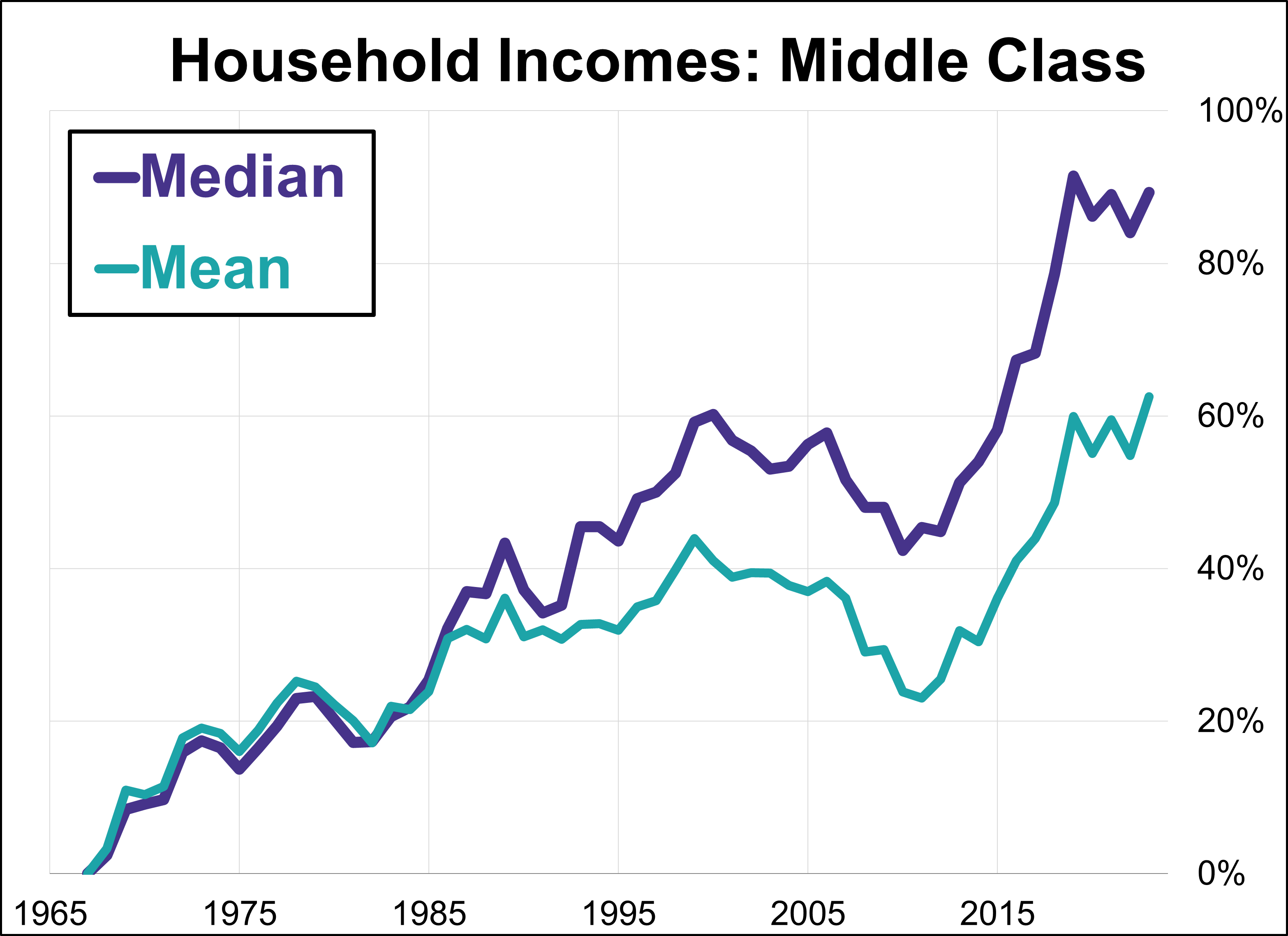

The median household is the statistical center of the Middle Class. Let's take a closer look at the Census Bureau's latest annual household income data with a focus on middle class income. In this update, we'll focus on the growing gap between the median (middle) and mean (average) household incomes across the complete time frame of the Census Bureau's annual reporting from 1867 to 2024.

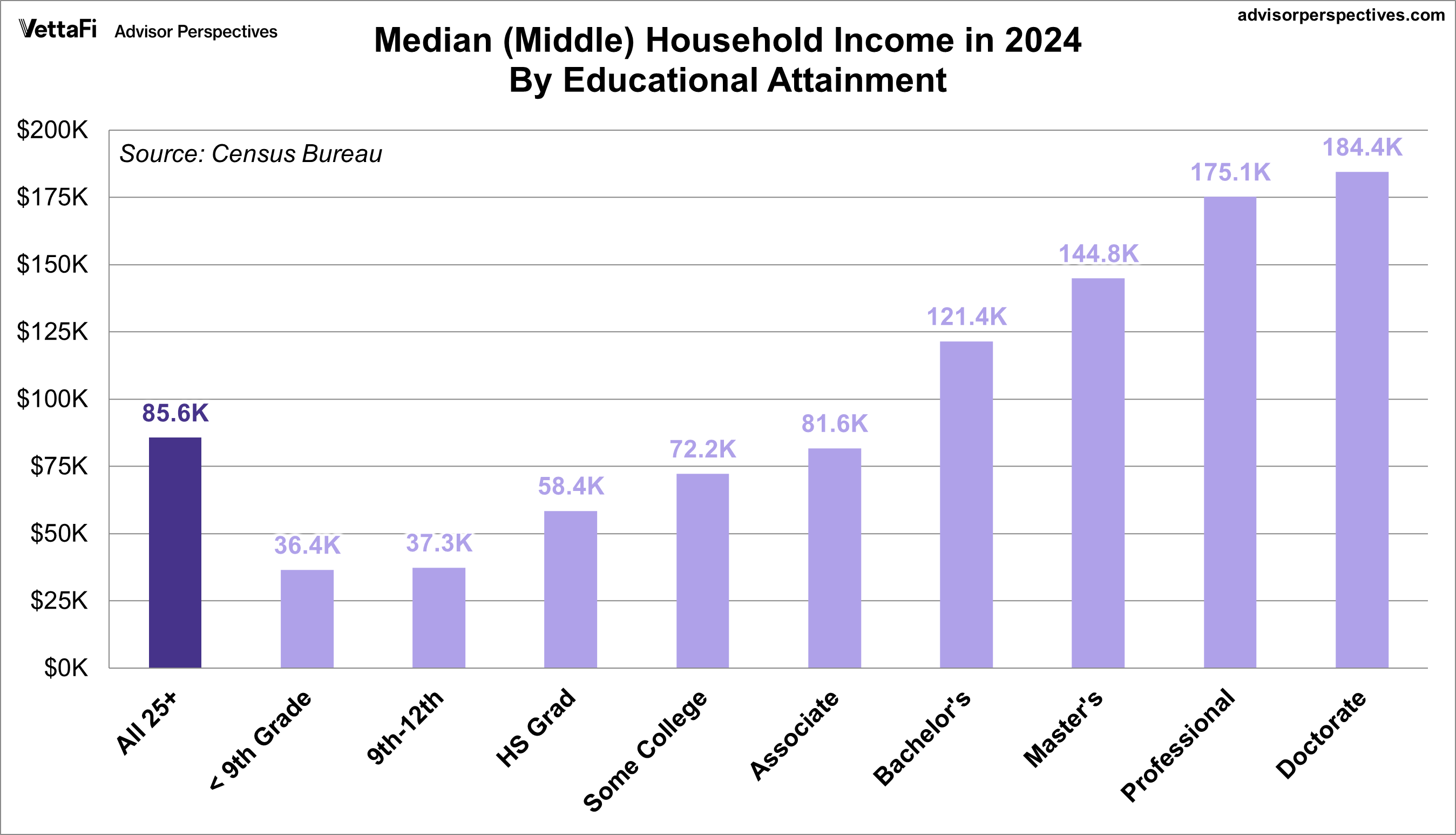

What is the relationship between education and household income? The Census Bureau’s 2024 annual survey data provides valuable insights into this question. The median household income for individuals aged 25 and older was $85,580, but how does this figure vary based on educational attainment?

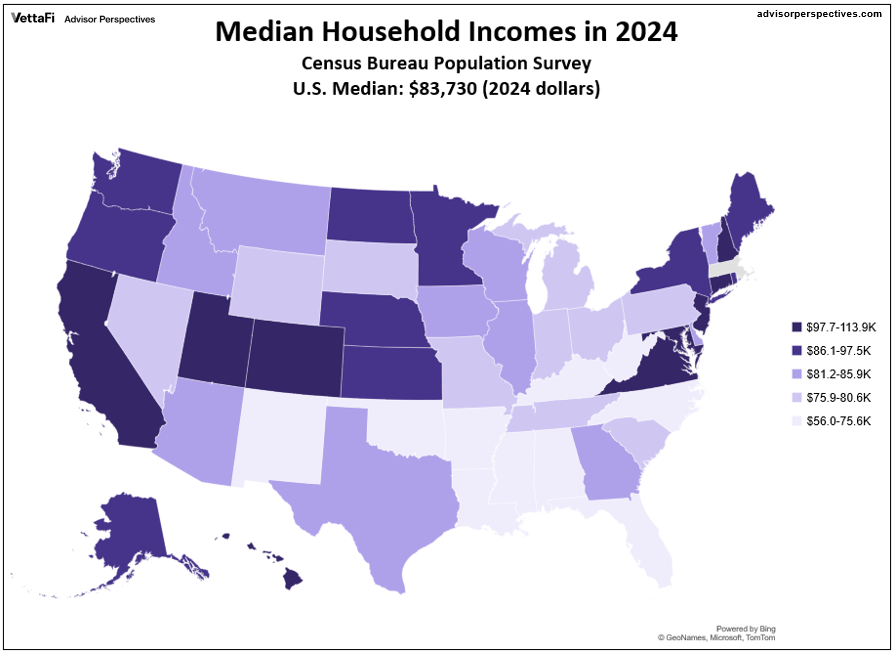

The median US income in 2024 was $83,730, up from $22,420 in 1984 — a 274% rise over the 40-year time frame. However, if we adjust for inflation chained in 2024 dollars, the 1984 median is $60.420 and the increase drops to 39%.

Our commentary on household income distribution offers some fascinating insights into average U.S. household incomes, but misses the implications of age for income. In this update, we examine household income with a focus on age bracket.

The Census Bureau recently released its annual report on household income data for 2024. The mean (average) household income for the middle quintile rose 4.5% to $84,390. Let's take a closer look at the quintile averages, which date back to 1967, along with the statistics for the top 5%.

Earlier this week we posted an update on the median household income for the 50 states and DC which includes annual data from 1984 to 2023. Let's now look at the actual purchasing power of those median incomes. For this adjustment, we're using the "C2ER Cost of Living Index" produced by C2ER, the Council for Community and Economic Research.

The Conference Board Leading Economic Index (LEI) increased slightly in November. The index rose 0.3% from the previous month to 99.7 after eight consecutive monthly declines.

Credit is an often-overlooked asset class. But the current outlook shows lots of opportunities in credit for advisors. Given today’s volatility, active management could also help investors find the right opportunities at the right time.

Join the experts at Simplify Asset Management and Asterozoa Capital Management to unpack how investors can benefit from an actively approached credit strategy.

Gold is seeing record prices, and while exposure to gold can be useful to a portfolio, it could behoove some investors to look at gold miners instead. Gold miners are well positioned to capitalize on the recent surge in interest in gold.

Join the experts at REX Shares for a free educational webcast and learn all about gold and gold miners.

In the coming Q4 Preview Symposium, investors will learn how they can best prepare for a host of possibilities and set up their portfolios to take advantage of opportunities and understand which areas of the market will face higher-than-normal risk.

Market expectations and FOMC projections for rate cuts have diverged at different times. Investors remain uncertain about the timing and pace of Fed moves. Spreads are tightening, and setting your fixed income portfolio up for success presents unique challenges and opportunities.

Are your clients receiving proceeds from property or business sales? They rely on your expertise to navigate tax-advantaged solutions. This free webcast will equip you with the expertise to guide clients through complex real estate transactions and provide them with the best financial strategies.

Earning returns for clients matters, and so is reducing taxes they pay. Clients looking to retain wealth from their portfolios, expect their advisors to be proactive when it comes to managing taxes.

Join the professionals at AssetMark to hear about tax management services that can help your clients keep more on their returns.

Join the experts at Eaton Vance for a webcast discussing best ideas for fixed income positioning going forward.

Despite a strong first half, volatility and tail risk remain top of mind for investors. A managed floor strategy could help give you core equity exposure while mitigating risk.

Join the experts at Innovator ETFs to learn all about their timely managed floor strategy and unpack how it can help your clients keep market upside exposure without the additional risk.

Oil prices have been resilient in 2024, and US natural gas prices have staged an impressive rebound. Oil demand remains in focus for energy markets, even as natural gas sees new long-term structural demand drivers.

Join the experts from GraniteShares for an educational webcast and learn all about how investors can find unique income strategies in today’s environment.

Join the experts at Amplify ETFs and learn how GLP-1's could revolutionize the weight loss drug market as well as a strategy that can give your portfolio exposure to a theme that could see significant growth in the coming years.

Buoyed by the Magnificent Seven, the first half of the year saw strong results for investors. But there are headwinds on the horizon — Fed policy changes, geopolitical tensions, and other factors that could impact market results.

Join the experts at State Street Global Advisors, Astoria Portfolio Advisors, and Clark Capital Management Group as they explore three takeaways from State Street Global Advisor's Midyear ETF Market Outlook: diversifying away from the Magnificent Seven, optimizing income through short-term core and credit, and positioning for macro volatility through real assets.

Join us for an insightful webinar where we delve into the transformative impact of Artificial Intelligence (AI) on society and explore innovative investment strategies that leverage this groundbreaking technology.

The Northern Trust Economics team shares its outlook for growth, inflation and interest rates in major markets.