Global Economic Outlook: Staying Focused

EASIER MONETARY POLICY IS ON ITS WAY AROUND THE WORLD.

Every summer, we hope for a reprieve from consequential events, allowing us to relax and recharge for the balance of the year. More often than not, we are disappointed.

Elections across a range of economies have yielded a lot of news, though few outcomes of consequence to our outlook. We will monitor the evolving policy possibilities as coalitions form in Europe and as the U.S. election enters its most active phase.

For now, the priorities of major economies remain well aligned: sustain growth, contain inflation, and plot a course to easier monetary policy. Trends to date are well-aligned with a soft landing in most of the world, with China presenting the greatest uncertainty.

Following are our thoughts on how major markets are faring.

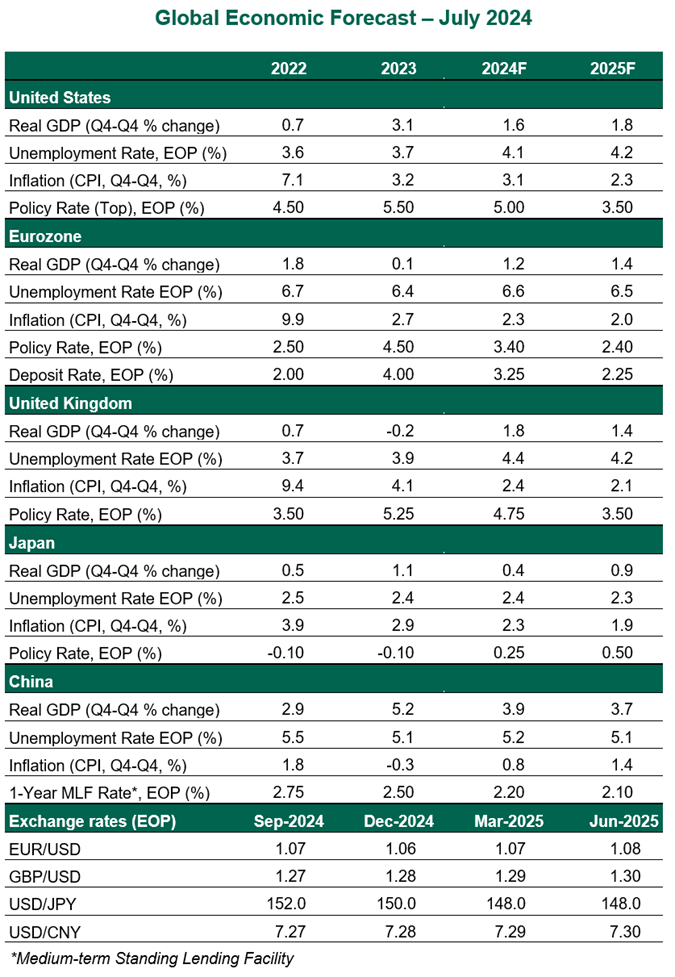

United States

- After some reheating in the first quarter, the cooling trend surrounding inflation has resumed. The consumer price index (CPI) was unchanged month-over-month from April to May, and then deflated slightly from May to June. Meanwhile, employment markets have slowed, with job gains averaging 222,000 per month in the first half, in line with updated expectations of break-even job creation. The unemployment rate has drifted upward to 4.1%—not yet a worrying level, but an unfavorable trend.

- The Federal Reserve has erred on the side of holding rates higher for longer, but we believe the evidence will be sufficient to justify a cut in September. The rate of inflation has fallen by nearly half since the last hike in July 2023, pushing the implied real rate of interest higher; slight reductions will still keep overnight rates in restrictive territory.

Eurozone

- The eurozone’s inflation retreat laid the foundation for the European Central Bank (ECB)’s first cut in June. Activity has since been mixed. First quarter gross domestic product (GDP) for most members was narrowly positive, characterized by sluggish consumption and lagging industrial production. Headline inflation moderated by one-tenth to 2.5% year over year in June, held higher by services prices. The ECB has been noncommittal in its forward guidance, but we believe the data have cleared the way for cuts to resume in September.

- European Parliamentary elections did not alter the balance of coalition power. Reelected European Commission President Ursula von der Leyen faces a tough mix of priorities, including more demands for security and the green transition, with limited funding.

United Kingdom

- The call for a summer election came as a surprise, but the outcome did not, with a sweeping victory for the Labour party. However, the party platform is fiscally neutral with only modest reform intentions. Updates to land use regulations will support growth; a solid upward revision to first quarter GDP and sustained momentum in recent months have also prompted a rise in our full-year growth forecast.

- The new leaders are stepping into a difficult economic context. Inflation remains high; the headline reading of 2% in June was the product of a divergent combination of deflating goods and high services inflation. The unemployment rate has risen by half a percentage point in the year to date, but wages are still hot, gaining 5.6% year over year. Members of the Bank of England’s Monetary Policy Committee have expressed a range of opinions, with some indicating they would be less tethered to backward-looking measures of inflation. On balance, we expect inflation is still firm enough to put off a cut until September.

Japan

- First quarter real gross domestic product growth contracted at a 2.9% annualized rate, led by a large decline in public fixed investment. While this result is disappointing, the weakness is unlikely to persist. Strong wage gains will help the economy bounce back in the coming months. Gains in exports will be gradual, as softer external demand will partially offset the boom in microchip exports and favorable currency effects. We have lowered our 2024 growth estimate, mainly to reflect the weak start to this year.

- The Bank of Japan (BoJ) maintained its policy rate at the June meeting, but announced its decision to start reducing its holdings of Japanese government bonds by a substantial scale in August. While another hike at this month’s meeting cannot be ruled out completely, we expect the BoJ to wait until September to confirm the impact of the strong wage settlement on consumption and prices. The end of negative rate era is welcome, but policy is still loose.

China

- The Chinese economy’s recent outperformance proved to be transient. Real GDP growth slowed six-tenths to 4.7% year over year in the second quarter. Manufacturing and exports lifted growth, but weak domestic demand remains an obstacle. The outlook for China remains cloudy. Stagnating household spending, low consumer confidence, and the ongoing property slump will prevent a clear turnaround anytime soon. Foreign capital outflows are depressing the yuan, but not enough to offset the downside risks from rising trade barriers and tariffs.

- Amid weakening economic momentum and persistent deflationary pressures, the People’s Bank of China cut its major short-term and long-term policy rates by 10-20 basis points in July. This small increment is unlikely to have much of an effect in a deleveraging economy. The decision to lower rates came just days after the release of the communiqué for the Third Plenum, which failed to shift economic reform into higher gear.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.