A remarkable feature of extended bull markets is that investors come to believe – even in the face of extreme valuations – that the world has changed in ways that make steep market losses and extended periods of poor returns impossible.

“Past Performance Is no guarantee of future of results.” Such is the disclaimer below every performance chart produce by the financial marketplace.

In 1905, the first gas pump appeared in St. Louis, Missouri, to meet the fueling demands of a rapidly growing number of motorists.

In our baseline forecast, the recent decline in U.S. Treasury yields will reverse somewhat, as some of the near-term factors pressuring yields lower ebb.

A few years ago, Paul Wallace penned an article entitled: “GDP Is A Grossly Defective Product.” The recent release of the Q2-2020 report reminded me of it as the media fawned over the 7.6% print.

Optimism around GDP growth, employment and earnings has, for now, outweighed worries related to COVID-19 variants.

With global growth rebounding amid uncertainties over inflation and COVID-19 variants, investors may want to consider a somewhat more cautious and flexible approach when seeking a consistent yield.

The stock market and economy are hanging by a thread over an economic abyss. That thread is zero interest rate policy (ZIRP).

In this past weekend’s newsletter, I discussed the issue of the markets next “Minsky Moment.”

Last week witnessed a bold adventure in in-person conferencing… and lessons in how to manage clients (and their portfolios) in an unprecedented market environment. But the memorable moment at the ENGAGE conference was David Kelly’s statement that bitcoin is a cult and not a currency.

Inflation has been on the rise recently, raising concerns about long-run inflation and its impact on the spending power of those who can least afford it—investors approaching or already in retirement.

Frank Pape is the senior director, portfolio consulting for Russell Investments’ advisor and intermediary solutions business. In this interview, he discusses the latest research on how advisors can maximize the after-tax income for their clients.

You may not be familiar with the term metaverse, but if you’ve been a consumer of popular books, movies and video games over the past 30 years or so, you probably are aware of the concept.

I am worried the Fed will either let inflation become psychologically entrenched, or wait too long to stop it and spark crisis with a too-hasty response, but there are other possibilities. None are especially good.

The yield curve is a powerful indicator. More powerful than many others as May West reminds us. As the greatest reopening momentum now appears behind us, today, our All-Weather portfolio looks more all-weather than it did earlier in the year.

Howard Marks doesn’t make bets on economic predictions. That’s especially true now when the biggest wildcard is inflation – a phenomenon no one fully understands. But just because something is unknowable doesn’t mean it’s unimportant. That’s why Howard has devoted his latest memo to a topic he largely disavows: macro forecasting.

As expected, in a unanimous vote, the Federal Open Market Committee (FOMC) of the Federal Reserve (Fed) kept the fed funds rate unchanged in its range of 0-0.25%.

Equities continued to rally in the second quarter, but the market remains undecided about whether the recent uptick in inflation is more likely to be transitory or persistent.

Despite a strengthening economy in the second quarter, investors were highly focused on the Federal Reserve’s response to the recent spike in inflation data.

Everyone was eager to put 2020 behind us, yet the Covid hangover lingers.

For the 10 years prior to the great financial crisis of 2008 (GFC), the 10-year Treasury bond’s average yield was 5.0%; for the 10 calendar years ended December 2020, it averaged just 2.3%, less than half its pre-crisis average (Source: Bloomberg).

In pursuit of higher yields, many investors are taking on more risk, either by going further out on the yield curve or further down the credit spectrum. In 2021, however, even the longer-dated and lower-quality segments of the bond market have failed to offer yields comparable to those of their shorter-dated, higher-quality counterparts prior to the GFC.

This dynamic has led investors to seek bond alternatives. One such alternative is a defined outcome investment with built-in buffers against losses.

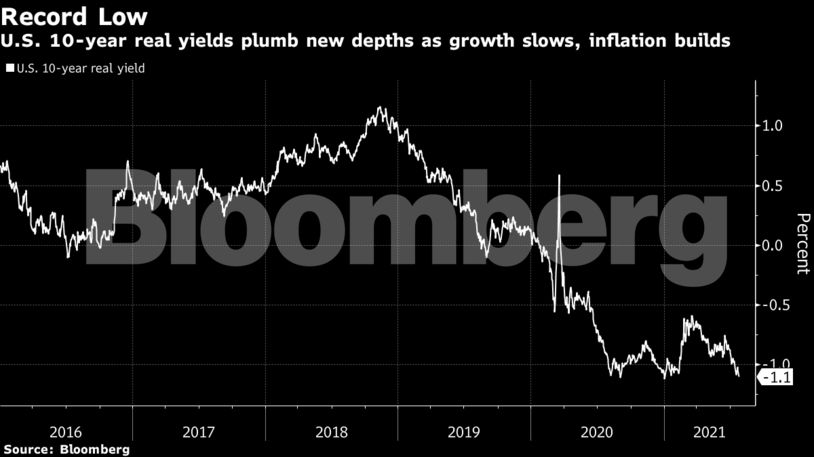

The real yield on 10-year Treasuries fell to a record low as concerns mounted over the outlook for economic growth even as investor flows fueled appetite for inflation-linked debt.

Our economic outlook remains constructive, though we recognize it’s still too soon to know whether the current bout of inflation is transitory. Given the potential for rate increases, particularly after the Fed’s comments in June, we continue to prefer non-investment grade bonds, as they have lower duration and higher yields.

A revival of the Obama-era Build America Bonds would raise funds with less taxes.

It’s now official that the recession of 2020 was the shortest in history.

Tweedy Browne is one of the most respected value managers in the world, with a legacy that includes having Benjamin Graham and Warren Buffett as clients. In this interview, members of its investment committee explain why value investing is on the cusp of a resurgence.

Recent protests offer hope that change may be right around the corner. But for now, gold and Bitcoin have helped fill the gap created by disastrously mismanaged currencies.

The impacts of passive investing are not as well understood as they should be.

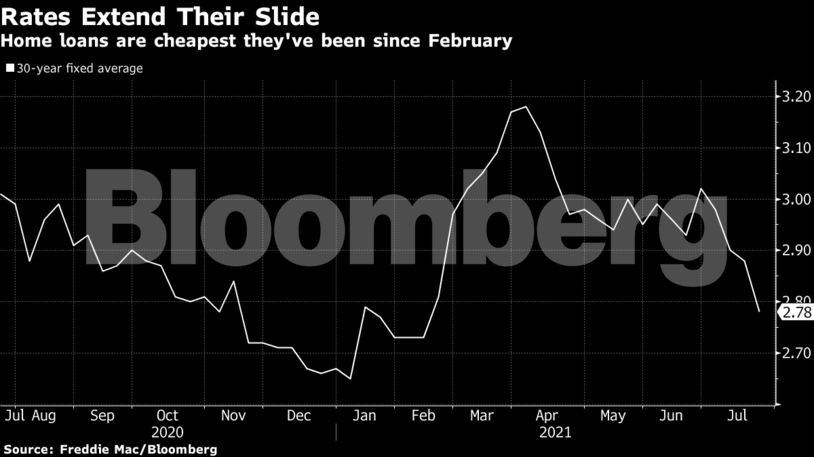

Mortgage rates in the U.S. plunged to the lowest level in more than five months.

Two months. That’s how long the pandemic-triggered recession lasted, from February to April 2020, making it the shortest economic downturn in U.S. history, according to the National Bureau of Economic Research’s (NBER) Business Cycle Dating Committee.

The imminent return of the U.S. debt ceiling is causing angst for money-market traders once again.

Municipal-bond investors still have concerns about the future of higher education even as schools in the U.S. look to a more normal-looking academic year thanks to Covid-19 vaccinations.

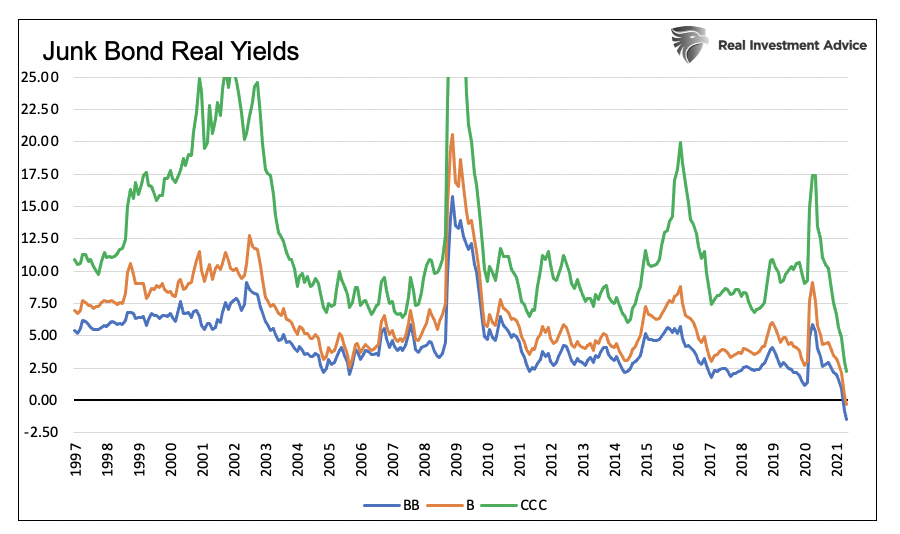

The US high-yield market has seen a strong comeback since its panic-driven downturn at the onset of the COVID-19 pandemic.

The worst is behind us, and over the next two years the global economy will continue to experience a strong economic recovery.

Monetary policy is not expansionary despite widespread belief otherwise.

Long-term Treasury rates tumbled to the lowest levels in months on Monday as the spread of the delta coronavirus variant called into question optimistic assumptions about economic recovery, also touching off a global stock market slump.

The title of this comment may seem odd, given that – as I write this on July 14, 2021 – the S&P 500 is at a record high.

During the second quarter, global equity markets extended their strong performance.

Amid a more modest equity market outlook, private equity and real estate are poised to thrive.

As summer hits its stride, here are some musings about municipal bond performance to mull over as you unwind at the beach or on the couch (no judging!).

The influx of federal aid to U.S. municipal-bond issuers has papered over longstanding credit risks that threaten to come back to bite investors when the relief runs dry.

The global economy is in a mid-cycle expansion, following peaks in policy support and growth, and what is likely a transitory spike in inflation. We expect global growth to moderate to a still above-trend pace in 2022.

The Nasdaq-100 has been a powerful tool for many investors. Its history has inspired some asset managers to innovate – seeking ways to adapt the Nasdaq-100 to meet a breadth of investor needs like higher yields, reduced volatility, lower downside capture or even the potential for increased returns. Each of these innovations is powered by a different strategic options overlay.

Join us to hear from three different asset managers on their unique approaches to using options strategies with the Nasdaq-100.

Forcing the price of money to absurdly low or even negative rates is slowly but constantly detracting from economic progress and ripping the social fabric of our nation.

As the global economy continued to reopen and the recovery gained speed, markets reached new highs.

Rising interest rates generated negative year-to-date returns for investment grade bonds in 2021, but the second half of the year looks more promising. We believe the combination of reduced supply and strong demand will create attractive opportunities, and we are constructive on corporate credit and asset backed securities (ABS).

For investors considering preferred securities today, there is good news and bad news.

Many investors with exposure to the Chinese renminbi (RMB), having enjoyed a strong rally in the second quarter, are worried that policy uncertainties could hurt the currency’s short-term outlook.

Gold notched its third straight week of higher prices as the yield on the 10-year Treasury dipped below 1.3% for the first time since February.

The most torrid Treasuries rally in a year is likely set for a breather as traders reassess their rush to abandon reflation bets with some potentially decisive events looming in the coming days.