Tweedy Browne: We Are in the Early Stage of Value’s Resurgence

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTweedy, Browne Company LLC, based in Stamford, CT, is a value-based asset manager with an investment philosophy based on the work of Benjamin Graham. It was originally a broker, and one of its clients was Graham, co-author and author of the seminal textbooks on value investing: Security Analysis (1934) and The Intelligent Investor (1949). The firm also had brokerage relationships with Walter Schloss and Warren Buffett.

As of May 31, 2021, its flagship fund, the Tweedy, Browne International Value Fund (TBGVX; it was previously called the Tweedy, Browne Global Value Fund until its name was changed effective July 29), has returned 8.97% annually since its inception in 1993. That is 249 basis points better than the hedged MSCI EAFE index and 212 basis points better than the foreign stock fund average (which is calculated by Tweedy, Browne based on data provided by Morningstar and reflects average returns of all mutual funds in the Morningstar Foreign Large-Value, Foreign Large-Blend, Foreign Large-Growth, Foreign Small/Mid-Value, Foreign Small/Mid-Blend, and Foreign Small/Mid-Growth categories).

I interviewed seven members of Tweedy Browne’s investment team: Tom Shrager, Bob Wyckoff, Roger de Bree, Frank Hawrylak, Jay Hill, Sean McDonald and Andrew Ewert.

The interview took place on June 22, 2021, over Zoom. I previously interviewed several members of the investment committee at Tweedy, Browne on February 5, 2019, when we discussed their investment philosophy, how they differentiate themselves, and their views on currency hedging. Please refer to that interview for information on those topics.

In your March 31 letter to shareholders, you noted the strong performance of your funds: “For the last two quarters cumulatively, all four Tweedy, Browne Funds produced returns of roughly 20% or more and outpaced their benchmark indices by 25 to as much as 364 basis points. They outpaced growth-oriented indices by an even more substantial margin, which contributed to absolute returns for all four Funds of between 33.8% and 40.9% for the full fiscal year.” Congratulations. In your letter, you discussed the relative outperformance of growth over value and the fact that such extremes have historically been followed by strong results for value. Where does that transition from growth to value stand, and how big a role has that played in your funds’ results?

Bob Wyckoff: When the vaccines were announced last November with 95% efficacy, it sparked a strong stock market reaction. We had very strong equity markets in November. We had particularly strong markets on the value side. Investors began to look forward to reopening the economy, and robust growth in the near term in some of the more traditional parts of the economy, as opposed to the stay-at-home economy, which was largely led by big tech.

November was one of our strongest months of performance in our history at Tweedy. That has largely held since November. In fact, in both the fourth quarter and the first quarter of this year, value has significantly outperformed growth by nearly double. In the current quarter (April 1, 2021 to date), there's been a continued tug of war between the value trade and the so-called growth-tech trade. Technology, over the last few weeks, has had a bit of a comeback in the equity market. But in our view, the so-called value rotation may persist over time.

November was one of our strongest months of performance in our history at Tweedy. That has largely held since November. In fact, in both the fourth quarter and the first quarter of this year, value has significantly outperformed growth by nearly double. In the current quarter (April 1, 2021 to date), there's been a continued tug of war between the value trade and the so-called growth-tech trade. Technology, over the last few weeks, has had a bit of a comeback in the equity market. But in our view, the so-called value rotation may persist over time.

We have no idea whether this rotation is sustainable, or how long it will last. But the past is often prologue when you see periods of extreme outperformance for one style over the other. When you look at 2020 in the global developed MSCI world index, the growth component outperformed the value component by approximately 3,500 basis points. That gap has rarely if ever been wider. You'd have to go back to the tech bubble of 2000 to see comparable numbers. Of course, we know what happened in March of 2000 – the tech bubble began to burst and over the next several years we had two to three years of significant outperformance by value.

Is it going to play out the same way this time? It's hard to know. There's a good bit that feels similar to the tech bubble, such as concentration of returns in tech and rampant speculation in a plethora of money-losing, tech-related companies, but we'll have to see.

What were the underlying factors that contributed to your outperformance over Q4 2020 and Q1 2021?

Bob Wyckoff: Value outperformed growth during those two quarters and international stocks outperformed U.S. securities. Our portfolios are global and international in scope. The outperformance of value and the modest outperformance of international during the period was helpful for us.

Bob Wyckoff: Value outperformed growth during those two quarters and international stocks outperformed U.S. securities. Our portfolios are global and international in scope. The outperformance of value and the modest outperformance of international during the period was helpful for us.

We had strong returns in a number of financial and industrial holdings in the funds’ portfolios. The technology holdings that the funds own also continued to do well. Most stocks were up. We've been in a very strong environment over the last several quarters, but value has certainly had the edge.

Jay Hill: I'm hopeful that we're in the early innings of a transition from growth to value and that value can outperform growth for hopefully a number of years. There are three main reasons why we suspect this could occur.

It starts with a wide valuation gap. If you look at the beginning of 2021, the valuation multiple gap between growth and value stocks has never been greater. The risk of multiple contraction is much higher with growth stocks.

Second, rising interest rates will disproportionately negatively affect the growth stocks that are longer in duration. We expect that over time we are going to have higher interest rates. I know that hasn't been the case in the last couple of weeks, at least looking at the 10-year Treasury yield. But over time, inflation expectations are building, and I expect interest rates to move much higher from the level that exists today.

Finally, if you study the value factor, it historically performs the best in the early stages of an economic recovery. We're clearly in the early stages of an economic recovery.

For those three reasons, I'm optimistic that value's going to outperform in 2021 and hopefully, as Roger said, for a much longer period.

Roger de Bree has written that the “last year has not so much been about value versus growth as it has been about big tech and everything.” Looking back, particularly since 2014 when growth and big tech began their outperformance, do you regret missing out on any of the successes in big tech? Have you or will you adapt your value investing processes to be more inclusive of some of the technology companies that have performed so well?

Roger de Bree: Every stock that you missed that goes up you regret. But what's more important to us than all of that is that we have to get in at the right entry price valuation. If those enterprises were not trading at attractive valuations, we couldn't get in. We have invested in a few technology companies where the valuations were attractive to us. The most notable examples are Google and Cisco. Over time, we’ve looked at any number of technology companies, and we've been close to buying some of them. Of late, we added some more technology companies where we felt the entry valuation made sense.

We believe we found the right ones at the right price with the right growth. We haven't had to adjust our process. With our process, we could have owned more. But we wouldn't want to be in a situation where performance was so dependent on five or ten top stocks. Apple alone is something like 4% of the international growth index.

Jay Hill: One evolution in our investment process is our approach to valuing currently unprofitable business segments that mask underlying consolidated earnings power in an otherwise profitable core underlying business.

Historically, we have tended to approach the valuation of money-losing business segments in a conservative fashion. For example, suppose you are studying a business with three completely independent, distinct business segments. If two of the segments are profitable and the other segment loses money, we have historically appraised the value of the money-losing segment at zero, or book value or some other de minimis valuation.

Historically, we have tended to approach the valuation of money-losing business segments in a conservative fashion. For example, suppose you are studying a business with three completely independent, distinct business segments. If two of the segments are profitable and the other segment loses money, we have historically appraised the value of the money-losing segment at zero, or book value or some other de minimis valuation.

Over time we have developed greater appreciation for the potential value of business segments that currently lose money but almost certainly have strong long-term earnings growth prospects. This is particularly relevant with some technology businesses that have a very profitable core underlying business, yet consolidated earnings are masked by other segments that are still early in the maturation process, sometimes referred to as “moonshots.” Often these more nascent business segments initially require high upfront fixed costs and heavy investment in the early stages of development. But as these nascent business segments mature and sufficient scale is reached, they are capable of generating very high margins on incremental revenue growth. In these situations, we have more recently begun to place a higher, but also more realistic, valuation on a money-losing segment which we believe has a strong long-term outlook. Our valuation of Alibaba’s Ali-Cloud business, a valuable segment that currently generates just break-even profits, is a great example that demonstrates this evolution of our investment process.

Tom Shrager: Analyzing a tech company is no different than analyzing any other company. We ask the same questions that we ask of any other company. But what we have to focus on a bit more in the case of a tech company is the competitive environment and the issues of potential obsolescence of that technology. But they are analyzable.

The reason we didn't have a bigger weighting in high-tech companies is because in those rare cases when we came across what appeared to be an undervalued tech company, they were often cheap for a good reason. In other cases, if they were expensive, it was for a good reason because they were growing very, very fast. We became aware of them at a point in time in which we felt they were at maximum profitability and maximum growth. They didn't fit because of optimistic expectations embedded in the valuation.

Value investing, as Jay has said, is buying stocks at the moment of pain, where there is some level of uncertainty in the market as to whether the company will make it, whether the growth will continue and so on. That's when we generally get involved with stocks and with tech stocks in particular.

We bought Google eight or nine years ago when there was a transition from the desktop to the mobile phone and revenues per click were falling. We were asking, “What's going on? Is their business model going away?” At that time, we were able to buy into an absolutely fantastic company for 12-times EBITA, because there was this moment of uncertainty.

When we bought our position in MasterCard ten years ago, it was when people were saying their business model was going to be negatively impacted by a collapse in interchange fees due the new Durbin Amendment. That didn’t happen. We more recently bought Alibaba at a moment of great uncertainty when the company’s share price was declining in the face of increased scrutiny by the Chinese government.

Sean McDonald: You asked about the ones that we regret. The one that I regret the most is Microsoft. If I look back to 2012, Microsoft was on our screens as being cheap. It had a great balance sheet. It was obviously a wide-moat, dominant business. But at the time there were some questions about future growth, capital allocation, and some of the products that it was launching. We wound up passing on it.

We have another name in our dividend fund, Intel, which we bought in September 2020. It fits our criteria today the same way that Microsoft did in 2012. At purchase, we bought it around eight times EBITA. It has a strong balance sheet, generates lots of cash, was buying back stock, and the CEO at the time, Bob Swan, was buying stock personally. It ticked all of our boxes.

Is Intel going to be the next Microsoft? That's a lot harder to say. But like Tom just said, the opportunities in these things come when there's a lot of uncertainty and a lot of pain. We've got that with Intel. The new CEO, Pat Gelsinger, has a vision for the company. If they're successful rolling out a foundry model, that could be a game changer for the company. If anybody can do that for Intel, it's the current CEO. We're obviously monitoring the situation pretty carefully, but it fits our criteria. It's something that we can own just like Microsoft back in 2012.

Bob Wyckoff: A lot of people think value investors, because of the factors Tom pointed out, can't often get involved in technology. Indeed, we have to be selective, but you can't be a successful value investor without an understanding of how technology can disrupt the businesses in which we are currently invested.

Thinking about what's going on in terms of innovation and new technology is critically important for us in analyzing the competitive positions of non-technology companies or companies that aren't as dominated by tech. Technology is on our minds every day as value investors.

You mentioned one notable addition to your funds was Alibaba, which does fit into the category of a large technology company. In your letter, you wrote that its appeal comes from it being a dominant, wide-moat, platform business. What made Alibaba attractive, as compared to U.S. companies like Amazon?

Andrew Ewert: This can provide a good example or case study to some of your previous questions. The reason comes down to price or valuation. Both companies obviously have core e-commerce businesses that are quite successful and dominant. They also have other ventures and businesses from online video to cloud computing. Many of those businesses are either unprofitable or arguably exist just to reinforce their ecosystems.

But without valuing any of those other assets, just on a stated-earnings basis, Amazon is trading at nearly 50-times next year's consensus earnings. Alibaba is at a high-teens earnings multiple. In our view, both businesses should grow at a high-teens rate and benefit from rising e-commerce consumption, but Amazon is just simply more expensive.

But without valuing any of those other assets, just on a stated-earnings basis, Amazon is trading at nearly 50-times next year's consensus earnings. Alibaba is at a high-teens earnings multiple. In our view, both businesses should grow at a high-teens rate and benefit from rising e-commerce consumption, but Amazon is just simply more expensive.

Related to some of the things Tom said, there is no uncertainty at Amazon. There is no margin of safety. You could say that both companies have regulatory risks or at least regulatory scrutiny. Alibaba is getting a discount for that, where there's no discount at all in the valuation of Amazon. Jay referenced our valuation methodology for Alibaba; we deduct our estimated value for Alibaba’s cloud computing business, which uses a normalized profitability based on the profitability for Amazon’s AWS segment. We also deduct the balance sheet value for Alibaba's financial investments and its equity affiliates as well as estimated values for its other businesses.

We estimate we're paying less than 12-times EBITA for Alibaba's core marketplace e-commerce business. We can't arrive at anywhere near that valuation for Amazon without assuming much higher margins for its core e-commerce business or looking at earnings several years out that assume very high growth rates. A lot of Amazon's other businesses like Prime do serve to reinforce the e-commerce ecosystem and they might not have much standalone value.

Amazon and Alibaba are not the same type of e-commerce business. Amazon is both a marketplace and a direct retailer. It's very asset intensive. It competes against merchants as well as enables them, whereas Alibaba exists to support its merchants. Its customer is the merchant. Amazon might have a better competitive position in its home market, but it is more asset intensive. We believe China should grow faster than the U.S. over time.

But it comes down to price or valuation and Amazon's priced for perfection, whereas Alibaba's priced with a great deal of uncertainty.

Your cash position in the Global Value Fund went from 11.9% at the end of March 2020 to 4.5% a year later. In your letter, you wrote this was a prolific period of new acquisitions. Are there any others you’d like to highlight?

Jay Hill: I'll mention one new idea that you're probably familiar with if you watch television. It's The Progressive Corporation, the third largest personal auto insurance carrier in the United States. It's a best-of-breed auto insurance carrier with clear competitive advantages. It has a long-term track record of growing market share, earning industry leading margins and generating high returns.

If you look at personal auto, Progressive's market share was 7% in 2007, and that grew to 13% in 2020. It is growing much faster than the rest of the industry. Yet at the same time, Progressive has industry-leading margins.

Normally, when you see an insurance company and it's growing its revenue at a high rate, you suspect it is giving business away or it is underwriting unprofitable business. But Progressive has a unique combination where it has been growing faster than the industry and yet it also has, using a 10-year average, industry-leading margins. Or said another way, the lowest 10-year average combined ratio.

It is also an insurance company that earns returns that are substantially higher than the average property and casualty company. Its 15-year average return on equity was 19%. At Tweedy, Browne, we refer to a metric called “value compounding” – how well has the company grown its value over time if you use a consistent valuation methodology. The way that we measure this for insurance companies is how fast has the business grown tangible book value per share, plus dividends per share, over time. Over the last 15 years, Progressive has done that, at about a 13% compounded annual rate. It has a long history of growing its underlying intrinsic value. This stems from two clear-cut competitive advantages: direct distribution and superior data analytics.

Its moat comes in part from direct distribution. More than half of Progressive’s personal auto insurance policies are sold direct over the internet without an agent. I don't know how you buy your auto insurance, Bob, but most older people have tended to use an agent, either a captive agent who works for a carrier or an independent agent. But buying insurance with an agent requires a commission that the insurance carrier pays.

Selling more than half of its personal auto insurance policies direct without agent commissions gives Progressive a cost advantage. That shows up as a lower expense ratio for this business over time. It allows Progressive to offer lower prices, gain market share and earn superior margins relative to its competition. That's extremely powerful. The trend towards more consumers buying insurance direct over the internet without an agent is going to grow.

The wind is behind its back in the direct channel because younger people are more comfortable buying insurance without an agent directly over the internet.

The second clear cut advantage that Progressive has is superior data analytics. The validation of that advantage shows up in its lower claims-loss ratio over time versus its competition.

Progressive is widely acknowledged as possessing the most granular data and knowledge about how to match risk with rate. There are lots of examples, but perhaps the best example is that it was the pioneer of telematics. It has a product, Snapshot, that is an app that goes on your phone. Bob, I don't know if you're a good driver or not.

My wife doesn't think so.

If you have this app on your telephone, it allows Progressive to monitor what time of day you drive, how many miles you drive, and how many left-hand turns you make. Are you driving in rush hour or non-rush hour? How often do you hard brake or change lanes? How fast do you accelerate? Are you playing with phone while driving? It takes a look at all of this data, and then it dynamically increases or lowers your rate based upon your driving behavior. Would you benefit from this, Bob?

It's interesting. I do watch TV and I am very aware of the Progressive ads. We've seen the same trend in the insurance industry with annuities, where they've disintermediated the agent. Many of the insurance companies are marketing annuities directly through advisors to clients, but without paying a commission to an agent.

It's a huge edge. By eliminating agent commissions, the trade-off is that Progressive has to spend more on advertising. GEICO has the same model. That's why you're inundated with Progressive and GEICO ads on television. But the net benefit is it's cheaper to not pay agent commissions and pay a little bit more for advertising.

Tom Shrager: One of the reasons that Progressive’s underwriting is better than a lot of other insurance companies is that it comes from a background of insuring high-risk drivers. If you do that, you ruin a business very, very quickly if you don't know what you're doing in terms of underwriting. If you come from that culture and you move up to average drivers, better drivers, it's a walk in the park.

Jay Hill: Progressive was founded in 1937 and its roots are in what Tom mentioned, the non-standard market. What that means is if you've got a bunch of DUIs or you've been in a bunch of accidents or if you have moved frequently, traditional standard auto insurance carriers would not insure you. That was Progressive's early market, and it didn't get into the standard market until the 1990s. Progressive’s roots in the non-standard, higher risk segments resulted in an intense focus on using data to drive pricing decisions.

Finally, in our estimation, Progressive is a pretty cheap stock.

We bought it for our dividend fund. If you use long-term average margins, we believe Progressive has normalized operating earnings power of about $5.70 a share. If you put a 20 P/E on this business, which we think it deserves because it has been growing its top line at a double-digit rate, we get a valuation of $114 per share. We were able to buy the stock at approximately $85 per share.

Progressive has paid an above-average dividend, but has done it in a unique way. It has paid a quarterly dividend of $.10 a share. In addition, it has paid a special dividend at least annually. If you look at the last couple of years, the dividend yield on our purchase price was between 3% and 6%. It clearly has been an above-average dividend payer.

The question that is at the forefront of economic discourse is whether inflation will be “transitory,” as the Fed expects, or more long-lasting. As value investors, I know that macroeconomic factors don’t play into your process. But what are your thoughts on the inflation question, specifically as to how it could affect the companies you own?

Bob Wyckoff: I'll make a couple of comments and then we can talk about how it relates to some of the companies we own. We're concerned about inflation. As value investors we are certainly not experts on predicting interest rates. But what has gone on in markets over the last decade – the unprecedented level of coordinated monetary largesse around the globe in Europe, Japan, the UK, and the United States – has led to very strong risk asset markets and moderate economic growth.

We are coming out of the pandemic with animal spirits beginning to stir in our economy in a big way. On top of this, we're adding a tremendous amount of fiscal and continued monetary stimulus. We've had a very significant rise in the money supply over the last year as well.

This dramatic increase in demand, the supply of money that's coming at us, supply disruptions that we're seeing coming out of COVID, and wage pressure that we're beginning to see could mean this inflation has further to go than we might suspect. But of course, we can't know. If inflation doesn't prove to be transitory and does prove to be sustainable at least in the early stages, that should inure to the benefit of value investors because of what Jay suggested earlier.

We'll get an uptick in rates that will likely have disproportionately negative effect on the valuation of longer duration growth stocks than it should on shorter duration, value stocks. But if inflation gets away from us in the next year or two, we could have a come-uppance across our equity markets. Even in an environment like that, value should hold up better than growth.

Jay Hill: When we speak to our companies, inflation comes up on every conference call. Companies are talking about three main buckets of inflation: high raw material inputs, increased logistics spending in transportation and shipping costs, and increasing labor costs. The first two, like the recent increases in lumber and copper and even in oil, could be more transitory. Perhaps the increases in shipping costs that were caused by the Suez Canal mishap and the port in China could be more transitory and worked out over time.

But that third bucket, the increase in wages, tends to be stickier. That has the potential to be much more long lasting and problematic and could lead to the Fed having to increase interest rates faster than its current projection.

Tom Shrager: I would like to provide a bit of historical perspective. If you think about the great inflation of 1965 to 1982, it began under William McChesney Martin, who developed a reputation as being a defender of Fed independence. He was arguing with Lyndon Johnson. At some point, Johnson screamed at him using indecent language, telling him not to increase interest rates.

But he stepped down in 1970 and inflation already was running around 6%. Arthur Burns, his successor, let it roar, partially because of policy mistakes; they were claiming that commodities or temporary things were happening in the labor market, such as strikes.

But what led to high inflation was a confluence of a couple of things. One of them was liberal monetary policy. We have now liberal monetary policy. The other one was significant increases in government spending to support Great Society Programs and the Vietnam War. We have now significant increases in government spending as well.

To create inflation, which means creating inflationary expectations that are anchored, it's not about lumber prices going up to $1,400 and then going down to a thousand or so. Those are temporary things that people get through. But as Jay said, once inflation expectations get anchored, then workers will ask for higher wages. Those wages are sticky. What you have to look over the next year or so is what happens to wages.

If you have significant wage inflation, then inflationary expectations are going to get anchored, and you'll have sustained inflation over a longer period of time. While inflation is good in the initial phases for value investors, for the overall stock market, periods of sustained high inflation are not good. Look at what happened in the 1970s.

Frank Hawrylak: Maybe some math will help. At a 2% inflation rate over a 10-year period, the value of a dollar depreciates by 18%. We've been running at 2%, maybe a little bit under that, for the last decade. Under the low inflation-no inflation scenario that people talk about, the dollar still is depreciating by 18%.

Bumping the rate up to 4% does not seem impossible.

At this inflation rate, the dollar depreciates by 33% over a 10-year period. At a 6%, inflation rate, you lose 46% of your purchasing power.

In fixed-coupon assets, like bonds, you're looking at 2% or so long government bond yields. The real return math is terrible at this level. That doesn't mean building a cash position to take advantage of future opportunities is a bad idea. But, to own long-dated fixed coupon assets does not seem like a recipe for financial progress, unless everybody is wrong and interest rates continue to go down. If they go down or go negative, then asset prices will continue to go up. But we think inflation is likely to be a big problem.

Roger de Bree: Overall, we are partly hedged. In some of our highly branded, consumer goods companies, labor and input costs play a role. But if you are a Coca-Cola producer, the sugar costs that you pay are a fraction of a percent of sales versus what a non-branded company would pay. Your margins are much higher.

The same is true for Unilever, Nestlé and Diageo. Labor and input costs in those businesses are less relevant when you have strong brands that protect you in a more difficult environment. When it comes to inflation, I'm not saying it will be very easy. But we believe it will be easier than for many other companies.

If you have a business that dominates local logistics and its model is based on that, like a rock pit – unfortunately, we don't own any now – it has an action radius where inflation doesn't matter that much. You can't ship the product very far. We think about those matters. Since we saw these crazy monetary actions starting 2007 to 2009, we have been thinking about what happens if you get a lot of inflation.

We're quite skewed to that outcome. We have many companies that we believe have strong business models. We have companies that don't sail into the wind in terms of their balance sheets or have a lot of debt. Those are the factors that we believe will give us some extra protection.

Much of the commentary on the market focuses on its “frothiness,” which is seen in SPAC issuance, Reddit and meme stocks, and cryptocurrencies. In this regard, you quoted Warren Buffett in your letter in his characterization of the risk associated with excessive valuations: “Geometric progressions eventually forge their own anchors.” How does that frothiness affect your thinking, if at all? Are you worried that companies you own will be held down by anchors?

Tom Shrager: We hope that all our companies are going to become frothier.

Roger de Bree: It's a little bit like being at a party where everybody's very drunk and you are sober.

Jay Hill: Your question raises the issue of how excessive valuations could impact our companies in a negative way, such as through capital allocation. We have several companies where M&A and share repurchases are a big part of the compounding story. To the extent that valuations across the board are higher, it makes M&A less attractive. In almost every conference call I'm on, management says, "Hey, we're looking for acquisitions, but we think seller expectations are too high."

I hope they remain prudent and resist the temptation to stretch. Share repurchases are a powerful driver of several companies that we own. All things being equal, share repurchases are less attractive or less value accretive when the stock price is closer to your estimate of intrinsic value. The best time to allocate capital for share repurchases is when there's a wide gap between what you think intrinsic value is and the stock price. The closer the gap, the less efficient share repurchase becomes as a tool for capital allocation.

Frank Hawrylak: We try to stay away from businesses we can't value. We rely on real, current cash flows to support our valuations. We're willing to look out a little bit when assigning values to cash flows and we are happy to receive free options on things we can’t value, but we won’t pay for them.

We approach investing in a business-like fashion. Which means we miss out on the excitement and gambling aspects that come with buying what is hot or in fashion. If you get in early and leave before the party ends, you can make a lot of money using this approach. But if you're late, the thrill that comes with rising prices can quickly turn to agony and huge losses. I just don't know when it's going to happen.

There will be a lot of losers in the cryptocurrency, SPAC, Reddit and meme game at some point. One of the best-performing funds over the last five years has been Cathie Wood’s ARRK, which is an actively managed ETF. Have you considered converting any of your funds to ETFs or offering ETF versions of them?

Bob Wyckoff: We've been studying ETFs. They offer investors very attractive tax advantages – the ability to effectively fund redemptions in kind with the help of arbitrageurs. This allows for the avoidance of security sales that would trigger capital gain recognition. We tend to be very tax-focused and tax-sensitive investors. We're interested in those positive attributes of ETFs. There are both transparent and non-transparent active ETFs.

Recently, non-transparent ETFs have attracted the interest of active money managers. We're not an exception. We're interested, but the regulatory authorities have yet to approve of non-transparent ETFs for international investing, which is a lot of what we do. But that approval may be on the not too distant horizon, and it could very well be of great interest to us when it comes about.

Value investing has become increasingly popular among active value managers and quantitative or factor-driven strategies. Has the demand for value stocks and the pursuit of value strategies diminished your opportunity set?

Bob Wyckoff: Value hasn't been terribly popular over the last six to seven years with the rise of “big tech.”.We heard in the press almost every day until the last couple of quarters how value had underperformed growth for such an extraordinary period of time that it was effectively dead. Indeed, this was the third time in my career that value had been declared dead by market commentators, and to borrow from Mark Twain, I suspect that this time around as with the other two, the reports of its death have been greatly exaggerated.

Without periods of underperformance, everybody would be a value investor and any benefit from the strategy would be arbitraged away. In our experience, investors who have been willing and able to endure sometimes uncomfortably long and difficult periods for value have been able to reap the superior returns that value investing has afforded. It is in these challenging periods that the opportunity set for price sensitive investors becomes more robust. Unless human nature changes, these periods of price opportunity are not likely to go away.

In my interview with you last year, which was in May and marked the 100th anniversary of your firm, I asked about the risks that you were facing and what made you optimistic. At the time, you were worried about a second wave of the pandemic, and you recognized that vaccines were on their way. Both indeed transpired, and your funds prospered. You were optimistic about the resilience of the U.S. economy and the history of America overcoming great challenges. What is your view today, particularly with respect to risks that concern you?

Bob Wyckoff: The unchecked and coordinated monetary largesse that has occurred over the last decade should concern investors. Consider the fiscal stimulus coming on top of that, and the impact that could have on interest rates and inflation going forward. Those are certainly worries that could be of benefit to value investors in the near term. But over the long term, if we get significant increases in interest rates and inflation, it will be challenging for financial markets.

Another area of concern is rising taxes. We have a new administration in the United States. We all know tax increases are in store for us soon. Administration officials are currently leading an effort to get a coordinated minimum corporate tax globally. Rising corporate taxes will likely have a significant negative impact on corporate earnings, which could impact valuations in our equity markets.

In addition, speculative activity in equity markets has been on the rise of late and can be seen in the fascination of younger investors with meme stocks, the rapid opening of retail accounts at places like Robinhood, increases in option trading, rising margin debt, the soaring performance of numerous unprofitable tech companies, and the unprecedented growth of SPACs over the last couple of years. There was a similar speculative fervor in late 1999 and early 2000 that in part helped lead to the bursting of the tech bubble beginning in March of 2000. We're again seeing aspects of that speculation in markets today

But at the end of the day, value investors are optimists. We believe in mean reversion. We are skating always to where we think the puck is going, not to where the puck is. As a result, a lot of what we get involved with is out of favor at any given point in time. We are optimistic that those companies will return to favor.

Tom Shrager: There are a couple of effects on companies from rising interest rates and taxes. One effect is for longer-held assets like growth stocks, where higher interest rates mean a lower present value. That's an issue for that segment of the market and for the market as a whole.

If you're going to increase corporate tax rates in a significant manner, the result would be a lower net present value of future cash flows. In part the rally that happened over the last couple of years in the stock market was driven by lower marginal tax rates for corporations. Maybe the reverse will be the case if tax rates for corporations are raised.

Jay Hill: All great investments began in discomfort. It's fear that breeds bargains. In the spring of 2020, there was a lot of fear in the world. Across our funds, from March through June, we bought in excess of 20 new securities, which was an unprecedented level of activity for Tweedy.

Today there's less fear, and the opportunity set is not as attractive. Howard Marks says there's always two risks in investing that you can't fully offset: the risk of missing an opportunity or what some people call the fear of missing out (FOMO), and the risk of losing money. You're always trying to balance those two. But today market participants are more concerned with the risk of missing out.

Tom Shrager: The typical “metal-basher” stocks that you could buy a year ago at very reasonable prices were similar to shooting fish in a barrel. Those stocks have become more difficult to uncover as they have appreciated in price. However, there are other opportunities that we have had over the last six months; for instance, we bought more stocks in China. But the number of opportunities that appear on our screen every day has gone down.

Roger de Bree: One should never forget that this is a wondrously big world. There are 90,000 stocks that you can invest in all over the world. Fear creates opportunity, but people tend to see that opportunity more in bigger stocks. There's also a lot of opportunity in obscure stocks. We do a lot of that. We love it when we find obscure stocks that are cheap. That keeps us going, especially in an environment where you have a lot of the big names that have frothy valuations, which may be a sign that things will turn.

Wirecard, Archegos, Greensill, Nikola – all those scandals were happening around us. That is a sign of the state of the market. As long as we can muddle through and find a few off-the-beaten-track companies with valuations and business models we like, we're happy campers. As Tom and Jay have said, there's less of that now, but we are still okay. The machine is turning and we're optimistic.

The information presented in this interview is designed to be illustrative of the general investment philosophy and broad investment style overview of Tweedy, Browne Company LLC (“Tweedy, Browne”). It contains forthright opinions and statements on investment techniques, economic and market conditions and other matters. These opinions and statements are as of the date indicated, and are subject to change without notice. There is no guarantee that these opinions and statements will prove to be correct, and some of them are inherently speculative. The information included in this interview is not intended, and should not be construed, as an offer or recommendation to buy or sell any security, nor should specific information contained herein be relied upon as investment advice or statements of fact. This interview does not contain information reasonably sufficient upon which to base an investment decision.

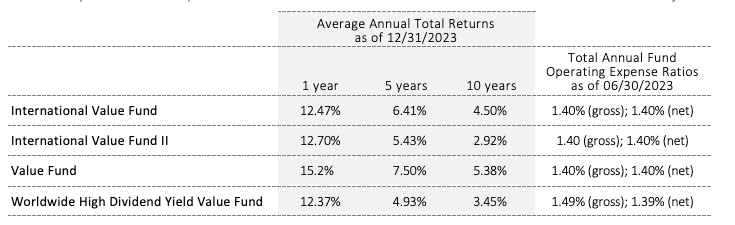

Tweedy, Browne is the investment adviser to four U.S. mutual funds (each, a “Fund” and, collectively, the “Funds”): Tweedy, Browne International Value Fund (the “International Value Fund”), Tweedy, Browne International Value Fund II – Currency Unhedged (the “International Value Fund II”), Tweedy, Browne Value Fund (the “Value Fund”), and Tweedy, Browne Worldwide High Dividend Yield Value Fund (the “Worldwide High Dividend Yield Value Fund”).

Investment performance and portfolio data for the Funds in the interview is as of the date indicated and is subject to change.

The performance data shown represents past performance and is not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Current performance may be lower or higher than the performance data shown. Please visit www.tweedy.com to obtain performance data that is current to the most recent month end, or to obtain after-tax performance information.

Tweedy, Browne has voluntarily agreed, effective May 22, 2020 through at least July 31, 2024, to waive the International Value Fund’s fees whenever the Fund’s average daily net assets (“ADNA”) exceed $6 billion. Under the arrangement, the advisory fee payable by the Fund is as follows: 1.25% on the first $6 billion of the Fund’s ADNA; 0.80% on the next $1 billion of the Fund’s ADNA (ADNA over $6 billion up to $7 billion); 0.70% on the next $1 billion of the Fund’s ADNA (ADNA over $7 billion up to $8 billion); and 0.60% on the remaining amount, if any, of the Fund's ADNA (ADNA over $8 billion). The performance data shown above would have been lower had fees not been waived during certain periods.

Tweedy, Browne has voluntarily agreed, effective December 1, 2017 through at least July 31, 2024, to waive a portion of the International Value Fund II’s, the Value Fund’s and the Worldwide High Dividend Yield Value Fund’s investment advisory fees and/or reimburse a portion of each Fund’s expenses to the extent necessary to keep each Fund’s expense ratio in line with the expense ratio of the International Value Fund. (For purposes of this calculation, each Fund’s acquired fund fees and expenses, brokerage costs, interest, taxes and extraordinary expenses are disregarded, and each Fund’s expense ratio is rounded to two decimal points.) The net expense ratios set forth above reflect this limitation, while the gross expense ratios do not. The International Value Fund II’s, Value Fund’s and Worldwide High Dividend Yield Value Fund’s performance data shown above would have been lower had fees and expenses not been waived and/or reimbursed during certain periods.

The Funds do not impose any front-end or deferred sales charges. The expense ratios shown above reflect the inclusion of acquired fund fees and expenses (i.e., the fees and expenses attributable to investing cash balances in money market funds) and may differ from those shown in the Funds’ financial statements.

Investment decisions for the Funds are made by Tweedy, Browne's Investment Committee, which is comprised of Roger R. de Bree, Frank H. Hawrylak, Andrew Ewert, Jay Hill, Thomas H. Shrager, John D. Spears and Robert Q. Wyckoff, Jr. Much of the information in this interview represents the opinions of the speakers and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Views expressed may differ from those of the Investment Committee or of Tweedy, Browne as a whole. In the course of the interview, Tweedy, Browne personnel mention certain securities that may have been held in one or more Funds managed by Tweedy, Browne as of or prior to the date of the interview. Discussion of any particular security, sector or Fund by Tweedy, Browne personnel does not constitute information reasonably sufficient upon which to base an investment decision, should not be considered a recommendation to purchase or sell any particular security, and should not be considered an offer to sell or a solicitation of an offer to buy any of the securities referenced. Moreover, discussions relating to portfolio consideration are for illustrative purposes only and not indicative of any specific portfolio. The information in this interview is not guaranteed as to its accuracy or completeness.

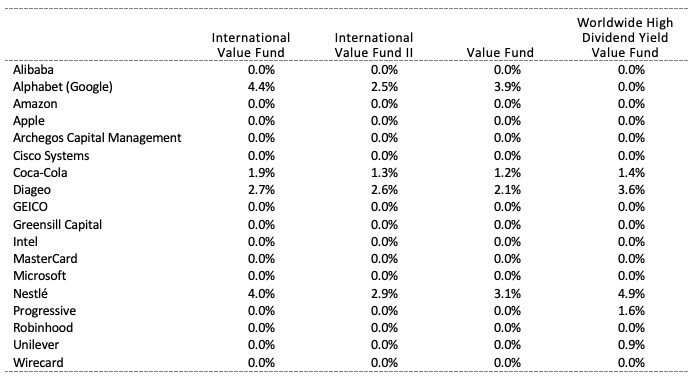

As of December 31, 2023, the International Value Fund, International Value Fund II, Value Fund, and Worldwide High Dividend Yield Value Fund had each invested the following percentages of its net assets in the following portfolio holdings:

Current and future portfolio holdings are subject to risk. The securities of small, less well-known companies may be more volatile than those of larger companies. In addition, investing in foreign securities involves additional risks beyond the risks of investing in securities of US markets. These risks, which are more pronounced in emerging markets, include economic and political considerations not typically found in US markets, including currency fluctuation, political uncertainty and different financial standards, regulatory environments, and overall market and economic factors in the countries. Force majeure events such as pandemics and natural disasters are likely to increase the risks inherent in investments and could have a broad negative impact on the world economy and business activity in general. Value investing involves the risk that the market will not recognize a security's intrinsic value for a long time, or that a security thought to be undervalued may actually be appropriately priced when purchased. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Diversification does not guarantee a profit or protect against a loss in declining markets. Investors should refer to the prospectus for a description of risk factors associated with investments in securities held by the Funds.

Although the practice of hedging against currency exchange rate changes utilized by the International Value Fund and Value Fund reduces the risk of loss from exchange rate movements, it also reduces the ability of the Funds to gain from favorable exchange rate movements when the US dollar declines against the currencies in which the Funds’ investments are denominated and may impose costs on the Funds. As a result of practical considerations, fluctuations in a security’s prices, and fluctuations in currencies, a Fund’s hedges are expected to approximate, but will generally not equal, the Fund’s perceived foreign currency risk.

The Managing Directors and employees of Tweedy, Browne Company LLC may have a financial interest in the securities mentioned herein because, where consistent with the Firm’s Code of Ethics, the Managing Directors and employees may own these securities in their personal securities trading accounts or through their ownership of various pooled vehicles that own these securities.

Earnings before interest, taxes and amortization (or EBITA) is used to gauge a company’s operating profitability.

Since September 30, 2003, the Foreign Stock Fund Average is calculated by Tweedy, Browne based on data provided by Morningstar and reflects average returns or portfolio turnover rates of all mutual funds in the Morningstar Foreign Large-Value, Foreign Large-Blend, Foreign Large-Growth, Foreign Small/Mid-Value, Foreign Small/Mid-Blend, and Foreign Small/Mid-Growth categories. Funds in these categories typically invest in international stocks and have less than 20% of their assets invested in U.S. stocks. These funds may or may not be hedged to the U.S. dollar, which will affect reported returns. References to "Foreign Stock Funds" or the "Foreign Stock Fund Average" that predate September 30, 2003 are references to Morningstar's Foreign Stock Funds and Foreign Stock Fund Average, respectively, while references to Foreign Stock Funds and the Foreign Stock Fund Average for the period beginning September 30, 2003 refer to Foreign Stock Funds and the Foreign Stock Fund Average as calculated by Tweedy, Browne.

The MSCI EAFE Index is an unmanaged, free float-adjusted capitalization weighted index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The MSCI EAFE Index (in US$) reflects the return of the MSCI EAFE Index for a US dollar investor. The MSCI EAFE Index (Hedged to US$) consists of the results of the MSCI EAFE Index 100% hedged back into U.S. dollars and accounts for interest rate differentials in forward currency exchange rates. Index figures do not reflect any deduction for fees, expenses or taxes. The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets.

© Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damage or losses arising from any use of this information.

Past performance is no guarantee of future results.

Tweedy, Browne International Value Fund, Tweedy, Browne International Value Fund II – Currency Unhedged, Tweedy, Browne Value Fund, and Tweedy, Browne Worldwide High Dividend Yield Value Fund are distributed by AMG Distributors, Inc., Member FINRA/SIPC.

This material must be preceded or accompanied by a prospectus for Tweedy, Browne Fund Inc. Investors should consider the Fund’s investment objectives, risks, charges and expenses carefully before investing. Click here or call (800) 432-4789 to obtain a free prospectus, which contains this and other information about the Fund. Please read the prospectus carefully before investing.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All