Unpack the latest ICI flow data as long-term mutual funds bleed billions directly into low-cost, model-ready ETFs.

The capital markets have become an increasingly complex space for investors, complexities that are heightened by the sheer number of ways one can invest.

Model portfolios are seeing billions in inflows, and part of that success may be from how these strategies implement ETFs and private assets.

The higher the rally in technology high-flyers, the louder the anxiety around a new wave of turbulence in the group.

The business of overseeing individually tailored municipal-bond portfolios has continued to grow rapidly, turning those money managers into the biggest holders of state and local government debt, according to JPMorgan Chase & Co.

It’s been a long time coming for the asset management world, but ETF share classes are now a reality. Fidelity Investments has joined that movement, with the launch of its first ETF share classes for some of its mutual funds.

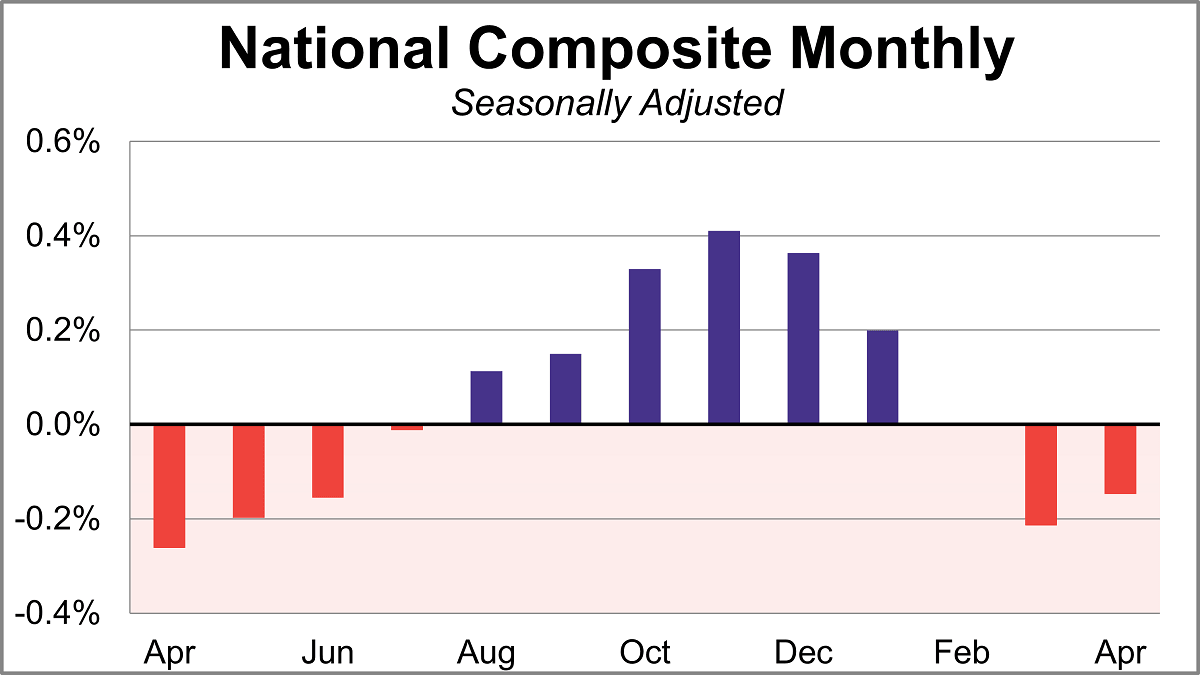

Home prices fell for a second straight month in April according to the S&P Cotality Case-Shiller index, as the housing slowdown intensifies. On a seasonally adjusted basis, the national index dropped 0.1% month-over-month and was up 0.8% year-over-year.

A strong quarter across major indexes. The second quarter is winding down and what a quarter it has been with the S&P 500 up 12.6% quarter to date, while the Nasdaq-100 and Russell 2000 are both up over 20%. Despite some twists and turns, the path of least resistance for stocks broadly remained up and to the right for much of the last three months.

For decades, financial advisors have built strong relationships by helping clients manage IRAs, taxable accounts, and rollover assets after they leave an employer. Meanwhile, a significant, often the largest pool, of client wealth has quietly remained out of reach: assets inside workplace retirement plans.

The ETF ecosystem is always changing and growing. Thanks to the ETF’s flexibility, transparency, and tradability, it can help investors achieve plenty of bespoke goals. That even includes investing with an eye towards philanthropic causes as with philanthropic ETFs ASD and DUTY.

The money is REAL. The question was never whether it exists. It’s who’s spending it, and what they borrowed to do it. When the wall of cash and the bottom half finally commit to risk at the same moment the Fed turns hawkish, that’s not the start of something. That’s the part of the cycle where the careful investor gets paid to be careful.

The way the SPIVA U.S. Scorecard evaluates performance is not well aligned with the experience of investors. Adjusting for this reveals a more balanced view of active fund performance. While active and passive U.S. equity funds perform similarly, active bond funds tend to outperform.

As expectations have shifted toward slower growth, higher inflation, and higher rates, investors have rotated back to sectors like large-cap technology and semiconductors, capable of delivering durable earnings in a tougher macro environment.

Private credit is having a moment in the headlines. Higher interest rates and a pullback in certain types of bank lending have pushed more financing activity into private markets. Investors may be left with a simple question: What exactly is private credit?

AI is both a foundational technology and the ultimate replacement product, which we believe explains why it has attracted unprecedented levels of capital and why the investment opportunities are so compelling.

The corporate world is awash in capex. Leaders in the artificial intelligence (AI) arms race are pouring hundreds of billions of dollars into tech projects, and uncertainty surrounds their profitability. For now, the market rewards this use of cash, but it’s not without pitfalls. Share buybacks, for instance, are seen as a net loser, while the S&P 500® dividend yield has sunk toward all-time lows near 1%.

Important investment decisions should always be based on investment principles, not predictions. Principles form the foundation of a sensible long-term financial plan and are timeless rules.

Green life, sustainable mutual funds, buying local, the “buy nothing” movement, plastic-free living, eco-fashion, electric vehicles. You’ve seen all the headlines about reducing your impact on the planet, but you may be wondering how you can best implement a greener workplace in a way that considers the needs of your business, employees and clients or customers.

In August 2025, the US President Donald Trump signed an executive order aimed at broadening the investments available in defined contribution plans (DC plans). On March 30, 2026, the US Department of Labor issued proposed guidance regarding a plan fiduciary’s selection of investments, including private market and other alternative investments, in 401(k) plans.

This week J.P. Morgan Asset Management launched two actively managed municipal bond ETFs focused on California and New York debt, offering investors a way to earn tax-free income inside a more flexible and transparent fund structure.

J.P. Morgan converted two mutual funds into active muni ETFs for California and New York investors seeking tax-free income.

Interest rates remain one of the primary concerns for investors as Kevin Warsh has officially assumed leadership at the U.S. Federal Reserve (Fed). While we believe the possibility of a rate cut has diminished considerably, we are not yet expecting additional rate hikes.

New York City is facing one of the most significant fiscal challenges in recent memory. The NYC Comptroller has projected a $2.2 billion budget shortfall for FY2026, growing to a $10.4 billion gap in FY2027 (Source: New York City Comptroller, January 2026). That is a two-year deficit of roughly $12.6 billion.

The essential feature of a useful alternative asset isn’t that it’s unusual or exotic, but that its returns aren’t tightly linked to the risks that already dominate the portfolio. The value of an alternative asset comes from the way it interacts with the other assets in the portfolio.

A tidal wave of conversions has siphoned an unprecedented amount of capital out of mutual funds and into the ETF wrapper. Last year’s record 60 mutual-fund-to-ETF conversions in 2025 across 31 firms pushed total converted assets past $260 billion, and the past five years have now seen a grand total of 203 conversions.

New AdvizorPro data shows RIAs broadened their ETF lineups in Q1 2026, leaning into real assets, active managers, and defense strategies.

I’ve lost count of the praise heaped on US hedge funds for their “historic performance” in April on artificial intelligence-related bets and alleged foresight of a ceasefire in the Iran war.

As more individuals turn to non-traditional financial advice — offered through social media, artificial intelligence, or other online services and platforms — advisors will be tasked with fostering a greater sense of trust with the public.

Private markets (private equity, private credit and real estate) have historically delivered an “illiquidity premium”. Institutions and family offices have recognized this illiquidity premium and have historically allocated significant capital to capture it.

Global bond yields are reaching frightening levels due to the continued war in Iran and the effective closure of the Strait of Hormuz. Continued high oil prices and the threat of reverberating inflation are causing investors to demand higher yields on government bonds.

Equities advanced in April, but hedges remain few and far between, as traditional risk mitigants like bonds and gold continue to show a correlation with stocks.

The exchange-traded fund marketplace continues to expand. Now with more than $20 trillion in assets under management ($14 trillion in the U.S., growing at an 18% five-year annualized clip), 2026’s volatility and emerging investment themes have taken the universe to new heights.

The percentage-of-assets fee is so embedded in advisory economics that most firms treat it as a fixed constant rather than a business decision. It shapes how you staff, how you plan, and how you define the relationship with clients. But the AUM model is neither as old nor as inevitable as it feels.

Vanguard research suggests that one practical answer may lie in pairing traditional target-date funds with a modest allocation to deferred-income annuities (DIAs).

Rising bond yields curbed traders’ appetite for risky bets early Friday, sending stocks lower following a weeks-long record-setting rally driven by a rush of cash into all things artificial intelligence.

Stock markets have been hitting all-time highs and credit spreads remain low, yet higher interest rates and mounting floating-rate debt are straining lower-rated borrowers. This tension is surfacing first in leveraged loans as “quiet defaults” become more common — opening up a dynamic set of opportunities for investors specialized in stressed and distressed assets.

Access to private equity, private credit, private infrastructure, and private real estate assets can potentially improve long-term investment outcomes for participants.

Rather than worrying about the narrow impact of faster IPO inclusion on index fund performance, we think investors would be better served by focusing on the long-term expected returns offered by the markets in which they’re investing – in particular the U.S. and non-U.S. equity markets.

What to do? Does one capitulate and chase the bubble at the highest valuations in history? Does one wring their hands at the prospect of a bubble that might only go higher and higher forever without end? My hope is that this month’s comment will offer both perspective and confidence that it is not necessary to chase current extremes, nor to be anxious even about the possibility of steeper ones.

As market volatility lingers, the latest S&P Persistence Scorecard reveals a sobering reality for active managers.

As equity markets transition into 2026, large cap equity portfolio managers share a surprisingly consistent framework — paired with sharp disagreements on where risk and opportunity sit. A survey of large growth, value, and blend managers reveals a market shifting away from simple narratives toward selectivity, fundamentals, and manager skill.

When it comes to investing, it’s the Wild West out there. Our clients are hearing things from less scrupulous members of the financial services industry that appear true on the surface but are really aimed at separating people from their money.

Treasury Inflation-Protected Securities, or TIPS, can help buffer a portfolio against inflation. However, it's important to understand their unique characteristics and complex nature.

Even before the first active dual share class fund from Dimensional launched, active mutual funds and ETFs were already roommates rather than existing in separate silos. Ben Johnson, head of client solutions at Morningstar, revealed in a LinkedIn post that active managers are increasingly using ETFs as essential tools for building portfolios.

Fixed-income market sentiment was dominated by geopolitical headlines, particularly the conflict in the Middle East following disruptions to the Strait of Hormuz and rising oil prices, which contributed to renewed inflation concerns.

Amid rising college costs and mounting student debt, parents are looking for more ways to lessen the financial burden of higher education. Luckily, 529 college savings plans can help. These unique savings vehicles offer several tax breaks for parents as they save for their children’s future education.

While Russ acknowledges that the ongoing conflict in the Middle East has contributed near-term volatility, he also notes that these rising tensions are occurring against the backdrop of a solid U.S. economy.

Active ETFs are no longer a niche satellite play; they are becoming central pillars of modern portfolio construction.

As transition activity increases, what was once seen as a step between portfolios is becoming part of the outcome itself. Execution is now more closely tied to how portfolios are reshaped, particularly as restructures grow larger, more frequent, and more complex.

“Diversification” has been the driving principle of investing and risk management for generations. But what does it mean to be “diversified?”