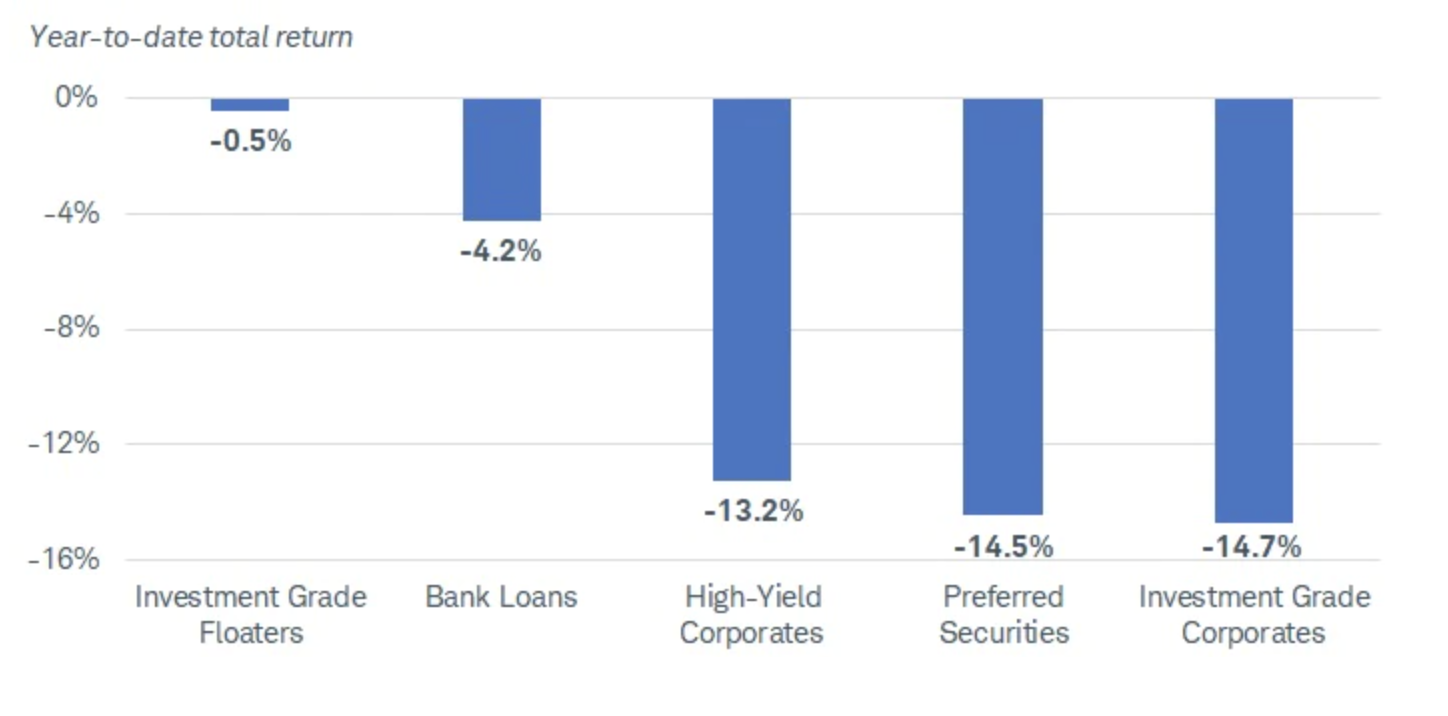

After the steep drop in prices during the first half of this year, yields on many corporate bond investments are at or near 12-year highs.

The Federal Reserve is trying to fight inflation by raising interest rates.

Our mid-March meeting’s “unenthusiastic” stance on global equities and negative stance on global bonds was a respectable decision, as was the overall macro theme “Stagflation Lite with GDP somewhat worse than consensus, but skirting recession.”

Latin America tilted further left this week as Colombian voters elected Gustavo Petro as president. Come August, the former Bogotá mayor and member of the M-19 guerrilla organization will join the region’s growing list of leftist leaders in a political shift some are likening to the “pink tide” of the late 1990s and early 2000s.

What to do in equity portfolios at the midyear point? Fundamental Equities CIO Tony DeSpirto assesses the backdrop and identifies three favored sectors.

The varied responses of individual countries to global inflationary pressures have contributed to elevated real-rate differentials between developed and emerging markets.

U.S. stocks are extending weekly gains, rebounding from yesterday afternoon's slide as the markets remain choppy amid lingering global recession concerns that have been bolstered by monetary policy tightening efforts around the globe aimed at getting high inflation under control.

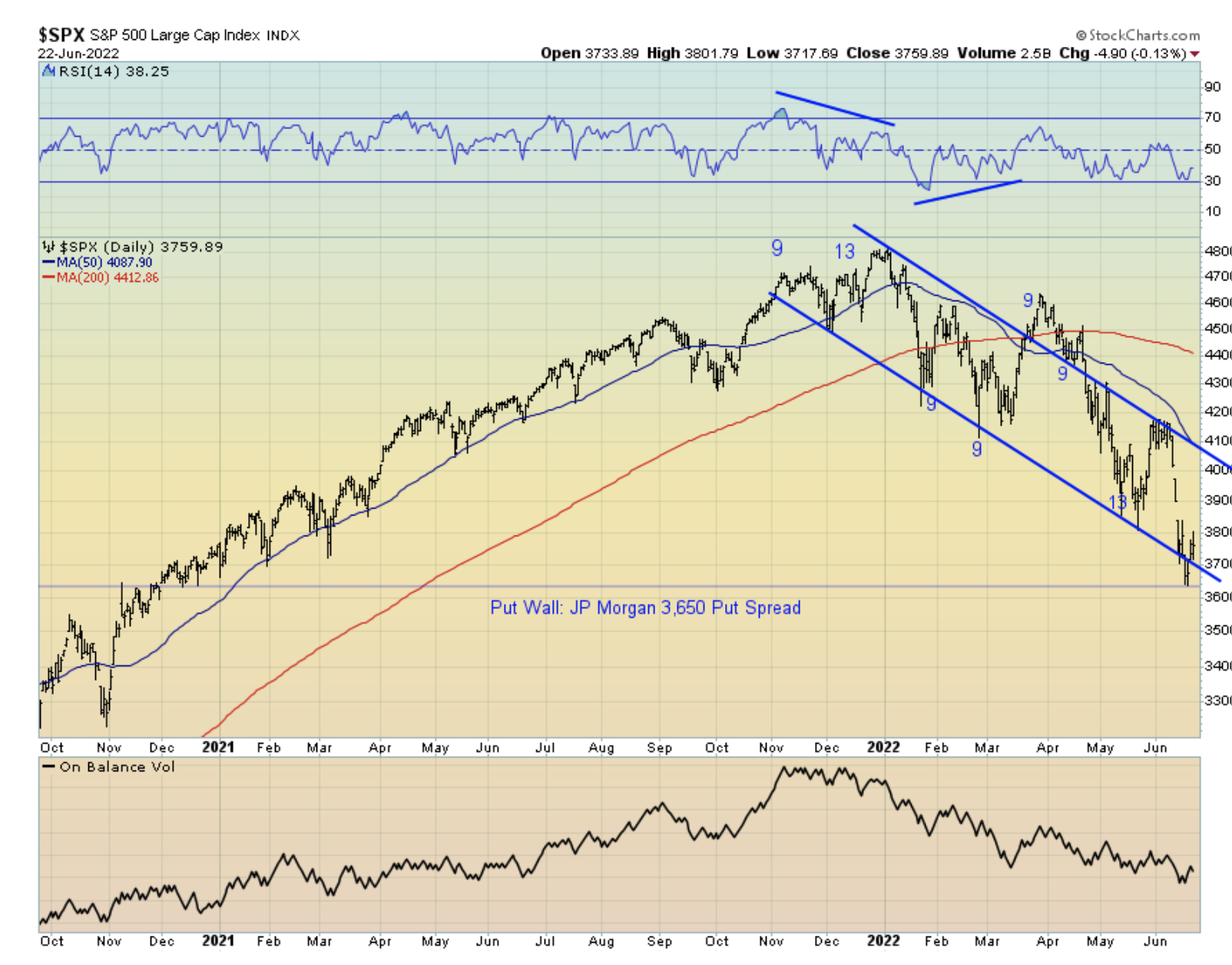

A number of key technical, sentiment and flow based indicators are suggesting we could see a relief in selling pressure over the coming weeks, and perhaps a countertrend rally in risk assets.

West Texas Intermediate crude oil futures fell below $102 a barrel Wednesday, which represents a 22% drop over the past two weeks and meeting the technical definition of a bear market.

Bonds have been whispering in the ears of stock investors all year. Now they’re starting to shout.

The yield of the U.S. high yield (HY) market, currently at 8.4%, has risen by over 420 basis points since the start of the year.

Agricultural commodities fell, offering some reprieve to rampant food inflation, as traders weigh incoming data on harvests and looming recessions in some major economies.

Given year-to-date fixed income returns, one would be forgiven if they never wanted to own the asset class again. Such a view, however, could prove costly as, for the first time in a year, areas of the market are starting to look attractive.

The yellow metal has managed to stay positive since the start of the year, skirting pressure from surging yields and a strong U.S. dollar. Meanwhile, nearly every other asset class has fallen into either correction or bear market territory.

The world’s central bankers are unleashing what may prove to be the most aggressive tightening of monetary policy since the 1980s, risking recessions and roiling financial markets as they rush to tackle the surge in inflation they didn’t see coming.

The equity-linked debt of some of the pandemic’s darlings has plunged to record lows and is now considered distressed.

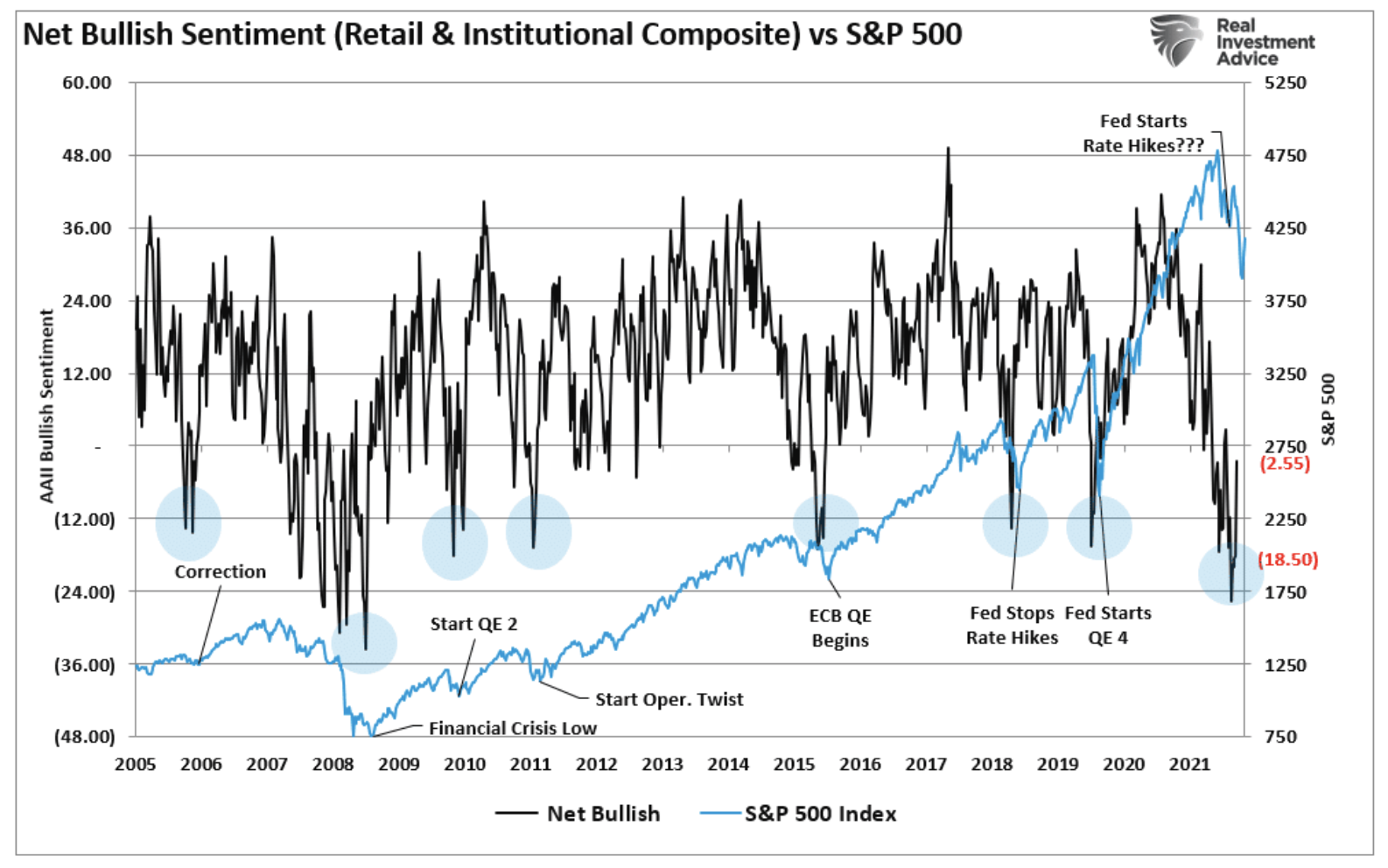

Investors are terrified.

It’s too soon to call an end to America’s worst bond-market collapse in at least half a century.

Late last year, investors who were clinging to the hope that inflation might be temporary took solace in the fact that real Treasury yields remained negative, a sign that bond investors might not be that worried about inflation.

Despite a lot of confident predictions, nobody knows what will happen at the Federal Reserve Wednesday, never mind what the impact will be on markets.

With stocks down around 20% year-to-date, it is important for investors to know what kind of bear they are dealing with.

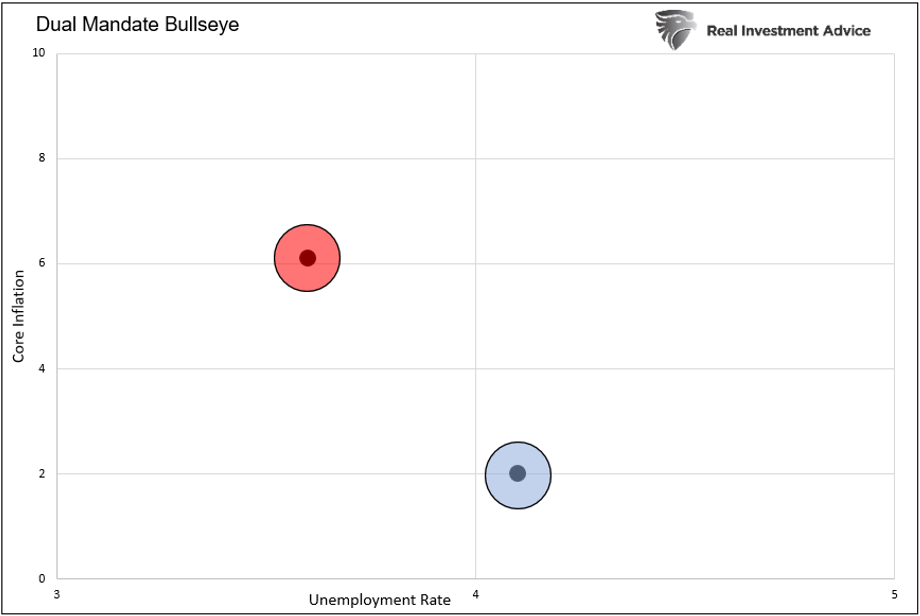

Recent experience shows that a third mandate – preventing financial instability – trumps the Fed’s two congressional mandates of full employment and low inflation.

Federal Reserve Chair Jerome Powell, who’s carefully telegraphed interest rate hikes over four years, looks likely to abandon gradualism and move more forcefully to stamp out inflation along with growing concerns that it will persist.

The world’s biggest technology stocks are crumbling on Monday as broad markets enter into bear market territory amid fears the Federal Reserve will send the US economy into recession.

Since the recession of 2008 in 2009, financial stocks in general have been trading at significantly lower valuations than normal.

With the Federal Open Markets Committee due to meet Wednesday, there was no way policy makers could guide the market on how last week’s awful inflation data for May had changed their plans.

Traders unnerved by a selloff that hit stocks and bonds alike are looking for refuge, increasing the appeal of investments offering reliable returns such as shares that pay steady dividends.

New research shows that positive returns to ESG portfolios from 2018-2020 were attributed to increased demand for “green“ stocks, raising the question of whether that outperformance will be sustained.

The hottest US inflation in four decades will push the Federal Reserve to raise interest rates more aggressively this year, and a recession may not be far behind.

Madonna was right. That iPhone on which you may be reading this article is far less important to society than the materials – like steel and plastic – that were used to build it.

US consumer prices surged to a 40-year high, defying expectations that gains would start to moderate after the Federal Reserve began tightening.

There’s no way of knowing for certain whether a recession is imminent, but for many Americans, it’s sure starting to feel that way. According to Google, more people in the U.S. searched for the term “recession” than at any other time in the past two years.

US inflation accelerated to a fresh 40-year high in May, a sign that price pressures are becoming entrenched in the economy.

Stanley Druckenmiller has a warning for Wall Street: The sharp decline in the stock market isn’t over just yet.

I bought an apartment last year and if I were buying today, I wouldn't be able to afford it.

It started with bonds. Now even collateralized debt obligations (CDOs) come in green.

Stocks modestly lower ahead of tomorrow’s inflation report.

Crude oil and energy equities have been on a tear for the last two years.

As corporate leaders increase their grim pronouncements about the future, there are still market economists who see stocks heading higher in the second half of this year and who say the US could sidestep a recession.

A wild year on Wall Street has traders fretting one of two extreme scenarios will engulf the $23 trillion Treasury market ahead: Either a fresh bond selloff thanks to red-hot inflation -- or a sustained rally on mounting recession risk that sends yields back toward historic lows.

The year 2022 sure has felt like a pretty bad one so far: interest rates and consumer prices have spiked up, and stock prices are sharply down. But, in terms of what really matters, many investors are better off than they were at the end of 2021–almost 5% better off for an investor in a diversified balanced portfolio.

The advisors who figure out how to work with Generation Z will take your wealthy Baby Boomer clients away. Stop rolling your eyes and listen to why.

The price of oil, as measured by the benchmark WTI index, could hit $150 this summer, according to Jeffrey Gundlach. That price may not be sustained, he said, “but the path of least resistance for oil prices is up.”

The ECB and the Fed both need to quickly normalize policy from the emergency settings adopted when the pandemic first hit.

Gold may be heading for another rally, with warnings over a global economic slowdown paving the way for a fresh push toward $2,000 an ounce.

U.S. equities are lower as the recent volatility continues despite yesterday's gains.

Investors are shifting their focus from runaway inflation to slowing global growth as central banks hike rates to tame price pressures.

We have a very precise methodology for dissecting the world’s equity markets.

In January Goldman Sachs projected that the FOMC would increase the federal funds rate at every other meeting (each meeting is 6 weeks apart) starting with the March meeting.

We strongly believe that the traditional benchmark-led approach to investing in emerging market debt can be far from optimal.