FOMC Inflation Test Coming

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIf Supply Issues Persist, Will the FOMC Keep Hiking?

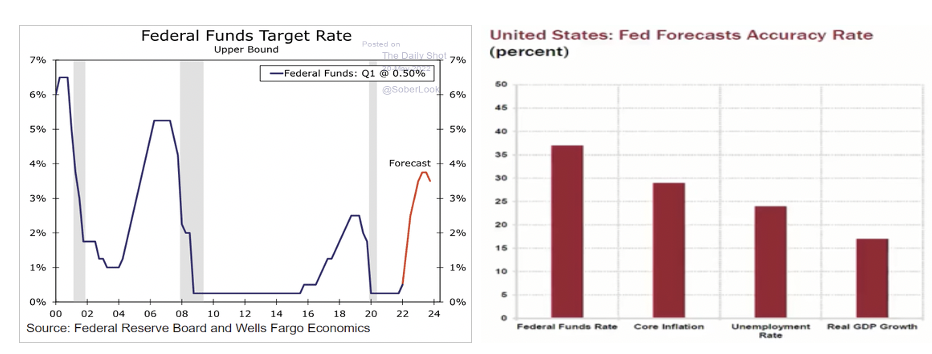

In January Goldman Sachs projected that the FOMC would increase the federal funds rate at every other meeting (each meeting is 6 weeks apart) starting with the March meeting. By February the major investment firms were leapfrogging over each other to guess how many increases there would be in 2022. Bank of America won that race by forecasting 7 increases. The new game is guessing the terminal level for the funds rate in the current hiking regime. The average guess for 2023 almost reached 4.0% before dipping to 3.75% last week. This is a silly game since there are so many variables that can’t be known that will determine the choices the FOMC makes in the next 12 months.

Another factor should humble those who participate in the terminate rate guessing game. The FOMC’s track record in forecasting the federal funds rate, Core inflation, Unemployment Rate, and Real GDP is awful, according to David Rosenberg. Forecast misses for the economic data is somewhat understandable, since they are out of the FOMC’s control. But only being 37% right about the funds rate, which the FOMC determines, is scary. This also should undermine the widespread view that the FOMC has better information than other economists and the brain power to formulate policy.

Since January the forecast pendulum has swung from the FOMC increasing the funds rate by 1.0% in 2022 to more than 3% by the end of this year. The rush to guess how high the FOMC will lift the funds rate overlooks the goals that the FOMC has clearly stated. I reviewed those goals in the May 16 Weekly Technical Review. “The FOMC has been specific about its goals, so monitoring the progress toward meeting those goals should provide some insight as to how policy may evolve in coming months.

- The FOMC wants to curb demand to reduce the imbalances between supply and demand in the economy, since it has no control over the supply side of the equation.

- The FOMC wants inflation to peak and then have confidence that the decline will persist so that the PCE can be expected to fall toward its 2.0% target in 2023 or 2024.

- The FOMC will quickly increase the funds rate to neutral to cause demand and inflation to soften by the end of 2022. If real progress is not realized, Chair Powell, Vice Chair Brainard, and other members have said the FOMC will increase the funds rate above neutral if needed to get inflation down.

- FOMC members want to avoid a recession so lower income workers aren’t disproportionately hurt. If at all possible, the FOMC wants to engineer a soft landing. This goal may exert more influence once the funds rate is at the neutral level.

The FOMC was completely wrong about inflation being transitory in 2021, but right in 2022 by speaking in one voice about their intentions to quickly lift the federal funds rate to neutral. St. Louis Federal Reserve president James Bullard did a great job of explaining what the neutral level meant in terms of monetary policy, as discussed in the May Macro Tides. “In a Financial Times interview on April 13, St. Louis Federal Reserve president James Bullard provided the conceptual framework. “There’s a bit of a fantasy, I think, in current policy in central banks. Neutral is not putting downward pressure on inflation. It’s just ceasing to put upward pressure on inflation.” Translation - Central banks must first remove the existing accommodation that is putting upward pressure on inflation.” This is why even the Doves on the FOMC agreed that the funds rate needed to rise to the neutral rate. There is no definitive level that represents the neutral rate. Chair Powell has said it’s between 2.0% and 3.0% and is 2.5% for him. The Doves would favor a lower rate, while the Hawks are closer to 3.0%.

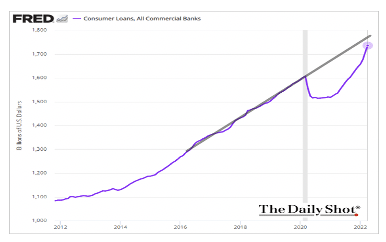

Those who are forecasting that the funds rate will top above 3.5% have not listened to Chair Powell and other FOMC members who have strongly expressed the desire to avoid a recession. Once the FOMC has increased the funds rate to near 2.0% - 2.5%, the emphasis will shift from getting to neutral to anticipating how the economy will absorb the rate increases in coming months. Many consumer loans are tied to the Prime Rate, as are loans to small and medium sized businesses. The Prime Rate is tied to the federal funds rate so the cost of these loans will increase as the FOMC increases the funds rate. The Prime Rate is up 0.75% since mid March, and is expected to increase another 1.0% after the FOMC raises the funds rate by 0.50% at the June and July meetings. The economic drag from the 1.75% increase in the Prime Rate will intensify in the second half of 2022 and in early 2023, since changes in monetary policy take 6 to 12 months to take hold. If the FOMC raises the funds rate by 0.5% at the June and July meeting, it will be at 1.75% - 2.0% and in the zip code of neutral.

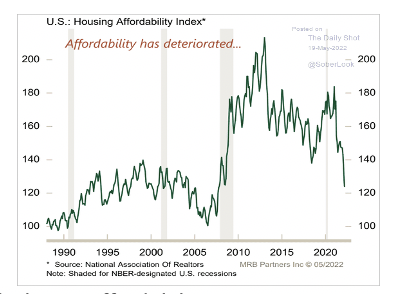

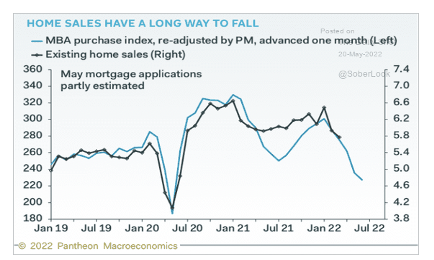

The housing market has weakened and will soften more in coming months. This was discussed in the April Macro Tides. “Since the end of 2021 the 30-year mortgage rate has soared from 3.25% to almost 5.0%. In the last year the median monthly mortgage payment on a median priced home has jumped from $1,572 to $2,183. The S&P 500 Core Logic Case-Shiller National Home Price Index rose 19.2% from January 2021 following an increase of 10.4% in 2020. Since December 2019 the Home Price Index is up 32.7%. Soaring home prices are making affordability worse. According to Bank of America the combination of higher home prices and mortgage rates will lower affordability 25% from March 2021 a record decline. Existing home sales follow changes in affordability by 6 months, so existing homes sales will drop more in coming months. In February Existing Home sales were 6.02 million, down -7.2% from January’s 6.49 million. If the past is any guide the sharp decline in affordability suggests Existing Home sales could approach 5.0 million before the end of 2022. New Home sales are also going to take a hit. In February new home sales and were 772,000 which was -2.0% under January’s total and -6.2% below February 2021. Total spending on housing represents almost 12% of GDP, so a pronounced decline in housing activity will ripple through the overall economy.”

In April Existing Home sales were 5.61 million, off -2.4% from March and down -5.9% from April 2021. The tally for April’s Existing Homes sales reflect contracts that were signed in February and March when mortgage rates were 3.66% in February and 4.78% in March. Mortgage rates were higher in May so the weakness will persist in coming months. Inventories in April were 1.03 million and 14% lower than in April 2021. The lack of homes for sale helped push the median sales price to $391,200 and up 14.8% from a year ago. The conditions that caused affordability to plunge have only gotten worse. New home sales fell -16.6% in April to 591,000 and were -26.9% lower than in April 2021.

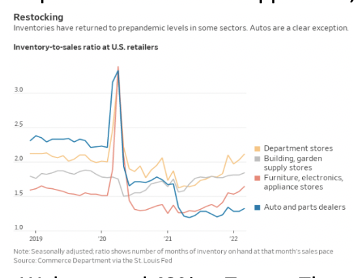

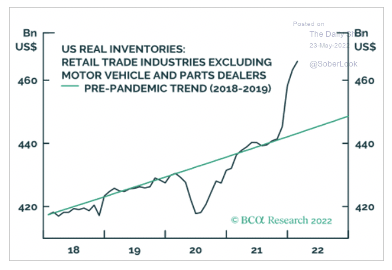

The decline in Existing and New Home sales has a direct impact on the sale of appliances, furniture, and every other home furnishing. The weak first quarter results for Walmart and Target confirm that this is happening. Walmart’s Q1 earnings fell -23.7% ($.97 versus $.74 per share), and Target’s crashed -48.2%. The primary reason for the big misses wasn’t a plunge in demand (Target and Walmart’s revenues were up 3%), but rising transportation costs (diesel fuel), higher wages, and stocking their shelves with large ticket stuff consumers weren’t interested in buying (furniture, major appliances). In the first quarter inventories were up +32% for Walmart and 43% at Target. There is a silver lining. In coming months Walmart and Target will likely mark down prices for appliances, furniture, and other furnishings to get their inventory under control. As this unfolds, the markdowns will show up in the CPI, even though these categories have a small weighting. The shift toward lower inflation will begin with more categories showing small price declines.

This subtle change will become more important in coming months, since inflation has broadened out to include a large majority of categories within the CPI. In April 76% of the categories in the CPI were up more than 4.0%, which illustrates how huge increases in energy, wages, and raw materials over many months infects almost everything. It will take time for this to unwind, as energy and wages are at best only likely to plateau as the rate of change slows.

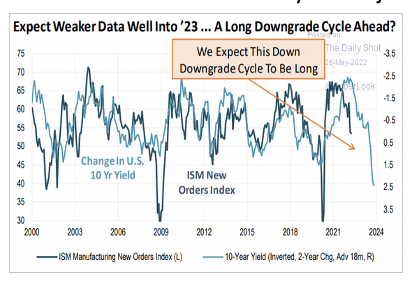

The first thing Walmart, Target, and any other retailer that finds their inventory of major appliances, furniture, TVs, and home furnishings in general will do will be to cut orders for these categories. This will lead to a decline in New Orders within the monthly ISM report, which will weigh on the overall index as production is reduced. It is likely that the New Orders Index in coming months will drop below 50 signaling a contraction. The two year Rate of Change (ROC) in the 10-year Treasury yield foreshadows changes in New Orders when the ROC is advanced 18 months. If the historical correlation holds, the New Order Index will drop below 50. Manufacturing comprises less than 15% of GDP, but a slowdown in this sector will show the FOMC that progress is being made toward slowing aggregate demand. Services comprise more than 80% of GDP and price pressures are likely to continue as consumers spend more on services. The FOMC will need to become convinced that pricing pressures in services have at least peaked. This will take longer to develop than a fall in goods prices.

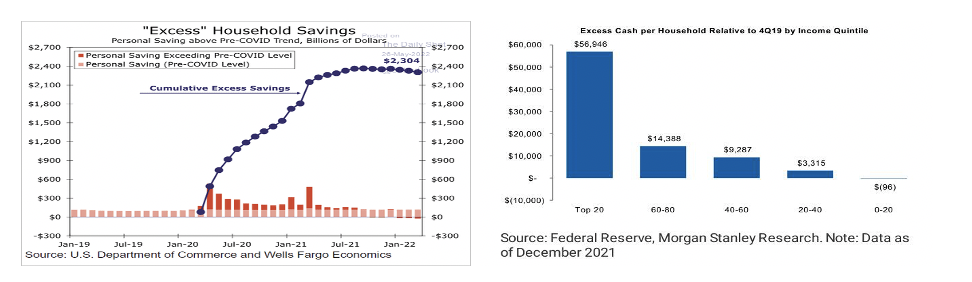

Walmart, Target, and other retailers have noted that consumers are not only shifting their buying from goods to services, but are buying less of premium brands in favor of store brands. Importantly, consumers are becoming resistant to price increases. This transition was anticipated and discussed in the April Macro Tides. “Consumers came out of the Pandemic with roughly $2.3 trillion in excess savings and a desire to get back to some semblance of normal as COVID retreated. Consumers had the wherewithal and were willing to knowingly pay more pay for the goods and experiences they wanted. The assumption investors are making is that this positive dynamic of pricing power won’t change, even as inflation remains high and erodes the purchasing power of wages. There is a good chance that inflation fatigue will set in for more consumers as they run down their Pandemic savings, and mentally and emotionally simply get tired of paying more for everything they buy. For companies that have been able to pass along cost increases, inflation fatigue will become resistance to additional price increases.”

In the fourth quarter, operating expenses at 442 nonfinancial companies in the S&P 500 rose 23% to a total $2.75 trillion. On average these firms spent 83.5% of their total revenue on expenses, according to S&P Global Market Intelligence. In the first quarter energy prices, transportation and raw material costs went up, as did labor costs. The pressure to cut costs has intensified and firms are beginning to act. Gartner surveyed 180 companies with annual revenue ranging from $500 million to $100 billion and found that 20% of them are planning to cut costs through July. The initial effort is focused on potential savings from marketing, sales, and real estate. Cutting deeper isn’t on the table or necessary, since revenue growth is decent.

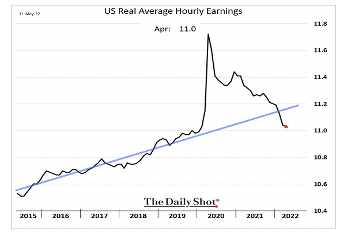

The cost of living has been rising faster than the healthy increase in wages, so the ‘real’ after inflation level of wages has fallen below the growth trend since 2015. In aggregate consumers are sitting on $2.3 trillion in savings that were accumulated after Congress provided extended Unemployment benefits and distributions of $1,200 and $1,400 to every taxpayer, even if they were gainfully employed. The extended lockdowns precluded most consumers from spending which added to their savings. The aggregate pool of savings is not evenly distributed. The bottom 20% and 40% of wage earners have far less in savings than the other income brackets. As discussed in the April and May Macro Tides, “The bottom 20% of wage earners spend almost 75% of their income on shelter, food, and energy, while a middle class family spends more than 50%.”

An indication that the bottom 40% of wage earners are being squeezed by inflation can be seen in the sharp increase in credit card debt. Since January the amount of credit card debt has jumped from $1.05 trillion to $1.097 trillion at the end of March. After paying down credit card balances during the Pandemic consumers have been aggressively adding to their balances. This suggests that a portion of consumers have run down their savings to a point that they are now using their credit cards to maintain spending.

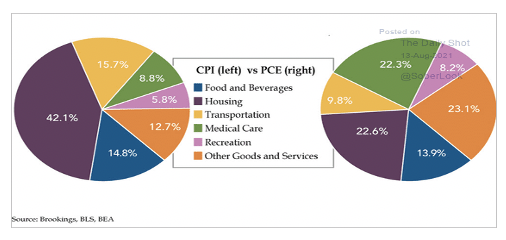

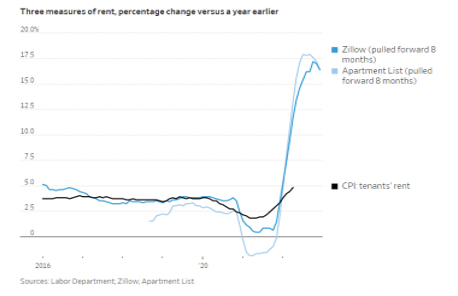

Owner’s Equivalent Rent (OER) comprises 32.9% of the CPI with Rents adding another 7.4% (40.3%), as of December 2021. (The graphic shows a combined total of 42.1% for OER and Rent prior to updated changes to the CPI.) Rents having soared during the last year rising by more than 15%, according to data provided by Zillow and Apartment List. For lower income families, shelter is a bigger expense than food and energy, and the size of the increase as their lease expires has to be a shock.

The gouge higher shelter costs are taking out of their income has undoubtedly led more people to use their credit cards on other living expenses. The increase in the cost of shelter is underreported in the CPI, which uses Owner’s Equivalent Rent (OER) to infer the cost of shelter. In April Owner’s Equivalent Rent was up 4.78% from the prior year, but home prices were up 14.8% and rents even more. The gap between the increase in home prices and rents is more than 10%, which would add more than 3% to the CPI if OER matched what is happening in the real world, i.e. the CPI would have been above 10% in March and April. While the CPI and PCE won’t be changed anytime soon, the economic impact of higher shelter costs are forcing many families in the bottom 40% of wage earners to make hard choices so they can pay their monthly rent.

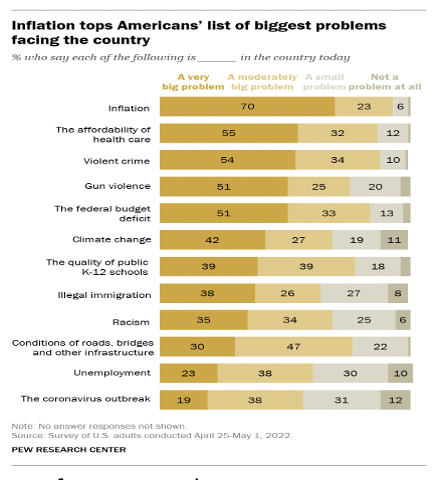

Concern and anxiety about inflation isn’t just limited to the bottom 40% of wage earners. According to a survey by Pew Research taken between April 25 and May 1, 70% of those surveyed think inflation is a very big problem or a moderately big problem 23%. Inflation isn’t the only pressing issue as 87% are worried about the affordability of health care, violent crime (88%) gun violence 76% was the top concern. Amazingly, only 57% of respondents are worried about COVID, even though COVID hasn’t disappeared. The top 4 concerns are issues that affect people in their everyday life and the quality of their life now. Issues like the federal budget deficit, climate change, and immigration have been put on the back burner. With the labor market so strong, unemployment is not much of a worry for most people.

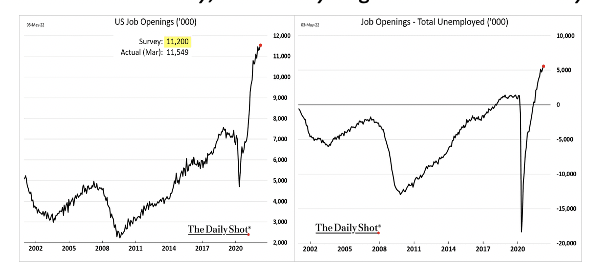

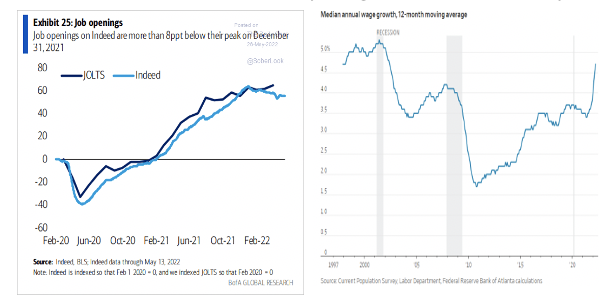

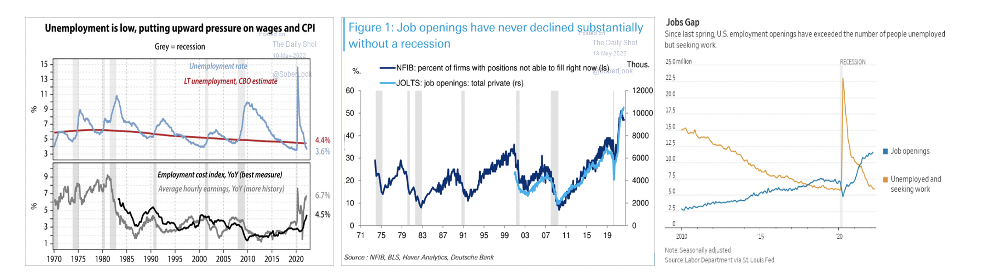

Chair Powell has described the job market as “extremely, historically” tight and “unsustainably hot”, and has referenced the ratio of job openings to the number of unemployed on a number of occasions. In March the ratio was 1.9 so there were 1.9 openings for every person unemployed, the highest ratio ever. The ratio of job openings to unemployed will fall in coming months. In the last two months a number of companies that feasted during the lockdowns have announced layoffs and the need to hire additional workers will ease as the economy downshifts.

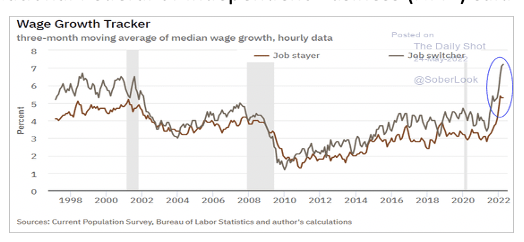

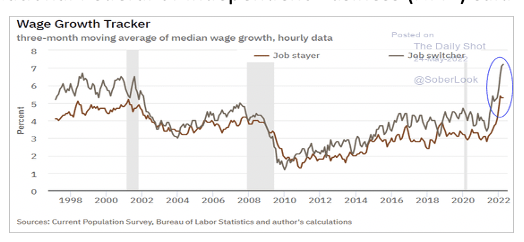

The job search firm Indeed also tracks the number of job openings and openings have already started to fall. The correlation between the BLS and Indeed survey is tight so the BLS survey will start to fall soon. Wage growth has soared as companies were forced to pay their employees more to prevent them from switching jobs and making more money. With inflation running so hot and faster than the growth in wages, employees will still have the leverage to ask for larger increases. This leverage will fade but it will take time, so in the next six months wage increases will continue, but the magnitude of the increase will decelerate from the torrid pace of the last year.

Stock Market

The stock market rallied smartly in the last week of May from a low of 3875 on May 24 to 4161 on May 31. In a Special Weekly Technical Review Update on May 20, I discussed why a strong rally was expected during the week of May 23. “The S&P 500, QQQ, and DJIA have a similar pattern, even though they fell below their May 12 low. The Russell 2000 didn’t drop below its May 12 low, which created a positive inter market divergence. Each of these averages rallied off the May 12 low in 3 waves, and then declined to a new low on May 20 in 3 waves. This suggests the S&P 500 could rally to 4090 next week in what would be wave c of the counter trend bounce from May 12. If the market gaps higher on the opening on May 23, wait for a pullback to buy.” From a high of 3982 on May 23, the S&P 500 pulled back to 3875 on May 24. In the May 23 Weekly Technical Review I noted that “The S&P 500 is expected to rally to 4091 or a bit higher”, so the rally was not a surprise.

Federal Reserve

The stock market was propelled higher on the notion that the FOMC would either hit the pause button on additional rate increases, or downshift from increases of 0.50% to 0.25% at the September meeting. The FOMC won’t hit the pause button on rate increases, but a downshift in the magnitude of increases is likely to be on the table, as discussed in the May 16 Weekly Technical Review.

“The funds rate will be up to 1.75% - 2.0% and in the zip code of neutral, if the FOMC increases the funds rate by 0.50% at the June and July meetings. After the meeting in July, Chair Powell won’t publically state that the FOMC might downshift to a 0.25% increase at the September 21 meeting. He may be able to note the progress that has been made on inflation (trending down), demand, (weakening), and acknowledge that the funds rate is nearing its neutral level.

The more dovish Fed governors and district presidents are likely to give speeches that mention the improvement in inflation and the improvement in the balance between supply and demand leading up to the September meeting. If this occurs, the financial markets will be happy to front run the FOMC, and a potential deceleration in the size of rate increases, by responding before the September 21 meeting. A downshift to 0.25% at the September and the November 2 meeting would leave the funds rate at 2.25% - 2.50% and at the neutral meeting.”

(On May 24 the Atlanta Federal Reserve President Raphael Bostic gave a speech and said he would be open to considering a change. This is discussed in the FOMC section below. His comments were seen as definitive and helped the S&P 500 move higher after the PCE report.)

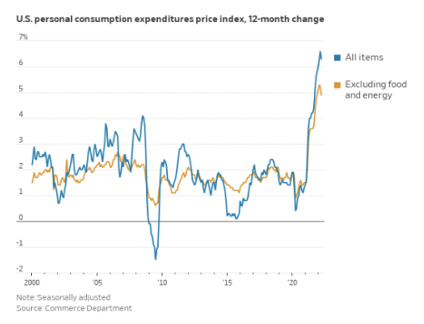

On May 27 the FOMC’s favorite inflation measure – the Personal Consumption Expenditures Index (PCE) – fell from 6.6% in March to 6.3% in April and the Core PCE dipped from 5.2% to 4.9%. In response the S&P 500 rallied 2.5% as traders concluded that this data point sealed the deal, even though the FOMC’s Core PCE inflation target is 2.0%. The reality is the FOMC doesn’t know whether a downshift will be appropriate in September, until future data confirms that inflation will continue to trend lower and aggregate demand slows. My expectation has been that inflation would peak in March or April (it did) and that the economy would slow (it is). The test for the FOMC is whether incoming data allows them to downshift without losing credibility, after being so wrong in 2021.

The extreme tightness in the labor market suggests any improvement in the short term won’t be enough to restore a balance between demand for workers and the available supply. The Congressional Budget Office estimates that the long term equilibrium for the unemployment rate is 4.2%. As long as the unemployment is below 4.2%, there will be upward pressure on wages. The unemployment rate would have to increase to 4.2% or higher to create more slack in the labor market and reestablish equilibrium.

More than 50% of small businesses in the National Federal of Independent Business (NFIB) said they weren’t able to find enough workers in April. This mismatch won’t be solved quickly. The spread between job openings and the number of unemployed workers has never been so wide. In the aftermath of the Financial Crisis wage gains were modest until 2018, when job openings exceeded the number of people out of work. The number of job openings is going to fall in coming months, and the novices in the stock will conclude that the problem of labor market tightness has been solved. A solution for labor market tightness won’t be realized until the unemployment rate is much closer to 4.2% and the number of job openings falls to 7.5 million. The labor market balance is a structural problem and won’t be restored for a long time, or more quickly, if the unemployment rate jumps by 0.6%. According to the Sahm rule an increase of 0.5% in the 3 month moving average in the unemployment rate has only occurred in a recession. In the short run detailed analysis won’t matter to retail day traders.

May Consumer Price Index

The computer chip shortage has depressed the production of new cars and car rental firms have gobbled up a disproportionate share of available used cars. With travel increasing to pre Pandemic levels, the shortage of used cars will persist as car rental companies buy more used cars to increase their rental inventory. The summer holiday travel season is just beginning and already there are reports of customers reporting they had paid for a rental car, but after arriving at their destination learning there were no cars to rent. In the near term car rental firms are missing out on potential revenue, so are likely to increase their purchasers of used cars. Used car prices will come down in coming months, but not as much if the demand for car rentals was less. The lead time for the majority of computer chips is still increasing, so no relief can realistically be expected before the first half of 2023. This will keep new vehicle production below demand, so New Car Prices aren’t likely to fall much. The only measurable relief will come from Reverse Base Effects, which will subtract from the monthly CPI in the next few months.

Since peaking in December, the Mannheim Used Car Index is down -3.8%. The data for Used Car prices in the CPI doesn’t track the Mannheim Index perfectly, but it is a good proxy. Used Car prices comprise 4.0% of the CPI. If Used Car prices fall -1.5% in May to 204.00 (my guess), the annual increase would drop from 22.73% in April to 13.63% in May. In April Used Car prices added 0.91% to the CPI and are estimated to add 0.54% in May. This will subtract about -0.37% from the May headline and Core CPI.

There are other categories that aren’t likely to add as much to the May CPI as they did in April. New Car prices were up 13.2% from April 2021, which was the largest annual increase since 1949. The change in New Car prices for May will only subtract a few basis points.

Air fares were up 18.6% in April, the largest one-month increase since 1963. The cost of staying in a hotel or motel rose 2.0% in April and was up 22.6% from the prior year. With the travel season ramping up, the cost of air fares and lodging away from home won’t decline, but the monthly and annual increases will moderate. These categories should also subtract from the May CPI by a small amount.

Energy comprises 8.29% of the CPI. The increase in energy costs in May will offset a large portion of the declines from Used and New Cars, Air Fares, and lodging away from home in the May CPI. In April gas prices were down (April +44.02% vs. 48.16% March), so they subtracted from the April CPI. According to Gas Buddy, a gallon of gas has soared more than 11.0% in May, and is up about 48.0% from a year ago. Crude oil is up 11.6% in May, and up more than 70% over the last year. Combined the increase in energy could add up to 0.80% to the May headline CPI.

This suggests the headline CPI won’t drop by much, and might even tick higher, when the May CPI is reported on June 10. The net change may depend on what many of the smaller categories do. The Core CPI will likely fall since energy and energy is excluded, but the shelter component will increase as will the prices for select services.

FOMC

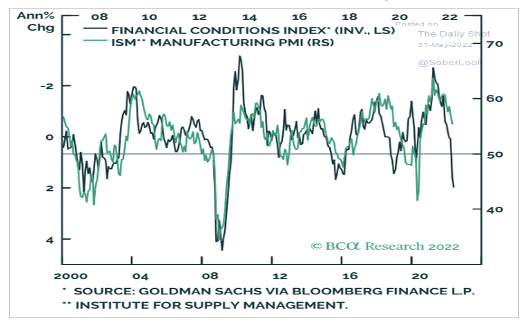

Changes in Financial Conditions are a key determinant in guiding monetary policy. The FOMC decided in March that financial conditions were too accommodative, which is why the FOMC is determined to increase the federal funds rate to its neutral rate. At the same time, the FOMC is not oblivious to a sharp decline in financial conditions. Since March financial conditions have tightened significantly. The Dollar has rallied to its highest level in more than a decade, and Treasury yields spiked with the 10-year Treasury yield rising from 1.70% in early March to 3.17% in early May. Credit spreads have widened as corporate high yield and junk bonds fell even more than Treasury bond prices. The S&P 500 was down almost -20%, while the average stock was off by almost -30.0%. If financial conditions tighten too much too quickly, the risk of a financial dislocation increases, which is something the FOMC doesn’t want to happen.

On May 24 the president of the Atlanta Fed Raphael Bostic gave a speech to the Rotary Club of Atlanta, and offered a hint that he might favor a pause in raising the funds rate by 0.50% at the September meeting. “After we get through the summer and we think about where we are in terms of policy, I think a lot of it will depend on the on-the-ground dynamics that we are starting to see. My motto is observe and adapt. I do want to make it clear that nothing is off the table. As we go through the months, we will see how it plays out. I’m at 50 basis points as long as the economy proceeds as I think it’s going to. If inflation starts moving in a different direction than it is right now, I’d have to be open to us moving more aggressively.” After his speech he commented to reporters, “I have got a baseline view where for me I think a pause in September might make sense.” The press headline focused on his comment to reporters, and not his broader view. It should be noted that Bostic is not a voting member in 2022 or 2023, so he can only sway others with his view.

In response to Bostic’s comment and the lower PCE report, credit spreads narrowed aggressively, Treasury yields fell, the Dollar weakened, and the stock market jumped. As a result, financial conditions eased. Ironically, an improvement in financial conditions allows the FOMC to pursue the path they have outlined.

The FOMC doesn’t want financial conditions to tighten too much, but they don’t’ want markets to lock them into a preset course either. They are more likely to say that they are data dependent and will make up their mind at each meeting, rather the deciding ahead of time. Basically, casting some doubt about downshifting at the September meeting, without ruling it out. Since every meeting is a ‘live’ meeting, an assessment of policy is will be on the table at the June, July, September, and November meeting.

In the FOMC’s world of Forward Guidance, it is always instructive to follow the interplay of when comments are made and by whom. On May 24 Raphael Bostic says he is open to consider a change in September, and on May 31 in Germany Federal Reserve Governor Christopher Waller pushes back aggressively. “In particular, I am not taking 50 basis-point hikes off the table until I see inflation coming down closer to our 2 percent target. And, by the end of this year, I support having the policy rate at a level above neutral so that it is reducing demand for products and labor, bringing it more in line with supply and thus helping rein in inflation.” Waller is a Governor and votes at every meeting, while Bostic has no vote in 2022 or 2023. As a Governor, Waller is more likely in agreement with Powell, so his views should be weighed more.

The May CPI will be released on June 10 and during the blackout period prior to the June 15 FOMC meeting, so there will be no public comments by members of the FOMC. If the CPI is a negative surprise, higher than estimated or actually higher than April, it might dampen expectations that the FOMC will moderate policy at the September meeting.

The FOMC lost a lot of credibility in 2021 after being wildly off about inflation being transitory. Any move to slowing the pace of rate hikes will have to be supported by data that confirms that inflation has peaked and trend lower and that demand is softening. These are the primary goals that the FOMC has established, and as Powell and others have stated, “We will go until we feel like we are at a place where we can say, ‘Yes, financial conditions are at an appropriate place. We see inflation coming down. We will go to that point, and there will not be any hesitation about that. This is not a time for tremendously nuanced readings of inflation. We need to see inflation coming down in a convincing way. Until we do, we’ll keep going.”

Forces outside the FOMC’s control have conspired to make inflation worse. One key to the decision at the September meeting and beyond will be the visibility for the Wild Cards that could assist in moderating inflation.

Wild Cards

Energy has been a big factor in driving inflation higher prior to Russia’s invasion of Ukraine. The Ukraine War further lifted oil and natural gas prices, more so in Europe than in the US. Yes, Putin’s War has contributed to US inflation, but President Biden’s response has been clearly underwhelming. When Joe Biden was campaigning in March 2020, he laid out his energy policy at a CNN Town Hall meeting. “Number one, no more subsidies for the fossil fuel industry, no more drilling on federal lands, no more drilling, including offshore, no ability for the oil industry to continue to drill, period, ends.” This tirade was directed at fellow democrats who consider climate change to be the number 1 concern the world faces. (Pew Research shows this is the number 1 concern for Democrats.) President Biden’s choices since taking office reflect this view. Releasing oil from the Strategic Petroleum Reserve (SPR) was acceptable, since it was oil that had already been drilled for and collected. In mid April President Biden announced that gas stations would be able to sell gas that has ahigher ethanol content. Here’s the announcement. “The Environmental Protection Agency will allow a gas blend with a higher ethanol content to be sold between June 1 and Sept. 15. The blend is currently available at 2,300 gas stations nationwide, but normally not sold during the summer because of environmental concerns.” Impressive, huh? There are more than 145,000 gas stations in the US, so this grade of gas won’t be available in 98.4% of gas stations. People will use more gas trying to find one of these gas stations, so the reduction in demand will be miniscule.

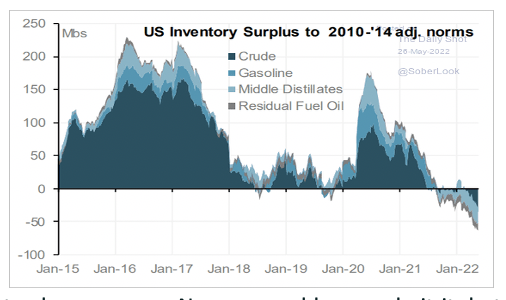

President Biden has done nothing to increase the supply of oil and natural gas in coming years, so global supply won’t be augmented from US production. This is a big deal since the inventory of oil and related products is the lowest it’s been in a long time. The net result is that the US consumers will have to tolerate higher energy costs potentially for years. The burden of higher energy costs is far heavier on lower income families, but according to President Biden that is a sacrifice they must be willing to make in the fight against the existential threat climate change poses. No one would ever admit it, but climate change zealots are not unhappy with the increase in the cost of fossil fuels. In their view it will hasten the shift away fossil fuels toward renewable energy sources. The lack of future supply from the US will prevent the US from helping Europe stop buying oil and gas from Russia in the future, and keep global energy prices high for years. The energy leverage Russia has over Europe is an existential threat right now.

Rather than encouraging US oil and gas companies to invest more to increase US production, the Biden administration asked Venezuela which produces so little oil (1.3 million barrels) it couldn’t make a difference, increased nuclear discussions with Iran (that could destabilize the middle east ) so it could pump more oil, and reached out to Saudi Arabia, which could increase production. The climate zealots in the Biden administration believe it’s OK to ask any country to increase their fossil fuel production, since the optics of asking US producers would incite a real insurrection within the Democratic Party. And maybe, God forbid, produce fewer votes in the mid-term election.

During the presidential campaign, candidate Biden vowed to treat Saudi Arabia as a pariah state and promised to hold the Saudi government accountable for alleged human rights abuses. President Biden was willing to talk to Venezuela, which is run by a dictator, but alienated Saudi Arabia which is exerts a huge influence on global oil prices and is a long standing friend of the US. When the Biden administration asked Saudi Arabia to increase production, the response was an emphatic no punctuated with this comment by Prince Bin Salman. “Simply, I do not care.” Prince Bin Salman refused to even take a phone call from President in mid February. The relationship between the US and Saudi Arabia has never been this fractured, according to most Middle East experts. This is in sharp contrast with President Trump who strengthened the ties between the countries. It’s OK to dislike Trump, but it would be nice to have more oil from Saudi Arabia.

A few weeks ago the Biden Administration sent the Director of the CIA to Saudi Arabia to mend fences. Although there was no formal announcement as to what was discussed (Ukraine War, Iran, and oil would be good guesses), the Administration called the talks ‘productive’.

Saudi Arabia will act in its best interests. The slowing in the global economy, and especially in Europe due to high energy costs, could hurt demand enough to prompt an increase in oil production by Saudi Arabia. OPEC has a meeting on June 4, but no one expects an increase from Saudi Arabia or other members of OPEC. All members of OPEC are raking in a ton of revenue with prices so high, so there is no incentive for them to act now. Weaker global growth may lead to a decline in oil prices that may pressure them to act. But that’s probably a bit down the road. That said, if Saudi Arabia increased production by even a small amount, it would have an inordinate psychological impact in the financial markets. Crude oil prices would fall by $25.00 or more virtually overnight, and lower the risk of a recession in the US.

China COVID Lockdown

President Xi of China has insisted on extreme zero-tolerance lock downs to crush COVID. President Xi wants to prove to the people of China that the Chinese approach has been superior to anything the West has done in dealing with COVID. The vaccines China developed are clearly inferior to those used in the West, but they will never be used in China. There has been some success in knocking down COVID in China, but the lock downs are also succeeding in hammering the Chinese economy. Not a single car was sold in Shanghai (25 million people) in all of April, according to the Shanghai Automobile Sales Association. The latest official data showed retail sales in April down -11.1% from a year earlier, while industrial production tumbled -2.9%.

On May 19, Premier Li Keqiang spoke to a group of senior representatives for American, European and Asian multinationals operating in China. Mr. Li said China is “committed to striking a balance, between getting the economy going and containing repeated Covid-19 outbreaks.” More importantly, Mr. Li didn’t defend President Xi’s zero-Covid strategy. This represented a departure from recent meetings that foreign executives have had with senior Chinese officials, including some involved in trade and commerce. It is highly unusual for a top official in the Chinese government not to echo statements by President Xi, and suggests that there is enough broad dissent with the zero tolerance approach for Premier Li Keqiang to express a division.

It’s not a question of if China will curtail or eliminate its zero tolerance approach, but when. It is likely that the People Bank of China will coordinate any COVD policy change by lowering interest more aggressively than the timid cuts in the past month. The outlook for improvement in global supply chains would increase significantly, even if the actual improvement took 3 to 6 months. This would have an outsized impact on financial markets, especially equities. The FOMC would certainly welcome the end of supply chain bottlenecks, as it would lower inflationary pressures without having to go past the neutral rate.

Ukraine War

The Ukraine War is likely to continue through the end of 2022 and possibly for years. Global food prices have climbed to a record high, and Russia can now control how grain grown in Ukraine is exported to a hungry world. Much like energy is a leverage point on Europe, food is Russia’s leverage on the many countries that rely on exports from Ukraine. The Ukraine War is an existential threat beyond energy as millions of people will die in 2023 as famine takes hold in many developing nations.

Here Comes the Taper!

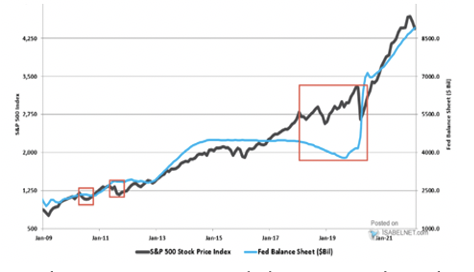

It is important to remember that the Fed’s balance sheet will be tapered starting in June. The process of tapering reduces in liquidity in the financial system and represents a more direct form of tightening financial conditions. This was discussed in the April Macro Tides. “The stock market has benefitted during periods of an expanding balance sheet and struggled when the FOMC reduced its sized in 2018. This can’t be viewed in a vacuum. Prior to 2018 the economy and earnings grew as the S&P 500 rose, and the FOMC was also increasing the funds rate in 2018 as they tapered the balance sheet. That clarification aside, liquidity in the financial system increases when the Fed’s balance sheet is growing and decreases when the FOMC doesn’t use the proceeds from maturing bonds to buy new bonds.” The FOMC plans to taper the Fed’s balance more aggressively in 2021 and 2022 than in 2018, so the financial markets will be facing a new headwind in coming months.

Treasury Yields

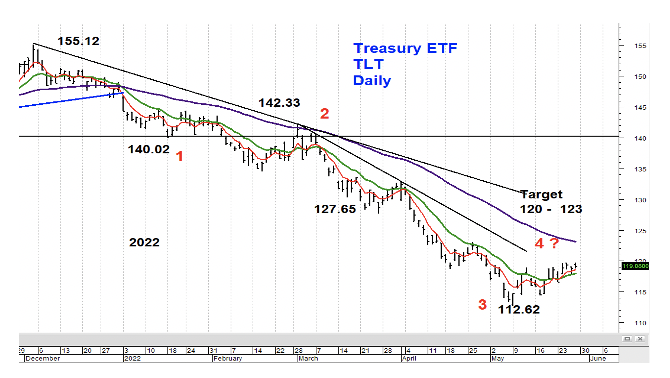

In the May 9 Weekly Technical Review I discussed the technical signs pointing to a coming decline in Treasury yields. “The 10-year Treasury yield pushed up to 3.167% on May 9 and recorded its third RSI non confirmation. In order to confirm a short term high in the 10-year Treasury yield, the 5 day MA (red) needs to cross below the green 13 day MA. This is likely to develop as more reports show the economy is slowing and may begin after the CPI report on May 11. The low for TLT in October 2018 was near $112.00 and on May 9 TLT traded down to $112.62. The $112.00 area should provide TLT important support and provide the basis for a rally as Treasury yields retreat from their yield resistance. TLT has the potential to rally to $121.00 - $123.00 if yields retreat in coming weeks.” TLT bottomed at $112.62 and subsequently rallied to $119.74 on May 27.

As discussed in the May 16 WTR, TLT was likely approaching a crossroad. “The decline from 155.12 appears to be incomplete with only 3 waves down. This suggests a bounce to 121.00 – 123.00 may be wave 4. If correct, TLT has the potential to decline below 112.00 to complete 5 waves down from 155.12.”

The rally from $112.62 to $119.74 may be wave a of Wave 4. TLT dropped from $119.74 on May 27 to $115.93 on May 31, which may be wave b of Wave 4. The 61.8% retracement of the rally would target $115.34, and this level must hold if TLT is going to rally in wave c of Wave 4 above $119.74. If TLT falls below $115.34, it is likely beginning Wave 5 to below $112.62.

Stocks

The S&P 500 was expected to rally above 4092 and potentially into the heavy resistance between 4150 and 4200. The S&P 500 reached 4158 on May 27, before pulling back to 4105 on May 31. The S&P 500 may dip below 4105 to complete wave 4 off the low at 3810, before rallying above 4200 in wave 5.

If the S&P 500 rallies above 4200 as expected, the top may form in the first few days of June as discussed in the May 23 WTR. “The red arrows highlight the proclivity of the S&P 500 to top in the first few days of each month, since the all time high on January 4. (February 4, March 2, April 5, May 4) This suggests this rally could extend into the first few days of June.”

If the S&P 500 completes 5 waves up from 3810, it will be at a fork in the road. The bullish view is that this 5 wave rally would be Wave 1 of a much bigger rally that will carry the S&P 500 potentially to a new all time high. The bearish view is that this 5 wave rally is wave C of an A-B-C rebound from 3859, and be followed by a decline below 3810 before a more significant low is formed. Market action will dictate which path the S&P 500 is taking.

In the May 23 WTR I suggested buying on May 24 in anticipation of a rally. The expected pull back brought the S&P 500 down to 3875. Taking profits on a portion of this trade is advised if the S&P 500 trades above 4200. If a corrective pullback (a-b-c) develops after trading above 4200, a wave 2 pull back will correct up to 50% of the rally from 3810 to whatever high is made for wave 5. For instance, if the S&P 500 tops at 4210, the pull back could be 150 to 200 points.

However, if the S&P 500 pulls back in a 5 wave decline, the odds of a deeper correction or drop below 3810 would increase. There is no way of knowing ahead of time whether the coming pull back (after the S&P 500 trades above 4200) will be an a-b-c corrective decline, or a 5 wave decline. This is why taking some profits above 4200 makes sense.

I will do my best to provide a real time update to identify which path is likely.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All