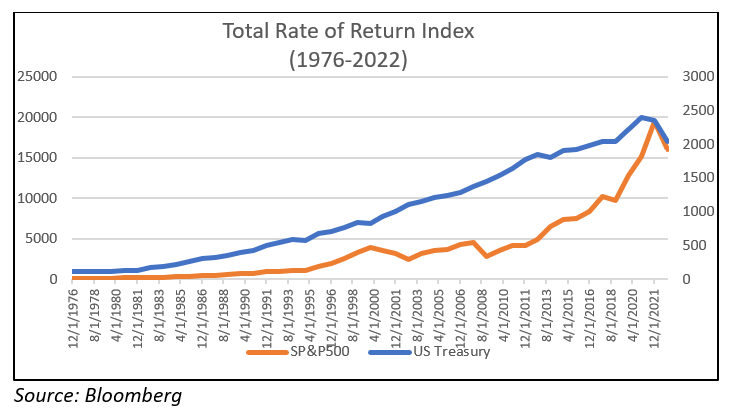

Since the March trough the S&P 500 Index has gained around 14% and ten-year Treasury yields have risen roughly 0.50%. As market conditions have improved, inter-asset correlations have also shifted.

Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

The exit from a decade of very low interest rates, via the most aggressive hiking cycle since 1980 has laid bare the distorted financing incentives that became entrenched in the years between the Global Financial Crisis in 2008 and the end of pandemic-era monetary policies in 2022.

At some point, the world might have too many planes again. But it’s a little early to worry about that too much.

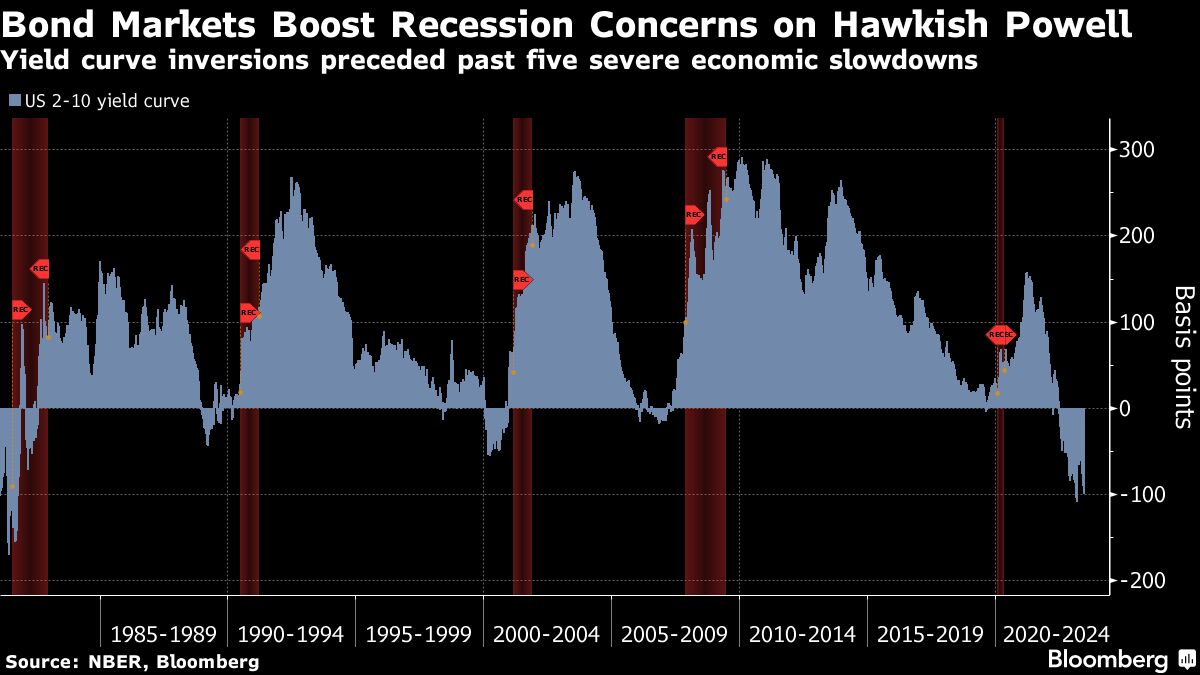

Bond investors’ concern over a potential US recession deepened after Federal Reserve Chair Jerome Powell signaled policymakers may keep pushing interest rates higher.

Japanese stocks may help boost the performance of international markets although the unique nature of Japan's economic and business structure could pose some risks.

Central banks have ramped up their hawkish rhetoric this month but for bond bulls, that’s a good thing.

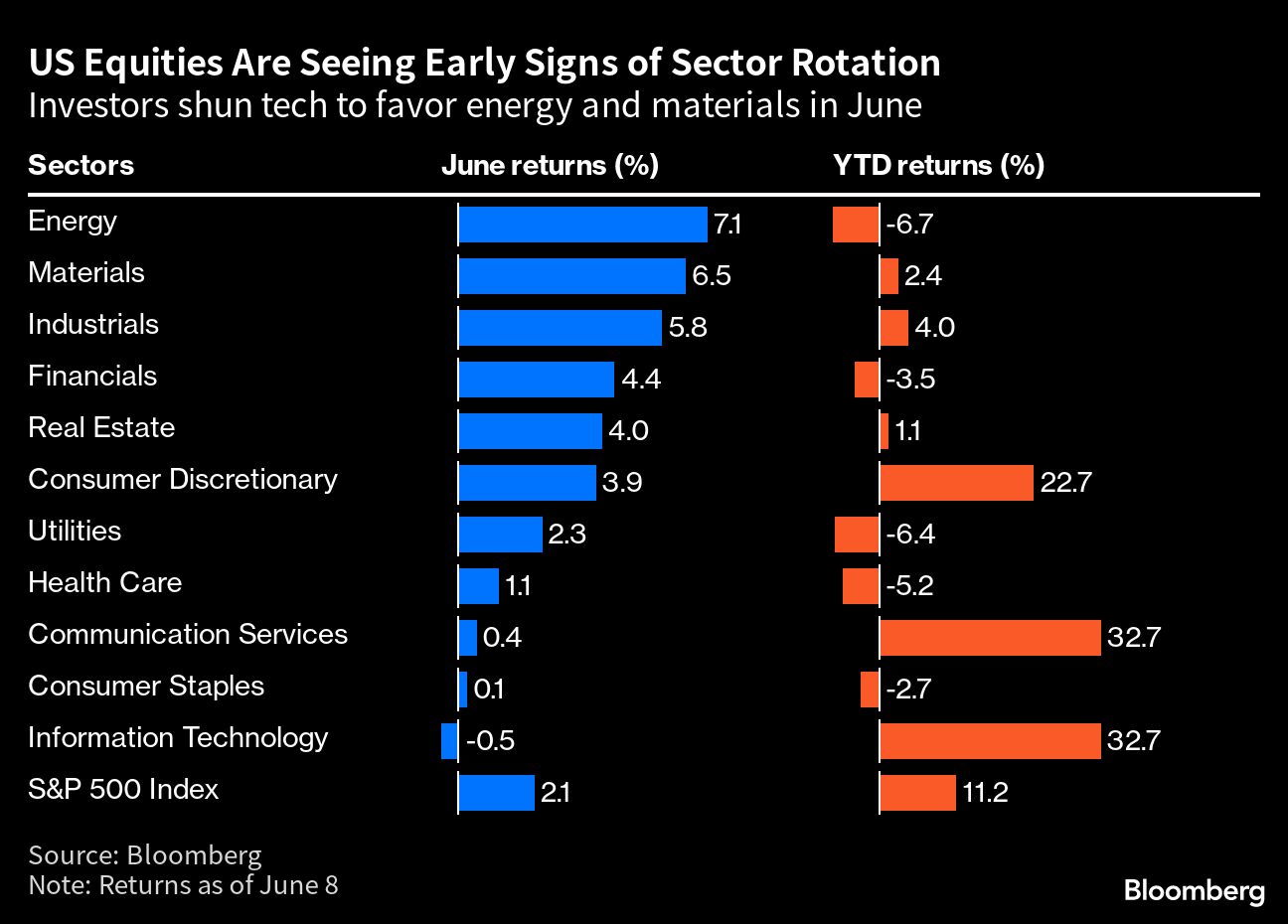

Amid fears of a recession, the S&P 500 is up more than 14% this year, and AI stocks have risen many times more than that. But the market is not in a bubble, according to Jeremy Siegel.

Sticky inflation looks to compel developed markets (DM) central banks to crank policy rates higher – and keep policy tight for longer. The Federal Reserve paused last week but pointed to more hikes on the way.

Federal Reserve Chair Jerome Powell said policymakers expect interest rates will need to move higher to reduce US growth and contain price pressures, even though they held rates steady at their meeting last week.

Our long-term outlook for commercial real estate investing argues for a flexible, long-term approach to seize opportunities in debt and equity investments across the real estate landscape.

Bull markets and bear markets can’t be identified in real-time – only in hindsight. More importantly, the return/risk profile of a “bull market” or a “bear market” can change dramatically depending on whether valuations are consistent with the beginning of a market cycle or the end of one.

The US money-market industry, one of the big winners on Wall Street as the Federal Reserve hiked interest rates, is getting another lift with more tools at its disposal to attract investors and expand its unprecedented mountain of cash.

T. Rowe Price Group Inc., Allspring Global Investments and AllianceBernstein Holding LP are among investors seeking opportunities in longer-dated high-grade corporate bonds, reflecting bets that the peak in interest rates is nearing and a US recession would force policymakers to reverse course.

Quarterly Macro Themes, a quarterly publication from our Macroeconomic and Investment Research Group, spotlights critical and timely areas of research and updates our baseline views on the economy.

In the last couple of weeks, I have had numerous requests to facilitate discussions for large and small teams. Here are my best practices.

At its June meeting, the Fed opted to forgo an increase in its key lending rate for the first time since March 2022 but projected that more rate hikes may be possible by year-end. Our investment strategy analyst shares his thoughts on when the central bank’s rate-hiking journey could finally end.

Most of the things we expected to happen during the first half of the year in fact did: Inflation eased, U.S. economic growth slowed, the Federal Reserve appears to be near the end of its rate-hike cycle, and the U.S. government debt ceiling standoff was resolved before a potential default.

For this edition of Bull vs. Bear, James Comtois, and Elle Caruso debate the pros and cons of investing in high-yield fixed-income ETFs.

They’re the gilded class of high finance, whose shrewd bets and jumbo-sized paydays are the envy of Wall Street.

The surprising resilience of the economy despite the aggressive tightening remains the Fed’s biggest challenge at this point in the cycle. Below we discuss how the Fed’s thinking will likely evolve for the remainder of the year and what it means for the markets.

Opportunities and risk abound in the fixed income space as questions remain about whether or not the Fed will continue to tighten. With the long end of the curve starting to look appealing, but short end yields still being attractive, investors need to unpack how they are approaching the fixed income space. Join iMGP and VettaFi for a webcast that digs into how investors can capitalize on the return of fixed income.

Topics covered will include:

The potential for a Fed pause presents an opportunity for investors to consider adding duration back into their portfolios.

Sometimes it feels like the economy and markets are on different tracks.

The European Central Bank (ECB) hikes rates and signals more tightening ahead.

Measuring changes in consumer prices is a messy, imprecise undertaking, one that can result in conflicting data, and yet these data are used by both the public and private sectors to guide important policy decisions.

Doug Drabik discusses fixed-income market conditions and offers insight for bond investors.

Money managers are flocking to extremely precise fixed-income exchange-traded funds as a hawkish central bank and economic uncertainty batter the bond market.

Macroeconomic uncertainty has sparked questions over the durability of the traditional 60/40 portfolio—highlighting why investors may want to add alternative investments to the mix.

The market faces unprecedented headwinds as the debt-ceiling crisis looms large. Investors can look into defensive strategies that can potentially navigate the choppy waters of the current and projected market environment. Quality, low volatility, and dividend yields are all factors that can help position a portfolio to weather even the toughest of storms. Join the experts at Invesco and VettaFi for an important webcast discussing strategies that incorporate defensive factors.

Topics will include:

Bond traders are stepping up wagers that the Federal Reserve will steer the US economy into a recession.

Turns out not even hawkish saber-rattling by the Federal Reserve is enough to awaken stock investors from the spell cast on them by artificial intelligence.

Advisors parking cash in short-term T-Bills yielding are missing out on potential capital appreciation. The current fixed income market provides an opportunity not seen since the financial crisis to earn total return from longer-dated, high-duration bonds.

Federal Reserve officials paused on Wednesday following 15 months of interest-rate hikes but signaled they would likely resume tightening to cool inflation, projecting more increases than economists and investors expected.

The market for wagers on the course of Federal Reserve policy shows that traders now expect the US central bank’s policy rate will peak in September, where they previously looked for it to crest in July.

In this article, we will compare the three largest U.S. real estate ETFs by market capitalization: Vanguard Real Estate ETF (VNQ), Schwab US REIT ETF (SCHH), and Real Estate Select Sector SPDR Fund (XLRE).

William Eigen isn’t about to apologize for his bond fund’s performance this year. Yes, his $8.7 billion JPMorgan Strategic Income Opportunities Fund is trailing about 60% of its peers after trouncing nearly every one of them last year.

While the 60/40 approach may rapidly become obsolete, the debate over its value has bolstered the teaching of MPT and stressed the benefit of extensive diversification as the most efficient portfolio construction methodology.

The risks for bond investors from next week’s Federal Reserve meeting go well beyond whether officials decide to raise interest rates again.

Despite high volatility in the bond market during the first half of the year, what's surprising is how much didn't change.

The artificial intelligence hype that has propelled US technology stocks in the past few weeks is showing signs of fatigue.

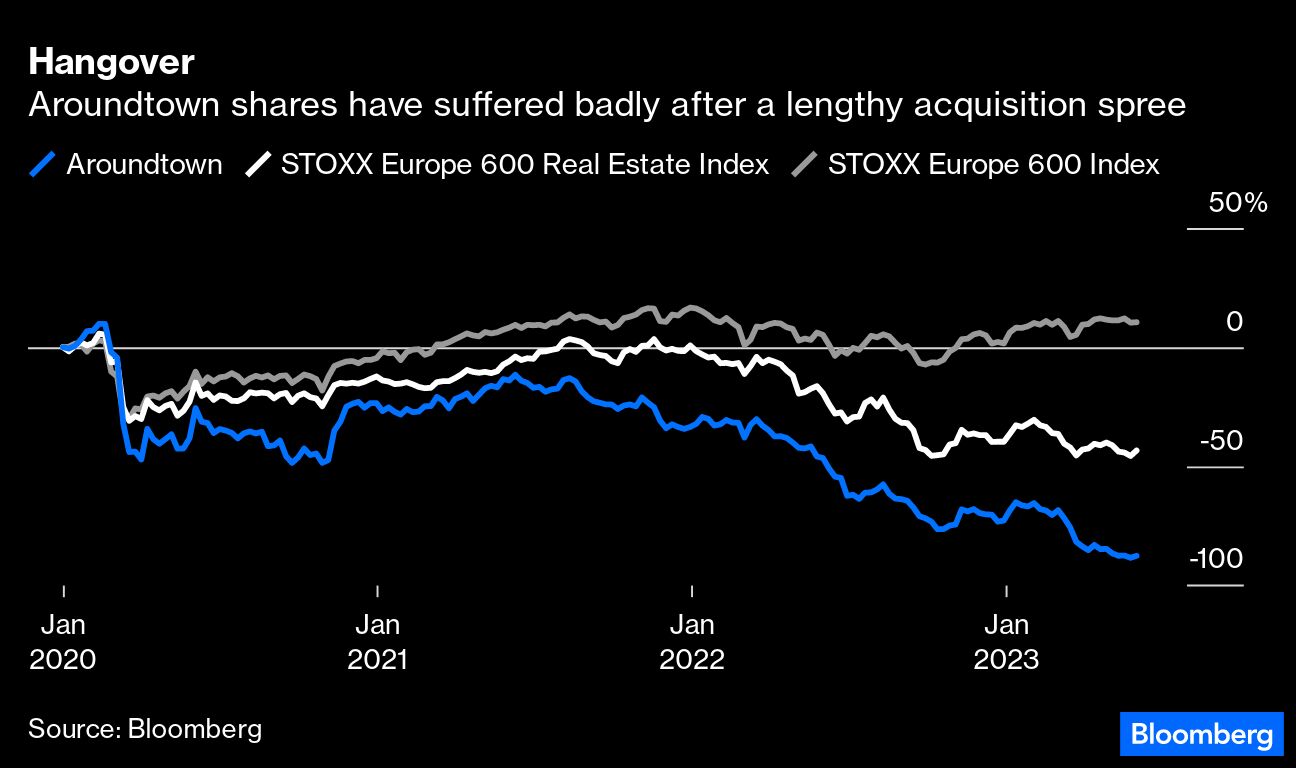

Spare a thought for the other AT1 crowd — not investors in Additional Tier 1 securities extinguished in Credit Suisse Group AG’s rescue, but shareholders in Aroundtown SA, the Frankfurt-listed property firm with the same stock-market ticker.

With the US debt ceiling standoff defused, the Treasury can start borrowing big money again. The government is forecast to issue up to $1 trillion of debt this year in short-term bills, sucking cash out of the US financial system.

If price stability is the legal mandate of the Bank of Japan (BOJ), and the central bank’s official target for price stability is 2%, as measured by the Consumer Price Index (CPI),* then why are fluctuations in prices the norm for Japan?

Transitioning into the post-COVID investment environment shifts the foundations of portfolio construction that investors relied on in recent decades. On full display in 2022, inflation and recession risk punished both bonds and stocks together to historic declines.

For this edition of Bull vs. Bear, Nick Peters-Golden and Karrie Gordon discussed the fundamentals for and against investing in Japan ETFs.

Global bonds are slumping after two shock interest-rate hikes this week served traders a reality check that central banks are far from done fighting inflation.

Investors have had a lot to contend with thus far in 2023. Moderating economic growth, persistent inflation, volatile interest rates, falling profits, stress in the banking sector, war in Ukraine, and the debt ceiling debate all combined to weigh on sentiment.

“Owning bonds is better than white-knuckling it in stocks in an economy that is going into a recession,” Jeffrey Gundlach said.

We see the market’s focus returning to higher-for-longer rates and sticky inflation after a U.S. debt ceiling deal. We prefer an up-in-quality portfolio.