The poor sentiment toward private credit funds has dragged down many high-quality BDCs, as well as weaker ones. The chaos and bad press surrounding private credit funds are not reasons to avoid BDCs. In fact, we think it’s a reason to consider them.

The part of the bond ETF complex that’s growing fastest isn’t that part. It’s the active and outcome-oriented funds — multisector strategies, flexible income vehicles, securitized credit funds, options-overlay products — that charge 0.30 to 1 percentage point and promise more yield, less duration, or both. And the marketing pitch behind them quietly elides something important.

Like Treasuries and Treasury Inflation-Protection Securities (TIPS), municipal bonds betrayed their normally docile reputations in March as the conflict in Iran stirred increased volatility for normally subdued corners of the bond market.

The U.S. economy ended April with mixed signals: steady interest rates and high Fed dissent met persistent, energy-driven inflation. Despite these hurdles, accelerated Q1 growth and rising consumer confidence provided a buffer against ongoing global instability.

April showed us just how sensitive markets can be to a small number of powerful forces: energy prices, inflation and geopolitical risk. The conflict in the Middle East dominated headlines, with a ceasefire helping to steady markets even as energy prices remained elevated.

Although sentiment remains sensitive to headlines around the Strait of Hormuz and energy markets, Franklin Templeton’s Emerging Markets Debt team sees an asset class that has shown it can absorb shocks, even as renewed geopolitical flare-ups or a broader risk-off episode could still test markets.

The sharp rebound from the March lows has pushed most major equity indexes back to record highs. This upside momentum has been fueled in part by signs of de-escalation with Iran and growing expectations that the Strait of Hormuz could reopen soon.

When Jamie Dimon turned to competitive threats in his shareholder letter this year, the chief executive officer of JPMorgan Chase & Co. did something unusual: He named some. Citadel Securities LLC and Revolut Ltd. were two of the firms Dimon picked out.

Where should advisors and investors be looking to find the best opportunities in fixed income? Given the current macroeconomic picture, now is certainly a good time to consider shifting one’s fixed-income portfolio.

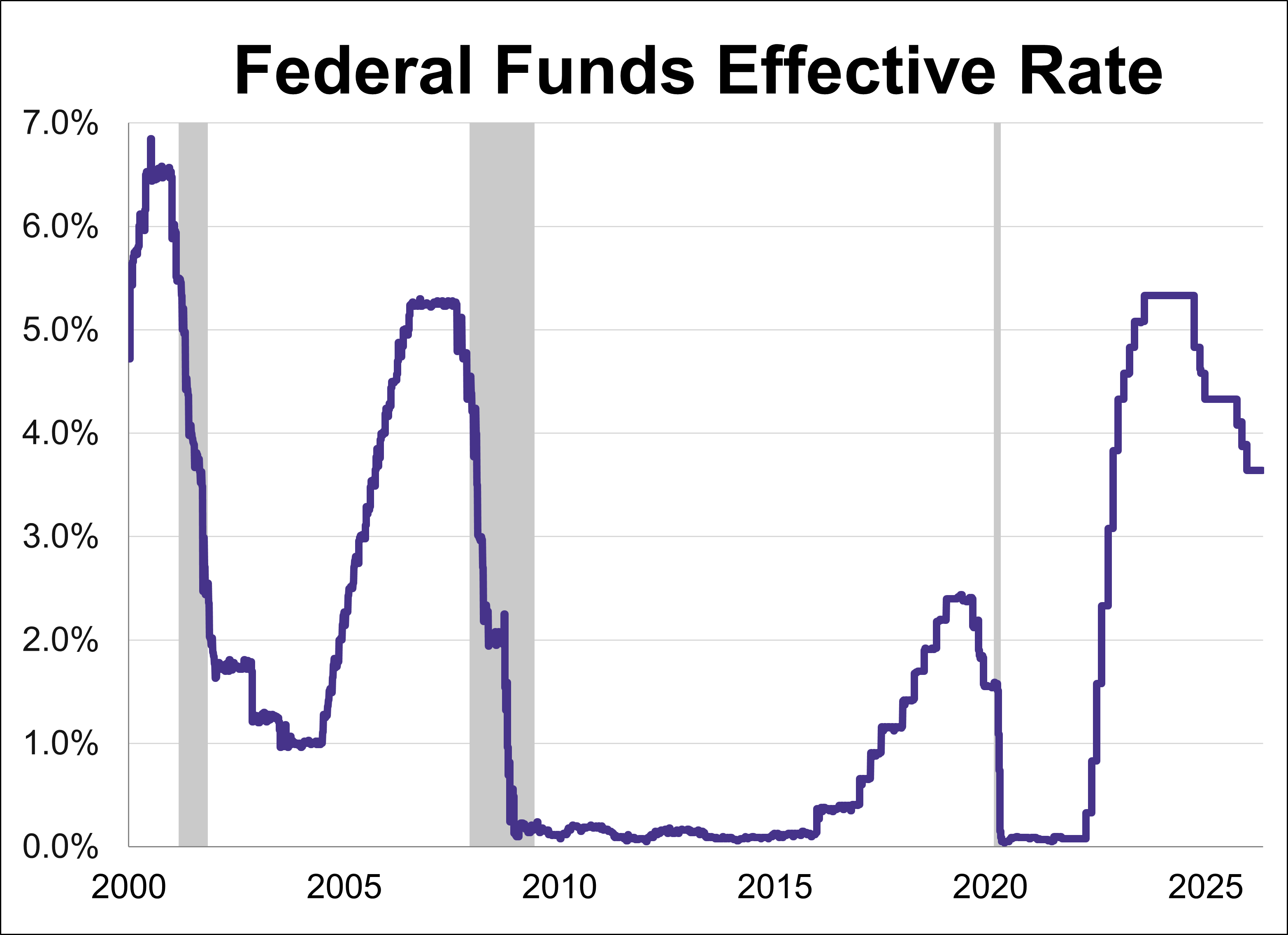

As widely expected amid rising oil, rates will remain 3.5% to 3.75%. However, four policymakers dissented. And Fed Chair Powell will stay as governor after his chairmanship ends.

In a recent (unscientific) Franklin Templeton social media poll, we asked investors what they felt was the biggest risk to the global economy over the next 12 months. Nearly half (45%) of respondents highlighted high oil prices as their greatest fear factor.

Treasury Inflation-Protected Securities, or TIPS, can help buffer a portfolio against inflation. However, it's important to understand their unique characteristics and complex nature.

The Federal Reserve concluded its third meeting of the year by holding the federal funds rate (FFR) steady in the 3.50%-3.75% range.

For much of the past few years, US Treasuries have failed to serve their traditional role as a sure-fire refuge from global market meltdowns.

A quarterly report providing an in-depth analysis of the global economic landscape, key drivers and insights into fixed-income markets for investors.

A few weeks ago, I sat down at my laptop and built a trading platform. It connects to three financial exchanges. It ingests news from RSS feeds, web searches, Reddit and Twitter.

Supply shocks from the Strait of Hormuz don’t hit immediately. But the lag is over. What comes next, across oil, food, plastics, and chips, lands on a Fed in transition.

The defining feature of a Ponzi scheme is that it persuades investors to pay for future cash flows that, at least in part, don’t actually exist, while creating the impression that those cash flows imply an attractive return on the price investors pay. If we look carefully at the record valuation extremes in the equity market, and the wildly elevated profit margins that investors appear to view as permanent, we can already see the potential for difficult, even tragic outcomes for investors.

Markets continue to ebb and flow with every headline out of Iran and the Strait of Hormuz, but the most important message from the markets is resilience. Earnings season is off to a very strong start, with roughly a 75% beat rate, and the AI investment cycle continues to provide a powerful tailwind for equities.

The Middle East war has entered a fragile ceasefire, offering tentative relief to energy and financial markets. Oil prices have eased and volatility has subsided, feeding hopes that the worst disruptions may be passing.

With a better understanding of the derivatives and leverage that led to the GFC, we now explore private credit — a small “niche” financial sector, such as subprime mortgages — which is being called the next match to light a financial bonfire.

If the first quarter of 2026 taught us anything, it's that markets are dynamic and that the factors shaping them extend well beyond corporate fundamentals. The road ahead presents a wider range of outcomes than investors have faced in some time. The outlook remains fluid and highly dependent on how several key factors evolve.

The world’s most important central banks will potentially hand investors fresh reasons to sell government bonds this week as policymakers find themselves forced to confront the risk of a war-driven inflation shock.

Back-and-forth developments over the weekend around the Strait of Hormuz have added near-term volatility to energy markets. That uncertainty is feeding into oil prices and reinforcing questions about how persistent energy-driven inflation pressures could become, particularly if disruption risks continue to ebb and flow.

Last week’s economic data was defined by conflicting signals from the consumer. While retail figures suggest resilience, sentiment levels have plummeted to record lows. Meanwhile, the S&P 500 continued its historic rally as markets prepare for the upcoming Fed decision.

As a more than $20 billion borrowing frenzy to build out data centers descended on the junk-bond market this year, some issuers offered up a rare sweetener: an early cash payback.

Global bond markets are heading for their worst week in a month as investors grow increasingly uneasy about a stalemate between the US and Iran.

Markets have long struggled to price geopolitical risk. Part of the issue is that each flare-up tends to be viewed as a one-off volatility jolt to be weathered and then faded once there is resolution.

During and after World War II, Allied forces established airbases across remote Pacific Islands, bringing with them food, medicine, tools, and machinery that the indigenous people had never encountered before.

Concerns about the sustainability of U.S. fiscal policy have moved back into the investment spotlight. Over the past week, both multilateral institutions and prominent policymakers have raised warnings about the potential implications of America’s expanding debt burden for Treasury markets.

When advisors and investors hear the terms “high yield” or “junk” as it relates to bonds, they understandably have some apprehension. After all, junk bonds carry elevated credit risk relative to their investment-grade peers. Hence the higher yields, which act as added compensation for the extra risk.

Fixed-income market sentiment was dominated by geopolitical headlines, particularly the conflict in the Middle East following disruptions to the Strait of Hormuz and rising oil prices, which contributed to renewed inflation concerns.

Since the Federal Reserve announced the resumption of quantitative easing (QE) in December, the central bank has expanded its balance sheet by over $200 billion.

The U.S. market story this year has been a tug-of-war between sticky inflation, slower growth, and resilient risk appetite. For fixed-income investors, that mix has produced more narrative movement than the 10-year Treasury itself.

Vanguard is boosting its holdings of Treasuries, taking advantage of higher yields following the Middle East conflict to lock in rates and hedge against the risks of a potential growth slowdown.

LPL Research examines the fixed income space as global bonds broaden yields and reduce U.S. concentration, offering diversified income and resilience via non‑U.S. developed and emerging markets.

As always, I hope you’re having a good 2026 and that all is well with you, my readers, and your family and friends. Here’s my latest.

The history of the U.S. airline industry is really a history of consolidation driven by crisis. The pattern has been remarkably consistent. Historically, when an external shock has hit—a recession, a war, an energy spike—the weakest carriers have folded or been acquired, while the strongest have emerged leaner and more profitable.

Get ready each week with high-conviction insights that go beyond media headlines.

Oil shocks hitting economies with weak demand and strained balance sheets are especially damaging. Firms cannot fully pass on rising costs, so margins shrink, layoffs increase, and investment falls. Tightening monetary and credit conditions would cause inflation to fade faster but job losses, failures, and fragile household finances to be much worse.

Given the misunderstanding linking subprime mortgages and private credit, I discuss how leverage and derivatives, layered atop subprime mortgages, were at the heart of the GFC. A better understanding of that event will help advisors and investors better assess whether recent woes in private credit are an omen of another crisis or an overstated concern.

The S&P 500 closed Wednesday at a fresh all-time high of 7,022.95, surpassing the late-January peak and capping a remarkable round trip from the spring selloff.

Iran war-related headlines continue to cause volatility in the markets and oil prices to rise, but our experts remind readers that uncertain times might also present opportunities.

The most exciting innovations aren't always the ones that break new ground—sometimes they're the ones that finally make breakthrough ideas work. This quarter’s spotlight reveals how researchers are removing practical barriers to turn promising laboratory technologies into deployable solutions, from agricultural robotics to dissolving medical devices, transforming theoretical possibilities into tools that can reshape industries today.

Much of the conversation around private credit versus public high yield focuses on yield levels, default expectations and headline volatility. But we think what matters most is how each market lets investors measure, manage and reprice risk as conditions change.

US stocks rallied Friday after Iran said it would open the Strait of Hormuz following the truce between Israel and Lebanon, promising to ease an oil shock that has shadowed the global economic outlook ever since President Donald Trump started the war seven weeks ago.

While recent market performance reflects optimism over potential geopolitical de-escalation, underlying economic data reveals a complex landscape of intensifying price pressures and cooling growth. This article examines the major economic news from the week of April 6-10th, 2026.

Late last year, the Federal Reserve ended its latest quantitative tightening (QT) program: the process by which it shrinks its balance sheet by selling securities or letting them mature without reinvestment.

Asia and emerging markets experienced extreme volatility in the first quarter of 2026 as markets surged in the first two months, supported by strong demand for artificial intelligence (AI) and an easing of the global monetary environment.

Rising oil prices and the historically inflationary aspects of war have changed expectations for Federal Reserve interest rate policy and have pulled Treasury yields higher.