Bullion is benefiting from the dollar’s weakness coupled with continued risk hedging, and a breach of the $2,000 mark will “fan the flames of interest.”

Led by technology and large-cap companies, the S&P 500 is on pace to post its best summer performance in over 80 years.

The Fed’s new take on inflation was a long time coming, while Japan’s downturn drags on and U.S. housing stays strong.

The Federal Reserve just tweaked how it thinks about inflation, and this could have a huge impact on gold and gold mining stocks. But Fed Chair Jerome Powell’s speech raises the question yet again if we’re even measuring inflation accurately in the U.S.

The world’s second-largest money manager said it will instead focus on individual investors in faster-growing parts of Asia, including mainland China.

Although many suggest that wealth inequality is attributable to globalization and technological advancements, what they miss is the role of speculative finance and the complicity of the central bank in driving this process.

The number of Americans filing for initial jobless claims this week spiked above 1 million, while the number of deaths attributed to COVID-19 remains above 1,000 a day. But there was much else to celebrate.

This depression/recession is unlike any we have experienced. Parts of our economy are doing well, parts are in recession, and a significant portion is already in a depression. As government guarantees wane in the future, more and more companies and people will slip into the depression category.

Companies from Samsung Electronics Co. to Apple Inc.’s assembly partners are showing interest in investing in India.

Four important trends are continuing in China: COVD-19 remains largely under control; the economy is in a V-shaped, post-COVID recovery, led by strong domestic demand; U.S.-China relations are tense and likely to worsen; but the political problems between Washington and Beijing should continue to have little impact on China's economy or its investment environment.

The price of gold had its first down week since early June, ending a spectacular nine-week rally. The yellow metal briefly fell below $1,900 an ounce on Wednesday as stocks neared their all-time closing high and the 10-year Treasury yield jumped on record supply.

Although certain high-frequency data haven’t improved markedly, the threat of the virus has started to recede.

The equity rally has been dominated by technology and other growth companies, some of which have valuations that already reflect earnings that are two years out, Wien said.

Cash may still be king, but cashless commerce is rapidly becoming the new king. The revolution in digitalization of commerce is already generating growth in transaction value of roughly 24 percent per year over the last three years.

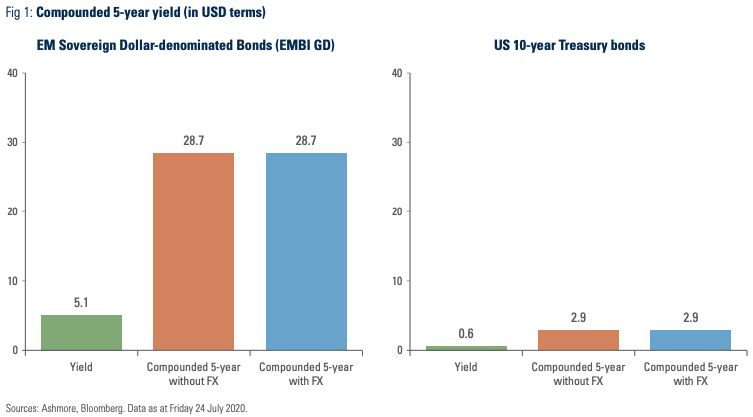

Welcome to the 9th annual review of the Emerging Markets (EM) fixed income asset class. Using new data from the Bank of International Settlements and other sources, we establish that the EM bond market has expanded by 12% in Dollar terms in the past twelve months to a size of USD 29.6trn, or 25% of the global fixed income universe as of the end of 2019.

Americans enjoy the economic prosperity and freedoms of its liberal democracy. But our elevated stature is threatened. As the U.S. recoils from the world, the era of U.S. dominance might be ending.

For the week, airlines stocks increased 9 percent, its best weekly performance since early June. Wheels up!

As the global economy continues to grapple with the COVID-19 pandemic, there are still opportunities for investors, says Franklin Equity Group Portfolio Manager Don Huber. He has an eye on international companies able to navigate the crisis period—particularly those in regions where recovery is happening faster.

Government bond yields have tumbled globally but China’s yields have risen to pre-COVID-19 levels. The RMB hasn’t yet reacted to the favorable rate difference, and we think bond yields are likely to decline moving forward—a favorable landscape for China bonds.

Several months into the Covid-19 era, Howard Marks takes a step back to consider the global health crisis, the economic fallout and the U.S.’s response to date. He also shines light on how one might – or might not – view the current circumstances in the framework of a market cycle.

The U.S. economy contracted 9.5% through the second quarter, the worst single-quarter decline in gross domestic product (GDP) since the Commerce Department started tracking it in 1947. It was expected the report would show a dip, but it’s important to recognize what that dip represents.

Two companies in the metals and mining space I’m looking forward to hearing from are Ivanhoe Mines and Franco-Nevada. Both are scheduled to report next week.

The U.S. dollar has fallen by about 7% against a broad basket of currencies since its mid-March peak. After a nearly decade-long bull market that saw it appreciate by more than 40%, we believe the dollar could be headed for a longer-term decline.

Gold has been on a tear over the last year, rising 32% while global equities have languished. A common objective of gold is to hedge against some type of risk. This paper shows how gold can reduce downside risk during big down markets, but isn’t the most effective inflation hedge.

Ultimately, we believe that investors who are unaware of ESG and do not integrate ESG into their investment processes may be exposing themselves to additional, unnecessary and possibly unrewarded risks.

Does 9 times higher yield in EM than in US bonds make for an attractive investment proposition? We lay out the arguments.

We all know that past performance is no guarantee of future results, but you can see in the chart below that the white metal could possibly be setting up for another epic run-up. At this stage of the bull market, silver’s current price appreciation is ahead of any previous rally.

The U.S. and EU deliberate how to disburse aid, China’s recovery carries risks, and U.S. mortgage rates find a floor.

Investors must balance ongoing risks of the coronavirus against the extra yield the bonds provide.

I’ve always been frustrated by the lack of clarity about what advisors earn. And then I did my own research…

In emerging markets, some industries and countries are in better shape than others. And many businesses have the right qualities to benefit from structural changes now and long after local conditions improve.

Weeks before the S&P 500 bottomed, many millennial Robinhood investors began picking up coronavirus-impacted airline stocks. The buying spree continued even after Warren Buffett announced that he’d dumped his holdings.

China's V-shaped economic recovery continued for a fourth consecutive month in June, led by strong domestic demand. If COVID-19 remains under control, China can remain the world's best consumer story.

At LPL Research, we know the stock market is forward-looking: It focuses on what’s happening today and what it sees on the path ahead. Much of the real-time economic data we follow—such as transportation activity, home sales, and jobless claims—is showing tangible evidence that economic activity—while still depressed—has begun to make a comeback.

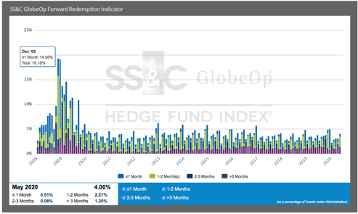

The value of this year’s annual hedge fund performance survey was turned on its head when a pandemic shut down the global economy and sent securities plummeting. But a deeper look at consistently performing funds revealed managers that as a group have largely been able to weather the storm better than the market and their peers.

Precious metals were the big winners for the first six months of 2020. Spot gold took the first place position, rising over 17 percent, followed in second place by silver, up nearly 2 percent. Palladium rounded out the top three, essentially flat at negative 10 basis points.

Software and hardware companies are supporting new forms of consumption in Asia, such as the growing popularity of online games. Portfolio managers Sharat Shroff and Inbok Song discuss the opportunity set for long-term investors.

But a survey did flag some promising growth areas for wealth managers.

With inefficiency comes opportunity, according to Franklin Templeton Fixed Income’s Nicholas Hardingham and Robert Nelson. They consider the emerging market debt landscape, and what the remainder of the year could bring for the asset class.

The COVID-19 pandemic continues to impact economies across the globe as they emerge from lockdowns, including emerging markets.

A key lesson of 2020 is the importance of staying invested even during times of high volatility. We believe that an appropriately risk-targeted, globally diversified portfolio is as important as ever. Maintaining an optimally risk-controlled portfolio is most desirable.

As states ease their COVID-19 lockdown measures, rising case numbers have put pressure on equity markets.

After reporting better than 4th quarter results on Tuesday, the stock price of FedEx Corp. (FDX) has been on a tear. With this article, I plan to demonstrate that the fundamentals support the current price rise.

Many investors are looking for emerging signs of a return to normalcy from the coronavirus crisis. While there are many indicators to choose from, we’ve assembled a group of signals, with the help of big data, that may point the way.

How does a Knowledge Leader handle a global pandemic? By adapting.

A “perfect storm” of surging government debt levels, plunging real bond yields, rising coronavirus cases and deteriorating economic forecasts pushed the price of gold to an eight-year high this week, and some analysts now project the metal to top its all-time high within the next 12 months.

Volatile markets and the economic fallout from the virus could wipe out as much as $16 trillion of global wealth this year and hinder growth for the next five years, according to a study.

Banks undergo a true stress test, smartphones measure movement, and poverty may rise.

As the global economy slows, we remain optimistic about the long-term growth potential of Chinese equities. From a public health perspective, China has flattened its curve of new cases COVID-19. Fiscal and monetary stimulus, while incremental, remains supportive. Interest rates remain positive, giving China's central bank room to maneuver.

The common characterization of US-China relations as a new Cold War is wrong. Instead, the most recent spike in tensions between the two countries – the second time this has happened since US President Donald Trump took office in 2016 – is primarily motivated by political considerations ahead of the November US presidential election.