Want to read more by Ashmore Group? Visit their Featured Firm page here

The common characterisation of US-China relations as a new Cold War is wrong. Instead, the most recent spike in tensions between the two countries – the second time this has happened since US President Donald Trump took office in 2016 – is primarily motivated by political considerations ahead of the November US presidential election. Therefore, tensions may well escalate leading up to November, but there will then be mileage in striking a deal and defusing those tensions after the next Administration takes office.

China and the US are so closely linked in economic terms that a serious worsening of ties would be costly for both countries, at a time when neither can afford further negative economic shocks. Hence, a proxy conflict looks more likely with Hong Kong clearly in the sights. If the US pulls the rug from under Hong Kong, we would expect China to step in with massive support and thereby deepen ties with Hong Kong at the expense of Hong Kong’s ties with the US. We believe that the US obsession with China is partly attributable to fear, given that China’s economy is on track to be nearly three times that of the US by 2050.

China is moving inexorably in the direction of replacing the US as the global economic and financial hegemon. The best play for the US is not to try to prevent China’s rise, but to focus on America’s own problems and how to overcome them. This is what China is doing as reflected in the government’s clearly defined dual policy focus on structural economic reforms and attaining technological independence from the US.

China’s biggest challenge is to overcome eye watering mistrust in Western economies. To address this problem, which is not entirely under Chinese control, China can be relied upon to continue to act in a responsible manner in global relations. On balance, this means that China should continue to be a positive factor for EM, regardless of what happens with US-China relations.

Not a Cold War re-run

Many have argued that the recent escalation in tensions between the US and China amounts to a new Cold War.1 In our view, the analogy with the Cold War is misplaced, especially as far as the rest of the world is concerned. There are two very important differences between the Cold War of old and the current worsening of US-China relations.

The first difference pertains to the two economic systems. The Cold War pitted two mutually exclusive economic systems against each other, centralised state planning models versus mixed market economies. This is patently not the case today. For example, US economic policies tend to aim at generating a short-term impact, while China implements very long-term economic policies. The US tends to focus more on stimulating demand, while China places far greater emphasis on supply-side reforms. China is opening its economy and assuming a greater international role, while the US is turning inwards and shrinking from its erstwhile role as global hegemon. Finally, the role of the state is gradually expanding in the US, while China is granting more and more room for the private sector in the allocation of capital.2 In short, both the US and China run mixed economies today based on market principles, where the differences are more in terms of style and nuance than substance. On balance, however, we expect that the growing emphasis on cooperation with other countries, economic openness, and private sector participation should enable the Chinese economy to continue to grow faster than the US economy for the foreseeable future, since these broad policies are all associated with higher trend growth rates.

The other reason why the current US-China tensions do not qualify as a re-run of the Cold War is that the US-China rivalry does not involve numerous ‘hot wars’ in large numbers of Emerging Market (EM) countries. During the Cold War, NATO powers and the Warsaw Pact supplied dictators in EM with guns and money to fight proxy wars on their behalf. These conflicts had massive negative economic, political, and humanitarian consequences for dozens of EM countries. Today, apart from a few flash points around the Middle East there is very little outside interference in the domestic affairs of most EM countries. The US no longer has the economic clout to install and maintain dictatorships in dozens of EM countries, while China never did go in for empire building. Indeed, China is often criticised in the West for not interfering in the domestic affairs of other countries. China’s involvement in EM today tends to revolve around mutually beneficial investments, such as the projects being implemented under the Belt and Road Initiative.

Elevated tensions

Even if US-China tensions do not amount to a fully-fledged Cold War, they should nevertheless be taken seriously. The number of disagreements between the two largest countries in the world has increased sharply, since President Donald Trump assumed office (see Figure 1). From the onset of his presidency, Trump signalled a more confrontational stance towards China, including the appointment to his Administration of two known ‘China phobes’, Director of Trade and Manufacturing Policy Peter Navarro and Secretary of Commerce Wilbur Ross. Tensions first spiked in 2018, when the US government unilaterally hiked tariffs on Chinese imports, thus firing the first shot in Trump’s Trade War with China. The Trade War ended with the singing of the Phase 1 Trade Agreement (‘Trade Agreement’) in early 2020.

The big anti-China election gamble

A second surge in US-China tensions is now upon us, manifesting itself through a sharp increase in the number, severity, and scope of largely one-sided US attacks on Chinese interests ranging from tech and investment to immigration, journalism, and transportation. The Trump Administration is also threatening sanctions against Chinese companies and individuals. The primary motivation for these attacks appears to be the upcoming US presidential election in November 2020. Trump’s approval ratings have steadily declined recently due to social tensions and his Administration’s handling of the coronavirus outbreak. Picking a fight with a foreign power is one of the oldest tricks in the book for politicians wishing to detract attention away from problems at home.

The official reason for hostility towards China is that China did not share information about its coronavirus outbreak early enough. Be that as it may. Yet, as late as 29 February 2020, long after coronavirus had already spread to Europe, Trump was still labelling the outbreak a Democratic Party “hoax”.3 Clearly, if China was late in reporting, the US was late in responding. Besides, it is largely irrelevant where the disease originated. MERS originated in the Middle East. SARS originated in Hong Kong. H1N1 originated in the United States. We can all be unfortunate to be the first to be hit by a new illness.

Hence, it is difficult to escape the conclusion that the US attacks on China are laden with political overtones. This has two clear implications. On the negative side, relations between the US and China can get a lot uglier between now and November, particularly since the presidential election race is now quite tight and the economic and political situation in the US is not great. Moreover, Democrats as well as Republicans are falling over themselves trying to sound as anti-China as possible. A détente between the two countries between now and November certainly seems unlikely at this stage. On the positive side, the fact that much of the anti-China rhetoric is politically motivated also means that things can change for the better surprisingly quickly. We think it is likely that relations will improve after the election, regardless of who wins, if only because by then relations will be so bad that there will be political mileage in mending fences. Or to put it more succinctly, we believe that this second spike in US-China tension is for the most part a big political play on the part of the US political establishment to garner support leading up to November.

How bad can it get?

Even if the current spike in tensions between the US and China is politically motivated and largely transitory, how bad can thing get between now and November? This depends largely on the politics in the two countries. The US has tended to be the aggressor in recent years, while China has generally exercised restraint, something which has clearly helped to limit the fallout from the conflict. Take, for example, China’s actions during Trump’s Trade War. China never initiated tariff increases, never increased tariffs as much as the US, nor did China ever apply tariffs to as many goods as the US. China also stuck to its official position that conflicts arising from competing national interests should be resolved within a multilateral framework, such as the World Trade Organisation. As we discuss later, China’s overt preference for conflict resolution within a multilateral framework is well-grounded and should generally be expected to continue.

Having said that, China will not always turn the other cheek. China cannot appear to be weak or humiliated. Domestic political considerations require China stand up to the US if and when the latter targets areas deemed to be of vital national importance to China. Hong Kong is a clear case in point. In a somewhat uncharacteristic move, China recently fast tracked the approval of new security laws for Hong Kong. China clearly wanted to pre-empt what China saw as likely US efforts to destabilise Hong Kong, given the long line of other US attacks in recent months. However, even in approving the new security laws for Hong Kong, China’s actions were largely defensive. For example, China has taken no measures against the US at all. Still, barred now from intervening in Hong Kong, the Trump Administration is likely to seek ways to escalate tensions with China, for example, by withdrawing Hong Kong’s semi-autonomous status. This has already led to speculation in the media that China will retaliate by reducing imports of US soy products, thereby putting the Trade Agreement in jeopardy. So far there is no evidence to support this allegation, though. In fact, Robert Lighthizer, the US Trade Representative, recently said that China has not broken the terms of the Trade Agreement.

The scope for escalation is ultimately going to be limited by the fact that China and the US depend on each other to a considerable extent. China sells goods to America and finances America in return. Political gain therefore soon precipitates economic pain, which is a tough trade-off at a time, when the US economy has officially entered recession. Besides, the US cannot destroy China, because Trump has already fired his most potent weapon, the Trade War in comparison to which almost everything else is fairly secondary in terms of causing potential damage to China. Washington will also be aware that the slowdown in Chinese economic growth caused by the Trade War did not weaken President Xi Jinping’s standing the way many thought it would.

One of the reasons for Chinese economic resilience is that China has been preparing for a more hostile external environment for more than a decade. This preparation is most clearly manifested in the rotation away from export-led to consumption-led growth. China and Chinese companies are also striving to be adaptable in a less predictable world. The Chinese government is not shy to extend support to help companies, when they are under attack. Chinese companies are also likely to respond to US demands for higher accounting standards and greater transparency by meeting those higher demands, since that is how they learn and become more acceptable in the West.

Finally, investors need to consider market conditions. Worsening US-China relations and the potential for further escalation is already to some extent priced in the market.5 As markets bounce back as lockdowns are lifted, sentiment is likely to remain reasonably supportive of risk, which in turn means that markets may discount somewhat any escalation in tensions.

What about Hong Kong?

For Hong Kong, of course, the situation is different. The new security laws are a done deal and will be implemented, in our view. They only need to be codified before they are presented to and approved by the Hong Kong Legislative Council. The US may well use this as a pretext for withdrawing Hong Kong’s special status, including tariff free trade. If so, Hong Kong, not China per se, will clearly face a serious economic shock. China’s economy is about 37 times larger than Hong Kong’s economy. We expect that China would respond to any US measures against Hong Kong by unleashing a massive support package for Hong Kong. Indeed, on 8 June Hong Kong and Macau Affairs Office Deputy Director Zhang Xiaoming said that China will “definitely strengthen” and “spare no effort” in supporting and reinforcing Hong Kong’s status as an international finance centre after the national security law is implemented. This means that any US effort to cut Hong Kong off will probably end up pushing Hong Kong even deeper into China’s embrace.

We expect that the majority of the Hong Kong population will respond positively to economic incentives and opt to remain in Hong Kong, even after the new security laws have been implemented. China is likely to maintain the official “One Country, Two Systems” policy until 2050, while at the same time gradually replacing more and more key positions of influence with pro-Chinese people. Indeed, this has already been going on for many years as anyone in Hong Kong will testify. The reality is that Hong Kong’s economic interests will inescapably gravitate further and further towards China over time as China’s economic influence in Asia and the world continues to grow.

Why China?

In some sense, the US obsession with China is a bit odd. After all, Europe – both bigger and more technologically advanced than China – is a more obvious target. However, Europe is the most tribalistic region in the world, which means that Europe punches far below its weight in terms of foreign policy – and will likely continue to do so for many years to come, in our view. Europe first needs to master basics, such as centralised fiscal policy, before it can hope to pose a threat to the US on the international stage.6

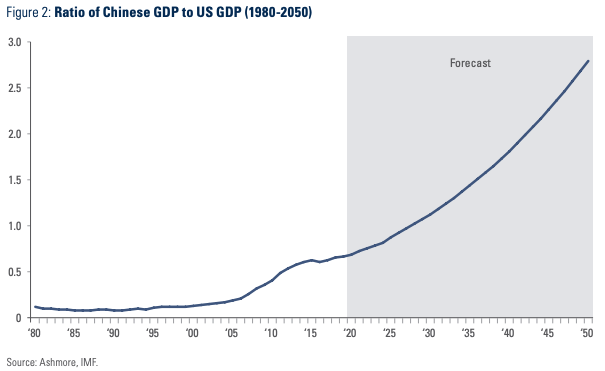

China, on the other hand, does speak with one voice and can act with purpose, though, as mentioned earlier, China is not keen on overtly aggressive foreign policy. The greater worry for Americans is that China has been so successful in economic terms over the last two decades. China may still be a lot poorer than Europe, but it is clearly catching up very fast. According to the IMF, China’s economy is on track to overtake the US within a decade. Figure 2 shows how the ratio of Chinese to US GDP is likely to evolve between now and 2050.7 By 2050, China’s economy should be somewhere between two and three times larger than the US.

Economic reforms

It is this prospect of China overtaking the US, which instils most fear in Americans,8 a fear that is cleverly exploited by the Trump Administration. Trump depicts international relations as a classic zero-sum game, wherein one country’s gain implies another country’s pain. In this simplistic narrative, a country is either the top dog or risks being vanquished. Staying on top means constantly fending off challengers. In this narrative, the US must therefore attack China while there is still time. In reality, of course, America cannot keep China a bay by attacking her. China’s own policies propel China forward regardless of what the US does. When a country falls behind, or perceives itself to be falling behind, its best option is never to attack, but rather to focus on its own problems and find ways to fix them in order to perform better. In that sense, policy making is very much like competitive rowing: you never look out of the boat at the competition, because you immediately lose rhythm and speed and end up hurting your own performance.

The policy direction in China

All China’s policies are geared in some way or another towards propelling China to fulfil its full economic potential.9 The policy framework is designed to achieve this by focusing on two specific areas. One is to transform the country’s economic structure; the other is to move China up the technology ladder. So far, China has managed not to lose sight of its longer-term policy objectives despite plenty of US provocation.

Structural reform

In terms of structural economic reform, China is currently in the process of transforming itself from an export-led economy to a consumption-led economy. China’s economy will soon look more or less like the US economy today. Consumption rather than investment will become the most important driver of growth. Domestic demand will be controlled primarily by using interest rates rather than directed credit, which means that the People’s Bank of China will increasingly assume a similar function as the Federal Reserve in the US. China’s current account will move into deficit, just like that of the US, and be funded by capital inflows. As her markets expand, China will grow ever bigger in global benchmark indices and investors will want to store more and more value in CNY, which will gradually emerge as the dominant global reserve currency of choice. Investors will choose to benchmark against Chinese markets precisely because they are the biggest and most liquid. To be sure, the US will also have sizeable and important markets, but they will no longer be the largest or most important. Asia will be the leading region of the world, led by China.

To bring about this outcome, the Chinese government is emphasising liberalisation of interest rates, prices, and the capital account. Freeing up rates, prices and cross-border flows is not easy, because it introduces more uncertainty, where previously there was the certainty of state planning. Growth naturally slows for a time during the transition, while private investors become accustomed to a more volatile environment associated with free prices and exchange rates and interest rates. China’s trend growth rate will gradually decelerate as the economy becomes more dependent on consumption and less dependent on fixed asset investment. Even so, due to China’s much greater proclivity to reform, her growth rates will still outperform those of most Western economies over the next couple of decades.

Tech policy

In terms of technology policy, China already developed an indigenous, self-sustaining process of technological change some time ago.10 China can already design chips, including CPUs. It can also manufacture chips, but very high end chips are still produced in Taiwan (TSMC), Korea (Samsung), and the US (Intel). China also still depends on the US for highly specialised inputs and processing facilities, particularly semiconductor equipment, such as lithography tools used to manufacture chips. In theory, the US could cut off China completely as without semi equipment there is no chip design and no chip manufacturing. But the US also depends on many inputs from China.

China wants to break its residual dependence on US technology firms. To address this vulnerability, China recently announced a New Infrastructure Plan worth USD 180bn, which will be executed via private sector internet companies. Some USD 100bn of this plan has already been committed with Alibaba is investing USD 28bn in datacentres over the next three years and Tencent spending USD 70bn on datacentres, AI, and other related investments.

The most likely outcome is that the world moves towards two tech ecosystems, one in Asia and one in US/Europe. A similar path adopted in the internet space, where for every major US company there is a Chinese counterpart: Amazon-Alibaba, Google-Baidu, Facebook-Tencent. Both ecosystems compete for business in EM, just like Alibaba/Tencent compete with Amazon in India, for example.

China’s real challenge

Despite having the right policies in place, China still faces an enormous challenge in overcoming . eye watering levels of mistrust in the West. Much of the suspicion about China is unwarranted as many EM countries understand well, since they have worked more closely with China in recent years than most developed countries.

To chip away at the prejudice, China uses every opportunity to act in the reasonable and multilateral manner expected of a future hegemon. This explains why China calls for free trade, when the US turns protectionist. It explains why China doubles down on environmental policies and calls for global action, when the US pulls out of climate accords. China offers to share vaccines, when the US pulls out of the WHO. Multilateralism is a long-term Chinese policy objective, but the success or otherwise of this strategy is obviously not entirely down to China’s own actions.

One thing is certain, however. As long as China continues to harbour ambitions to become a global hegemon it can be expected not to do anything draconian to destabilise the world order, which China, after all, stands to inherit. In this vein, investors should not expect China to sell US Treasury bonds in response to US provocation. In fact, China will happily continue to buy US debt, even to the point where the US drowns in debt.

Implications for the rest of EM

Whenever risk aversion spikes and investors pull money from EM, such as during the coronavirus outbreak China eyes an opportunity to deepen international ties and extend influence. To this end, finance plays a very important part. China recently suspended the debt service obligations of no fewer than 77 developing countries nations. In one fell swoop, China beefed up its ‘soft power’ by making friends with 77 countries – more than one third of the world’s countries. By contrast, America’s main contribution to many of the lowest income countries in the world has been to label them “shithole” countries.11

There is also no reason to expect China to trade less with EM countries, regardless of what happens with US-China relations. Indeed, there is evidence that US protectionism has led to greater intra-EM trade.12 For most EM countries, there is scope for increasing trade with China, which still only measures single digits in terms of percentage of GDP.

In terms of growth, EM will contribute more than 80% of global growth over the next five years. The main driver of EM growth will be domestic demand as capital flows back to EM to ease financial conditions. China’s contribution will be substantial, but should stabilise around 33%, while the contribution of non-China EM rises steadily towards 51% by 2024. Developed economies will only contribute about 16% of global growth by 2024.

1 For recent examples, see https://www.ft.com/content/fe59abf8-cbb8-4931-b224-56030586fb9a and https://www.economist.com/leaders/2019/05/16/a-new-kind-of-cold-war?gclsrc=aw.ds&gclid=EAIaIQobChMI-67y6pv16QIVGLLtCh3lTQ_mEAAYASAAEgL89fD_BwE&gclsrc=aw.ds and https://thediplomat.com/2020/06/the-3-flashpoints-that-could-turn-a-us-china-cold-war-hot/ and https://www.wsj.com/articles/yes-america-is-in-a-cold-war-with-china-11591548706.

2 For a discussion of the gradual encroachment of the state on markets in Western economies see: ‘Macroeconomic control regimes’, Market Commentary, 15 May 2020.

3 See: https://www.youtube.com/watch?v=G5TZ6fTYrsE

4 See: https://www.nber.org/cycles.html

5 The market has not priced an increase in tension over Tibet.

6 In fact, the fact that Europe does not interfere as much in other countries’ affairs as, say, UK and US, is a good thing, in our view. The age of mercantilism is over.

7 The analysis is based on a constant ratio of US and Chinese population sizes and the real GDP growth rates, which prevailed from 1980 to today, using IMF data

8 See for example: https://fortune.com/2018/08/15/china-us-learn-mandarin-language/

9 For a discussion of the strategic outlook for China see: ‘China roadmap’, Market Commentary, 17 June 2015.

10 See: ‘China’s R&D revolution’, The Emerging View, 7 May 2015.

12 See EM trade patterns after two years of Trump, The Emerging View, 3 March 2020.

No part of this article may be reproduced in any form, or referred to in any other publication, without the written permission of Ashmore Investment Management Limited © 2020.

Important information: This document is issued by Ashmore Investment Management Limited (‘Ashmore’) which is authorised and regulated by the UK Financial Conduct Authority and which is also, registered under the U.S. Investment Advisors Act. The information and any opinions contained in this document have been compiled in good faith, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. Save to the extent (if any) that exclusion of liability is prohibited by any applicable law or regulation, Ashmore and its respective officers, employees, representatives and agents expressly advise that they shall not be liable in any respect whatsoever for any loss or damage, whether direct, indirect, consequential or otherwise however arising (whether in negligence or otherwise) out of or in connection with the contents of or any omissions from this document. This document does not constitute an offer to sell, purchase, subscribe for or otherwise invest in units or shares of any Fund referred to in this document. The value of any investment in any such Fund may fall as well as rise and investors may not get back the amount originally invested. Past performance is not a reliable indicator of future results. All prospective investors must obtain a copy of the final Scheme Particulars or (if applicable) other offering document relating to the relevant Fund prior to making any decision to invest in any such Fund. This document does not constitute and may not be relied upon as constituting any form of investment advice and prospective investors are advised to ensure that they obtain appropriate independent professional advice before making any investment in any such Fund. Funds are distributed in the United States by Ashmore Investment Management (US) Corporation, a registered broker-dealer and member of FINRA and SIPC.