The dollar is supposed to be dying. We’ve heard that argument for the better part of a decade, and it’s getting louder, not quieter. Dollar dominance isn’t fading. In fact, the events of late April 2026 just delivered the loudest counter-signal in years.

Equities extend gains as earnings and semiconductors lead markets higher. Consumer confidence remains subdued despite economic resilience. Inflation is easing gradually but remains above the Fed’s targey.

Last week’s data tracked a shifting economic trajectory over the last several months. While the latest reading on first-quarter GDP confirms the economy started the year with steady growth, subsequent inflation metrics moved higher and ultimately weighed on consumer confidence.

U.S. equities moved higher last week, with the S&P 500 advancing 0.9 percent – its eighth consecutive weekly gain and the longest such streak since 2023. The Russell 2000 fared even better, rising 2.7 percent.

Recent market volatility and the conflict in Iran have understandably pushed many emerging market investors to the sidelines. But periods of uncertainty have historically offered attractive entry points into emerging market debt (EMD), particularly when underlying fundamentals are improving and asset flows are likely to increase.

Since early April, U.S. stocks have rallied sharply despite an ongoing war, rising inflation fueled by soaring oil prices (near $100/barrel), higher bond yields (up 0.6 to 0.7 percentage points), and frothy valuations (21 times projected earnings vs. a historical average of 17 times for the S&P 500 Index).

On the surface, last week looked engineered to embarrass our positioning. The dollar index climbed to a six-week high above 99.3 by Friday and finished the week roughly flat at those levels.

California continues to demonstrate fiscal resilience, supported by strong liquidity balances and the absence of projected cash‑flow borrowing through FY 2026–27. However, Medicaid cost pressures, a progressive tax structure highly sensitive to equity market swings, and constitutional spending constraints remain key differentiators between California and other large states.

An unexpected rap on your front door is sometimes cause for anxiety. You are not sure who or what is out there, wanting to get in.

New home sales fell more than expected in April while the median price experienced its largest jump in seven years.

Treasuries rallied back to be little-changed on the day, erasing earlier declines spurred by higher oil prices, after a key US inflation gauge rose less than expected.

Bankers are preparing to sell a jumbo debt package to support the $110 billion acquisition of Warner Bros. Discovery Inc. It’s a risky deal and comes at a moment when the bond markets have been wobbling.

In a relatively light week for traditional economic data, a mix of corporate earnings, business surveys, Federal Reserve minutes, and the latest read on the consumer from the University of Michigan helped paint an increasingly clear picture for investors.

The artificial intelligence (AI) boom has transitioned from an equity market narrative to a defining force in fixed income. Hyperscalers (Amazon (AMZN), Alphabet (GOOG/L), Meta (META), Microsoft (MSFT), and Oracle (ORCL)) are shifting from internal cash flows to substantial bond issuance to fund massive data center, graphics processing unit (GPU), and power infrastructure buildouts.

Contrary to what legal television series portray, verdicts rarely turn on a single moment of drama. They take shape gradually, as evidence accumulates and a broader narrative comes into focus.

Chris Galipeau discusses high-conviction insights that go beyond media headlines.

After three decades of watching market cycles play out from both sides of the trade, I’ve come to a simple conclusion: Wall Street’s love of simple rules is one of the most dangerous aspects of investing.

Private credit is more inherently complex than the traditional bond market. In comparison, private credit information comes at a deficit. That’s because private credit loans are essentially bespoke agreements between a lender and a private borrower.

Almost two-thirds of fund managers permit some level of “nuclear exposure,” with 34% allowing investments in nuclear weaponry, according to Jefferies Financial Group Inc.’s fourth-annual ESG and defense survey.

Despite the move lower late last week, U.S. Treasury yields are still holding well above recent lows and close to highs not seen in more than a year. By contrast, risk assets are firmly bid: U.S. equities have been routinely touching new historical highs, and credit spreads over Treasuries remain tight.

The White House’s decision to take a 9.9% stake in Intel Corp. is looking like very shrewd business indeed. Since the government bought in at $20.47 a share last August, the American chipmaker’s surging stock price has delivered the US a $43 billion return.

Gold has dropped more than 11 percent from its all-time high of just over $5,102 an ounce in January, and selling pressure continues to dominate the market. A well-established mainstream narrative is driving the bearish sentiment.

Despite these higher costs, a projected 45 million Americans are expected to travel at least 50 miles from home this weekend, setting a new record. Close to 40 million will drive while some 3.7 million will fly.

Despite headwinds from rising oil prices, fundamentals have remained strong. The S&P 500 has notched 18 record highs year to date and, more importantly, surpassed our prior target of 7,250. Following a standout 1Q earnings season, we are raising our 2026 earnings per share (EPS) estimate to $326 from $300.

As Kevin Warsh takes the helm at the Federal Reserve, bond investors are betting he’ll prioritize the central bank’s inflation-fighting credibility over President Donald Trump’s push for lower interest rates.

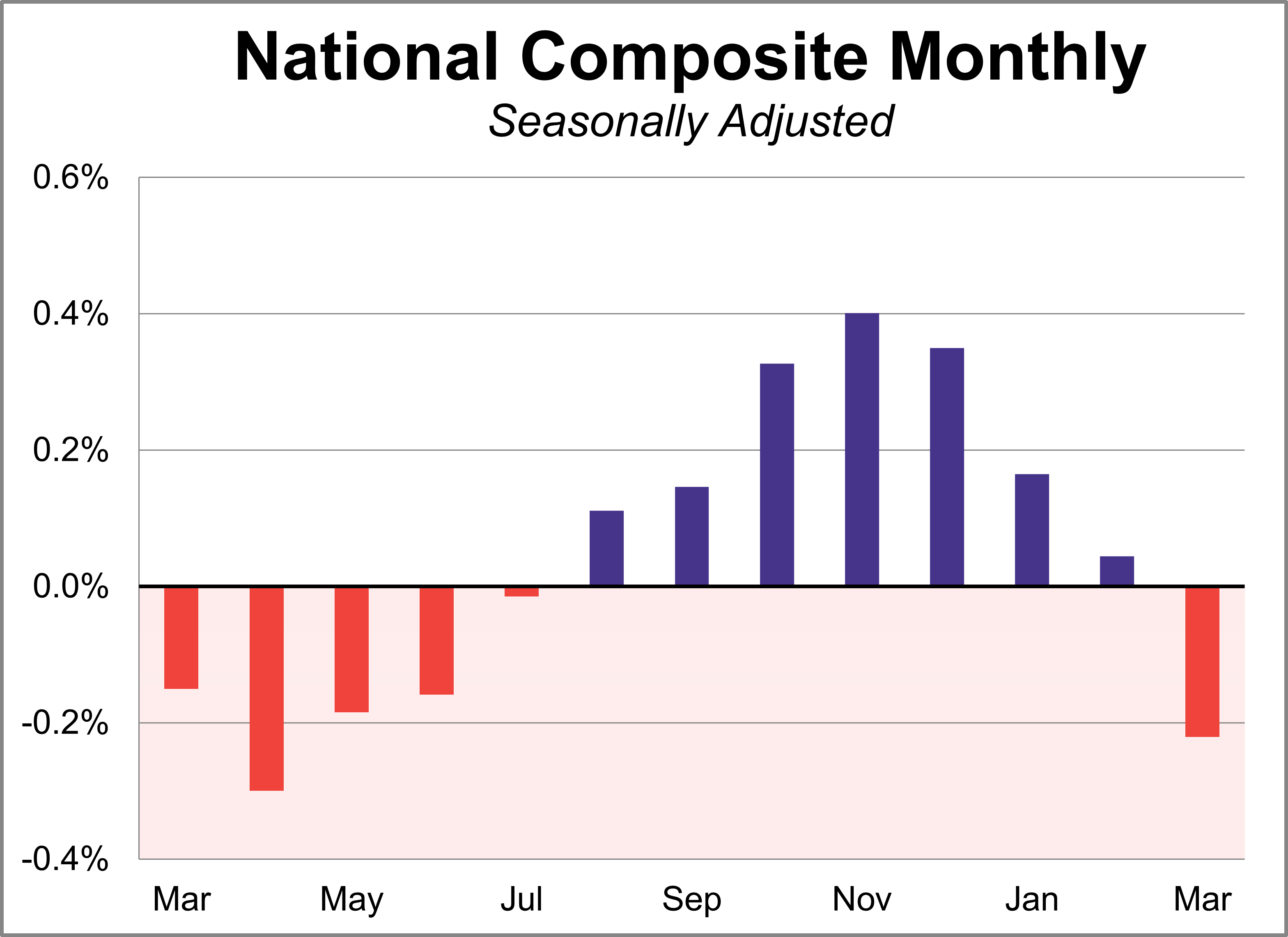

Home prices fell for the first time in eight months in March according to the S&P Cotality Case-Shiller index, as the housing slowdown intensifies. On a seasonally adjusted basis, the national index dropped 0.2% month-over-month and was up 0.7% year-over-year, the slowest pace since June 2023.

Last Friday closed with the 10-year Treasury yield at 4.60%, a one-year high, and the doom commentary about rising interest rates was waiting before the bell even rang. Hyperinflation. Bond market breakdown. Paradigm shift. A 1981 fair-value retest.

I have often written about one of the few indicators in economics that has earned its reputation over the years, and for good reason. It has preceded virtually every US recession since World War II. I’m talking about the inverted yield curve.

Now, that prospect feels much farther off. Indeed, as government debt grows and macroeconomic pressures and inflation reemerge, investors face a complicated rate environment. Dividends can provide a solution.

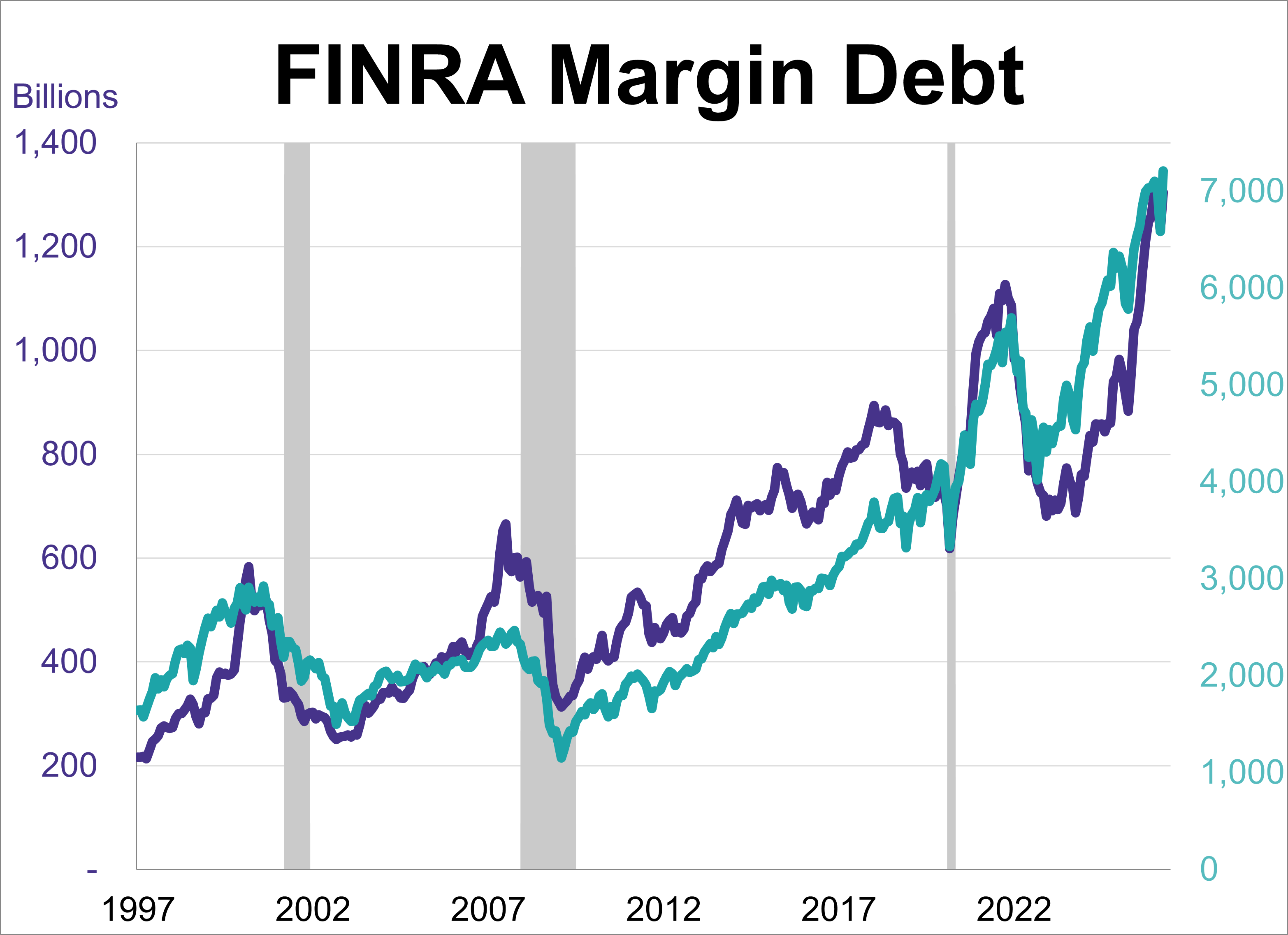

There is currently a stark contrast between everyday consumer confidence and financial market behavior. On one hand, persistent inflation and elevated living costs have driven consumer sentiment to historic lows. On the other hand, financial market participants are exhibiting aggressive risk appetite, with margin debt surging to an all-time high record on the heels of major equity market gains.

In this second quarter update, Western Asset believes global fixed-income markets face a more complex backdrop as geopolitics, rapid AI adoption and private credit scrutiny intersect.

For private equity firms, capital flexibility is prized today. Merger-and-acquisition (M&A) activity has cooled, while commodity prices and artificial intelligence (AI)-driven disruption have heated up, creating uncertainty for investors. This makes it more challenging to sell portfolio companies, so private equity firms are holding investments longer. As a result, many firms are turning to net asset value (NAV) loans for capital needs.

By moving beyond benchmark constraints, active portfolios can access off-the-run bonds, specific securitized tranches, and maturity buckets with superior risk-reward profiles. They also have the flexibility to adjust positioning throughout the market cycle — reallocating across sectors, ratings, and issuers as conditions evolve to capture opportunities and mitigate drawdowns.

I still don’t think the Fed is close to a rate hike, but for the upcoming June FOMC meeting, a shift in the language of the policy statement from an easing bias to one of a ‘balanced’ outlook seems to be the most likely scenario. However, the fed funds futures market has now fully priced in a rate hike for March 2027, a remarkable shift from its pre-war status of discounting almost three rate cuts for the same timeframe.

US stocks advanced as investors struck an upbeat tone ahead of a long holiday weekend, with optimism fueled by hopes for resolution of hostilities in the Middle East, resilient economic data and relentless enthusiasm for artificial intelligence-linked trades.

Global bond yields are reaching frightening levels due to the continued war in Iran and the effective closure of the Strait of Hormuz. Continued high oil prices and the threat of reverberating inflation are causing investors to demand higher yields on government bonds.

Hedge funds have been selling the scorching rally in US semiconductor stocks to book profits, while keeping their overall exposure to the AI theme, according to traders at Goldman Sachs Group Inc.

Equities advanced in April, but hedges remain few and far between, as traditional risk mitigants like bonds and gold continue to show a correlation with stocks.

There’s a whiff of panic among investors these days. US Treasury yields have climbed to levels unseen in more than a year at the same time as a furious rally has left stocks near all-time highs. Surely, both moves can’t coexist for long, goes the narrative.

Najimah Roberson, a lifelong renter, spent the past two years searching around Harrisburg, Pennsylvania, for a home she could afford — getting outbid nearly 30 times along the way.

The exchange-traded fund marketplace continues to expand. Now with more than $20 trillion in assets under management ($14 trillion in the U.S., growing at an 18% five-year annualized clip), 2026’s volatility and emerging investment themes have taken the universe to new heights.

Inflation surged higher in April, with the Consumer Price Index (CPI) jumping 3.8 per cent from 3.3 per cent in March and the Producer Price Index (PPI) up six per cent from four per cent in March. The increase in the CPI owed much to energy and food prices.

Margin debt rose for the first time in three months to a record high in April, coming in at $1.30 trillion. This marked a 6.8% increase from March and a 53.3% rise compared to the previous year.

Although a lot has changed since our last quarterly, its central theme – dispersion – feels like it’s only become more pronounced. We wrote last time that ‘‘we believe we’re entering a new era of dispersion in the performance of financial assets.’’

On Friday, May 15, the 10-year Treasury yield closed at 4.59%, its highest level since February 2025. The 30-year Treasury yield closed near 5.12%, a level last seen in 2007. Those are significant moves because they reflect a repricing of the market’s inflation, growth, and Federal Reserve expectations.

That Buffett cash hoard has also created a lot of speculation, innuendo, and assumptions, which is what I want to walk through in today’s discussion. Primarily, what that cash hoard actually represents, the popular theories explaining it, and what it really costs shareholders to hold.

Markets ended last week under pressure as the optimism that had been building around a potential geopolitical breakthrough faded quickly. The China summit did not deliver the progress that had been hoped for. The Boeing aircraft order was smaller than expected; there was no meaningful movement on Iran; the Taiwan issue was brought forward in a way that unsettled markets; and the hoped-for easing of tensions around the Strait of Hormuz did not materialize.

Emerging market debt is compelling as a medium‑term structural allocation, particularly for investors seeking to diversify away from concentrated U.S. exposures.

Tax-equivalent yields on high-quality munis are hitting 7% to 9%. Discover how WisdomTree ETFs, WTMU and WTMY, exploit the steep yield curve.