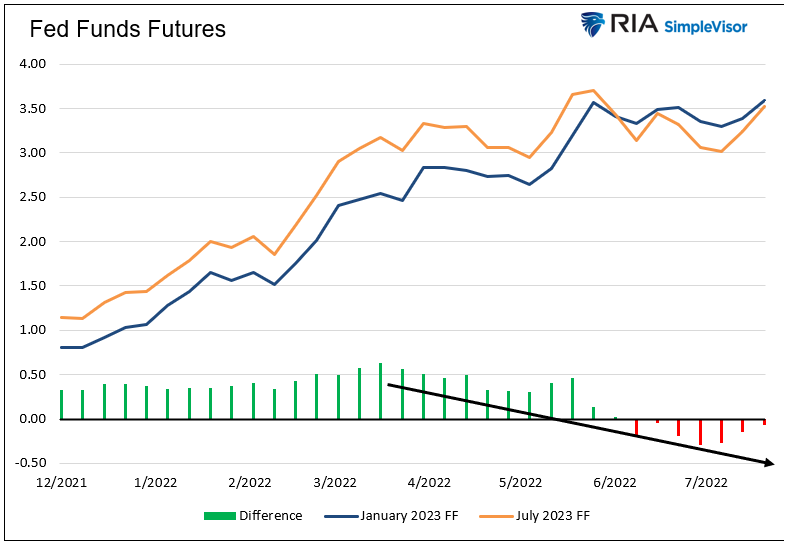

The latest data shows inflation is still with us at an 8.5% annual rate. That means we can expect the Fed to keep tightening, trying to reduce demand and relieve pressure on consumer prices.

With interest rates now hovering around 5%, existing-home sales are down more than 14% from last year. Some potential buyers are sitting on the sidelines until rates or prices or both decline, while sellers are hoping the market picks up again so they can get a higher price.

U.S. stocks are moving upward, continuing yesterday's rally, as the markets digest the release of the Producer Price Index.

Stocks are rallying on hopes the Fed will stop increasing interest rates this fall, pivot, and start reducing them next year. Investors are blindly buying into this pivot narrative.

If you have an aversion to the mathematics that go with the bond market, you’re not alone. It’s complicated and counter-intuitive, based in concepts that are hard to visualize.

US inflation decelerated in July by more than expected, reflecting lower energy prices, which may take some pressure off the Federal Reserve to continue aggressively hiking interest rates.

Most consumers wait for things to go on sale before buying them, look for promo codes prior to purchasing something online, and suggest that discounts are the greatest influence on their purchase decisions around the holidays...

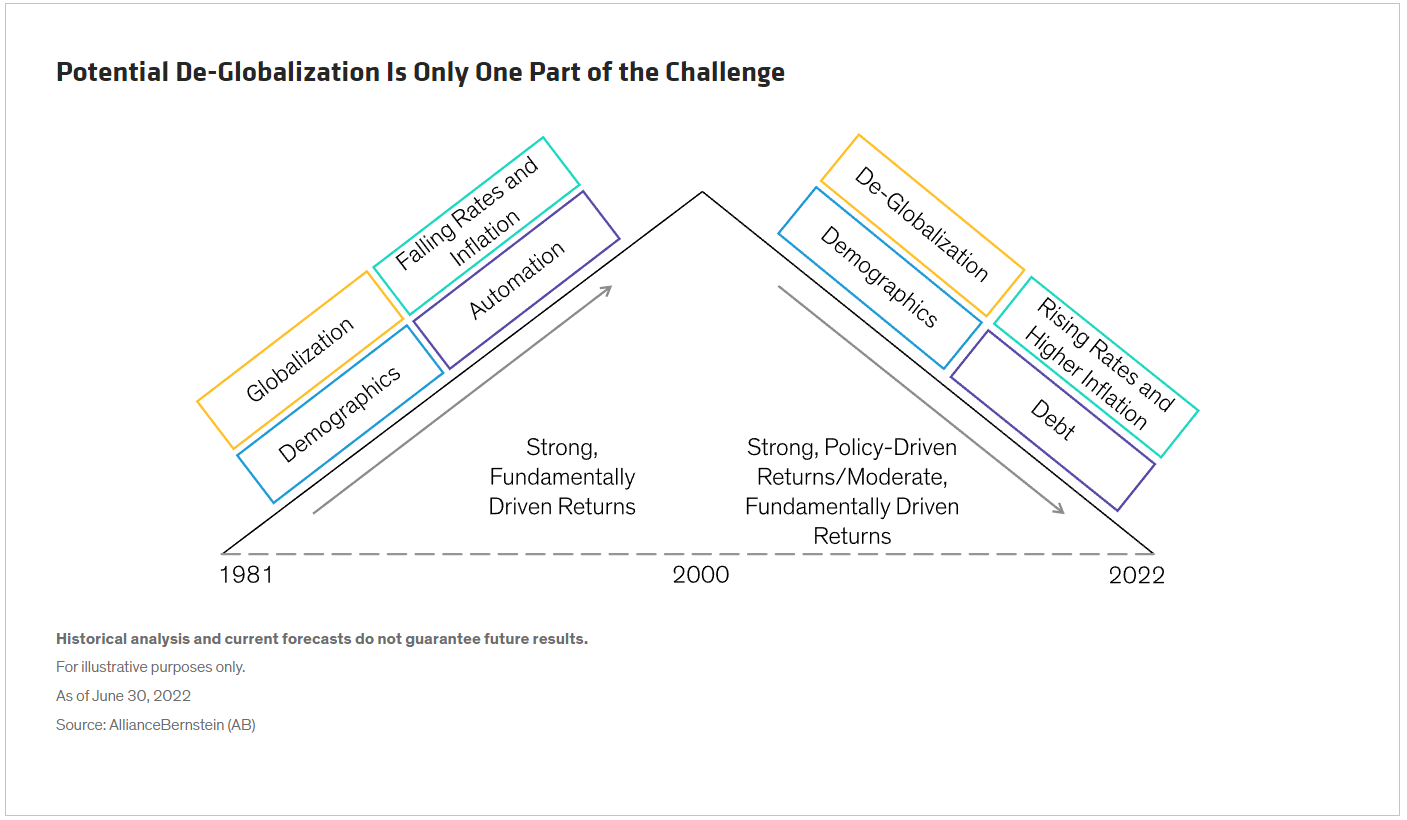

For decades, relative global stability, sound economic-policy management, and the steady expansion of trade to and from emerging markets combined to keep costs down.

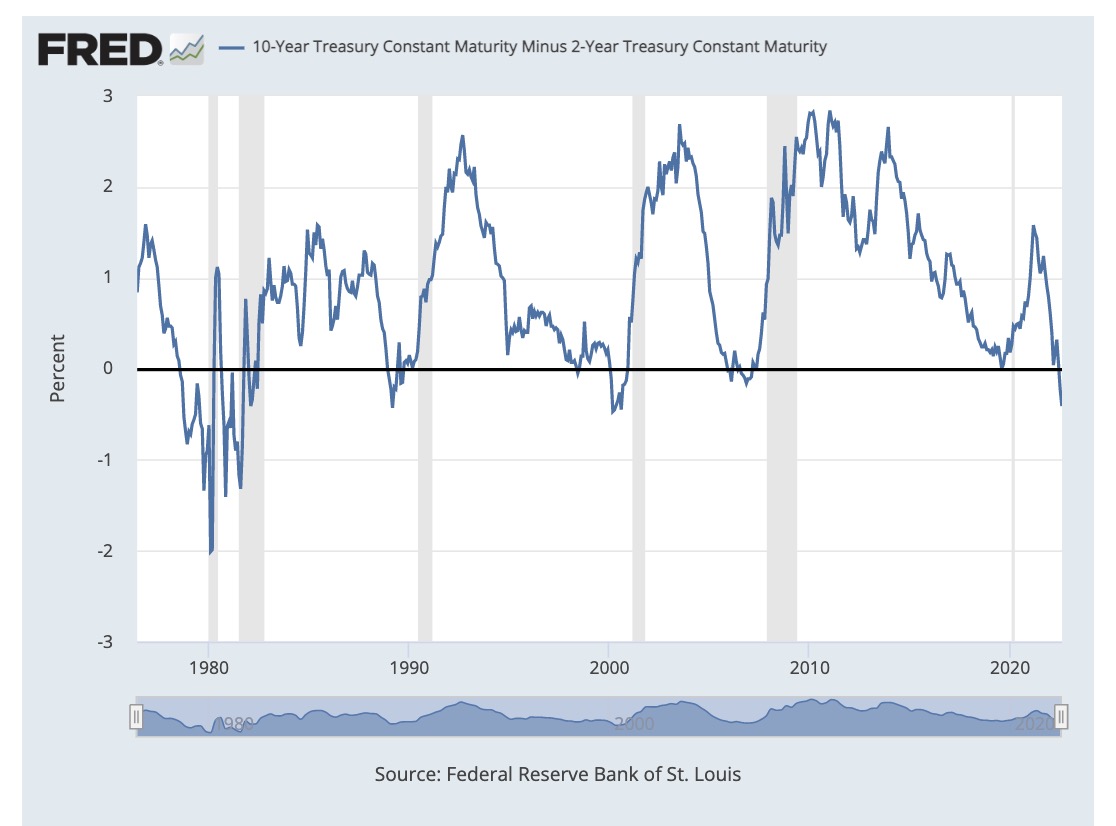

The bond market’s yield curve has a sort of mythical hold on economists and investors. It’s easy to see why, given that every recession since the 1950s has been preceded by an inverted curve, which happens when short-term rates rise above long-term ones.

U.S. stocks are trading mixed in pre-market action, with the markets anticipating tomorrow's start of a flood of July inflation data.

Corporate fundamentals have been deteriorating in the US. Over the past six months we have seen meaningful erosion in profit margins, pricing power and the outlook for credit.

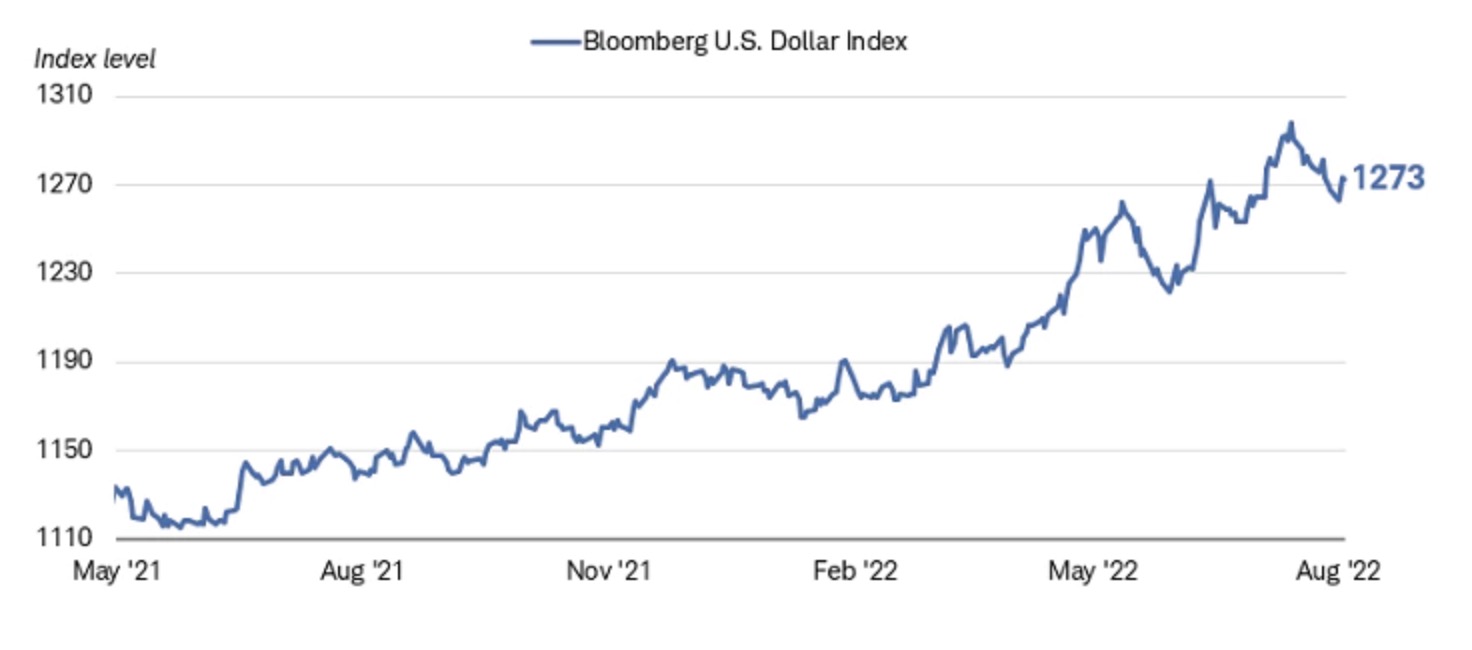

A trifecta of factors support the dollar, including the relatively strong performance of the U.S. economy, tightening monetary policy by the Federal Reserve, and safe-haven buying.

Gold, according to financial markets lore, is a pretty simple beast.

Meta Platforms Inc., one of the few S&P 500 companies without debt, is selling $10 billion in its first ever corporate bond sale as its cash flow and stock price fall.

The tight labor market probably didn’t get the US into this inflationary mess, but it is part of the reason that it’s going to be so hard to get out of it.

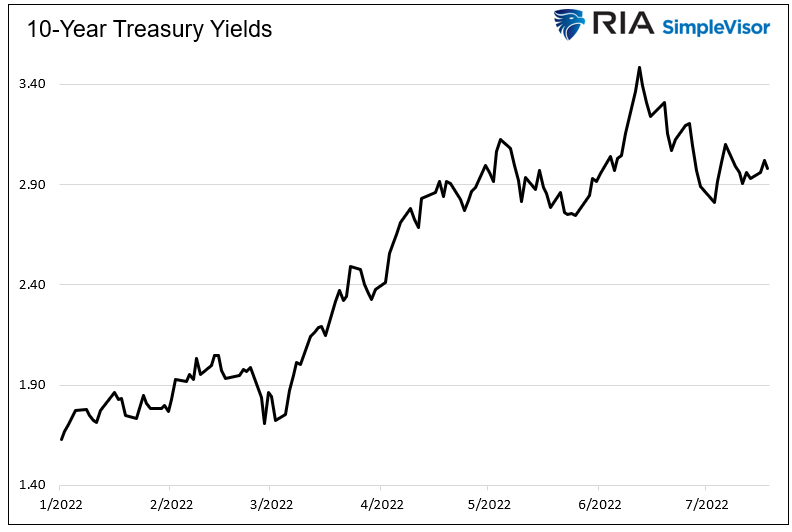

Treasury yields surged on stronger-than-expected US employment data that shore up the case for additional hefty central bank interest-rate increases.

As of last month, the U.S. jobs market fully recouped the number of jobs that were lost due to the pandemic, in less than half the time it took following the previous downturn.

US employers added more than double the number of jobs forecast, illustrating rock-solid labor demand that tempers recession worries and suggests the Federal Reserve will press on with steep interest-rate hikes to thwart inflation.

For some reason, people are feeling good. Animal spirits are on the run.

Across US indexes, growth has experienced a resurgence relative to value off the June 17, 2022 low.

The latest signs of life from corporate bond issuers sure don’t signal a market that’s in a recession.

When it comes to the economy, so-called soft landings are as rare as sightings of Halley’s comet.

Concerns regarding inflation are almost everywhere you look—unless you happen to be looking at the Treasury bond market.

After the US saw inflation hit its highest levels in 40 years (since the bond bull market started), fueling bets that the Federal Reserve would embark on the most aggressive tightening campaign in a generation, it seemed that the bear market had finally started.

U.S. equities finished mixed in choppy trading amid a host of data, events and cautious Fedspeak driving sentiment.

We met with the portfolio managers of BlackRock Strategic Income Opportunities to have a wide-ranging discussion on their approach and why it’s so well suited to the current market environment.

July was an illustration of the adage that “the market is not the economy.” US stocks had their best month in two years while the economy received discouraging news about both growth and inflation.

Bond bulls, while savoring a stellar rebound in returns fueled by growing recession fears, are braced for potential setbacks.

Necessity is the mother of invention, so they say. And in this case, stupidity is as well.

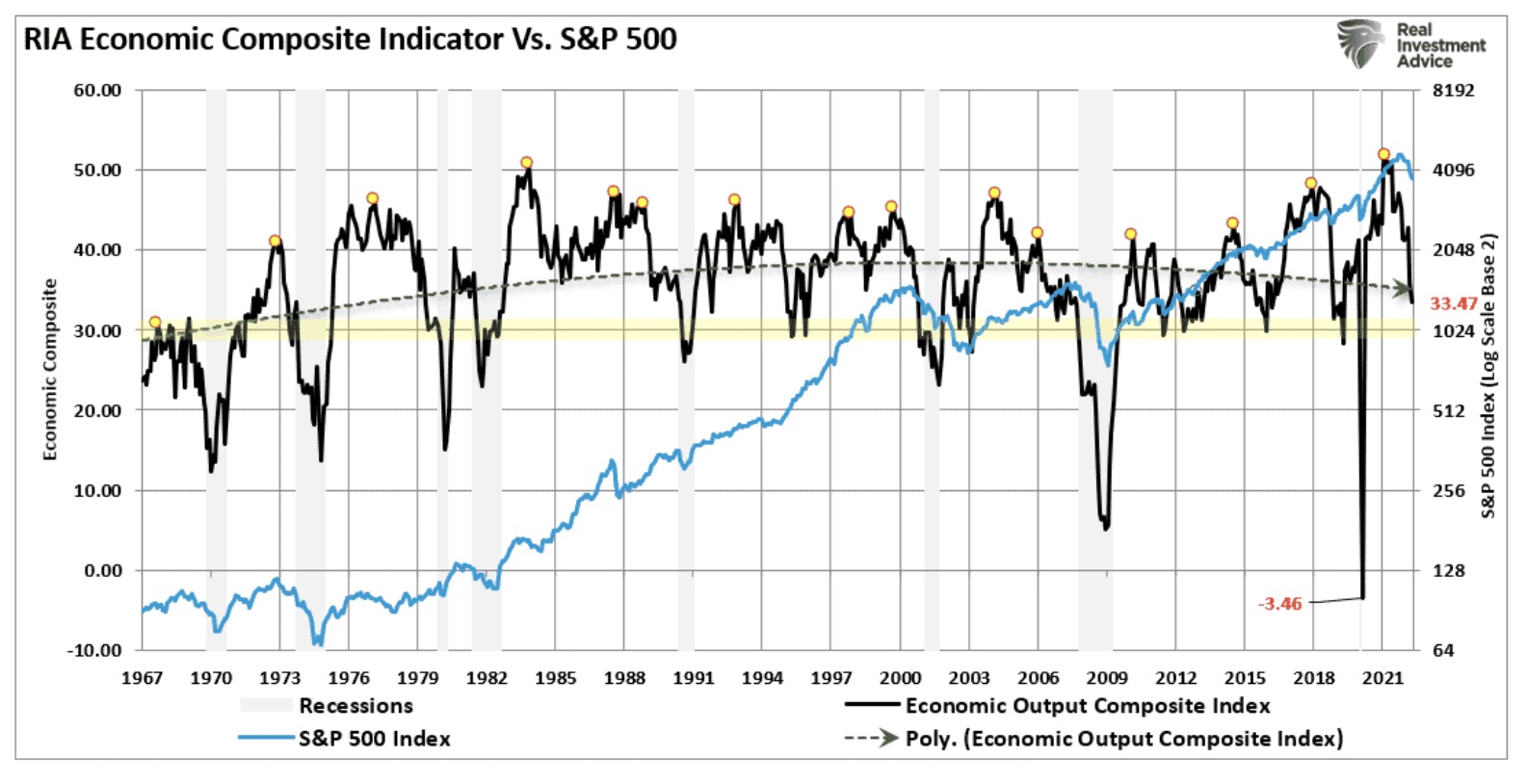

No recession.

Two key US inflation gauges posted larger-than-forecast increases on Friday, heightening concerns that prices will remain persistently high and prompt continued aggressive interest-rate increases from the Federal Reserve.

US consumer spending barely rose in June after falling in the prior month, underscoring how decades-high inflation has eroded Americans’ paychecks and tempered demand.

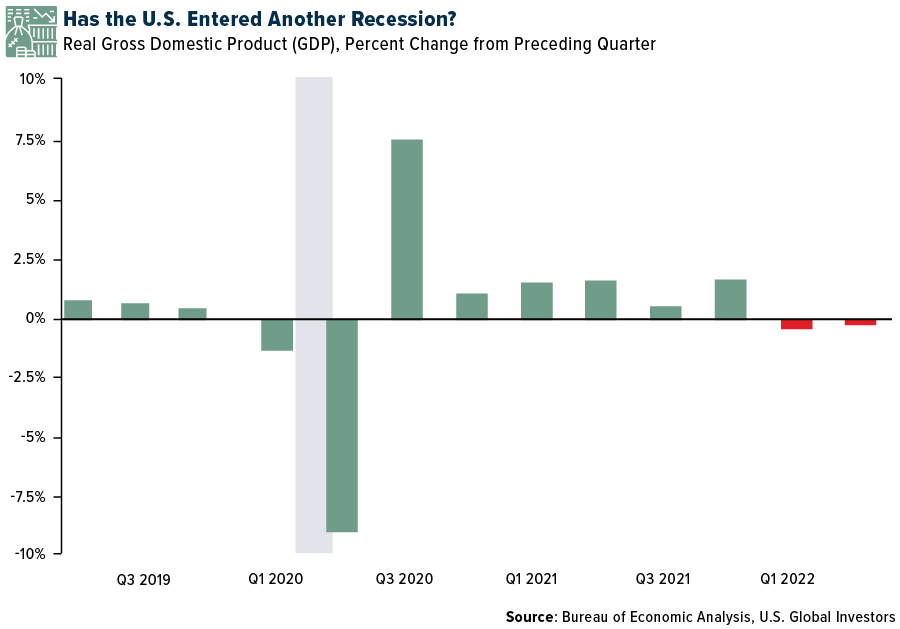

So did the U.S. just enter a recession? It depends on who you ask.

The market’s inflation concerns are taking a back seat to recession fears.

Gold climbed after the US economy shrank for a second consecutive quarter, pushing the dollar and Treasury yields lower, and clouding the outlook for further aggressive interest-rate hikes as the Federal Reserve fights inflation.

The US economy shrank for a second straight quarter, raising chances of a recession, as decades-high inflation undercut consumer spending and Federal Reserve interest-rate hikes stymied business investment and housing demand.

U.S. stocks are trading higher as the Street is reacting positively to softer-than-expected earnings results from some key companies.

Since the COVID low in US Treasury rates and subsequent rise, the Japanese Yen has tracked the yield differential between the US and Japan.

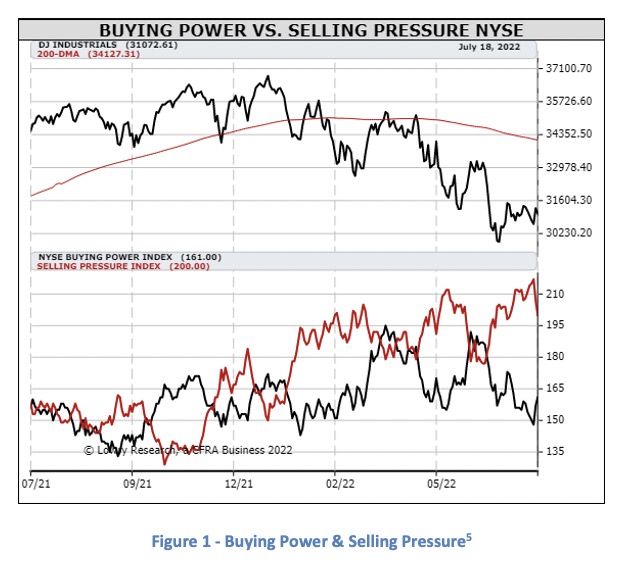

In downward trending markets as we have seen for much of 2022, it is important to distinguish price declines which may present similarly.

The biggest stock-bond rally in more than two decades has just raised the ante for investors betting Jerome Powell will send somewhat dovish signals at Wednesday’s high-stakes policy decision.

Howard Marks’s latest memo argues that investors seeking superior performance must have the courage to depart from the pack, even though doing so means accepting the risk of being wrong. Thinking differently and better than others is key to outperformance, he explains, because in investing, it’s not enough to be right.

U.S. equities finished higher last week (S&P 500 +2.6%) as Treasury yields fell and growth nicely outperformed value. 2Q earnings are coming in less bad than feared.

he Federal Reserve’s interest-rate hikes are wearing out their welcome in bond markets, with a measure of the yield curve that Chair Jerome Powell has highlighted as a recession indicator sending out a warning message.

What drove the U.S. dollar's surge, and can it last?

Our last two quarterly letters conveyed a cautious attitude regarding both the economy and financial markets. The cautious season persists this quarter.

During Tesla’s quarterly results webcast this week, Musk admitted to dumping some $936 million of Bitcoin to raise cash out of concern of an economic pullback due to pandemic lockdowns in China.

U.S. stocks are mixed in a subdued session to close out the week, but remain on target for a sharp weekly advance.

The Fed’s most pressing concerns are to not only reverse its monetary excess and misjudgment of inflation, but also to instill confidence that they will follow important provisions of the Federal Reserve Acts.

For decades, globalization has been on an inexorable rise, a key pillar fueling economic growth, driving inflation and yields down, bolstering corporate profit margins and supporting an upward climb in market valuations. Over the past few years, though, cracks have started to develop in globalization, as populism has seen a resurgence and trade wars have erupted.

We all know that the world as a whole suffered from a pandemic, and is now suffering inflation in its aftermath. But the ECB has to deal with three pressures that don’t affect the Federal Reserve.