I’ve written many times about having joined the investment industry in 1969, when the “Nifty Fifty” stocks were in full flower. My first employer, First National City Bank, as well as many of the other “money-center banks” (the leading investment managers of the day), were enthralled with these companies, with their powerful business models and flawless prospects. Sentiment surrounding their stocks was uniformly positive, and portfolio managers found great safety in numbers. For example, a common refrain at the time was “you can’t be fired for buying IBM,” the era’s quintessential growth company.

I’ve also written extensively about the fate of these stocks. In 1973-74, the OPEC oil embargo and the resultant recession took the S&P 500 Index down a total of 47%. And many of the Nifty Fifty, for which it had been thought that “no price was too high,” did far worse, falling from peak p/e ratios of 60-90 to trough multiples in the single digits. Thus, their devotees lost almost all of their money in the stocks of companies that “everyone knew” were great. This was my first chance to see what can happen to assets that are on what I call “the pedestal of popularity.”

In 1978, I was asked to move to the bank’s bond department to start funds in convertible bonds and, shortly thereafter, high yield bonds. Now I was investing in securities most fiduciaries considered “uninvestable” and which practically no one knew about, cared about, or deemed desirable . . . and I was making money steadily and safely. I quickly recognized that my strong performance resulted in large part from precisely that fact: I was investing in securities that practically no one knew about, cared about, or deemed desirable. This brought home the key money-making lesson of the Efficient Market Hypothesis, which I had been introduced to at the University of Chicago Business School: If you seek superior investment results, you have to invest in things that others haven’t flocked to and caused to be fully valued. In other words, you have to do something different.

The Essential Difference

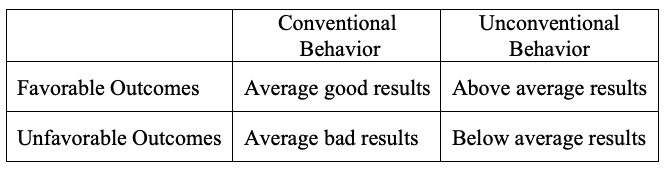

In 2006, I wrote a memo called Dare to Be Great. It was mostly about having high aspirations, and it included a rant against conformity and investment bureaucracy, as well as an assertion that the route to superior returns by necessity runs through unconventionality. The element of that memo that people still talk to me about is a simple two-by-two matrix:

Here’s how I explained the situation:

Of course, it’s not easy and clear-cut, but I think it’s the general situation. If your behavior and that of your managers is conventional, you’re likely to get conventional results – either good or bad. Only if the behavior is unconventional is your performance likely to be unconventional . . . and only if the judgments are superior is your performance likely to be above average.

The consensus opinion of market participants is baked into market prices. Thus, if investors lack insight that is superior to the average of the people who make up the consensus, they should expect average risk-adjusted performance.

Many years have passed since I wrote that memo, and the investing world has gotten a lot more sophisticated, but the message conveyed by the matrix and the accompanying explanation remains unchanged. Talk about simple – in the memo, I reduced the issue to a single sentence: “This just in: You can’t take the same actions as everyone else and expect to outperform.”

The best way to understand this idea is by thinking through a highly logical and almost mathematical process (greatly simplified, as usual, for illustrative purposes):

- A certain (but unascertainable) number of dollars will be made over any given period by all investors collectively in an individual stock, a given market, or all markets taken together. That amount will be a function of (a) how companies or assets fare in fundamental terms (e.g., how their profits grow or decline) and (b) how people feel about those fundamentals and treat asset prices.

- On average, all investors will do average.

- If you’re happy doing average, you can simply invest in a broad swath of the assets in question, buying some of each in proportion to its representation in the relevant universe or index. By engaging in average behavior in this way, you’re guaranteed average performance. (Obviously, this is the idea behind index funds.)

- If you want to be above average, you have to depart from consensus behavior. You have to overweight some securities, asset classes, or markets and underweight others. In other words, you have to do something different.

- The challenge lies in the fact that (a) market prices are the result of everyone’s collective thinking and (b) it’s hard for any individual to consistently figure out when the consensus is wrong and an asset is priced too high or too low.

-

Nevertheless, “active investors” place active bets in an effort to be above average.

- Investor A decides stocks as a whole are too cheap, and he sells bonds in order to overweight stocks. Investor B thinks stocks are too expensive, so she moves to an underweighting by selling some of her stocks to Investor A and putting the proceeds into bonds.

- Investor X decides a certain stock is too cheap and overweights it, buying from investor Y, who thinks it’s too expensive and therefore wants to underweight it.

- It’s essential to note that in each of the above cases, one investor is right and the other is wrong. Now go back to the first bullet point above: Since the total dollars earned by all investors collectively are fixed in amount, all active bets, taken together, constitute a zero-sum game (or negative-sum after commissions and other costs). The investor who’s right earns an above average return, and by definition the one who’s wrong earns a below average return.

- Thus, every active bet placed in the pursuit of above average returns carries with it the risk of below average returns. There’s no way to make an active bet such that you’ll win if it works but not lose if it doesn’t. Financial innovations are often described as offering some version of this impossible bargain, but they invariably fail to live up to the hype.

- The bottom line of the above is simple: You can’t hope to earn above average returns if you don’t place active bets, but if your active bets are wrong, your return will be below average.

Investing strikes me as being very much like golf, where playing conditions and the performance of competitors can change from day to day, as can the placement of the holes. On some days, one approach to the course is appropriate, but on other days, different tactics are called for. To win, you have to either do a better job than others of selecting your approach or executing on it, or both.

The same is true for investors. It’s simple: If you hope to distinguish yourself in terms of performance, you have to depart from the pack. But, having departed, the difference will only be positive if your choice of strategies and tactics is correct and/or you’re able to execute better.

Second-Level Thinking

In 2009, when Columbia Business School Publishing was considering whether to publish my book The Most Important Thing, they asked to see a sample chapter. As has often been my experience, I sat down and described a concept I hadn’t previously written about or named. That description became the book’s first chapter, addressing one of its most important topics: second-level thinking. It’s certainly the concept from the book that people ask me about most often.

The idea of second-level thinking builds on what I wrote in Dare to Be Great. First, I repeated my view that success in investing means doing better than others. All active investors (and certainly money managers hoping to earn a living) are driven by the pursuit of superior returns.

But that universality also makes beating the market a difficult task. Millions of people are competing for each dollar of investment gain. Who’ll get it? The person who’s a step ahead. In some pursuits, getting up to the front of the pack means more schooling, more time in the gym or the library, better nutrition, more perspiration, greater stamina or better equipment. But in investing, where these things count for less, it calls for more perceptive thinking . . . at what I call the second level.

The basic idea behind second-level thinking is easily summarized: In order to outperform, your thinking has to be different and better.

Remember, your goal in investing isn’t to earn average returns; you want to do better than average. Thus, your thinking has to be better than that of others – both more powerful and at a higher level. Since other investors may be smart, well informed and highly computerized, you must find an edge they don’t have. You must think of something they haven’t thought of, see things they miss, or bring insight they don’t possess. You have to react differently and behave differently. In short, being right may be a necessary condition for investment success, but it won’t be sufficient. You have to be more right than others . . . which by definition means your thinking has to be different.

Having made the case, I went on to distinguish second-level thinkers from those who operate at the first level:

First-level thinking is simplistic and superficial, and just about everyone can do it (a bad sign for anything involving an attempt at superiority). All the first-level thinker needs is an opinion about the future, as in “The outlook for the company is favorable, meaning the stock will go up.”

Second-level thinking is deep, complex, and convoluted. The second-level thinker takes a great many things into account:

-

-

- What is the range of likely future outcomes?

- What outcome do I think will occur?

- What’s the probability I’m right?

- What does the consensus think?

- How does my expectation differ from the consensus?

- How does the current price for the asset comport with the consensus view of the future, and with mine?

- Is the consensus psychology that’s incorporated in the price too bullish or bearish?

- What will happen to the asset’s price if the consensus turns out to be right, and what if I’m right?

-

The difference in workload between first-level and second-level thinking is clearly massive, and the number of people capable of the latter is tiny compared to the number capable of the former.

First-level thinkers look for simple formulas and easy answers. Second-level thinkers know that success in investing is the antithesis of simple.

Speaking about difficulty reminds me of an important idea that arose in my discussions with my son Andrew during the pandemic (described in the memo Something of Value, published in January 2021). In the memo’s extensive discussion of how efficient most markets have become in recent decades, Andrew makes a terrific point: “Readily available quantitative information with regard to the present cannot be the source of superior performance.” After all, everyone has access to this type of information – with regard to public U.S. securities, that’s the whole point of the SEC’s Reg FD (for fair disclosure) – and nowadays all investors should know how to manipulate data and run screens.

So, then, how can investors who are intent on outperforming hope to reach their goal? As Andrew and I said on a podcast where we discussed Something of Value, they have to go beyond readily available quantitative information with regard to the present. Instead, their superiority has to come from an ability to:

- better understand the significance of the published numbers,

- better assess the qualitative aspects of the company, and/or

- better divine the future.

Obviously, none of these things can be determined with certainty, measured empirically, or processed using surefire formulas. Unlike present-day quantitative information, there’s no source you can turn to for easy answers. They all come down to judgment or insight. Second-level thinkers who have better judgment are likely to achieve superior returns, and those who are less insightful are likely to generate inferior performance.

This all leads me back to something Charlie Munger told me around the time The Most Important Thing was published: “It’s not supposed to be easy. Anyone who finds it easy is stupid.” Anyone who thinks there’s a formula for investing that guarantees success (and that they can possess it) clearly doesn’t understand the complex, dynamic, and competitive nature of the investing process. The prize for superior investing can amount to a lot of money. In the highly competitive investment arena, it simply can’t be easy to be the one who pockets the extra dollars.

Contrarianism

There’s a concept in the investing world that’s closely related to being different: contrarianism. “The investment herd” refers to the masses of people (or institutions) that drive security prices one way or the other. It’s their actions that take asset prices to bull market highs and sometimes bubbles and, in the other direction, to bear market territory and occasional crashes. At these extremes, which are invariably overdone, it’s essential to act in a contrary fashion.

Joining in the swings described above causes people to own or buy assets at high prices and to sell or fail to buy at low prices. For this reason, it can be important to part company with the herd and behave in a way that’s contrary to the actions of most others.

Contrarianism received its own chapter in The Most Important Thing. Here’s how I set forth the logic:

- Markets swing dramatically, from bullish to bearish, and from overpriced to underpriced.

- Their movements are driven by the actions of “the crowd,” “the herd,” and “most people.” Bull markets occur because more people want to buy than sell, or the buyers are more highly motivated than the sellers. The market rises as people switch from being sellers to being buyers, and as buyers become even more motivated and the sellers less so. (If buyers didn’t predominate, the market wouldn’t be rising.)

- Market extremes represent inflection points. These occur when bullishness or bearishness reaches a maximum. Figuratively speaking, a top occurs when the last person who will become a buyer does so. Since every buyer has joined the bullish herd by the time the top is reached, bullishness can go no further, and the market is as high as it can go. Buying or holding is dangerous.

- Since there’s no one left to turn bullish, the market stops going up. And if the next day one person switches from buyer to seller, it will start to go down.

- So at the extremes, which are created by what “most people” believe, most people are wrong.

- Therefore, the key to investment success has to lie in doing the opposite: in diverging from the crowd. Those who recognize the errors that others make can profit enormously from contrarianism.

To sum up, if the extreme highs and lows are excessive and the result of the concerted, mistaken actions of most investors, then it’s essential to leave the crowd and be a contrarian.

In his 2000 book, Pioneering Portfolio Management, David Swensen, the former chief investment officer of Yale University, explained why investing institutions are vulnerable to conformity with current consensus belief and why they should instead embrace contrarianism. (For more on Swensen’s approach to investing, see “A Case in Point” below.) He also stressed the importance of building infrastructure that enables contrarianism to be employed successfully:

Unless institutions maintain contrarian positions through difficult times, the resulting damage imposes severe financial and reputational costs on the institution.

Casually researched, consensus-oriented investment positions provide little prospect for producing superior results in the intensely competitive investment management world.

Unfortunately, overcoming the tendency to follow the crowd, while necessary, proves insufficient to guarantee investment success . . . While courage to take a different path enhances chances for success, investors face likely failure unless a thoughtful set of investment principles undergirds the courage.

Before I leave the subject of contrarianism, I want to make something else very clear. First-level thinkers – to the extent they’re interested in the concept of contrarianism – might believe contrarianism means doing the opposite of what most people are doing, so selling when the market rises and buying when it falls. But this overly simplistic definition of contrarianism is unlikely to be of much help to investors. Instead, the understanding of contrarianism itself has to take place at a second level.

In The Most Important Thing Illuminated, an annotated edition of my book, four professional investors and academics provided commentary on what I had written. My good friend Joel Greenblatt, an exceptional equity investor, provided a very apt observation regarding knee-jerk contrarianism: “. . . just because no one else will jump in front of a Mack truck barreling down the highway doesn’t mean that you should.” In other words, the mass of investors aren’t wrong all the time, or wrong so dependably that it’s always right to do the opposite of what they do. Rather, to be an effective contrarian, you have to figure out:

- what the herd is doing;

- why it’s doing it;

- what’s wrong, if anything, with what it’s doing; and

- what you should do about it.

Like the second-level thought process laid out in bullet points on page four, intelligent contrarianism is deep and complex. It amounts to much more than simply doing the opposite of the crowd. Nevertheless, good investment decisions made at the best opportunities – at the most overdone market extremes – invariably include an element of contrarian thinking.

The Decision to Risk Being Wrong

There are only so many topics I find worth writing about, and since I know I’ll never know all there is to know about them, I return to some from time to time and add to what I’ve written previously. Thus, in 2014, I followed up on 2006’s Dare to Be Great with a memo creatively titled Dare to Be Great II. To begin, I repeated my insistence on the importance of being different:

If your portfolio looks like everyone else’s, you may do well, or you may do poorly, but you can’t do different. And being different is absolutely essential if you want a chance at being superior. . . .

I followed that with a discussion of the challenges associated with being different:

Most great investments begin in discomfort. The things most people feel good about – investments where the underlying premise is widely accepted, the recent performance has been positive, and the outlook is rosy – are unlikely to be available at bargain prices. Rather, bargains are usually found among things that are controversial, that people are pessimistic about, and that have been performing badly of late.

But then, perhaps most importantly, I took the idea a step further, moving from daring to be different to its natural corollary: daring to be wrong. Most investment books are about how to be right, not the possibility of being wrong. And yet, the would-be active investor must understand that every attempt at success by necessity carries with it the chance for failure. The two are absolutely inseparable, as I described at the top of page three.

In a market that is even moderately efficient, everything you do to depart from the consensus in pursuit of above average returns has the potential to result in below average returns if your departure turns out to be a mistake. Overweighting something versus underweighting it; concentrating versus diversifying; holding versus selling; hedging versus not hedging – these are all double-edged swords. You gain when you make the right choice and lose when you’re wrong.

One of my favorite sayings came from a pit boss at a Las Vegas casino: “The more you bet, the more you win when you win.” Absolutely inarguable. But the pit boss conveniently omitted the converse: “The more you bet, the more you lose when you lose.” Clearly, those two ideas go together.

In a presentation I occasionally make to institutional clients, I employ PowerPoint animation to graphically portray the essence of this situation:

- A bubble drops down, containing the words “Try to be right.” That’s what active investing is all about. But then a few more words show up in the bubble: “Run the risk of being wrong.” The bottom line is that you simply can’t do the former without also doing the latter. They’re inextricably intertwined.

- Then another bubble drops down, with the label “Can’t lose.” There are can’t-lose strategies in investing. If you buy T-bills, you can’t have a negative return. If you invest in an index fund, you can’t underperform the index. But then two more words appear in the second bubble: “Can’t win.” People who use can’t-lose strategies by necessity surrender the possibility of winning. T-bill investors can’t earn more than the lowest of yields. Index fund investors can’t outperform.

- And that brings me to the assignment I imagine receiving from unenlightened clients: “Just apply the first set of words from each bubble: Try to outperform while employing can’t-lose strategies.” But that combination happens to be unavailable.

The above shows that active investing carries a cost that goes beyond commissions and management fees: heightened risk of inferior performance. Thus, every investor has to make a conscious decision about which course to follow. Pursue superior returns at the risk of coming in behind the pack, or hug the consensus position and ensure average performance. It should be clear that you can’t hope to earn superior returns if you’re unwilling to bear the risk of sub-par results.

And that brings me to my favorite fortune cookie, which I received with dessert 40-50 years ago. The message inside was simple: The cautious seldom err or write great poetry. In my college classes in Japanese studies, I learned about the koan, which Oxford Languages defines as “a paradoxical anecdote or riddle, used in Zen Buddhism to demonstrate the inadequacy of logical reasoning and to provoke enlightenment.” I think of my fortune that way because it raises a question I find paradoxical and capable of leading to enlightenment.

But what does the fortune mean? That you should be cautious, because cautious people seldom make mistakes? Or that you shouldn’t be cautious, because cautious people rarely accomplish great things?

The fortune can be read both ways, and both conclusions seem reasonable. Thus the key question is, “Which meaning is right for you?” As an investor, do you like the idea of avoiding error, or would you rather try for superiority? Which path is more likely to lead to success as you define it, and which is more feasible for you? You can follow either path, but clearly not both simultaneously.

Thus, investors have to answer what should be a very basic question: Will you (a) strive to be above average, which costs money, is far from sure to work, and can result in your being below average, or (b) accept average performance – which helps you reduce those costs but also means you’ll have to look on with envy as winners report mouth-watering successes. Here’s how I put it in Dare to Be Great II:

How much emphasis should be put on diversifying, avoiding risk, and ensuring against below-pack performance, and how much on sacrificing these things in the hope of doing better?

And here’s how I described some of the considerations:

Unconventional behavior is the only road to superior investment results, but it isn’t for everyone. In addition to superior skill, successful investing requires the ability to look wrong for a while and survive some mistakes. Thus each person has to assess whether he’s temperamentally equipped to do these things and whether his circumstances – in terms of employers, clients and the impact of other people’s opinions – will allow it . . . when the chips are down and the early going makes him look wrong, as it invariably will.

You can’t have it both ways. And as in so many aspects of investing, there’s no right or wrong, only right or wrong for you.

A Case in Point

The aforementioned David Swensen ran Yale University’s endowment from 1985 until his passing in 2021, an unusual 36-year tenure. He was a true pioneer, developing what has come to be called “the Yale Model” or “the Endowment Model.” He radically reduced Yale’s holdings of public stocks and bonds, and invested heavily in innovative, illiquid strategies such as hedge funds, venture capital, and private equity at a time when almost no other institutions were doing so. He identified managers in those fields who went on to generate superior results, several of whom earned investment fame. Yale’s resulting performance beat almost all other endowments by miles. In addition, Swensen sent out into the endowment community a number of disciples who produced enviable performance for other institutions. Many endowments emulated Yale’s approach, especially beginning around 2003-04, after these institutions had been punished by the bursting of the tech/Internet bubble. But few if any duplicated Yale’s success. They did the same things, but not nearly as early or as well.

To sum up all the above, I’d say Swensen dared to be different. He did things others didn’t do. He did these things long before most others picked up the thread. He did them to a degree that others didn’t approach. And he did them with exceptional skill. What a great formula for outperformance.

In Pioneering Portfolio Management, Swensen provided a description of the challenge at the core of investing – especially institutional investing. It’s one of the best paragraphs I’ve ever read and includes a two-word phrase (which I’ve bolded for emphasis) that for me reads like sheer investment poetry. I’ve borrowed it countless times:

. . . Active management strategies demand uninstitutional behavior from institutions, creating a paradox that few can unravel. Establishing and maintaining an unconventional investment profile requires acceptance of uncomfortably idiosyncratic portfolios, which frequently appear downright imprudent in the eyes of conventional wisdom.

As with many great quotes, this one from Swensen says a great deal in just a few words. Let’s parse its meaning:

Idiosyncratic – When all investors love something, it’s likely their buying will render it highly priced. When they hate it, their selling will probably cause it to become cheap. Thus, it’s preferable to buy things most people hate and sell things most people love. Such behavior is by definition highly idiosyncratic (i.e., “eccentric,” “quirky,” or “peculiar”).

Uncomfortable – The mass of investors take the positions they take for reasons they find convincing. We witness the same developments they do and are impacted by the same news. Yet, we realize that if we want to be above average, our reaction to those inputs – and thus our behavior – should in many instances be different from that of others. Regardless of the reasons, if millions of investors are doing A, it may be quite uncomfortable to do B.

And if we do bring ourselves to do B, our action is unlikely to prove correct right away. After we’ve sold a market darling because we think it’s overvalued, its price probably won’t start to drop the next day. Most of the time, the hot asset you’ve sold will keep rising for a while, and sometimes a good while. As John Maynard Keynes said, “Markets can remain irrational longer than you can remain solvent.” And as the old adage goes, “Being too far ahead of your time is indistinguishable from being wrong.” These two ideas are closely related to another great Keynes quote: “Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally.” Departing from the mainstream can be embarrassing and painful.

Uninstitutional behavior from institutions – We all know what Swensen meant by the word “institutions”: bureaucratic, hidebound, conservative, conventional, risk-averse, and ruled by consensus; in short, unlikely mavericks. In such settings, the cost of being different and wrong can be viewed as highly unacceptable relative to the potential benefit from being different and right. For the people involved, passing up profitable investments (errors of omission) poses far less risk than making investments that produce losses (errors of commission). Thus, investing entities that behave “institutionally” are, by their nature, highly unlikely to engage in idiosyncratic behavior.

Early in his time at Yale, Swensen chose to:

- minimize holdings of public stocks;

- vastly overweight strategies falling under the heading “alternative investments” (although he started to do so well before that label was created);

- in so doing, commit a substantial portion of Yale’s endowment to illiquid investments for which there was no market; and

- hire managers without lengthy track records on the basis of what he perceived to be their investment acumen.

To use his words, these actions probably appeared “downright imprudent in the eyes of conventional wisdom.” Swensen’s behavior was certainly idiosyncratic and uninstitutional, but he understood that the only way to outperform was to risk being wrong, and he accepted that risk with great results.

One Way to Diverge from the Pack

To conclude, I want to describe a recent occurrence. In mid-June, we held the London edition of Oaktree’s biannual conference, which followed on the heels of the Los Angeles version. My assigned topic at both conferences was the market environment. I faced a dilemma while preparing for the London conference, because so much had changed between the two events: On May 19, the S&P 500 was at roughly 3,900, but by June 21 it was at approximately 3,750, down almost 4% in roughly a month. Here was my issue: Should I update my slides, which had become somewhat dated, or reuse the LA slides to deliver a consistent message to both audiences?

I decided to use the LA slides as the jumping-off point for a discussion of how much things had changed in that short period. The key segment of my London presentation consisted of a stream-of-consciousness discussion of the concerns of the day. I told the attendees that I pay close attention to the questions people ask most often at any given point in time, as the questions tell me what’s on people’s minds. And the questions I’m asked these days overwhelmingly surround:

- the outlook for inflation,

- the extent to which the Federal Reserve will raise interest rates to bring it under control, and

- whether doing so will produce a soft landing or a recession (and if the latter, how bad).

Afterwards, I wasn’t completely happy with my remarks, so I rethought them over lunch. And when it was time to resume the program, I went up on stage for another two minutes. Here’s what I said:

All the discussion surrounding inflation, rates, and recession falls under the same heading: the short term. And yet:

- We can’t know much about the short-term future (or, I should say, we can’t dependably know more than the consensus).

- If we have an opinion about the short term, we can’t (or shouldn’t) have much confidence in it.

- If we reach a conclusion, there’s not much we can do about it – most investors can’t and won’t meaningfully revamp their portfolios based on such opinions.

- We really shouldn’t care about the short term – after all, we’re investors, not traders.

I think it’s the last point that matters most. The question is whether you agree or not.

For example, when asked whether we’re heading toward a recession, my usual answer is that whenever we’re not in a recession, we’re heading toward one. The question is when. I believe we’ll always have cycles, which means recessions and recoveries will always lie ahead. Does the fact that there’s a recession ahead mean we should reduce our investments or alter our portfolio allocation? I don’t think so. Since 1920, there have been 17 recessions as well as one Great Depression, a World War and several smaller wars, multiple periods of worry about global cataclysm, and now a pandemic. And yet, as I mentioned in my January memo, Selling Out, the S&P 500 has returned about 10½% a year on average over that century-plus. Would investors have improved their performance by getting in and out of the market to avoid those problem spots . . . or would doing so have diminished it? Ever since I quoted Bill Miller in that memo, I’ve been impressed by his formulation that “it’s time, not timing” that leads to real wealth accumulation. Thus, most investors would be better off ignoring short-term considerations if they want to enjoy the benefits of long-term compounding.

Two of the six tenets of Oaktree’s investment philosophy say (a) we don’t base our investment decisions on macro forecasts and (b) we’re not market timers. I told the London audience our main goal is to buy debt or make loans that will be repaid and to buy interests in companies that will do well and make money. None of that has anything to do with the short term.

From time to time, when we consider it warranted, we do vary our balance between aggressiveness and defensiveness, primarily by altering the size of our closed-end funds, the pace at which we invest, and the level of risk we’ll accept. But we do these things on the basis of current market conditions, not expectations regarding future events.

Everyone at Oaktree has opinions on the short-run phenomena mentioned above. We just don’t bet heavily that they’re right. During our recent meetings with clients in London, Bruce Karsh and I spent a lot of time discussing the significance of the short-term concerns. Here’s how he followed up in a note to me:

. . . Will things be as bad or worse or better than expected? Unknowable . . . and equally unknowable how much is priced in, i.e. what the market is truly expecting. One would think a recession is priced in, but many analysts say that’s not the case. This stuff is hard…!!!

Bruce’s comment highlights another weakness of having a short-term focus. Even if we think we know what’s in store in terms of things like inflation, recessions, and interest rates, there’s absolutely no way to know how market prices comport with those expectations. This is more significant than most people realize. If you’ve developed opinions regarding the issues of the day, or have access to those of pundits you respect, take a look at any asset and ask yourself whether it’s priced rich, cheap, or fair in light of those views. That’s what matters when you’re pursuing investments that are reasonably priced.

The possibility – or even the fact – that a negative event lies ahead isn’t in itself a reason to reduce risk; investors should only do so if the event lies ahead and it isn’t appropriately reflected in asset prices. But, as Bruce says, there’s usually no way to know.

At the beginning of my career, we thought in terms of investing in a stock for five or six years; something held for less than a year was considered a short-term trade. One of the biggest changes I’ve witnessed since then is the incredible shortening of time horizons. Money managers know their returns in real time, and many clients are fixated on how their managers did in the most recent quarter.

No strategy – and no level of brilliance – will make every quarter or every year a successful one. Strategies become more or less effective as the environment changes and their popularity waxes and wanes. In fact, highly disciplined managers who hold most rigorously to a given approach will tend to report the worst performance when that approach goes out of favor. Regardless of the appropriateness of a strategy and the quality of investment decisions, every portfolio and every manager will experience good and bad quarters and years that have no lasting impact and say nothing about the manager’s ability. Often this poor performance will be due to unforeseen and unforeseeable developments.

Thus, what does it mean that someone or something has performed poorly for a while? No one should fire managers or change strategies based on short-term results. Rather than taking capital away from underperformers, clients should consider increasing their allocations in the spirit of contrarianism (but few do). I find it incredibly simple: If you wait at a bus stop long enough, you’re guaranteed to catch a bus, but if you run from bus stop to bus stop, you may never catch a bus.

I believe most investors have their eye on the wrong ball. One quarter’s or one year’s performance is meaningless at best and a harmful distraction at worst. But most investment committees still spend the first hour of every meeting discussing returns in the most recent quarter and the year to date. If everyone else is focusing on something that doesn’t matter and ignoring the thing that does, investors can profitably diverge from the pack by blocking out short-term concerns and maintaining a laser focus on long-term capital deployment.

A final quote from Pioneering Portfolio Management does a great job of summing up how institutions can pursue the superior performance most want. (Its concepts are also relevant to individuals):

Appropriate investment procedures contribute significantly to investment success, allowing investors to pursue profitable long-term contrarian investment positions. By reducing pressures to produce in the short run, liberated managers gain the freedom to create portfolios positioned to take advantage of opportunities created by short-term players. By encouraging managers to make potentially embarrassing out-of-favor investments, fiduciaries increase the likelihood of investment success.

Oaktree is probably in the extreme minority in its relative indifference to macro projections, especially regarding the short term. Most investors fuss over expectations regarding short-term phenomena, but I wonder whether they actually do much about their concerns, and whether it helps.

Many investors – and especially institutions such as pension funds, endowments, insurance companies, and sovereign wealth funds, all of which are relatively insulated from the risk of sudden withdrawals – have the luxury of being able to focus exclusively on the long term . . . if they will take advantage of it. Thus, my suggestion to you is to depart from the investment crowd, with its unhelpful preoccupation with the short term, and to instead join us in focusing on the things that really matter.

July 26, 2022

Legal Information and Disclosures

This memorandum expresses the views of the author as of the date indicated and such views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

This memorandum is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree Capital Management, L.P. (“Oaktree”) believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Oaktree.