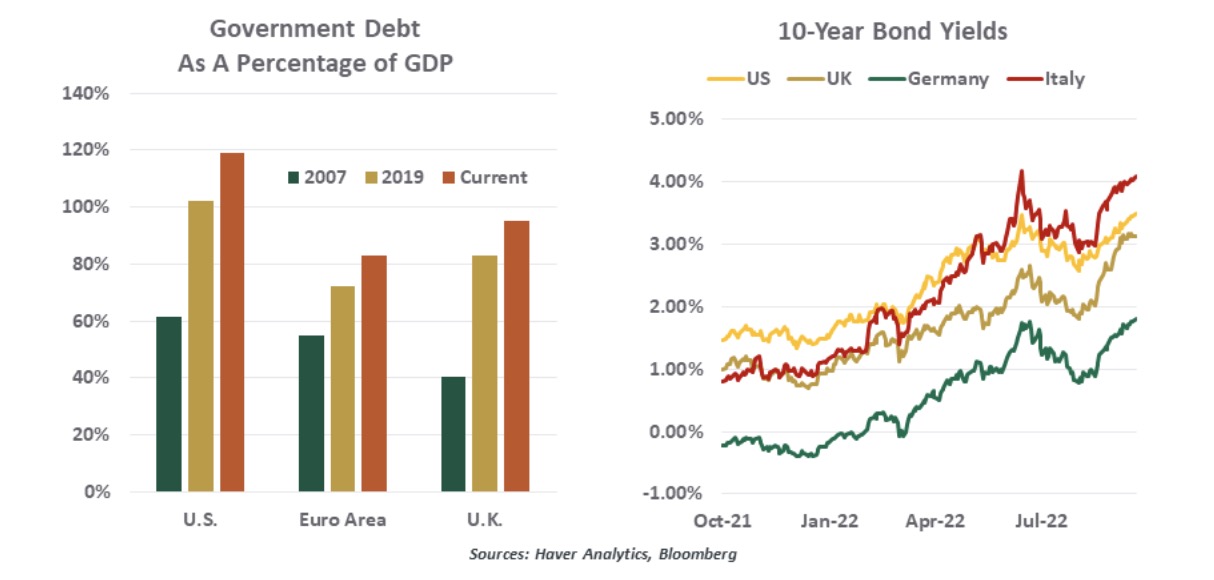

The pandemic drove up debt, and higher interest rates are adding to the burden.

We had been bullish on stocks all the way back to March 2009, when mark-to market accounting was fixed and the Financial Panic started to recede

The great tech selloff of 2022 is far from over as investors brace for earnings misses that may spur a more than 10% plunge in the Nasdaq 100.

For years, asset allocators had it easy: Buy the biggest American tech companies and watch the returns rack up. Those days are gone, buried under a crush of central bank rate hikes that are rewriting the playbooks for investment managers across Wall Street.

Week by week, the bond-market crash just keeps getting worse and there’s no clear end in sight.

Cryptocurrencies lingered near almost two-year lows as digital-asset investors sought a fresh catalyst with central bank rate increases depressing demand for riskier assets.

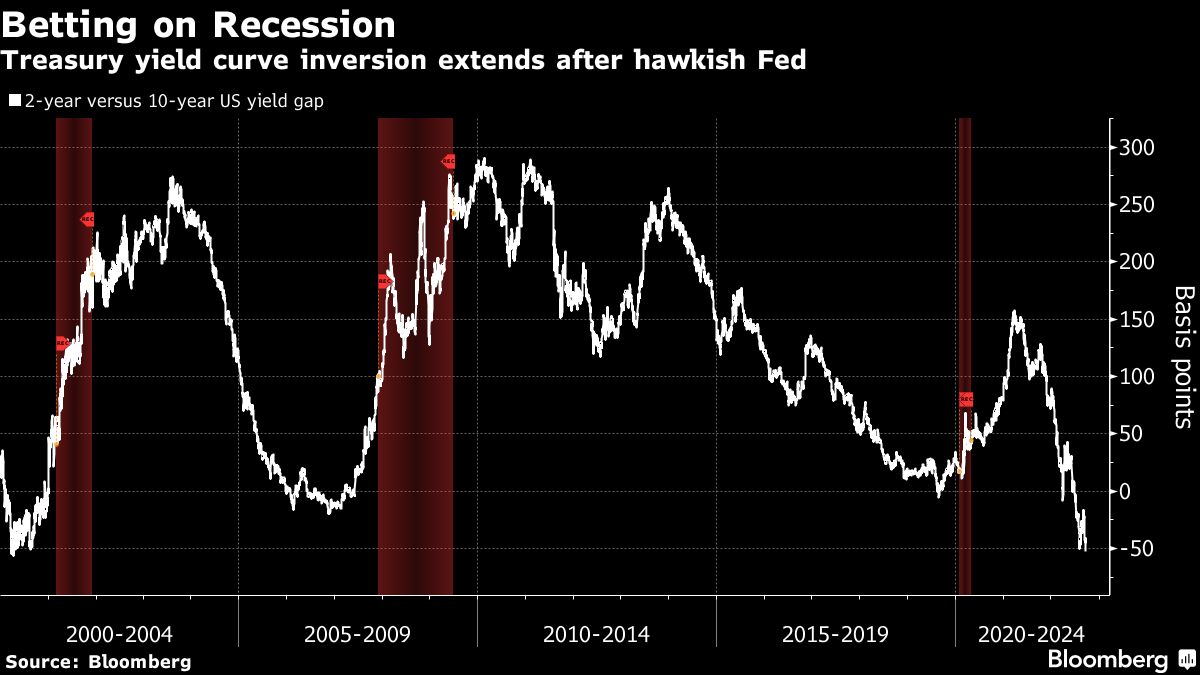

Bond traders are girding for the risk that Federal Reserve Chair Jerome Powell is ready, willing and able to plunge the US into recession to get the inflation bogey under control.

Even as the Federal Reserve jacks up interest rates and sends technology stocks tumbling, it only gets harder to stay away from the sector.

Mortgage rates in the US rose for a fifth straight week, threatening to freeze more would-be buyers out of the market for homes.

U.S. stocks are moving higher in pre-market trading, following yesterday's third-straight 75-basis point rate hike from the Fed.

Federal Reserve Chairman Powell delivered another forceful message to markets that an early pivot back to rate cuts will not happen until inflation is under control.

The world’s top gold mining executives see cost pressures sticking around into next year, adding to industry headwinds fueled by economic and political uncertainty, supply-chain disruptions and surging interest rates.

Generating investment income is challenging, especially in the low-yield environment we have been living with for the past decade.

Would you rather buy a risk-free long-term Treasury bond yielding more than 3.5% or take your chances in the stock market? The jury is apparently still out among investors...

Innovation was the market darling thematic for many years leading up to COVID.

Wednesday’s meeting of the Federal Open Market Committee is dominating all discussions. That’s inevitable. But if there’s one area where the Fed’s monetary policy could wreak changes, and where many Americans fear that it will, it is on housing.

U.S. stocks are declining in pre-market trading as the markets await the Fed’s highly anticipated monetary policy decision tomorrow.

Most pundits and thinkers are wrong about the relationship between interest rate hikes and bond prices.

Wall Street analysts have trimmed their overly optimistic earnings estimates slightly in recent months, but they’re still nowhere close to acknowledging the threat of a recession.

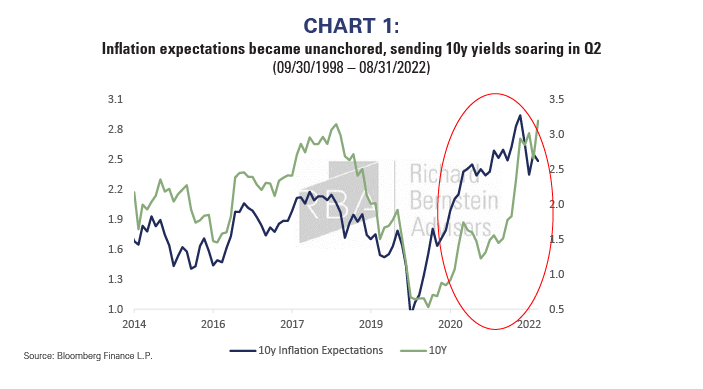

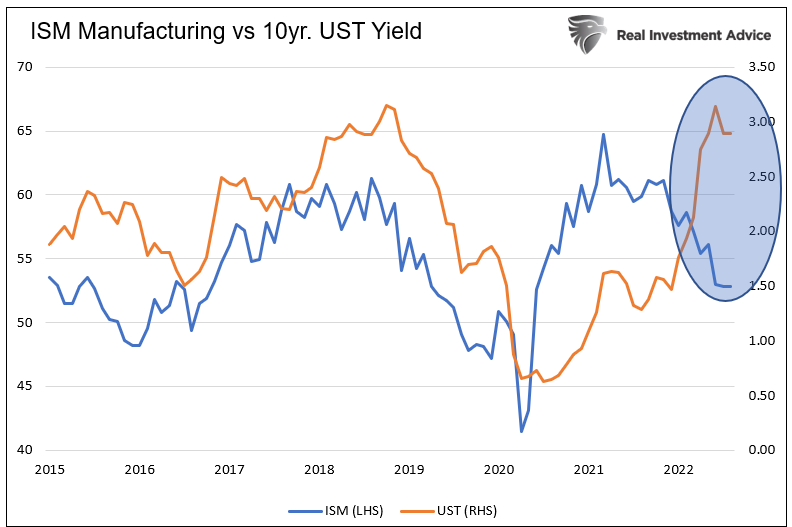

The 10-year Treasury yield briefly rose above 3.50% for the first time since 2011 on Monday, with the bond market extending its bearish run ahead of another jumbo rate hike expected this week by the Federal Reserve to bring down inflation.

The $24 trillion US Treasury market has gotten too big for even the “Masters of the Universe.” As the Federal Reserve reverses its bond purchase program and more government securities flood back into the hands of dealers, banks, investors and traders, the chances of extreme, unhealthy volatility are rising.

I wrote an article last month regarding the 10 things I got wrong about financial planning over my 20-year career. As it happens, I also got some things right and was happy when I was asked to write about them.

After more than 40 years of work in the financial markets, studying all the data I could get my hands on, I’ve found it to be universally true that those who argue “history doesn’t matter” have never actually studied history.

Bull or bear, in stocks lately, the punishment has been the same. Swift and brutal.

US stocks haven’t seen the worst of this year’s declines yet against the backdrop of scorching inflation and a hawkish Federal Reserve, according to Bank of America Corp. strategists.

What lessons for today? Any intervention in foreign exchange markets must be credible to have any chance of working. And when the Fed takes a course that is out of sync with the rest of the world, stresses increase on the rest of the foreign exchange architecture.

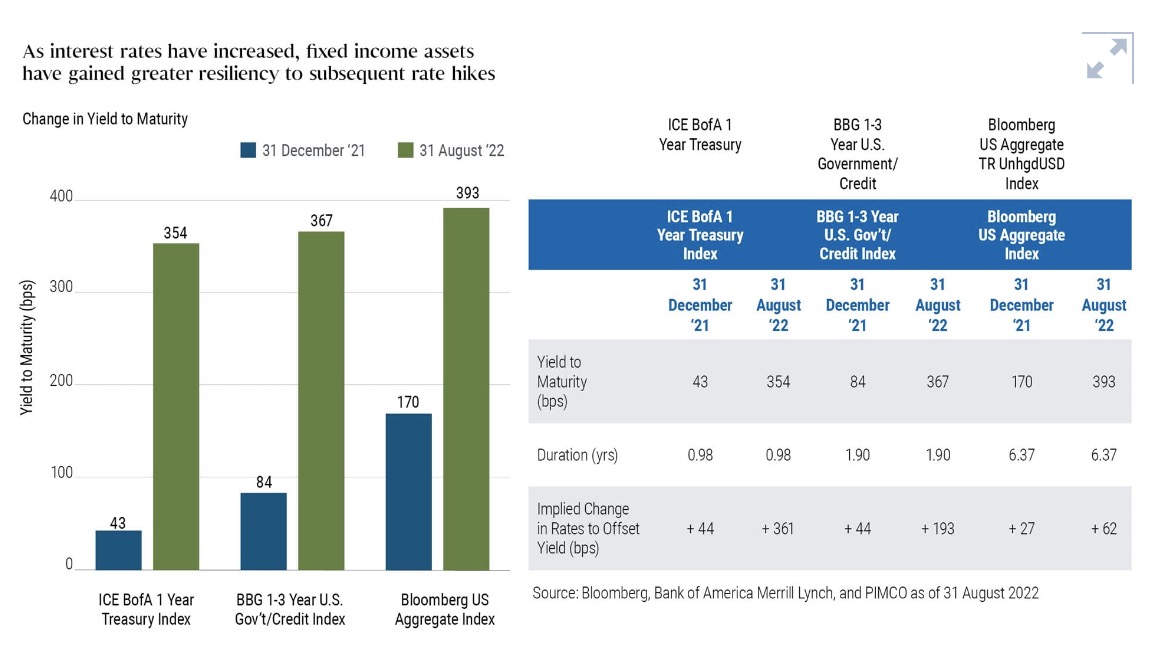

We believe short-dated bonds can offer attractive yields, flexibility, and a means to proceed cautiously as central banks continue to raise interest rates.

Dividends and dividend-paying stocks are getting renewed attention in recent months.

Sell stocks and buy opportunistic bonds, according to Jeffrey Gundlach. “The capital gains potential is the best in the last 15 years," he said. Bonds are “the place to be.”

The specter of US interest rates at 4% or even higher is bringing into sharper focus the question of when and how investors should really get back into bonds after Treasury markets suffered one of their worst beatings in decades.

We more than doubled our portfolios’ duration in a single day this summer.

U.S. equities are modestly higher in afternoon action on the heels of yesterday's sharp drop that came as consumer price inflation surprisingly came in hot.

The S&P 500 is a popular proxy to represent the state of the stock market.

“Price matters again in investing,” according to Bob Wyckoff a managing director of Tweedy, Browne. “That serves the interests of value investors.”

How bad was the August US inflation report? Let me count the ways. It’s a while since a macroeconomic release has come as such a nasty surprise, but on balance the extremely negative market reaction to the numbers was justified; they’re awful.

When the supply and demand for bonds normalize, bond investors will realize that economic, inflation and other factors warrant much lower yields.

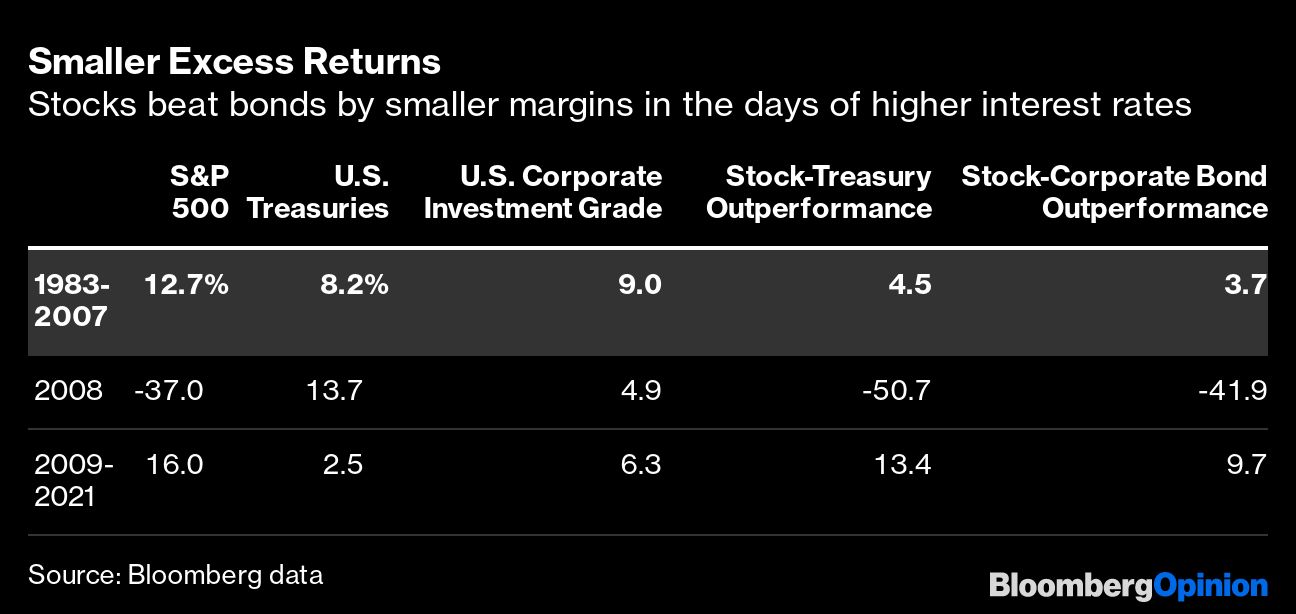

A valuation bulwark that had supported stocks relative to credit is starting to erode.

US consumer prices were resurgent last month, dashing hopes of a nascent slowdown and likely assuring another historically large interest-rate hike from the Federal Reserve.

“CPI Tuesday” doesn’t have the same ring as some other regular market dates, but there’s little denying that no single data release matters more these days than US consumer price inflation. Tuesday morning’s release on price rises in August will matter a lot.

Peak bond-issuance week is in the books, and high-grade corporate bond deals are hanging tough in the face of recession fears and surging risk-free rates, a trend that appears to be extending into the second week of September.

U.S. stocks are starting the week in positive territory, extending last week's advance that snapped a three-week losing streak.

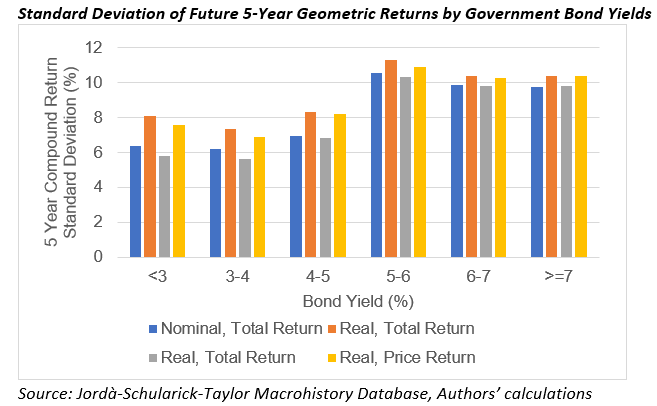

The historical evidence strongly suggests that equity returns are likely to be lower in a lower bond yield environment and this needs to be incorporated into financial projections and investor decision making.

We have always believed that common sense is the key to successful investing.

There is one and only one S&P 500 sector that is up massively this year.

Seasoned investors, staring at a world clouded by war, inflation and economic uncertainty, are buying catastrophe insurance at a record clip.

U.S. stocks are continuing to trade higher in the final session of the week and are on pace to end a three-week losing streak.

The Fed's program of QT has flown under the radar for a lot of reasons. That low profile belies its importance, however. Not only is the Fed likely to persist in this program, but it will create a strong headwind for risk assets.

Value investing is all about finding bargains that meet your investment goals and provide a margin of safety long-term. HP Inc (HPQ) and Hewlett-Packard Enterprises (HPE) represent two dividend growth stocks with uncanny similarities regarding valuation and yield.

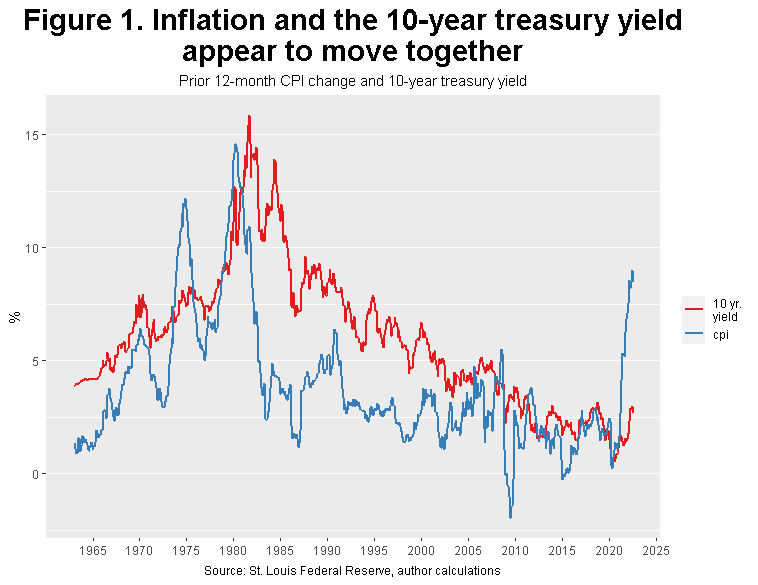

Recent inflation is a poor forecaster of changes in treasury yields. Pronouncements of a break in long-term treasury yield trends based solely on inflation may be mistaken.

Global imbalances are growing ever more intense, and that’s visible most clearly in the incredible strength of the US dollar. It’s becoming quite extraordinary.