Do Equities Perform Better When Bond Yields are Lower?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Decades of research has documented the existence of a positive realized equity risk premium (ERP), i.e., that stocks have outperformed bonds over the long-term. But there is less research on the relative future performance of stocks in international markets during different bond yield environments (i.e., the expected ERP). This article summarizes some of my forthcoming research in the Journal of Investing where I explore this effect using the Jordà-Schularick-Taylor (JST) Macrohistory database, which includes historical returns from 16 countries from 1870 to 2015.

While future equity returns have generally been lower during periods of lower bond yields, the decline is less than would be implied by a constant expected ERP. The predictive significance of bond yields varies significantly depending on the future return metric considered (nominal return versus real return, as well as total return versus price return), and whether dividend yields and inflation are considered. Overall, while the data is noisy, the analysis strongly suggests assumed returns for stocks should vary with bond yields and this should be reflected in financial projections.

Research on the equity risk premium

There is a significant body of literature demonstrating that stocks have outperformed bonds over the long-term, on average, which is the ERP. Early research on this effect generally focused on U.S historical returns, primarily leveraging the Ibbotson Stocks, Bond, Bills, and Inflation (SBBI) data series, which begins in 1926. Early research on ERPs for international markets generally leveraged MSCI country-specific returns, which begin around 1970. The introduction of the Dimson, Marsh, and Staunton (DMS) dataset significantly extended the period of analysis back to 1900. Overall, though, across countries and time periods the findings have been remarkably consistent, demonstrating that stocks outperformed bonds over prolonged periods.

Most research has focused on the realized ERP, which is the difference in the return of equities versus bonds over the period (i.e., is estimated by subtracting the realized return on bonds from the realized return on stocks). While evidence of a positive realized ERP is obviously important, the realized ERP is a backward-looking metric (i.e., ex post). While the realized ERP documented the potential benefits of investing in equities, it doesn’t provide investors with important context about what to do in different bond-yield environments.

The expected ERP is forward-looking (i.e., ex ante) metric, since it is estimated by subtracting the prevailing government bond yield from the future return of equities. The expected ERP effectively assumes an investor can earn a guaranteed return (i.e., the bond yield) or invest in equities, which has an uncertain return; the expected ERP is the difference between the two. There is obviously some risk associated with investing in government bonds, such as interest rate risk, default risk, reinvestment risk, etc., but government bonds are generally assumed to be “risk free” for research purposes and are considered as such for this article.

Data

Data for the analysis is from the JST database. The JST dataset is relatively new and includes historical return data for 18 countries primarily from 1870 to 2015 (although some time series go through 2017) in addition to other economic metrics such as GDP, government expenditure, household loan information, etc.

The JST dataset is similar to the DMS dataset, which has been used in a variety of research publications over the last decade. The DMS dataset includes historical return data for 21 countries going back to 1900. The JST dataset includes historical data further back than the DMS dataset (starting in 1870 versus 1900) and includes data series not available from DMS, in particular historical bond yields and dividend yields, which is why the JST dataset I selected it for this analysis. The JST dataset is also available for free online, while the access to DMS dataset requires a subscription from Morningstar.

I relied entirely on data from the JST dataset for this analysis, based on a download as of June 21, 2022. Canada and Ireland were excluded from the analysis because returns are not available, which reduced the number of countries considered from 18 to 16. Additionally, I excluded the country-specific returns for Germany in 1922 and 1923 given how notably they deviated from averages over the period.

The analysis used five time series from the JST dataset: bond yields (series “bond_rate”), bond returns (series “bond_tr”), equity returns (series “eq_tr”), dividend yields (series “eq_dp”), and inflation (series “cpi”).

The underlying data for each series (for each country) typically comes from a variety of sources, as outlined in the respective documentation files. Bond yields and bond returns included in this analysis would generally be defined as those that are longer term in nature, with maturities of approximately 10 years, although the actual maturity varies both by year and country.

Dividend yields were used as a valuation metric for the analysis. While other valuation metrics, such as the CAPE ratio (Shiller and Campbell 1998) are perhaps more popular, especially given the rise of buybacks, the CAPE ratio is not available in the JST dataset.

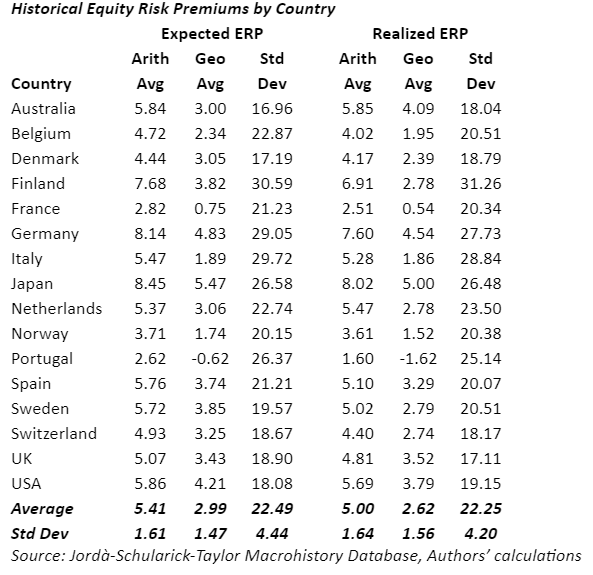

The historical ERP

The exhibit below provides some context around the historical average arithmetic return, geometric return, and standard deviation for the expected and realized ERPs over the period, versus bond yields and bond returns, respectively. The expected ERP is calculated by subtracting the future one-year return on equities from the bond yield available at the end of the previous year and the realized ERP is calculated by subtracting the one-year return on equities from the one-year return on bonds for the same year.

The average annual arithmetic expected ERP was 5.40% and the average annual expected geometric ERP was approximately 3.0%. This is slightly higher than the realized ERP values, at 5.0% (arithmetic) and 2.6% (geometric), respectively.

The average annual arithmetic expected ERP was 5.40% and the average annual expected geometric ERP was approximately 3.0%. This is slightly higher than the realized ERP values, at 5.0% (arithmetic) and 2.6% (geometric), respectively.

The expected ERPs and realized ERPs have also been relatively similar, which isn’t necessarily a surprise, but it is important context for the analysis I give later and the focus on expected ERP, given the fact most research has focused on realized ERPs.

The U.S. ERP values have been higher than other countries, especially the geometric averages. Finland has also had a relatively high arithmetic and geometric average equity return over the historical period. This is important for context purposes for investors who may rely entirely on historical returns for financial projections. While it is certainly possible the differences across countries noted in Exhibit 1 will persist in the future, it is unlikely they would do so at the same levels they have historically.

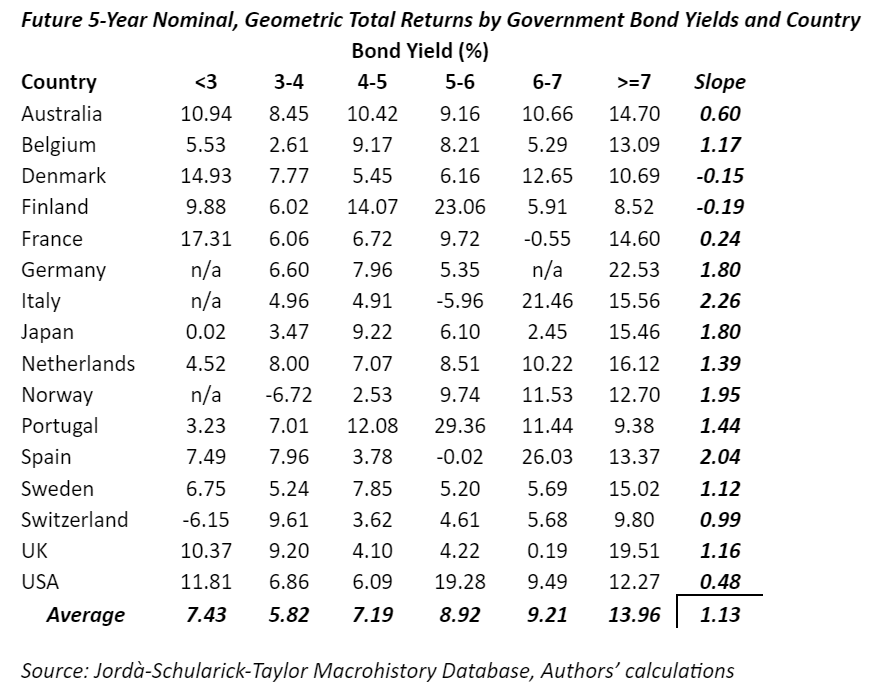

The exhibit below shows where bond yields are binned in roughly 1% increments and the future five-year geometric returns and the standard deviations of the returns are reviewed. The binning occurs across all countries and time periods. I controlled for these variables, though, in future analyses and regressions.

For this analysis, and future calculations focused on future ERP values, only nonoverlapping periods were used to ensure independence across each calculation. Only calendar years with values ending in zero or five were included.

Four different future five-year return metrics were considered: nominal total return, real total return, nominal price return, and real price return. I considered different return definitions to better control for some of the other factors that could be related to future equity returns (e.g., inflation). Additionally, there are some return components that are effectively endogenous in future regressions (e.g., dividend yield is a component of total return). The standard deviations for the groups are also reported.

These results provide preliminary evidence that equity returns have been higher during periods when yields on bonds were higher, since there is clearly a positive relationship between equity returns and bond yields.

The standard deviation of future returns also increased during higher bond yield environments. In other words, there appears to be more uncertainty around the future return of equities when bond yields are higher.

The analysis is repeated, but for individual countries, where the results are included below.

While the relation between bond yields and future five-year nominal geometric equity returns was relatively noisy, the effect is positive for all but two countries (Denmark and Finland). In other words, equity returns have historically been higher during periods of higher bond yields, at least on average.

Additional analysis

It could be that other variables are driving the noted effects (e.g., inflation, dividend yields, etc.) in addition to the approach used to bin the variables (i.e., combining across time periods and countries), though. Therefore, I also conducted a series of ordinary least squares (OLS) regressions to better understand the relation between bond yields and future equity returns.

The full results are included in the paper, but the regressions suggest that while future equity returns were positively related to bond yields (i.e., equity returns were generally higher when bond yields were higher), the slope was clearly less than one. For example, the coefficient for bond yields (as the only independent variable) when nominal total return is the dependent variable is .817 (with an intercept of 5.907). This implies that the return on equities rises as bond yields increase, but that a 1% rise in bonds has only historically resulted in a .8% increase in return. The size of the bond yield coefficient declines further when other independent variables (and dependent variables) are included, further suggesting that equity returns are likely to be lower in a low yield environment, but higher than a constant equity risk premium would suggest.

Conclusions

Low bond yields present an obvious challenge for investors. While there is significant evidence documenting that stocks have outperformed bonds historically, i.e., the realized equity risk premium (ERP) is positive, there is less research exploring how stocks performed in different bond yield environments on a forward-looking basis (i.e., the expected ERP). This article summarizes some forthcoming research exploring this effect.

Lower expected equity (and bond) returns have important implications for advisors and investors, both with respect to investing/allocation decisions and financial projections. With respect to allocation decisions, the historical evidence suggests that the relative return on equities has been higher in lower yield environments, especially when controlling for other economic variables (e.g., inflation and dividend yields).

With respect to financial projections, this analysis suggests that using pure historical averages in a projection is unlikely to be a reasonable assumption, since such an approach would not capture lower expected returns in the near-term (especially for fixed income, but also for equities). However, since financial projections can last for extended periods (50+ years), and it’s uncertain how long the current market environment will last, one potential strategy is to create two sets of return assumptions: a shorter-term (conditional) set of values that incorporate current market environment conditions, and long-term (unconditional) set of values that reflect longer term expected returns (that are based more on long-term fundamentals).

Regardless, the historical evidence strongly suggests that equity returns are likely to be lower in a lower bond yield environment and this needs to be incorporated into financial projections and investor decision making.

David Blanchett, PhD, CFA, CFP®, is managing director and head of retirement research at PGIM. PGIM is the global investment management business of Prudential Financial, Inc. He is also an Adjunct Professor of Wealth Management at The American College of Financial Services and a Research Fellow for the Retirement Income Institute.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All