I built a 4.36% real (inflation-adjusted) systematic withdrawal portfolio using a 30-Year TIPS ladder.

Is it time to move beyond I bonds?

Investors love easy-to-follow “rules.” The simpler, the better.

Key Takeaways

Macro uncertainties and tightening financial conditions are pressuring the real estate investment market. Tim Wang, Head of Investment Research for Clarion Partners, discusses the challenges and opportunities in this current environment.

With this week’s announcement that the White House is deploying nearly $3 billion to boost domestic output of EV batteries and the minerals used to make them, it may be time for investors to take notice.

The Treasury market was upended Friday by a surge in wagers that circumstances will allow Federal Reserve to slow its pace of rate increases as early as year-end.

In a week where homebuilding stocks were faced with surging US Treasury yields and data showing weakening demand for homes, one analyst is throwing in the towel on the sector.

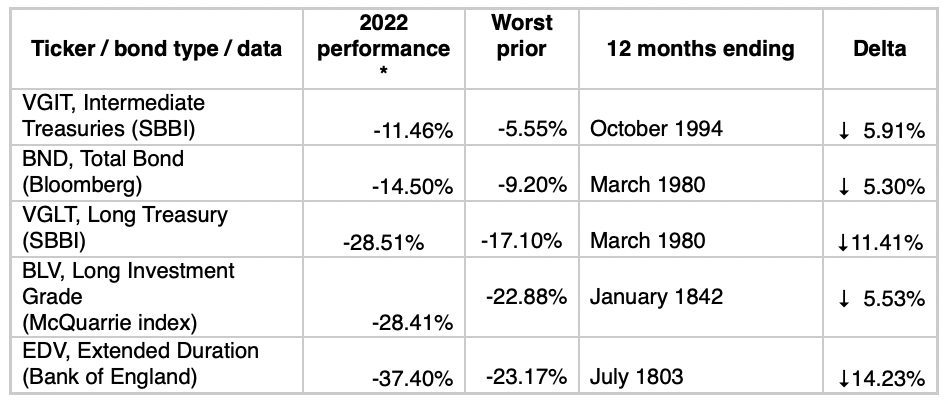

Treasury Inflation-Protected Securities can be a buffer against long-term inflation, but it's possible for TIPS price declines to outpace principal adjustment in the short term.

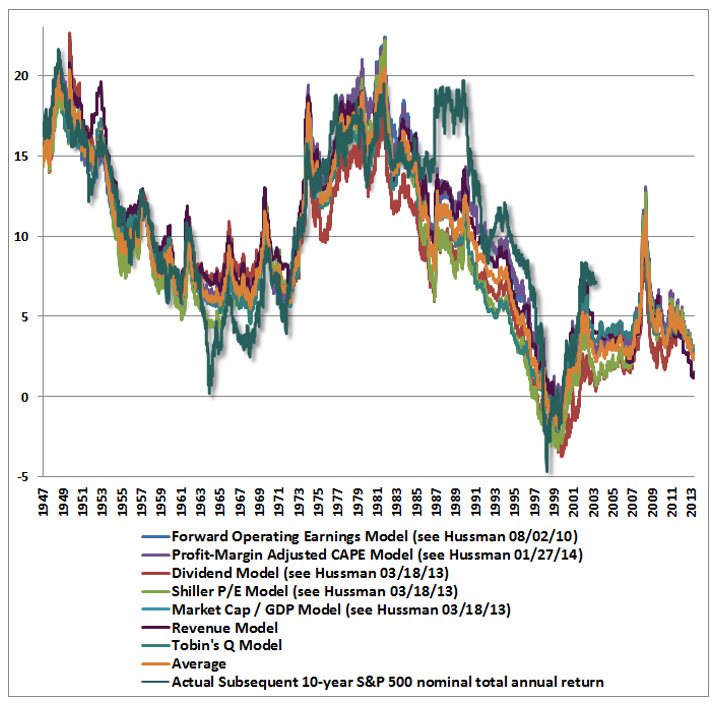

At the beginning of 2022, our most reliable stock market valuation measures stood at record levels, beyond even their 1929 and 2000 extremes. The 10-year Treasury yield was at 1.5%, the 30-year Treasury bond yield was at 1.9%, and Treasury bill yields were just 0.06%. By our estimates, that combination produced the most negative expected return for a conventional passive investment portfolio in U.S. history.

The battering of bonds this year from inflation and higher rates has made long-term municipal securities so cheap that investors who usually shun them may be buyers.

Overall, Wall Street has made only modest downward adjustments to earnings outlooks this year. For all the recession hysteria, consensus earnings forecasts for 2023 are a meager 2% below where they started the year.

Blame the Fed, war and fiscal profligacy all you want. But big trouble was lurking in many widely followed portfolio strategies long before those threats took hold.

The stock market might be trying to bounce back, but one group of investors is staying on the sidelines: retail traders.

While the Fed continues to hike rates to combat high inflation levels aggressively, history shows that deflation will become a more significant threat when something “breaks” in the financial or credit markets.

The Fed remains singularly focused on containing inflation but has made little headway so far.

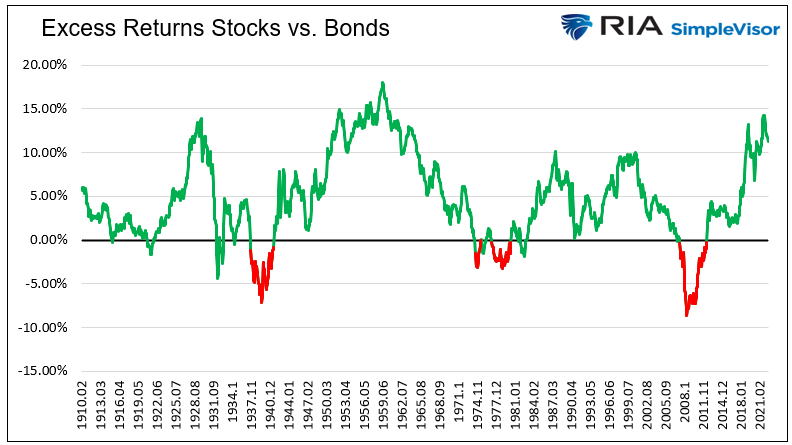

I look back to other periods when bonds outperformed stocks. This analysis allows us to assess specific stock traits and specific industries that over- and underperformed in those eras.

The difficult capital markets saga of 2022 continued through the third quarter with few safe harbors as rates rose and growth slowed.

Bill Gross pioneered the “total return” strategy in the 1980s that revolutionized the once-sleepy bond market.

Mortgage rates above 7% have put the housing market on ice as affordability challenges put off a lot of buyers. Newer, younger homeowners who locked in their mortgage at a low interest rate — and whose next move probably would be trading up — are content to stay where they are until mortgage rates fall.

Exchange-traded fund investors are preparing for the possibility that peak bond pain has passed.

The long-simmering idea that the US government should stand ready to buy back Treasury securities from investors to improve market functioning is moving closer to reality.

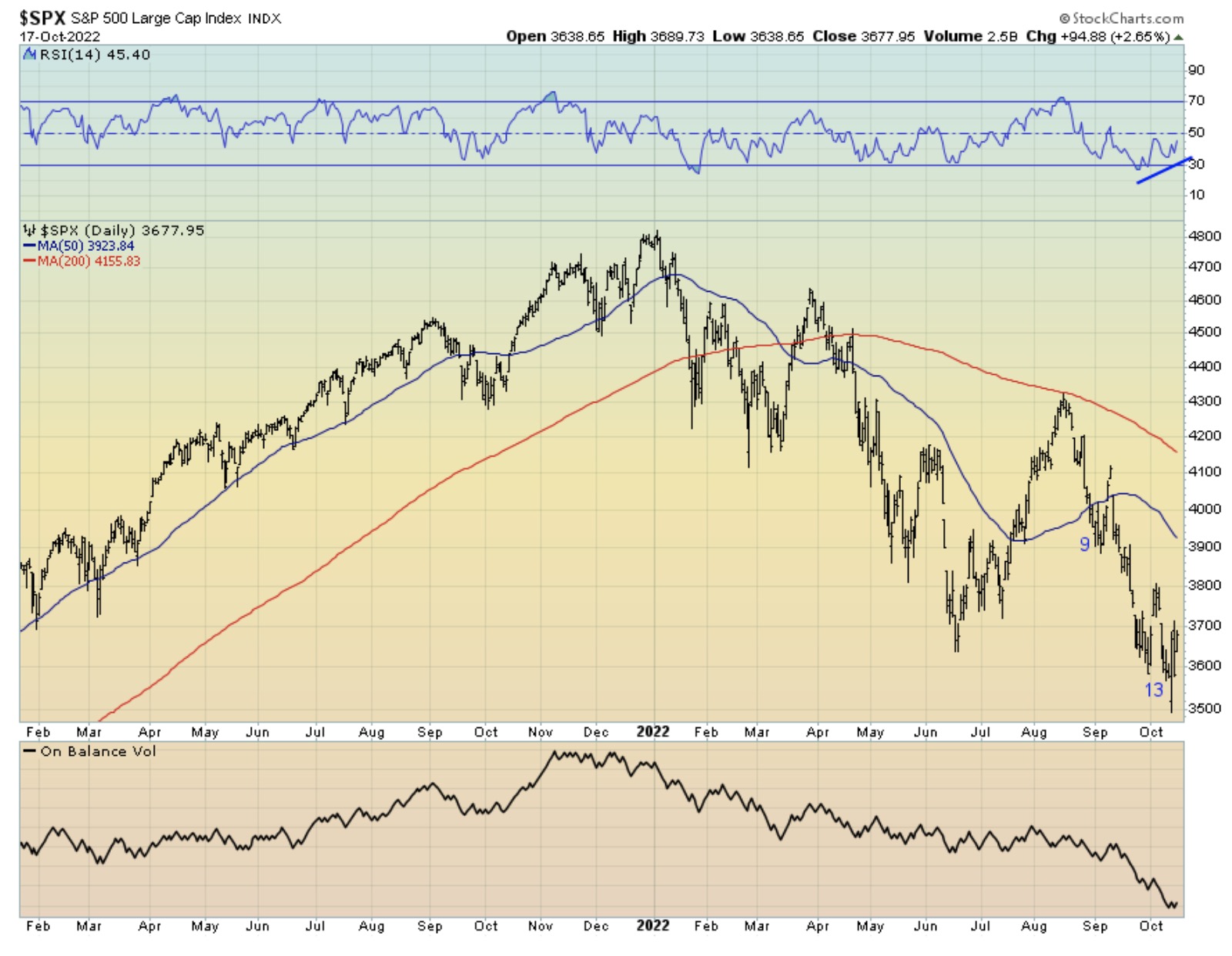

As has been the case in recent weeks, the stockmarket finds itself in a position where various technical factors, market internals, positioning and sentiment are suggesting this sell-off may be overdone and a short-covering rally due.

Citigroup calls it a “head scratcher.” Goldman Sachs terms it “striking resilience.” For Columbia Threadneedle, it’s a “reward for proactiveness.”

A strange thing keeps happening in this nightmare year on Wall Street: Seemingly surefire bets that outsize volatility will engulf equity indexes keep misfiring, even as those riding turmoil in single stocks pay off handsomely.

The world is in a very different macroeconomic position today compared to the prior forty years.

The sleeper hit of 2022 investing is about to lose some of its luster — but it still might be one of the best places to store your cash.

Investors are looking beyond a looming global recession and they see one country – and its financial markets – emerging strongest on the other side.

U.S. equities are beginning the new week sharply higher, getting a boost from the U.K.'s decision to abandon nearly all its tax cut plans.

Despite crippling stock and bond market performance in 2022, there are nuggets of good news for clients.

In 1987, Sports Illustrated, the preeminent sports periodical of the time, predicted the Cleveland Indians would win the American League pennant in its baseball season preview.

Inflation concerns on Friday once again pulled the rug from under investors struggling to find their footing as the Federal Reserve's battle against rising consumer prices shakes the economic terrain.

2022 has been a stormy year for bond investors, and the forecast calls for more of the same. We address today’s biggest investment challenges—from persistent inflation to rising rates to a looming recession—the silver linings of higher yields, wider credit spreads, and strategies for navigating bad weather.

A couple of weeks ago, in our quarterly strategy report, I argued that it appeared that innovation had bottomed.

Digging in a little deeper, we sifted through this first quintile of the S&P 500 for other insights.

Is a recession lurking around the corner in 2023? If so, how might it impact defined benefit (DB) plan sponsors—and what steps, if any, should they consider taking?

Sandpiles can be fun. Nothing beats taking kids to the beach (or being a kid!) and watching their creativity blossom into all kinds of magical shapes. The problem with sand construction is it doesn’t last. I have it on good authority that building your house on the sand probably won’t end well.

Review the latest portfolio strategy commentary from Mike Gibbs, managing director of Equity Portfolio and Technical Strategy.

Yields on popular Series I savings bonds — intended to protect consumers against price increases — are likely heading down even as inflation continues to surge.

In August 2020, as the global pandemic was straining emerging countries’ ability to make debt payments, we published a white paper – “Sovereign Contingent Bonds: How Emerging Countries Might Prepay for Debt Relief” – introducing the concept of “sovereign coco bonds,” a way for countries to structure bond agreements to allow for more flexible policy options in the face of a crisis.

2022 has hit investors with an unprecedented 1-2 punch of sharply negative returns in both the equity and fixed income markets, but our Strategic Income team feels the selloff has created attractive opportunities in high yield bonds.

Senior Sovereign Analyst Jon Levy tackles three big questions on the Bank of England's recent operations.

With Treasury yields around 4% and corporate bonds yields even higher, fixed income is the better alternative to stocks.

The strong dollar remains a risk to corporate profits and asset prices as the impact on the global economies grows.

Federal Reserve officials committed to raising interest rates to a restrictive level in the near term and holding them there to curb inflation, though several said it would be important to calibrate hikes to mitigate risks.

The top 50 broad strategy funds – determined by highest historical performance through 2021--outperformed the market by 21 percentage points through the first six months of 2022.

U.S. stocks are mixed and subdued as the markets digest another hot inflation report in the form of the September Producer Price Index.

"Carry on!!" was the gruff but oh so welcomed command screamed at me by Marine drill Sergeant Jo Quinn Cruz in October of 1967.

A couple weeks ago, in our quarterly strategy report (see: QSR-Has Innovation Bottomed?), I argued that it appeared that innovation had bottomed.

The era of “TINA”—short for “there is no alternative” and describing a phenomenon where bond yields were so low that many investors felt they had no choice but to invest in stocks, even at stretched valuations—has given way to a market where they can “pay attention to the yield(s).” Or “PATTY,” for short.

Jamie Dimon says don’t be surprised if the S&P 500 loses another one-fifth of its value. While such a plunge would fray trader nerves and stress retirement accounts, history shows it wouldn’t require any major departures from past precedents to occur.