As the market continues to broaden in 2026, a balanced approach matters more than ever.

According to Gleason, the freezing of Russian assets following the 2022 invasion of Ukraine accelerated the global push toward de-dollarization. Nations around the world took notice that access to the dollar-based financial system could be restricted, increasing the appeal of gold as a reserve asset that cannot be frozen or sanctioned by foreign governments.

US technology stocks rebounded, lifting key indexes, after the latest flareup of concerns about the scale of the artificial-intelligence-fueled rally wiped nearly $1.3 trillion from the market capitalization of Nasdaq 100 companies over the first two days of the week.

A real, potentially lasting U.S.-Iran deal appears to be on the horizon for the first time in many weeks of on-, then off-again negotiations. Should this be the deal that does it, or another one in the near term, oil prices will respond. In fact, they’ve already dropped in response to the news that the Strait of Hormuz will reopen.

Kevin Warsh, the new chairman of the FOMC, has long been critical of forward guidance, which is the Fed’s practice of explicitly signaling the future path of interest rates (e.g., “rates will stay low for an extended period” or publishing a projected path for policy rates). His concern is that the guidance could give the impression that policymakers might have a high degree of confidence about the future path of the economy and rates.

The announcement of an extended ceasefire in the Middle East is welcome news. The accord, which is scheduled to be signed late this week, reduces a source of geopolitical uncertainty that has hovered over the global economy. But significant risks remain.

Emerging market (EM) fixed income's risk-adjusted profile has meaningfully improved. Sharpe ratios across EM credit and local rates have rebounded, with EM credit delivering one of the strongest risk-adjusted performances in fixed income over the past two years.

One of the key questions for investment professionals is whether oil prices will return to pre-war levels once the Middle East crisis is resolved. At the same time, many are asking why oil prices are not higher, especially since the latest geopolitical deal recently pushed crude to its lowest level since the initial attack.

JPMorgan Chase & Co.’s asset-management arm is urging investors to stick with stocks and other higher-risk assets in the second half of 2026, arguing that an AI investment boom and resilient consumers should keep the expansion intact despite persistent inflation and a Federal Reserve on hold.

As we go to press, fighting in the Mideast has escalated, sending crude higher, but stocks, in early Monday trade, have shown remarkable stability following Friday’s deep selloff.

Silver's chart also weakened substantially, although the metal remains near important longer-term support levels and has not yet confirmed the same degree of structural breakdown seen in gold.

After more than three years of underperformance, our prognosis for global health care stocks remains positive. The sector now offers a broader set of high-quality companies at valuations that appear increasingly disconnected from fair value.

Equity markets should remain supported by strong earnings and capital investment trends through 2026, but market concentration and macro risks leave less room for error.

The war in Iran is putting pressure on airlines. Higher jet fuel prices are cutting into profit margins, and the risk of a prolonged conflict may reduce travel demand in Europe and Asia. But for lessors, these gathering clouds may come with a silver lining.

Fertilizers sit at the center of this transmission mechanism. As much as a third of the global supply of these commodities passes through the Strait of Hormuz, which has largely been closed for three months. This has triggered shortages and a price spike.

In case you’ve been living under a rock for the past few months, three of the world’s largest and most consequential private companies—SpaceX, Anthropic and OpenAI—are preparing to go public in the same year. Together, they could add nearly $4 trillion in market cap to public markets.

The world is not ending. It is restructuring. But restructuring, as I noted at the outset, comes with an asterisk. What is really happening is a replacement, of assumptions, of guarantees, of the architecture that held everything together for eighty years.

The latest Emerging Markets Insights discusses companies across various sectors that have expressed cautious optimism for the second half of 2026 despite ongoing geopolitical pressures and higher input costs. Templeton Global Investments highlight what they observed at a recently attended summit.

Climate change has become a defining force in geopolitics. As governments respond to record heat waves, floods, wildfires and droughts, their policies and economic posturing are reshaping manufacturing, trade and energy security across the capital markets.

While insurance coverage has broadly kept pace with rising catastrophe exposure, the protection gap — in absolute terms — has gone up as the value of exposed assets has grown, the Swiss Re Institute said on Wednesday.

Get ready for a magnificent month, and then some. Mega-cap tech stocks dominate the corporate event calendar in June, already highlighted by NVIDIA (NVDA) CEO Jensen Huang’s keynote address at Computex 2026 in Taiwan earlier this week, one of many major conferences.

Businesses are racing to build the physical infrastructure that makes AI usable at scale – data centers, the graphics processing unit (GPU) hardware stack, power, and cooling.

If you’re not familiar with the name Leopold Aschenbrenner, you should be. A 24-year-old wunderkind, Aschenbrenner was hired by OpenAI in 2023 to work on the company’s “superalignment” team, essentially trying to figure out how to keep AI systems safe once they become smarter than the people building them.

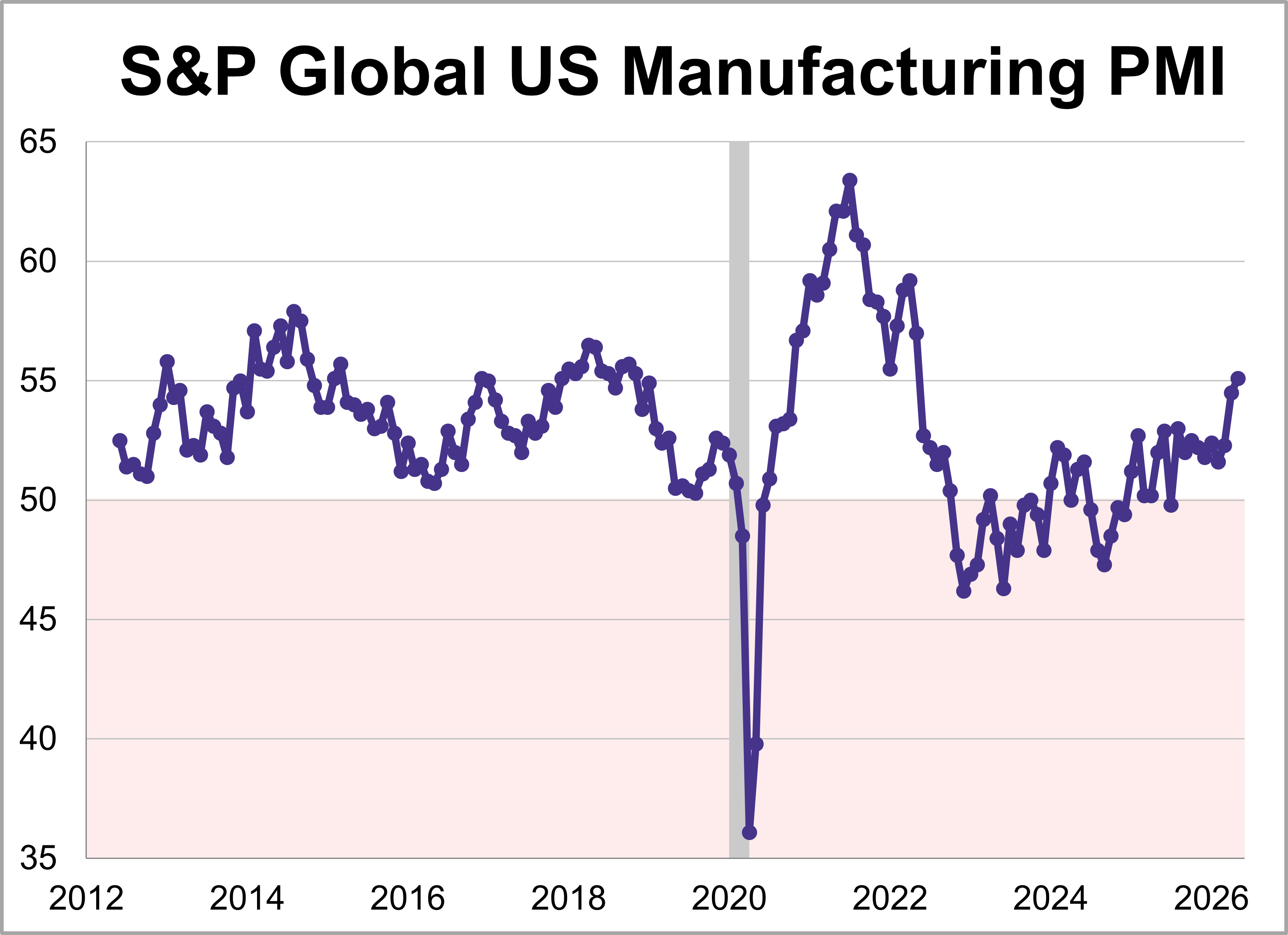

U.S. manufacturing hit its highest level in four years, as the S&P Global PMI climbed 0.6 points to 55.1 in May. For a second straight month, the expansion was largely driven by defensive stockpiling as companies continue bracing for supply disruptions and price hikes linked to conflict in the Middle East.

The dollar is supposed to be dying. We’ve heard that argument for the better part of a decade, and it’s getting louder, not quieter. Dollar dominance isn’t fading. In fact, the events of late April 2026 just delivered the loudest counter-signal in years.

If you want a blueprint for how countries can survive this era of great power rivalry, look no further than Vietnam.

Recent market volatility and the conflict in Iran have understandably pushed many emerging market investors to the sidelines. But periods of uncertainty have historically offered attractive entry points into emerging market debt (EMD), particularly when underlying fundamentals are improving and asset flows are likely to increase.

Despite these higher costs, a projected 45 million Americans are expected to travel at least 50 miles from home this weekend, setting a new record. Close to 40 million will drive while some 3.7 million will fly.

In this second quarter update, Western Asset believes global fixed-income markets face a more complex backdrop as geopolitics, rapid AI adoption and private credit scrutiny intersect.

Global bond yields are reaching frightening levels due to the continued war in Iran and the effective closure of the Strait of Hormuz. Continued high oil prices and the threat of reverberating inflation are causing investors to demand higher yields on government bonds.

Hedge funds have been selling the scorching rally in US semiconductor stocks to book profits, while keeping their overall exposure to the AI theme, according to traders at Goldman Sachs Group Inc.

Emerging markets (EM) are using low-cost renewables to cut fuel imports, stabilize power costs and improve energy security—positioning EM as the growth engine of the energy transition. Countries and companies that leverage their dominance in critical minerals and green technology could pull ahead, creating dispersion in potential outcomes for investors.

Nineteenth-century oil processing plants used simple, column distillation of crude oil to produce kerosene, which was in high demand for lighting lamps. The process also yielded a dangerously flammable byproduct called gasoline which had no obvious use.

Emerging market debt is compelling as a medium‑term structural allocation, particularly for investors seeking to diversify away from concentrated U.S. exposures.

The nothing-burger that came out of the Xi-Trump summit drove home a new reality for global investors. The NACHO trade, which stands for “not a chance Hormuz opens,” is on. Prospects of prolonged inflation have risen, sending global bond yields higher and the US dollar stronger.

I’ve long been a student of game theory, the branch of mathematics that studies how rational actors make decisions when their outcomes depend on what everyone else does. It’s a helpful framework for understanding markets and geopolitics, and right now, there’s no better place to apply it than Taiwan.

Investors shed government bonds around the world, propelling borrowing costs to multi-year highs from Japan to the US amid intensifying fears that war-driven inflation will force central banks to pursue higher interest rates.

AI is surely the zeitgeist at industry conferences across sectors right now. Emerging technology, increased efficiency, and scalability are all talking points. But so too are headcount reductions, reduced tech-sector free cash flow, and growing worries about a 1990s-like bubble.

Stock markets have been hitting all-time highs and credit spreads remain low, yet higher interest rates and mounting floating-rate debt are straining lower-rated borrowers. This tension is surfacing first in leveraged loans as “quiet defaults” become more common — opening up a dynamic set of opportunities for investors specialized in stressed and distressed assets.

It’s likely not a bubble. Earnings are high. Prices are high because they anticipate future high earnings growth. The historical record shows that growth rate is achievable.

Artificial intelligence (AI) leadership is no longer a developed-market monopoly. Emerging markets (EM) now have their own AI champions, and productivity gains may follow. For bond investors, we expect the implications to differ by country—driven by industry composition, capital intensity, digital infrastructure and speed to adoption.

China investors are counting on the summit between Xi Jinping and Donald Trump to deliver just enough to sustain the detente trade underpinning stocks and the yuan.

After going negative in March after the outbreak of hostilities between the U.S. and Iran, flows of gold into ETFs flipped positive again in April, with all regions reporting inflows of metal.

Early detection, I believe, is one of the smartest investments you can make, whether we’re talking about your portfolio or your health.

Gold demand was up 2 percent year-on-year in the first quarter, setting a record in value terms. Including over-the-counter (OTC) selling, gold demand came in at 1,231 tonnes.

Artificial intelligence unknowns are creating stress in the market, and we don’t see that ending any time soon. For long-term investors, these stressors can create opportunities.

Though the U.S. drills far more oil than in the past and relies less on supplies from the war-torn Persian Gulf, U.S. consumers see there's no escaping global price realities.

With the war in Iran dragging past the original ceasefire deadline, how might the situation impact global energy markets—and other sectors—from here? To cut through the noise, we asked Luke Pryor, Security of the Future Portfolio Manager and Co-Portfolio Manager of Strategic Equities, to share his oil and gas industry expertise.

Something unusual is happening with U.S. inflation data. While the core Consumer Price Index (CPI) has looked relatively cool recently, core Personal Consumption Expenditures (PCE) inflation has risen sharply.