Bringing family into an advisory firm is not a shortcut. It can add complexity and raise expectations. But when the mission is clear, standards are applied consistently, and systems are strong, involving family can create meaningful long-term stability. That stability, however, depends on fairness.

The 30-year rate increased six basis points to 5.18% on Tuesday, a level last seen on the brink of the global financial crisis in 2007, rising alongside US government yields across maturities.

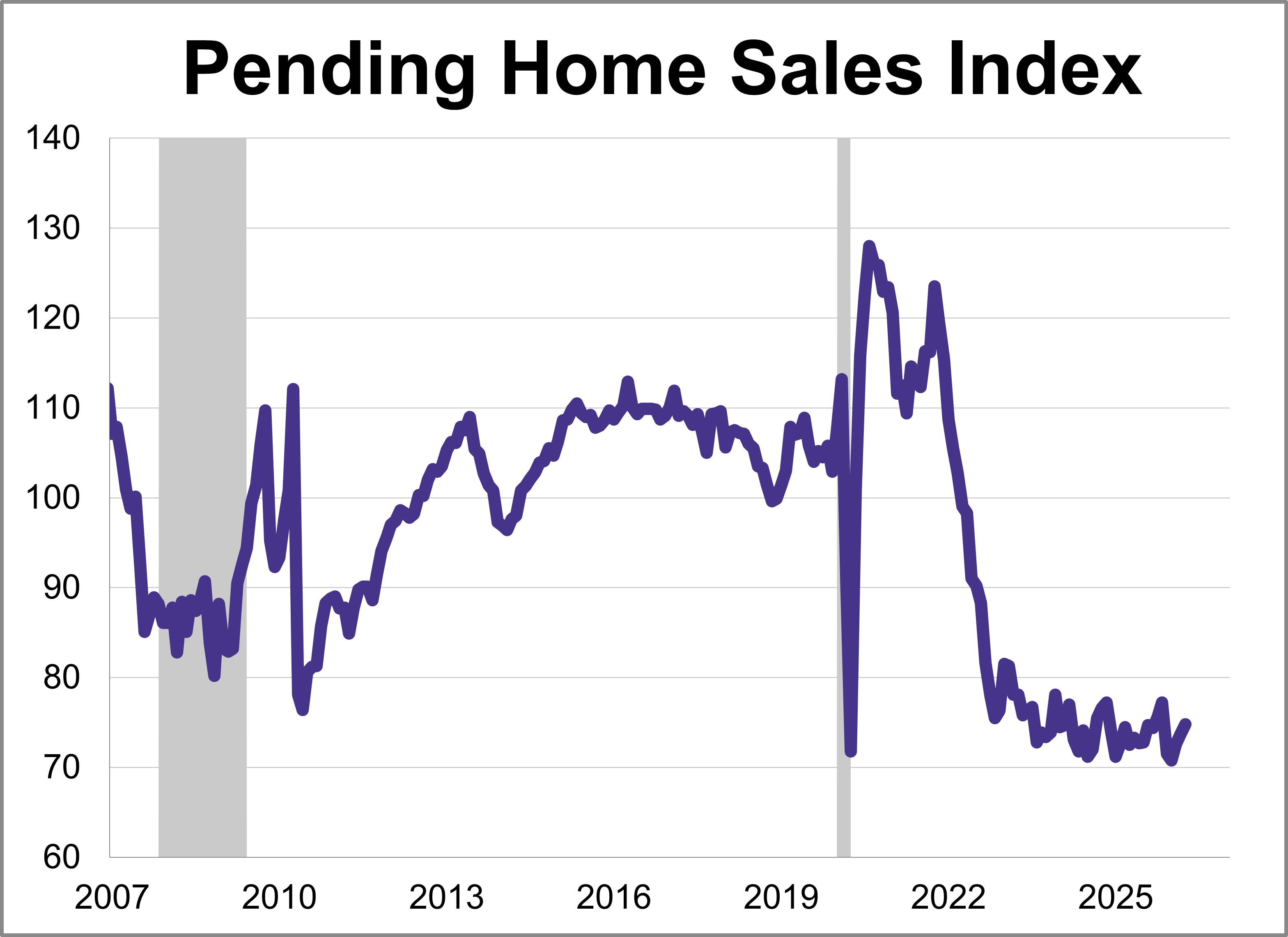

The National Association of Realtors® (NAR) pending home sales index rose 1.4% in April to 74.8, markings its third consecutive increase and highest level since November.

The nothing-burger that came out of the Xi-Trump summit drove home a new reality for global investors. The NACHO trade, which stands for “not a chance Hormuz opens,” is on. Prospects of prolonged inflation have risen, sending global bond yields higher and the US dollar stronger.

I’ve long been a student of game theory, the branch of mathematics that studies how rational actors make decisions when their outcomes depend on what everyone else does. It’s a helpful framework for understanding markets and geopolitics, and right now, there’s no better place to apply it than Taiwan.

A frequently asked question in recent weeks is whether the market is simply ignoring the risks stemming from the current geopolitical conflict, especially given the spike in oil prices that has pushed inflation pressures higher.

As Kevin Warsh takes over as Federal Reserve chair with his own goals, he may face challenges even beyond rate policy, from inflation to independence to a bulbous balance sheet.

Investors were forced to pay attention Friday, when the most interest-rate sensitive corners of the market saw big plunges in an ugly market selloff. The small-cap Russell 2000 Index dropped 2.4% for the biggest single-day decline since November.

Yields on US bonds dipped as much as three basis points Monday after Iran’s semi-official Tasnim reported that Washington proposed a temporary waiver on Iran oil sanctions until the final agreement, citing a source close to the negotiation team.

U.S. inflation and rates remain elevated. Credit markets continue to show resilience. Opportunities are emerging across securitized and high yield assets

First quarter 2026 earnings were stronger than expected and we think that there might be continued strength in the second quarter, unless there is a major macro shift.

The U.S. economic landscape in April was defined by a significant rebound in inflation across both consumer and wholesale sectors, complicating the path for future monetary policy.

The United States has not felt the greatest costs of the Iran conflict, but challenges are becoming visible. Energy prices have risen, with limited prospects for relief. Inflation measures are poised to spread to other product and service categories. Inventories that helped to blunt the impact are depleting; supply chain distortions are accumulating.

With tensions simmering in the Middle East and the global economy feeling the pinch of high energy prices, high-yield bonds might not be on every investor’s radar. In our view, they should be.

ClearBridge Investments: The ongoing energy crisis is pushing global oil inventories, including many critical product inventories, toward all-time lows, and it may be time to position portfolios given the potential for supply shortages to emerge.

Rising bond yields curbed traders’ appetite for risky bets early Friday, sending stocks lower following a weeks-long record-setting rally driven by a rush of cash into all things artificial intelligence.

Investors shed government bonds around the world, propelling borrowing costs to multi-year highs from Japan to the US amid intensifying fears that war-driven inflation will force central banks to pursue higher interest rates.

AI is surely the zeitgeist at industry conferences across sectors right now. Emerging technology, increased efficiency, and scalability are all talking points. But so too are headcount reductions, reduced tech-sector free cash flow, and growing worries about a 1990s-like bubble.

What were the key takeaways from last month’s numbers? Our corporate bond specialists look back at the market’s performance and provide incisive commentary to help you make sense of what drove the market—and what may be on the horizon for fixed income investors.

Yields for preferred securities have generally risen more than corporate bond and long-term Treasury yields over the past few months, making them more attractive to investors.

Stock markets have been hitting all-time highs and credit spreads remain low, yet higher interest rates and mounting floating-rate debt are straining lower-rated borrowers. This tension is surfacing first in leveraged loans as “quiet defaults” become more common — opening up a dynamic set of opportunities for investors specialized in stressed and distressed assets.

It’s likely not a bubble. Earnings are high. Prices are high because they anticipate future high earnings growth. The historical record shows that growth rate is achievable.

April delivered a constructive backdrop for preferred securities, with the ICE BofA Fixed-Rate Preferred Securities Index rebounding 2.23% and bringing YTD returns back into positive territory at 0.8%.

Our reading is that this is a meaningful positive at the surface — a real-time confirmation that the most pessimistic recession scripts written in March can be set aside — but it is also a print that fails to alter the structural calculus we have been describing all year. The labor market is steady. The trajectory of fiscal policy, monetary credibility, and dollar reserve status is not.

US equity futures pushed higher early Wednesday as traders snapped up technology shares after a pullback in the group, with enthusiasm around strong earnings outweighing a resurgence in inflation.

Get ready each week with high-conviction insights that go beyond media headlines.

In the current market, broad healthcare exposure means navigating relentless regulatory pressure and drug-pricing reform, a combination that can erode returns quickly. To find true value in this challenging macro environment, investors are increasingly turning to cash as the ultimate truth-teller, specifically, free cash flow (FCF).

After going negative in March after the outbreak of hostilities between the U.S. and Iran, flows of gold into ETFs flipped positive again in April, with all regions reporting inflows of metal.

Early detection, I believe, is one of the smartest investments you can make, whether we’re talking about your portfolio or your health.

LPL Research explores how a potential Warsh-led Fed could reshape policy, Treasury markets, and volatility amid rising deficits and shifting demand.

The U.S. labor market demonstrated remarkable endurance in April, with job gains outpacing expectations and private sector expansion reaching its strongest point in over a year. As the Federal Reserve maintains a steady interest rate policy, the focus now turns to upcoming inflation and retail data to gauge the sustainability of this momentum.

DoubleLine Capital’s Jeffrey Gundlach is repositioning some of his funds for the extreme scenario that the US government could choose to restructure its debt in response to a potential future recession.

US stocks were on track for a record closing high, buoyed by semiconductor stocks, strong monthly payrolls figures and a US-Iran ceasefire that appeared intact even with overnight clashes near the Strait of Hormuz.

US employers added more jobs than expected for a second month and the unemployment rate held steady in April, indicating the labor market is holding up despite rising energy costs sparked by the Iran war.

Last week was the busiest week of Q1 earnings season, as close to half of the S&P 500 reported quarterly results including Microsoft, Amazon, Meta, Alphabet, and Apple. Alphabet stock jumped 10 percent on the back of strong results from Google Cloud and Gemini.

Dividends have historically been the dominant method by which companies returned capital to shareholders. Share repurchases have only recently surpassed cash dividends as the primary form of corporate payout in the United States. Investor interest in buyback strategies has grown rapidly as a result.

As equity markets transition into 2026, large cap equity portfolio managers share a surprisingly consistent framework — paired with sharp disagreements on where risk and opportunity sit. A survey of large growth, value, and blend managers reveals a market shifting away from simple narratives toward selectivity, fundamentals, and manager skill.

The generational divide is a part of the human condition – and the investor condition. It’s not just that one group has more experience than the other, or that one is more eager to make its own way, but that both groups can learn totally different lessons from the same event.

In a recent Market Outlook Symposium we hosted at VettaFi, we learned that 2026 has marked the return of fixed income as a strong contributor to an investor’s total return. We also learned that the biggest theme in fixed income investing this year is dispersion. Where you are putting your money to work matters.

Investors are piling into municipal bonds at the fastest rate in five years, drawn by attractive yields and the promise of a safe harbor from recent market volatility.

Deglobalization supports diversification: Reversing global trade reduces economic productivity, but the resulting decoupling of international markets increases the protective value of geographic diversification.

Thus far 2026 has been a roller coaster year for fixed income markets. The 10-year Treasury, the benchmark rate for the bond market, saw its yield trade as low as 3.94% and as high as 4.43%.

A persistent oil shock implies higher inflation and weaker growth, but risk assets appear unfazed, with equities and credit spread performance diverging from the caution implied by government bonds.

There is also a popular notion that bond traders can see the future, that they know what inflation will be or if a recession is coming. But bond markets are often wrong. And they may be wrong now because bond yields are low relative to the risks the economy faces.

The complication is that the ceasefires stopped the escalation without resolving the underlying disruption. The Strait of Hormuz, which carries roughly 20% of global oil supply, remains effectively closed. Oil prices fell sharply on the ceasefire announcements (including the largest single-day decline since 2020), then climbed back above $100 per barrel.

Last week’s data was a good reminder that we are likely in a “resilient but uncertain” phase of the cycle.

April showers came in the form of more inflows raining down on the exchange-traded fund (ETF) market last month. Assets under management (AUM) have now grown to a staggering $14.7 trillion for the year. That’s punctuated by year-to-date (YTD) net inflows of over $636 billion.

What a week this was! On Tuesday, I participated on a panel at the Bitcoin Conference in Las Vegas, where I discussed why Bitcoin miners have a head start in the race for AI compute.

The Federal Reserve held rates steady as expected last week, but the real story was the shift in tone inside the Committee. Three dissents in favor of moving to a neutral bias are highly unusual, and I do not recall seeing dissents on a bias in this way before.