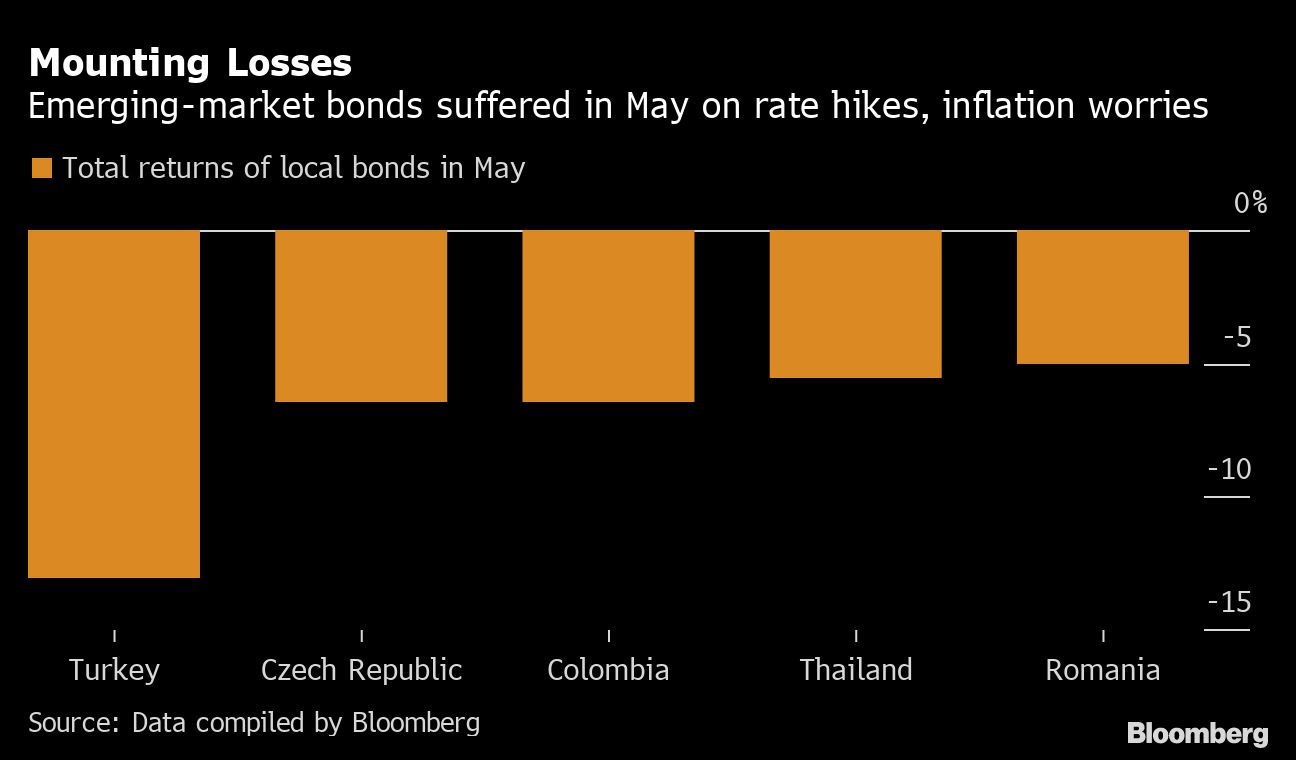

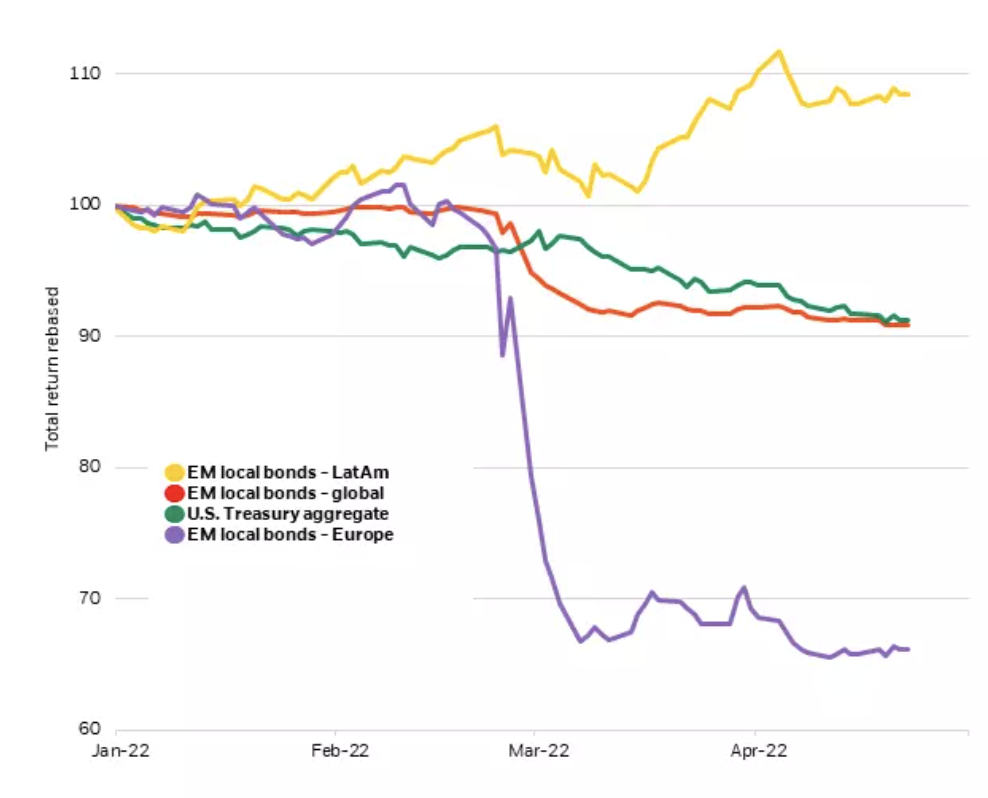

Local-currency debt from developing nations -- which is far more sensitive to a country’s domestic inflationary pressures than dollar denominated equivalents -- has slumped almost 9% this year, the most since at least 2008, according to a Bloomberg index.

U.S. stocks are trading lower as another week begins on the heels of six-straight weekly losses for the S&P 500.

When life gives you lemons: sell them!

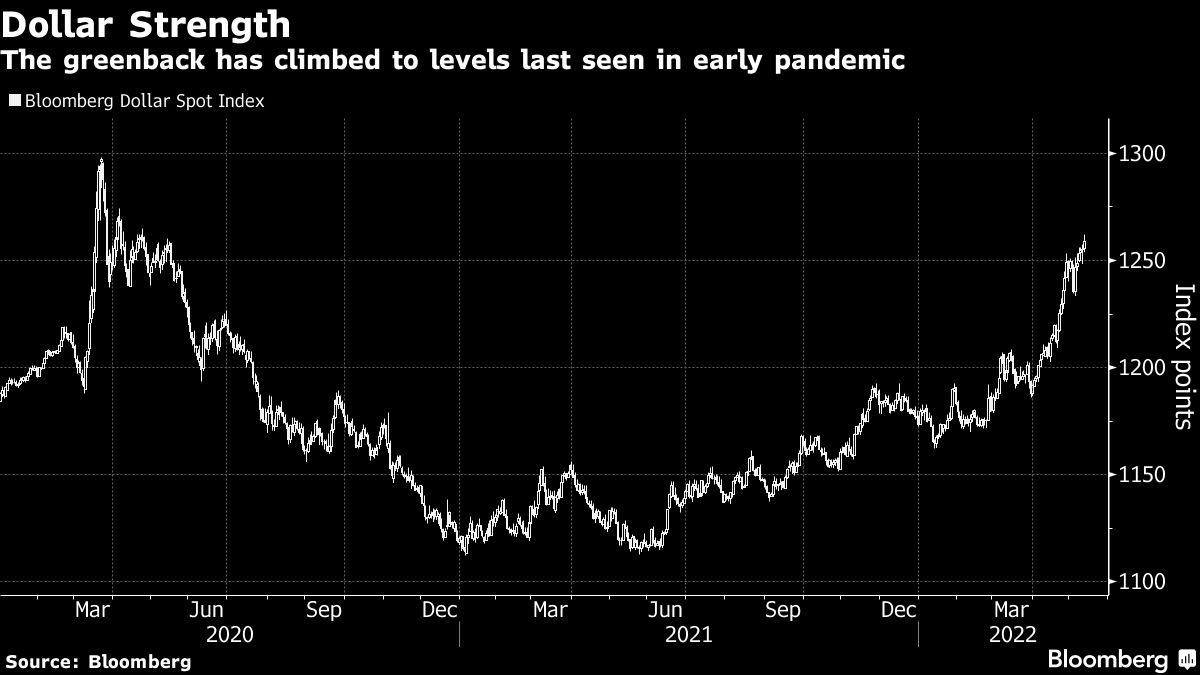

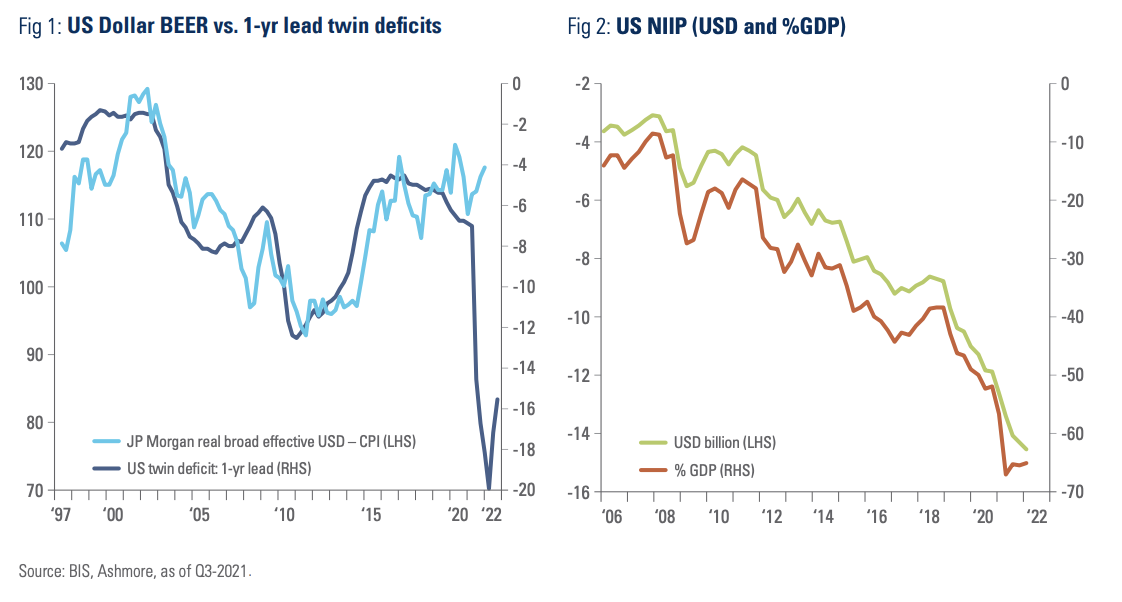

The soaring dollar is propelling the global economy deeper into a synchronized slowdown by driving up borrowing costs and stoking financial-market volatility -- and there’s little respite on the horizon.

Some big-name investors forecast that Bitcoin will eventually hit $100,000, $1 million or more. It could very well do that, but for now, its price is closer to $0. That’s both a risk and an opportunity.

Rising yields, wider spreads, and heightened market volatility are providing an attractive environment, but caution in credit selection is warranted.

Stock markets continued to sink following last week’s recession worries, fueled by the Federal Reserve’s rate decision and the threat to global growth from China’s continued Covid lockdowns. The fear could be seen across asset classes, as traders offloaded equities and other risk assets in favor of cash.

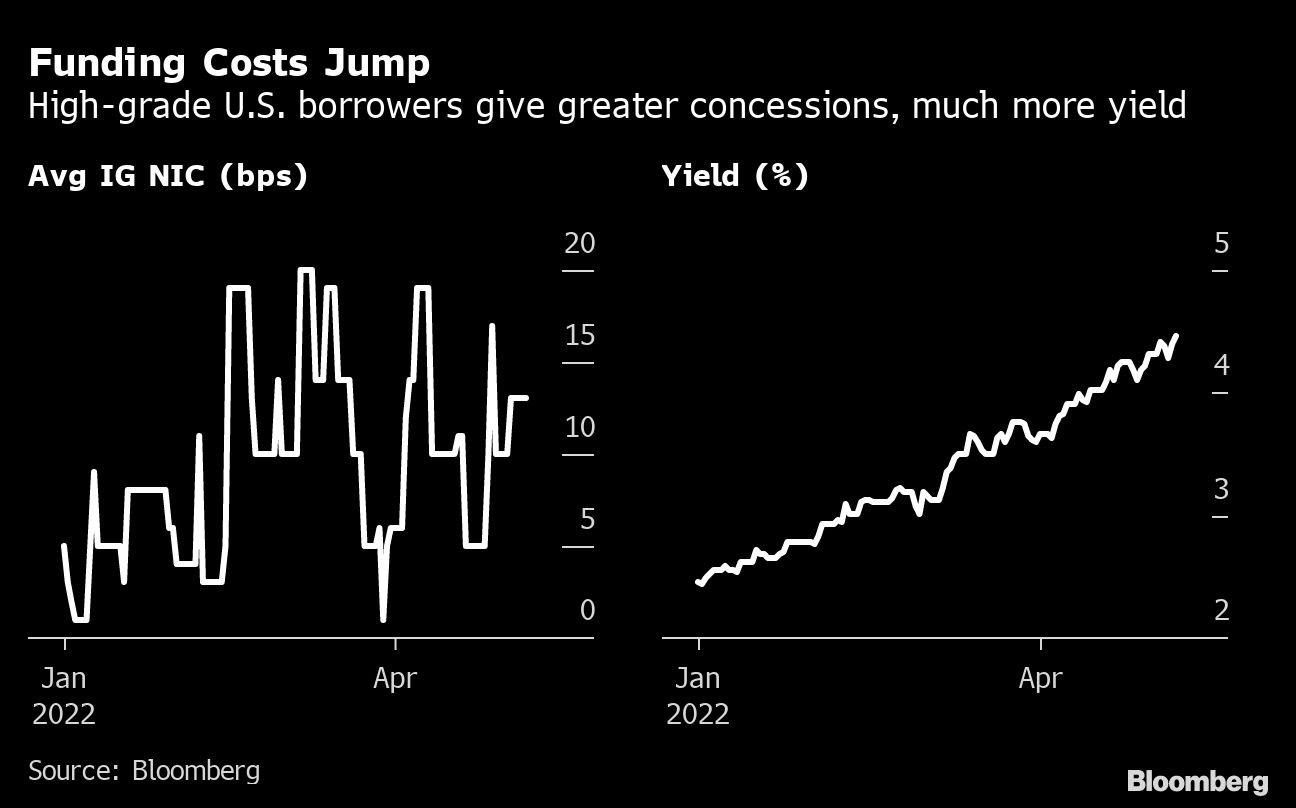

U.S. investment-grade debt sales have missed Wall Street estimates for two consecutive weeks with issuers choosing to sit on the sidelines instead of braving volatile markets. Bond sales were expected to pick up this week amid a growing backlog, but seven potential issuers opted to stand down amid broad volatility on Monday.

Advisor Perspectives has announced its Venerated Voices™ awards for commentaries published in Q1 2022.

With volatile markets fraying investors’ nerves, companies are now paying the biggest premiums to sell new bonds since the height of the coronavirus pandemic two years ago.

The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.63%. The S&P 500 Stock Index rose 0.40%, while the Nasdaq Composite fell 1.02%. The Russell 2000 small capitalization index lost 0.28% this week.

I borrowed this letter’s “Soft Now, Hard Later” headline from Dave Rosenberg. It was the title of his leadoff SIC presentation, for reasons I’ll explain.

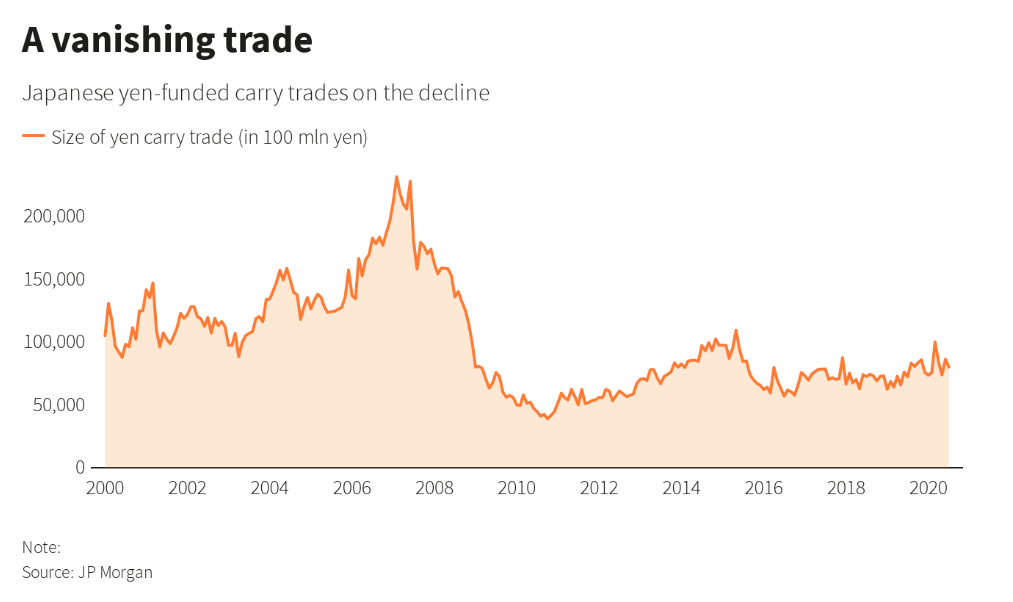

The BOJ is trapped. It is conducting unlimited QE to keep rates low and weaken the yen, which promotes inflation.

The push-and-pull between centralization and decentralization is the great contest of our times. And decentralization is winning out.

Sensient is a leading global maker of colors, flavors and specialty ingredients for the cosmetic, food, and pharmaceutical industries.

Inflation and hawkish central bank talk have spooked investors and led to bond losses not seen since the 1980s in developed markets (DMs).

With France’s polls closing yesterday Emmanuel Macron will now serve a second consecutive term as the president of France, the first to do so since Jacques Chirac in 2002.

As chief architect of the finance industry’s biggest climate coalition, Mark Carney said banks and asset managers are doing a better job at steering capital away from fossil fuels than is implied by what he described as “clickbait” headlines.

On May 29, Colombia could elect its very first leftist president should Gustavo Petro receive a majority of the vote. The former congressman and mayor of the capital city of Bogotá, Petro is an unabashed admirer of and Hugo Chávez.

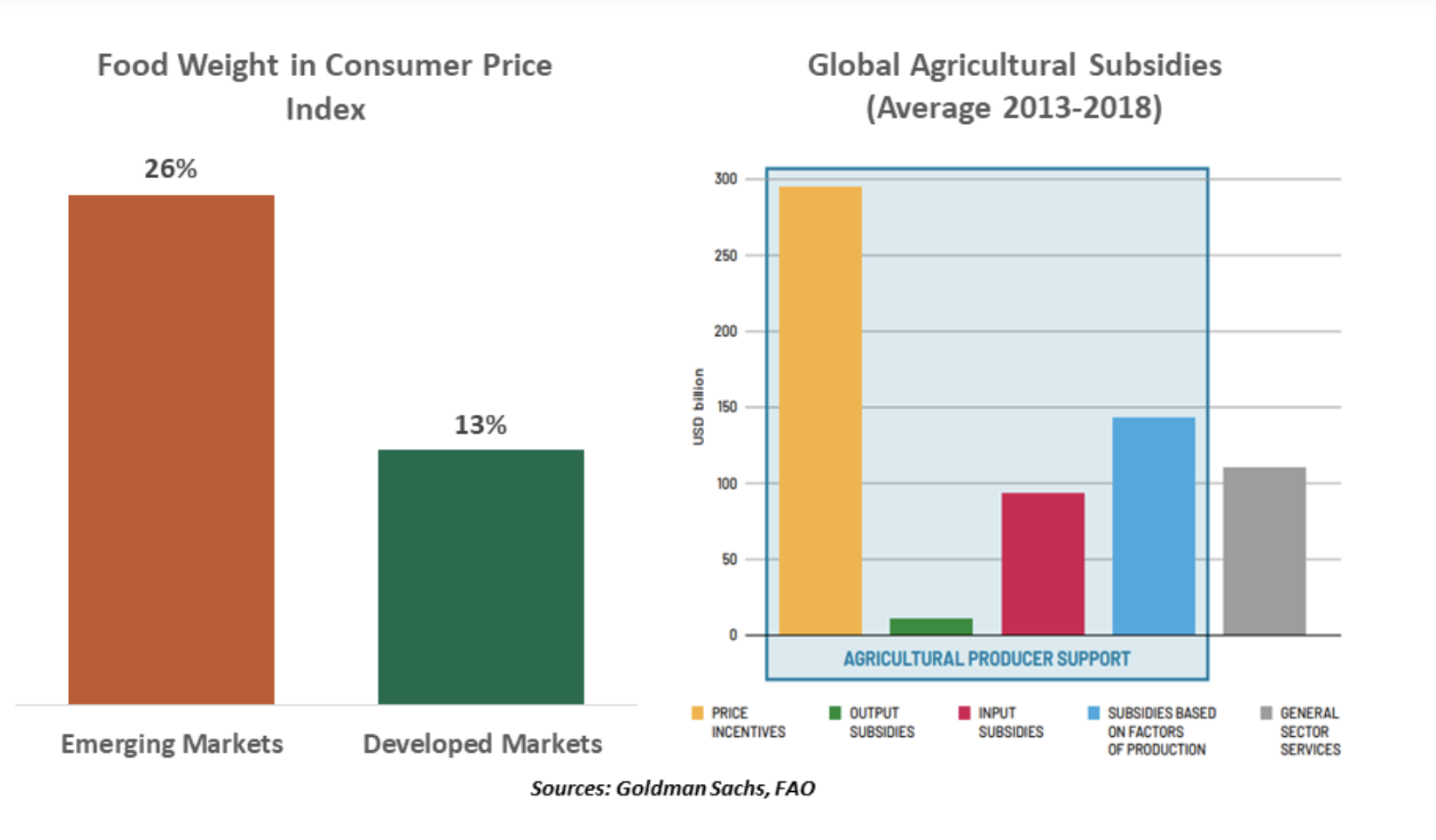

It might seem at first that everything is against emerging markets.

Concerns about the Ukraine war, inflation, and the Fed were top of mind last quarter, but a lesser appreciated long-tern headwind is the de-globalization of the labor force, which could have profound effects on the economy.

Despite gloomy news out of China, Andy Rothman explains why he remains optimistic about China’s road ahead.

Real Treasury bond yields fell into deeply negative territory in 2021.

Many of you are struggling to decide whether you should breakaway and form your own RIA. I confronted the same decision many years ago. Here’s my story.

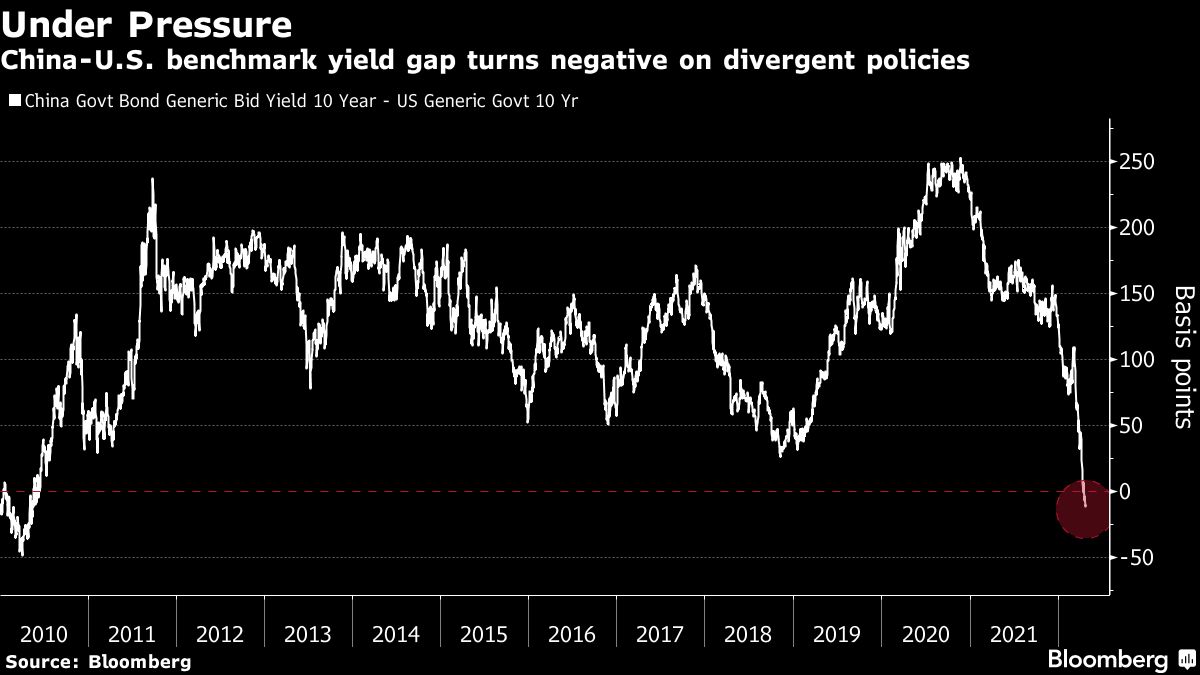

Asia’s two biggest central banks are having to grapple with the fallout from the Federal Reserve’s hawkish pivot.

The war in Ukraine has further complicated the investment backdrop, and fears of a recession are rising now that the U.S. yield curve has inverted. Given so much uncertainty, we are focusing on what we can control and maintaining a defensive posture

The fastest inflation in decades and the resulting rush by central banks to raise interest rates are stoking recession fears in financial markets -- worries that are being compounded by the impact of aggressive coronavirus lockdowns in China and the war in Ukraine.

The war in Ukraine has contributed to inflation in the short term, but there’s much more to the story, which began way before Russia invaded its neighbor.

The Northern Trust Economics team shares its outlook for growth, inflation and interest rates.

The war in Ukraine is shifting the conversation on what a post-COVID-19 world will look like.

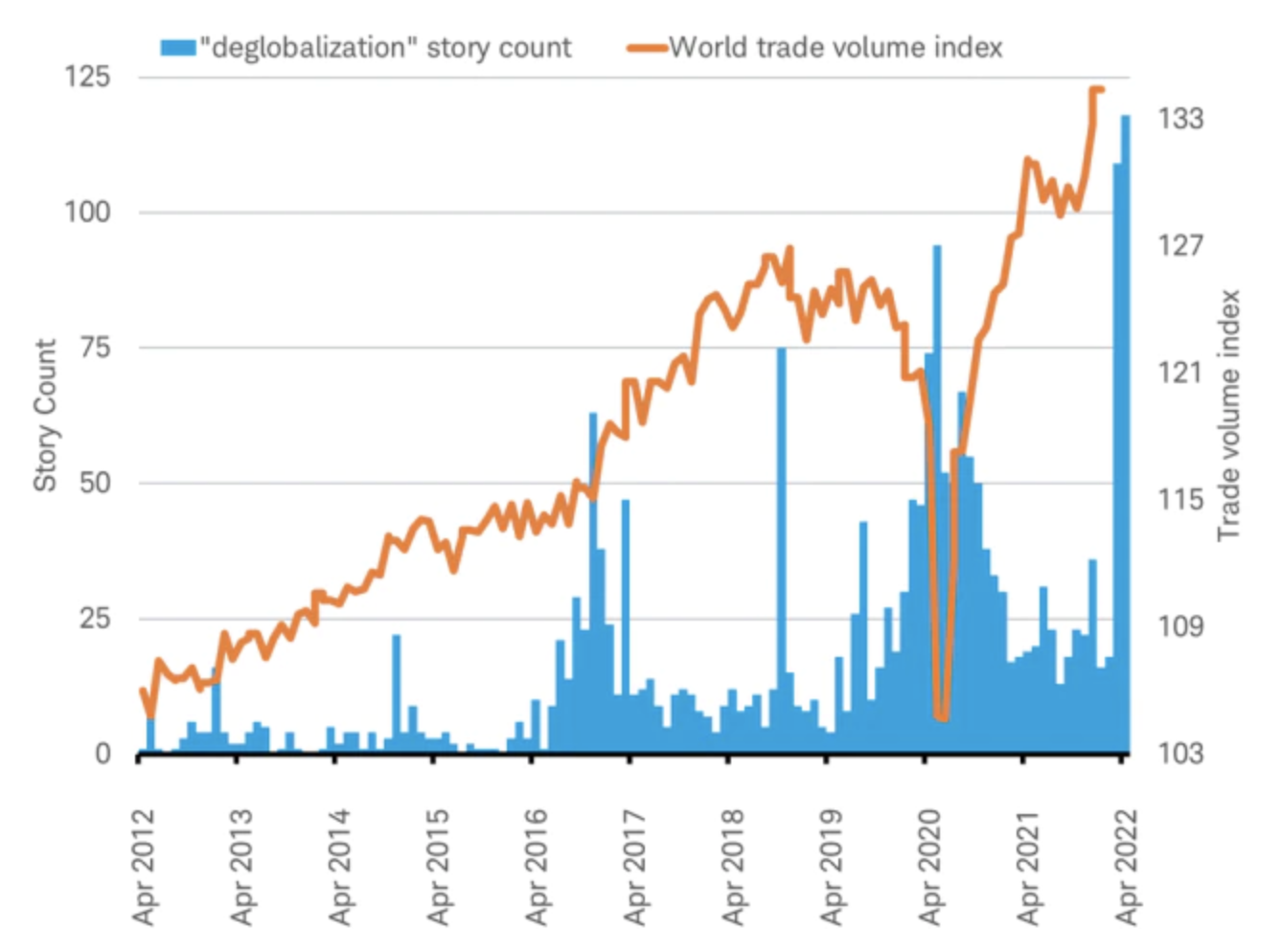

The "end of globalization" is a phrase that has come up a lot lately.

The search for havens from the worst inflation in four decades feels like it’s about to get a lot more real. The bad news is that the task isn’t looking at all easy or straightforward, at least for individual investors whose choices are confined to the standard asset classes and who rely on a traditional 60-40 portfolio mix of equities and bonds to weather the ups and downs of market cycles.

An estimated 30,000 people attended this week’s Bitcoin 2022 conference in Miami, which is rapidly becoming a major global crypto-finance hub.

A “soft landing” scenario is not so straightforward in the current context. We have emphasized companies that we believe have pricing power because of the mission-critical or value-add nature of their products and services.

As a solar panel was raised onto the roof of their mud-brick home in a Tanzanian village in sight of Mount Kilimanjaro, Akida Saidi and his wife felt giddy at the prospect of entering a new era. In a place where most residents make do with pit latrines instead of toilets and till their fields of maize and pigeon peas with hoes, suddenly having electricity would catapult them into the 21st century.

John Vail, Chief Global Strategist at Nikko Asset Management, discusses Nikko AM’s Global Investment Committee views on current global market drivers as well as expectations for the markets moving forward.

The first quarter of 2022 brought violence that rocked communities – and markets – internationally. We look at what aftershocks may still be yet to come.

Diverse opportunities in Global Convertibles, as well as structural features, provide tailwinds to counter rising rates and equity volatility. In rising rate environments, convertibles have historically done quite well relative to longer-duration traditional fixed income investments.

CIO Robert Horrocks, PhD, examines the ramifications of Russia’s invasion of Ukraine on China’s trade and economic strategy and the implications the conflict has for Asia’s development and markets.

Banks are gearing up to offload billions of dollars in junk debt backing leveraged buyouts, counting on the nascent stability in the market to finally get rid of underwrites for businesses such as Wm Morrison Supermarkets Plc and Unilever Plc’s tea unit.

The poor performance of factor-driven value strategies over the past decade has raised the question of whether intangible assets, such as patents and proprietary software, are properly treated. New research confirms that intangibles indeed distort valuation metrices, but there is no consensus on how to address the problem.

Globalization in all its forms, from social to economic to political, has been on the rise since about the 1970s, and I genuinely believe it’s had more benefits than drawbacks on average.

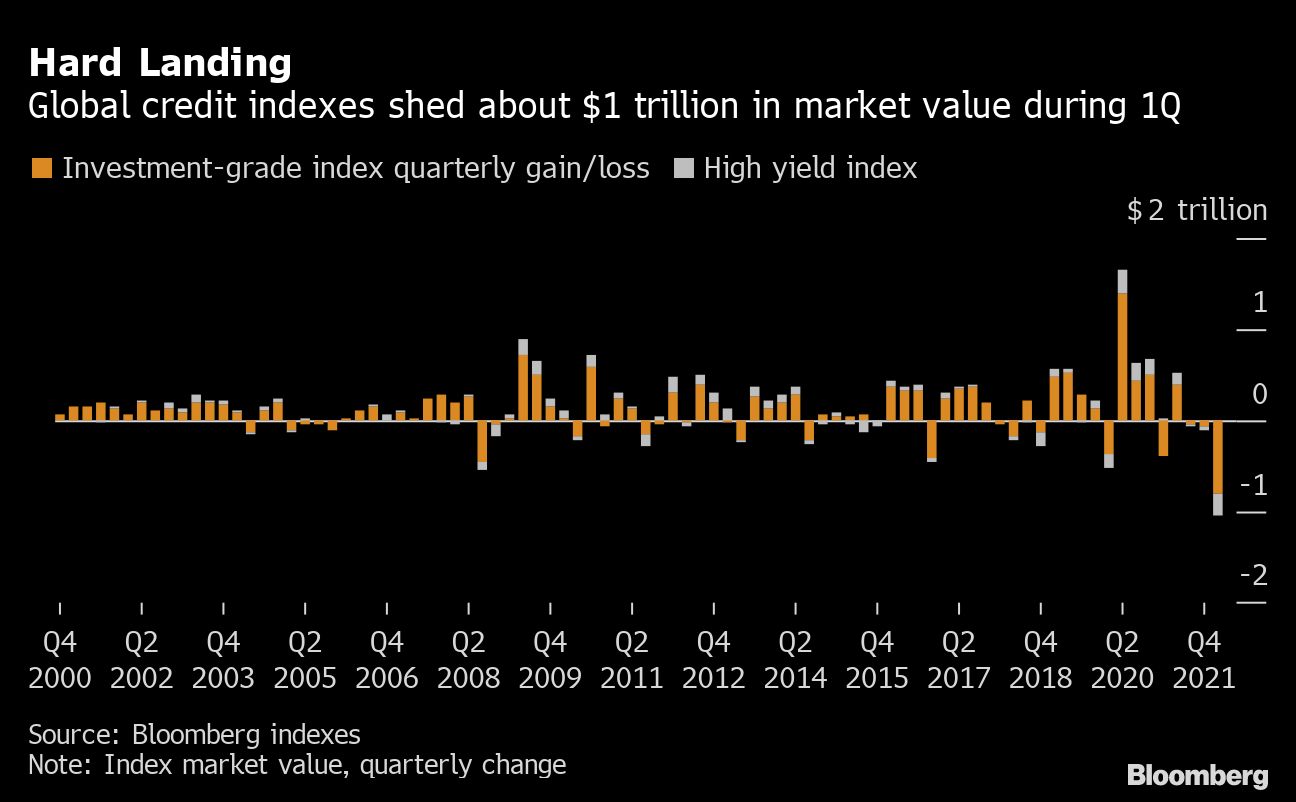

Investors in corporate bonds are bracing for more trouble after getting hammered by rampant inflation and rising yields in the first quarter.

Supply chains set to become less dependent on China over time.

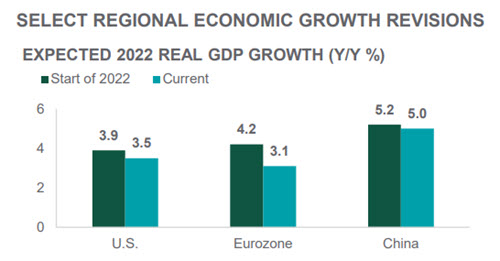

War in Europe comes at a time when the global economy was just emerging from the COVID-19 pandemic.

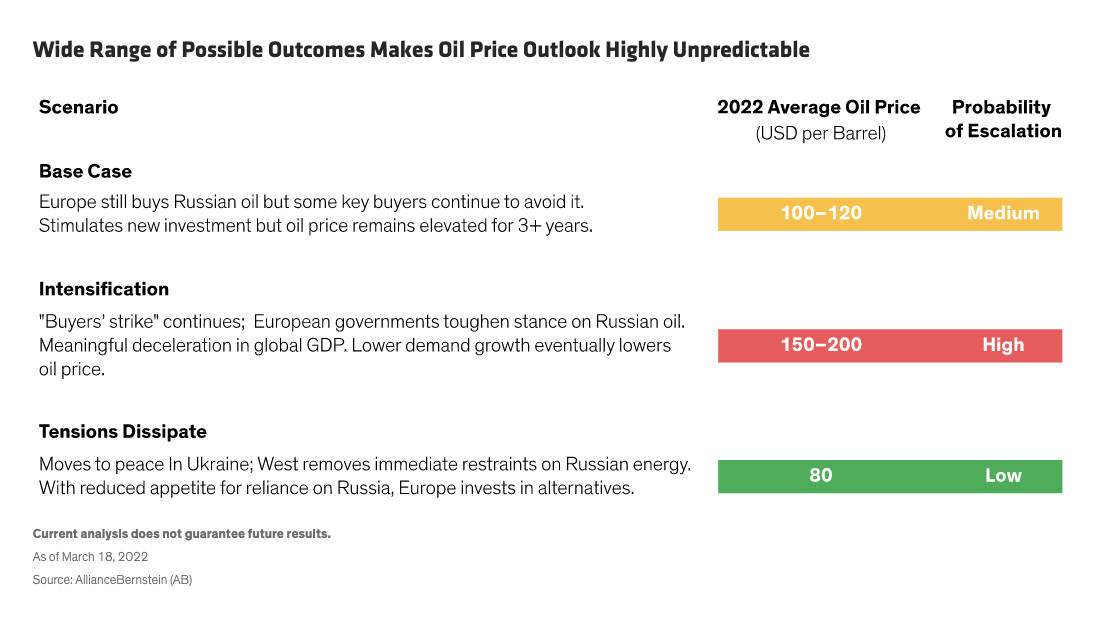

Russia’s power on the world stage is supported by its vast reserves of oil and gas.

Get out of stocks, according to Gary Shilling, who has gone to 30% cash in the portfolios he manages. The economy will be in recession by the end of the year, and stocks will fall in response.

ICYMI: In this roundup, we’re highlighting the five most popular pieces of content from the previous week.

The Russian invasion of Ukraine is a shock to the existing world order. From an economic perspective, the initial impact of the war is rising inflation given the importance of Russia and Ukraine in the supply of commodities to the world.

The halt of Russian equity markets, the prospect of higher U.S. inflation and rising interest rates are all contributing to uncertainty in emerging markets. How should investors navigate these headwinds and what could the impact be to markets in Asia, Europe, and Latin America?