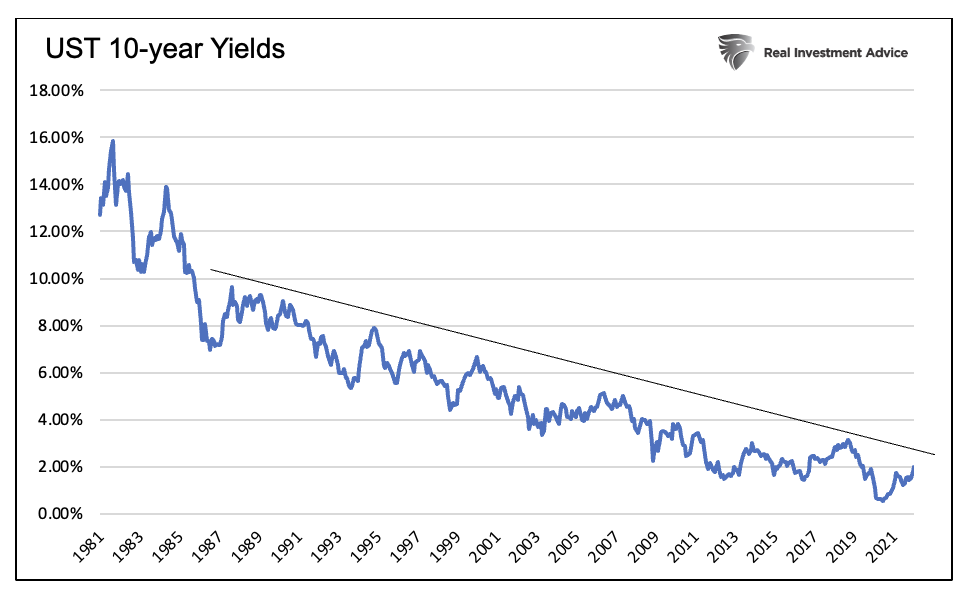

Investors continue to need a balanced portfolio, including fixed income. But the bond markets are challenging: Rates are low, duration risk is high, and runaway inflation is putting pressure on long-term rates. “Buy and hold” fixed-income strategies will not work as well as they have in the past. A better alternative is a tactical, disciplined approach to when and how to invest in fixed income.

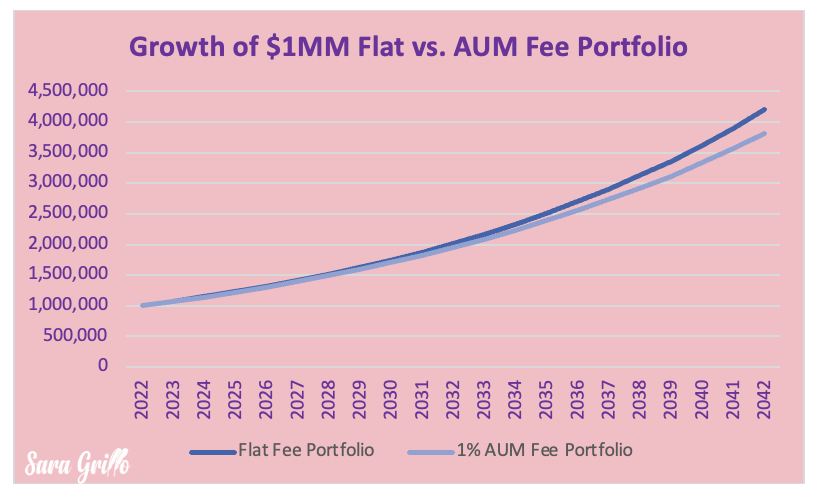

I’ll take an order of flat fees (otherwise known as retainers) with a side of financial planning. Customers are lining up out the door for this.

“Cash Is Trash” is a common theme as of late as inflation rages from the massive monetary interventions of 2020 and 2021.

You’ve researched the nuts and bolts of cryptocurrencies and considered whether you should invest in them.

Actively managed global allocation funds claim that skilled investment managers can produce a superior rate of return compared to traditional index funds. But the reality does not match the hype.

Recession is where we are headed. So let’s review what it will be like.

Quick – where were you 25 years ago?

On March 1, two unrelated Securities & Exchange Commission actions set out the state of its thinking on enforcing the “best interest” and “fiduciary” standards.

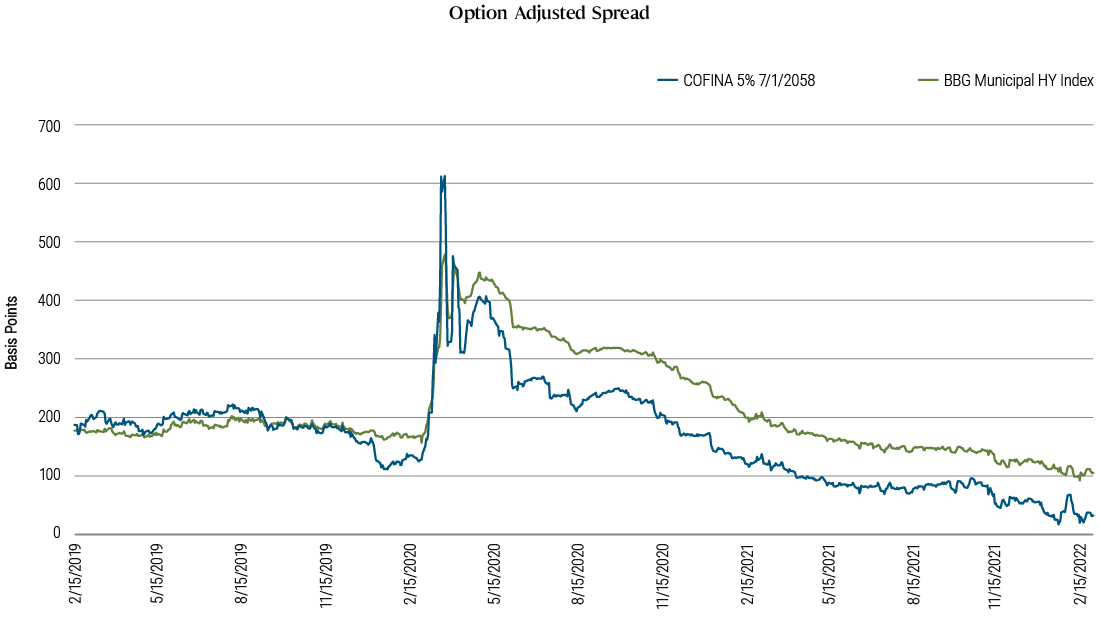

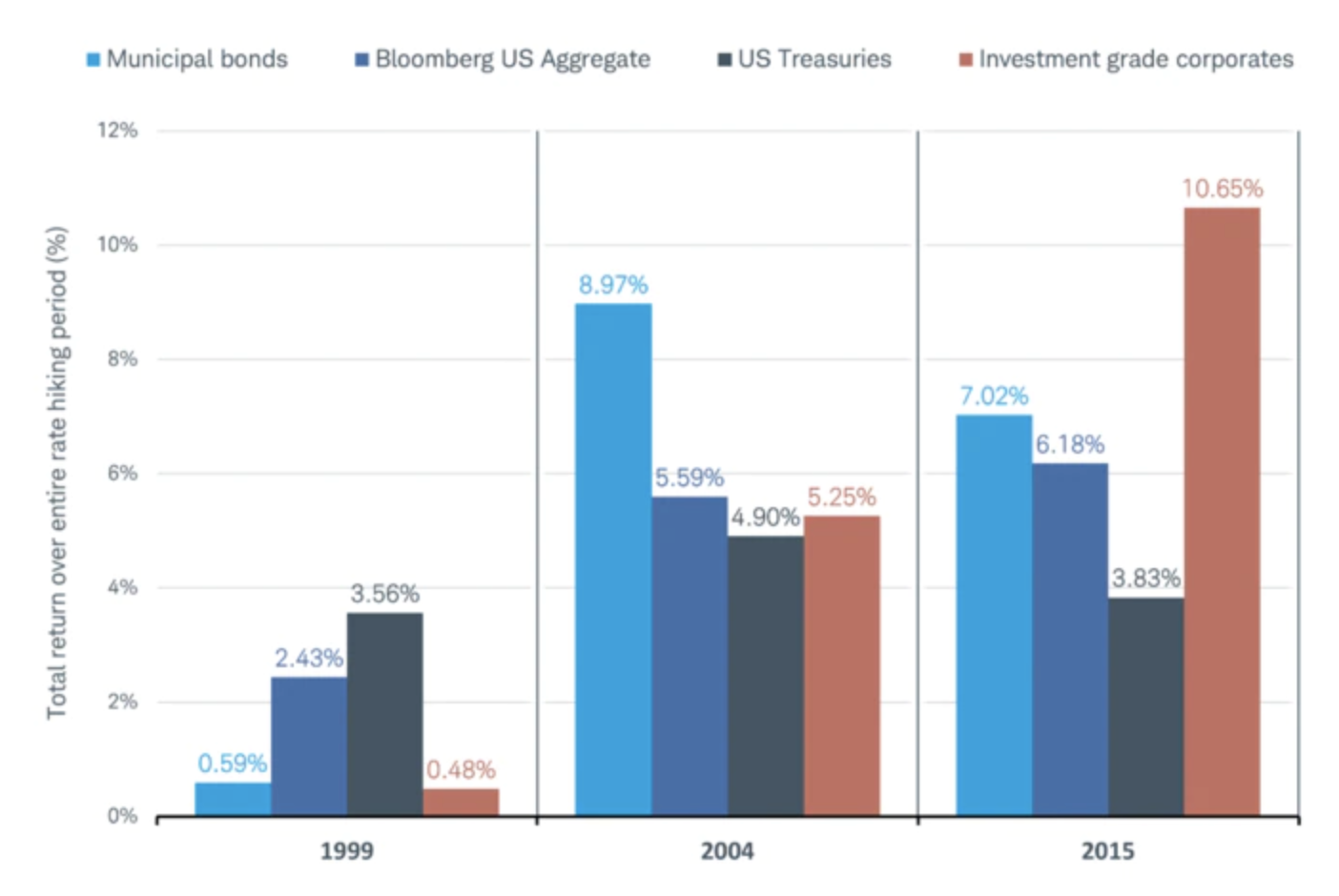

Restructured debt has often outperformed the broader municipal bond market as issuers emerge from bankruptcy with higher debt-servicing capacity.

Over the last 10+ years, U.S. equity outperformance has been caused by increased profit margins, the accretive impact of share buybacks, dollar weakness, and most significantly, an outsized expansion in equity multiples. There are risks to all of these sources of outperformance, suggesting that a neutral long-term strategic allocation to U.S. equities is now likely warranted.

The live-streaming of Ukrainians' suffering as Russia wages an unprovoked war on the country has outraged much of the world. Governments are leveling devastating financial sanctions on President Vladimir Putin for his aggression, and many Americans are looking for ways to do their part.

The same morning Russia invaded Ukraine, the people running the Church of England’s $5 billion pension fund decided they’d seen enough, and quickly went to work to clear their portfolio of Russian investments.

This article, which is written for clients, explains that direct indexing portfolios are broadly diversified with individual stocks that are personalized to meet the needs, values, and preferences of an investor.

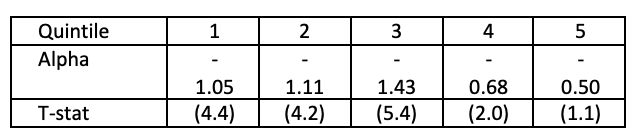

The academic evidence against active management is mounting. New research shows that information is incorporated into security pricing far too quickly for investors to profit from it.

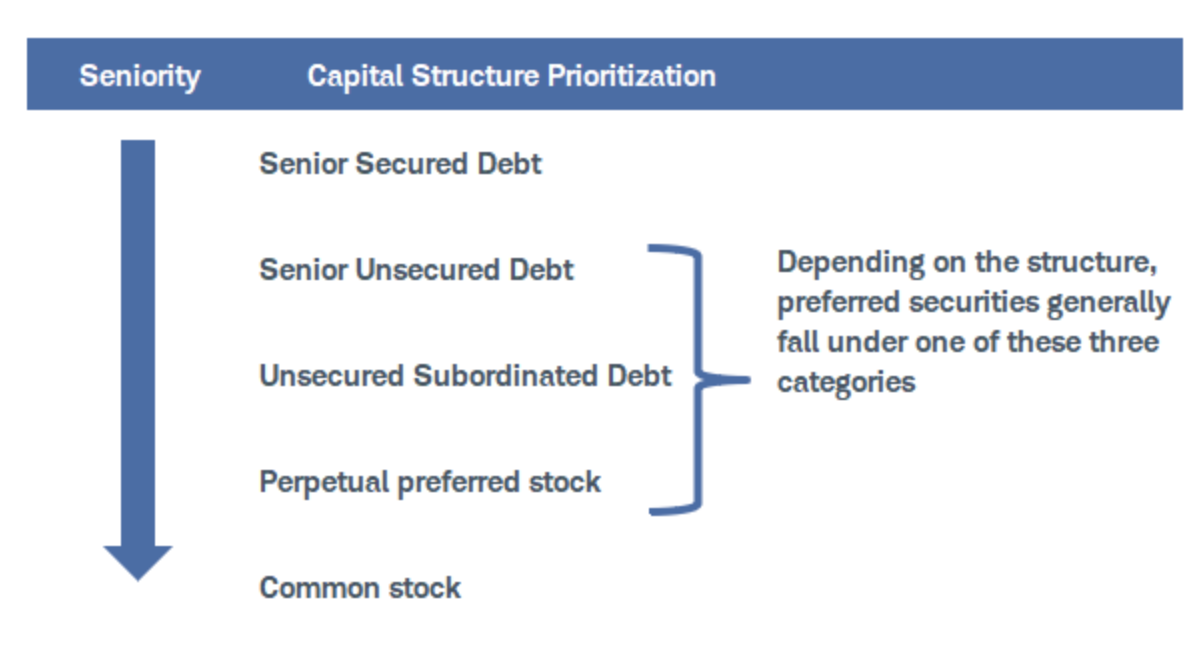

Preferred securities are a type of investment that generally offers higher yields than traditional fixed income securities, such as U.S. Treasury securities or investment-grade corporate bonds.

I propose a strategy that can produce larger price gains or losses than bonds and higher yields than traditional bond funds or ETFs. If yields decline soon, investors can expect double-digit returns in a relatively short period.

Since the initial publication of research documenting active share, its advocates have clung to the belief that the metric could identify funds that would outperform. But the academic evidence has all but disproven that thesis.

With many mutual funds converting into exchange-traded funds (ETFs), the combination of ETF trading and net asset value is garnering more attention.

A crash to Earth for growth stocks and cryptocurrencies is one thing, but a sharp decline in mainstream bond mutual funds could spell enormous trouble. Signs are emerging of the beginnings of a potential downward spiral in these funds, which could ultimately lead to redemption halts and subsequent panic by retail investors.

The term “value” is being grossly misapplied.

In the past year, a large number of climate-focused funds have launched. Some invest in companies seeking to lower their carbon risks, while others steer assets to companies developing innovative solutions to climate change. And, sometimes it’s a combination of both.

As we begin 2022, there is a lot of noise in the marketplace: midterm elections, omicron and everything in between.

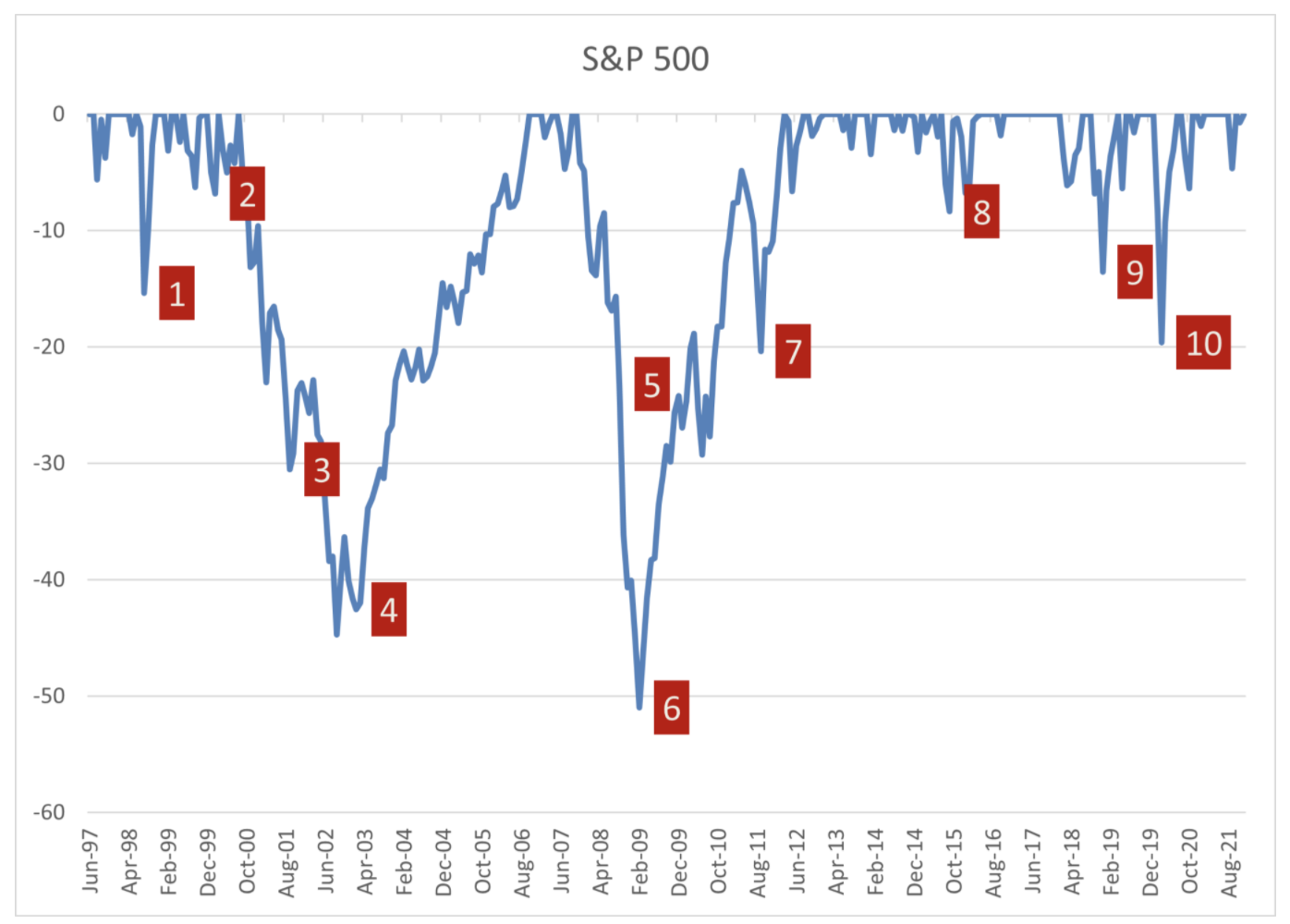

From 2008 onward, U.S. market returns have been strong and consistent, and 2021 was no different, with the S&P 500 returning a solid 29%.

We have never seen anything like this. Governments and their central banks injected approximately $30 trillion of fiscal and monetary stimulus into the global economy from February 2020 to the end of 2021.

The Federal Reserve has indicated it plans to start raising short-term interest rates soon.

So-called “green” stocks that have a good environmental, social and governance (ESG) profile have lower expected returns. But new research shows that they also have less risk and similar risk-adjusted returns to “brown” stocks.

Investors have already started positioning for a new Fed tightening cycle as well as sticky inflation. Many are rotating into real assets, including gold and real estate, which have inherent value outside of the traditional financial system.

ETFs are a negligible owner of US stocks. Primary and secondary ETF trading has not grown quicker than total stock trading. The impact of ETFs on stocks is less strong than frequently suggested.

The term direct indexing is somewhat of a misnomer.

Companies are buying raw and intermediate goods at a record pace, which we believe will influence economic growth in 2022.

A portfolio’s return is driven by its investment strategy—a set of decisions that governs allocation and timing of capital among the portfolio’s positions.

With January being a month for prognostications, David Mann, our Head of Global Exchange-Traded Funds (ETFs) Capital Markets, shares his annual outlook for the ETF industry and key trends he sees taking shape in 2022.

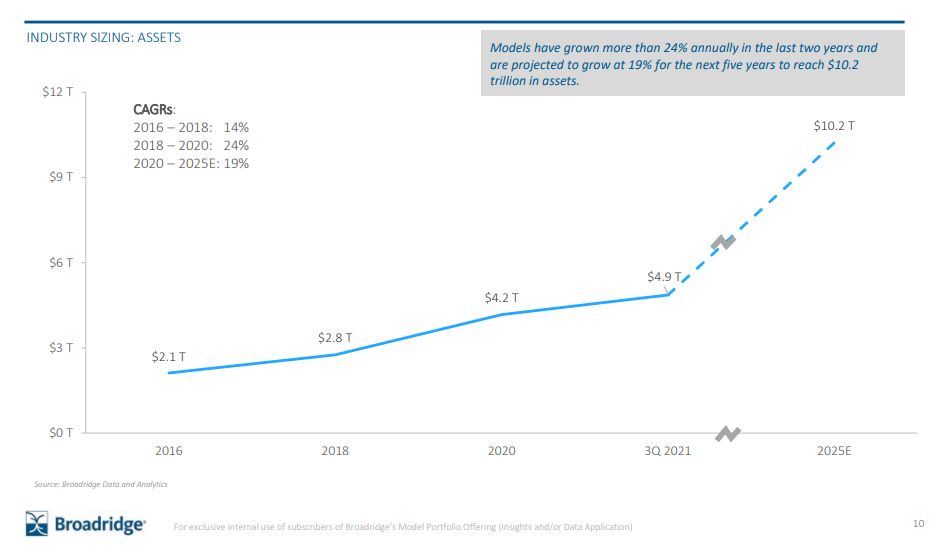

A booming $4.9 trillion branch of the U.S. asset management industry is funneling investor cash into funds that are pricier and worse-performing than alternatives, new research claims.

Passive ETFs are hiding a bear market in stocks.

Impact investing seeks to achieve social good, but new research shows that it has had a negligible effect on the cost of capital for so-called “brown” companies.

Investing in ESG funds is like trying to navigate “the Wild West” as both regulations and enforcement fall short, according to Andrew Behar, the chief executive of As You Sow.

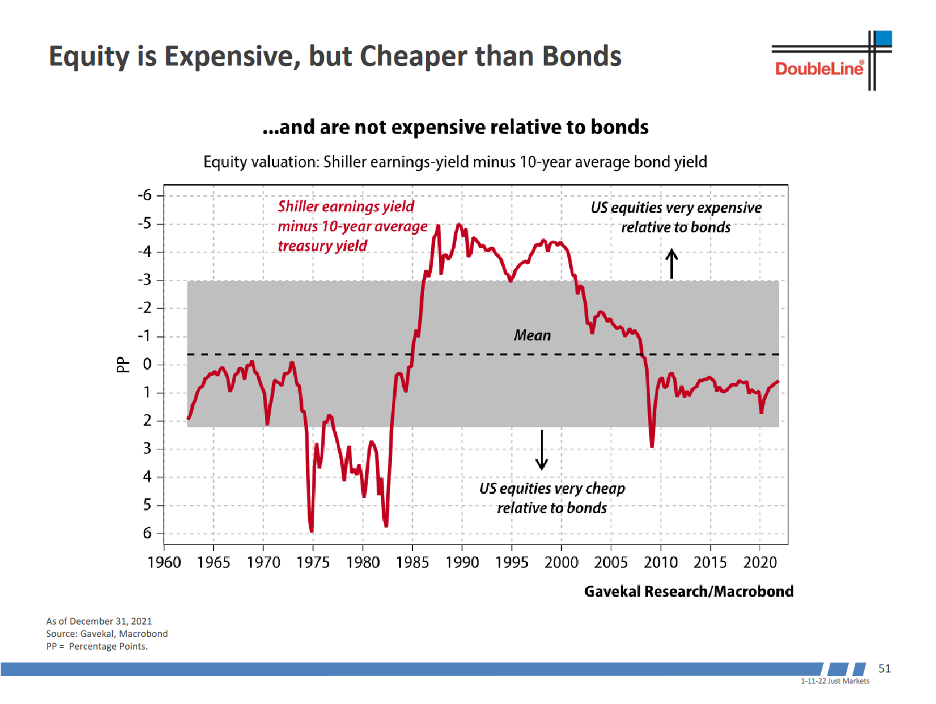

Monetary policy has driven U.S. stock prices to excessive valuations, according to Jeffrey Gundlach. But they remain cheap relative to bonds.

Assuming the value that clients obtain from an advisor is distributed in a bell-shaped curve, the average client obtains considerable value from the average advisor – and even from a mediocre one.

Leveraged loan supply and demand experienced a banner year in 2021.

I predicted that 2021 would be a transitional year for managing an advisory business, and I expect this transition to accelerate and become fully formed in 2022. These are the changes that I envision for the coming year and beyond.

Finding the right professional to manage your finances is challenging. Financial professionals have many different titles, certifications and qualifications, but which type is right for you?

Equities have enjoyed strong gains since the pandemic low of 2020, aided by massive monetary and fiscal stimulus, excess consumer savings, and incredibly negative real policy rates and bond yields.

Soon – within the next two years – the SEC will wake up and start holding financial advisors who use TAMPs to the same fiduciary standards they hold them to in selecting mutual funds, ETFs, and other investment products. When it does, many advisors will be in trouble.

Northern Trust, one of the world’s largest asset managers, foresees 2022 as a year of transitions. Central bank fiscal policy might become less accommodative or stimulative through a reduction in bond purchases. After years of virtually no inflation, investors are becoming more aware of the importance of hedging against it, given its recent sharp emergence. While there are indications of inflationary pressures decreasing in key supply chain bottlenecks, this is countered by strong housing and labor markets.

New research confirms that investing with an environmental, social and governance (ESG) mandate does not lead to higher risk-adjusted returns. But investors will reduce exposure to climate-related risks and get the “psychic” benefit of making a positive impact for society.

In this interview, Spencer Logan discusses Harbor Capital’s recent launch of an active transparent ETF that uses a scientific approach to fixed income investing.

As the end of 2021 draws near, investors are pleased with the impressive performance posted by most asset classes, but we are still awaiting the transition to the endemic state of the virus.

The purpose of this whitepaper is to highlight the development of values-based investing at a summary level and, more importantly, provide research that indicates there is no sacrifice of investment returns in adopting a faith-based approach to values investing.

What might equity investors expect in 2022? Active stock picker Tony DeSpirito reviews the potential positives and impediments in his Q1 market outlook.

It’s well studied that factors like debt and financial uncertainty impact the way people feel about retirement and prepare for it. In this series, BlackRock explores insights from our 2021 DC Pulse research and additional work with the Employee Benefit Research Institute (EBRI) to recognize inequitable effects and find ways to build a better retirement for all.