June of 2024 was a good month for financial markets. Leading the pack were (again) technology stocks, with the NASDAQ up 6% on the month. Close in second place were emerging market ex-China stocks, largely driven by India, Taiwan, and South Korea, all of which had large rallies in the month.

After a weak April, markets bounced back in May, with the S&P 500 staging a breathtaking rally in the final few hours of trading on Friday, May 31.

Relative to 18 developed economies since 1870, U.S. leverage is high though not unprecedented. However, unless the recent rise in interest rates reverses, the U.S. will need to cut its debt load.

From the end of March until the end of April, the market had a serious rethink about the path of monetary policy for the rest of 2024.

TIPS offer inflation protection, but at the cost of higher volatility and lower returns in bad times (when inflation is low). TIPS behave somewhere between corporate bonds and nominal Treasuries.

Many asset allocation strategies operate at the level of industry groups. Industry momentum -- buying past winners and selling past losers -- is present in U.S. data going back to the early 2000s.

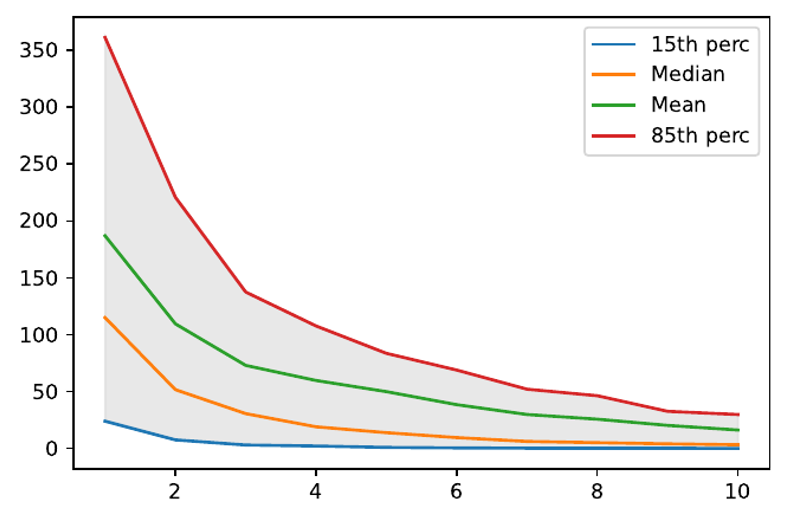

I asked Google's Gemini LLM to opine on the historical drawdowns of the Nasdaq 100. The results, though not perfect, are good enough that investors need to start paying attention.

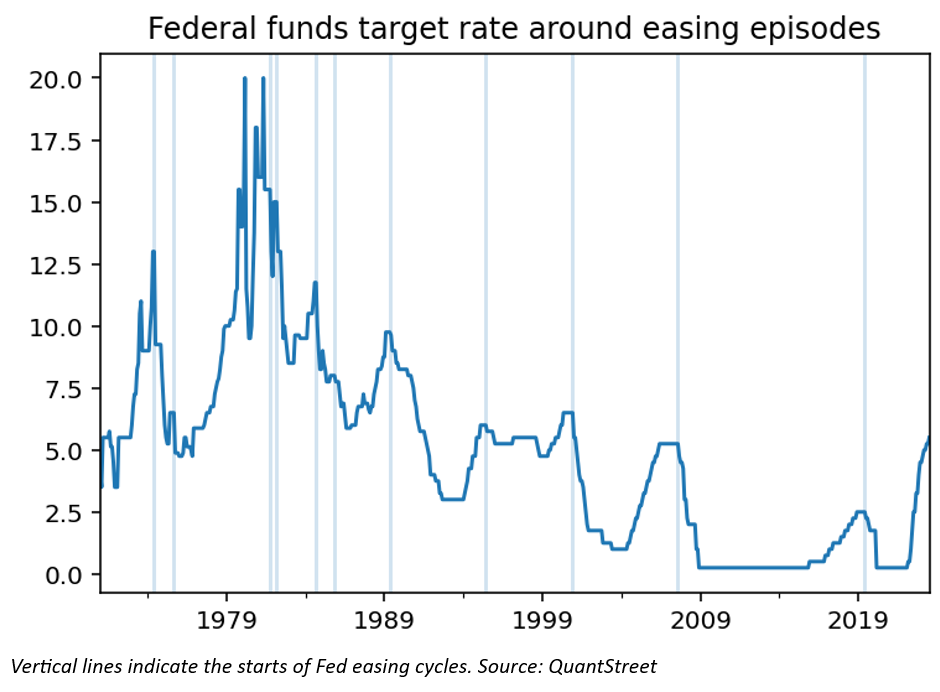

Gold prices have done well around Fed easing cycles. In addition, inflation concerns and high interest rates make the year-ahead gold return forecast attractive.

People like to compare price run-ups of tech stocks to what happened to Enron. The implication is that, since Enron failed, these companies will as well. But this argument does not work.

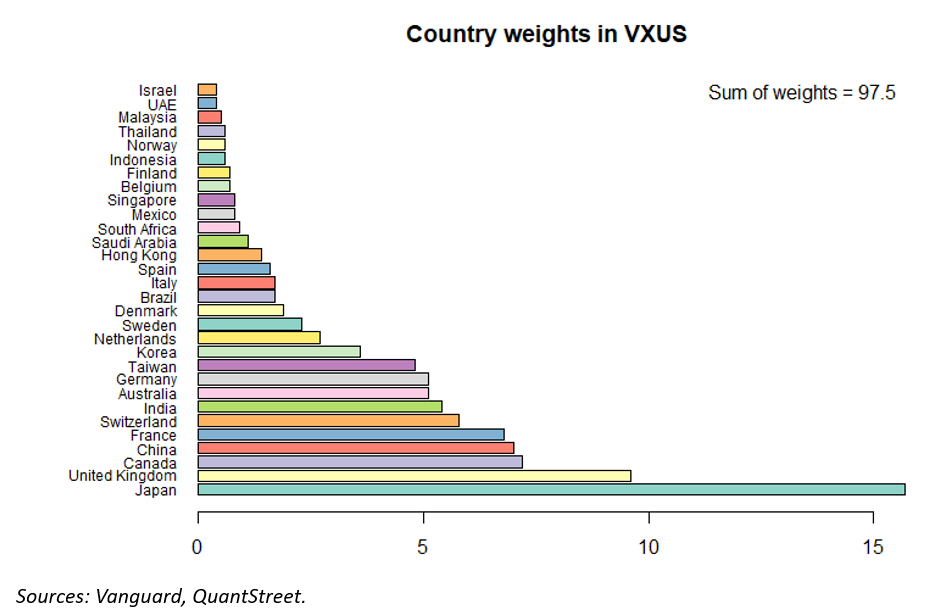

Academic work shows that openness, rule of law, and legal protections are associated with investor inflows to global stock markets. Based on such considerations, non-U.S. stocks don't look very good.

Advisor Perspectives recently asked its community they are recommending the new spot bitcoin ETFs. Many made incorrect statements in their efforts to justify their opposition.

Value investing is the lens through which many view financial markets. Yet, a simple value factor has performed poorly for the last 16 years. Is the value effect over, or will it come back in 2024?

I asked our authors and guest contributors the following question: Given the availability of spot bitcoin ETFs, would you recommend them (or any other cryptocurrency allocation) to your clients?

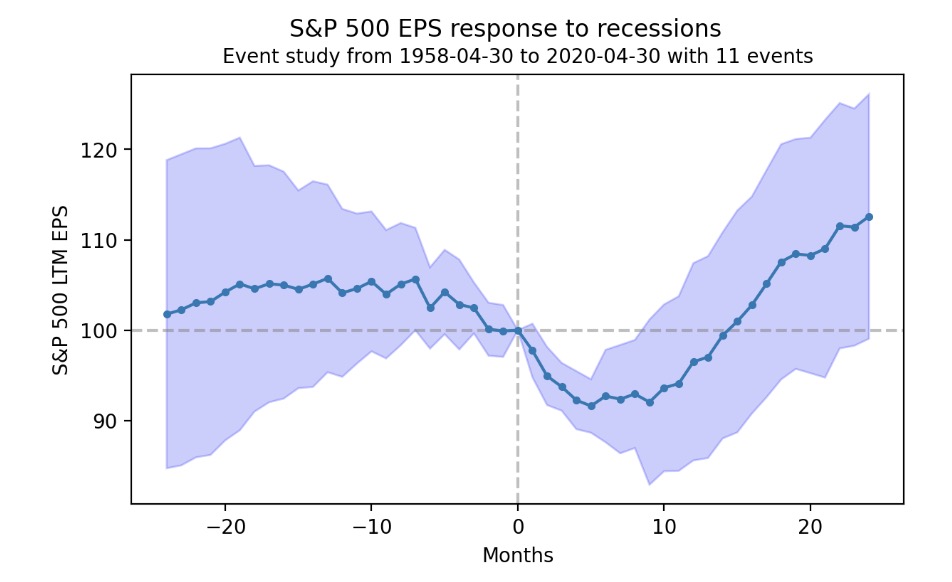

It was a heck of a year for stocks. In 2023, tech led the way with a return of over 40%, leading to concerns about overvaluation in the sector. Nonetheless, past sector booms have been associated with volatile, but on average positive, future returns.

In November, Treasury rates dropped, and risk assets rallied. The market expects continuing drops in inflation and slower, but not disastrous, growth. The data support the market's sanguine assessment.

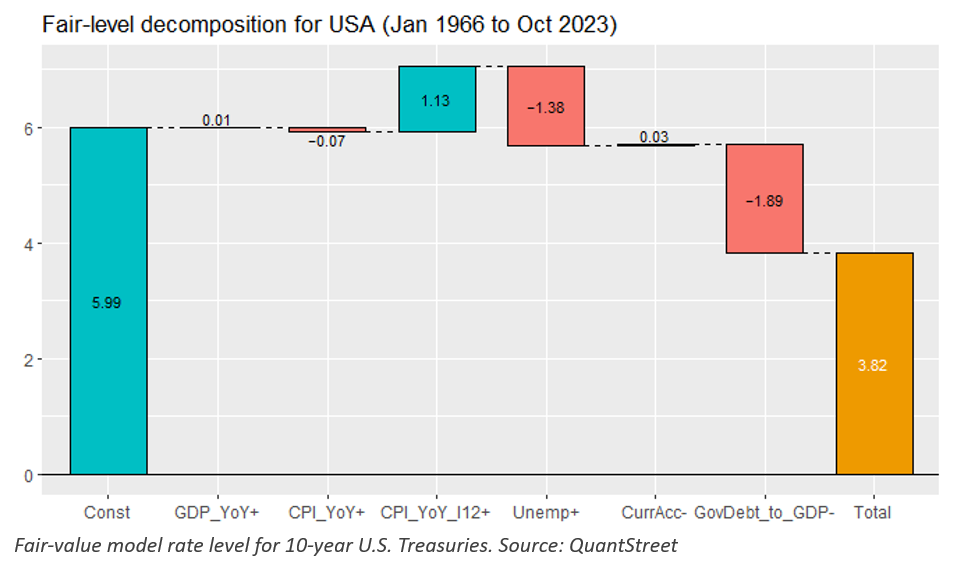

U.S. Treasury rates in the long-end of the curve are 100 basis points too high relative to a fair-value model. The risk-adjusted opportunity in long-dated, low-coupon Treasuries is attractive.

As 2023 enters the home stretch, I reflect on asset class performance for the year and discuss what my firm’s models are saying for the next 12 months.

There are compelling arguments that interest rates will remain low rather than rise.

Investors think about companies as being either large or small. In between those extremes are midcaps. Based on historical performance and fundamentals, midcaps should command more attention.

The Fed typically starts to ease ahead of economic weakness. But this isn't necessarily bad news for financial markets.

Investors have access to multiple personalized indexing products, a key benefit of which is to allow for tax-loss harvesting (TLH). I analyze when TLH works and how helpful it is to returns.

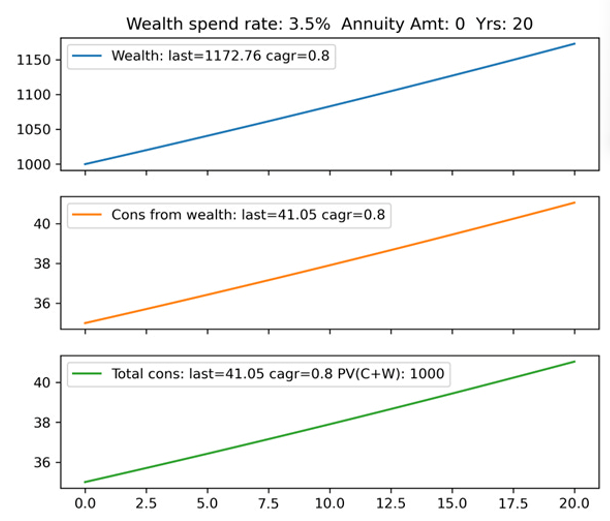

Advisors and investors wonder what role annuities should play in retirement planning. Here are the pros and cons of a common annuity product versus consuming out of invested wealth.

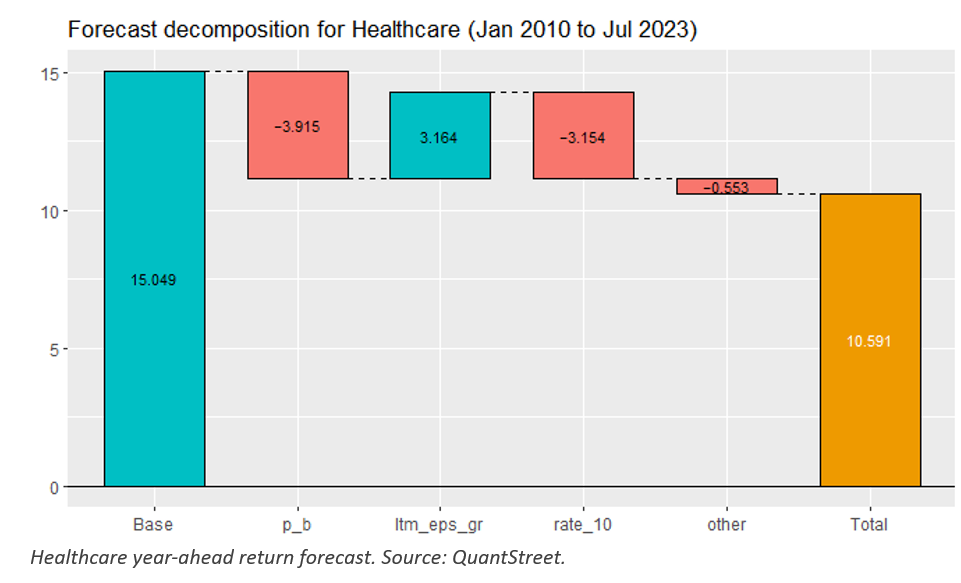

Healthcare stocks have been laggards on the back of cost pressures and punitive regulations. But the long-term trends are extremely favorable, making the sector a compelling opportunity.

Tech stocks have had a great year in 2023. Despite many prognostications to the contrary, a rational evaluation of the evidence does not suggest a price bubble in tech or the overall market.

Tech stocks are not in a bubble for two reasons. Not all stock price booms result in busts, and fundamentals and valuations do not suggest a tech bust is imminent.

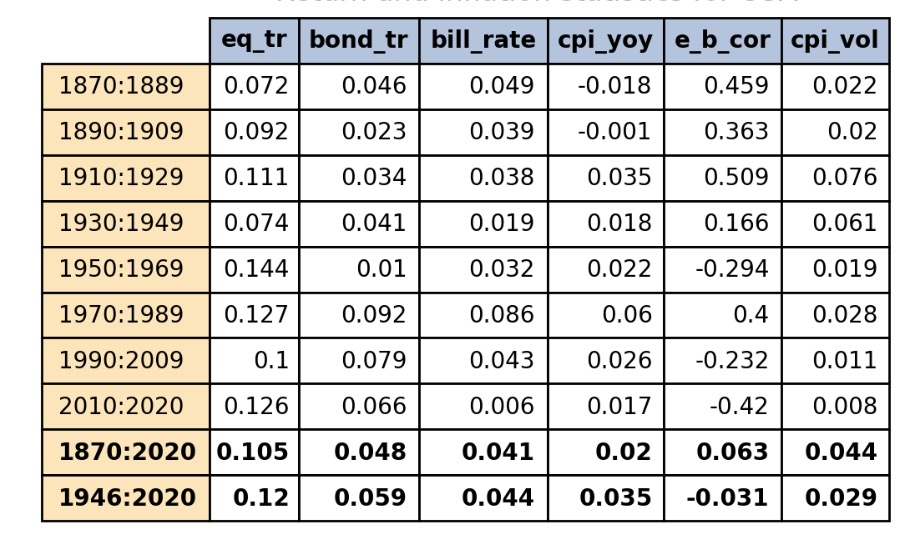

To properly guide their clients, financial advisors must have a good understanding of the long-run behavior of stock and bonds returns.

With Tuesday's (Nov 15th) Producer Price Index (PPI) numbers bringing more relief on the inflation side, a new bearish narrative has been put forward by financial pundits over the last few days.

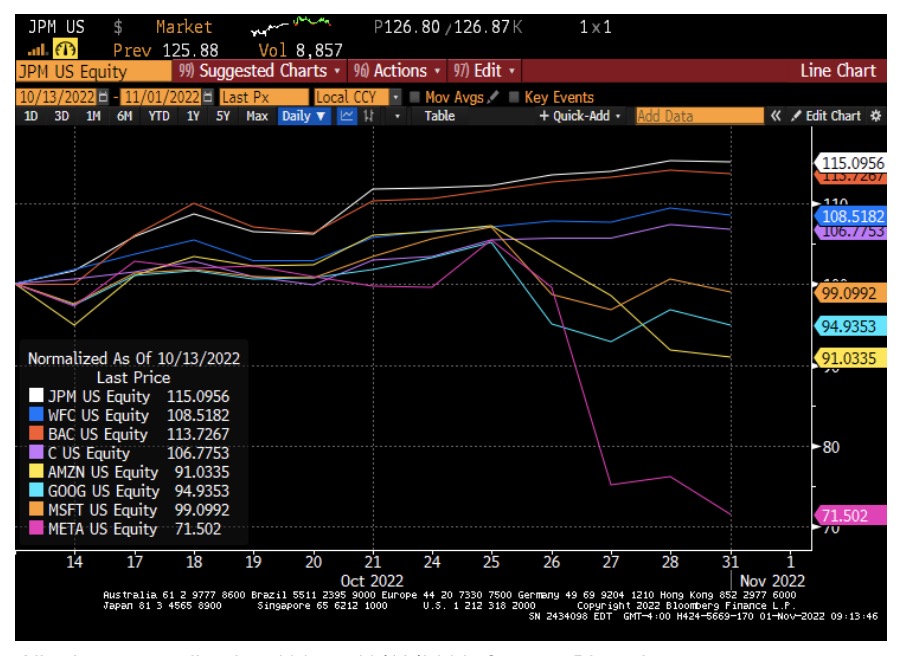

Market negativity reached a crescendo sometime around the middle of October, as interwoven narratives of doom and gloom occupied investor and media attention

If finance could be distilled into one idea, it likely would be that there should be a tradeoff between risk and reward: an investment with low risk should have a low expected return, while one that could make you rich should also be one that could lose you a lot of money. The Overnight Effect flies in the face of this core tenet.

For a long time, it worked. Wealthy investors did, in fact, enhance their yield through the firm’s YES strategy – and they were hooked. But then the market crashed, and the honeymoon was over.