Industry Momentum

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Many asset allocation strategies operate at the level of industry groups. Industry momentum -- buying past winners and selling past losers -- is present in U.S. data going back to the early 2000s.

In one of the most influential papers in empirical finance, Jegadeesh and Titman (1993) showed that past winning stocks outperform past losing stocks. Here, I analyze momentum at the industry level, by studying the performance of the 11 SPDR Sector Funds, as well as the Russell 2000 and S&P Midcap 400 indexes, going back to the early 2000s.

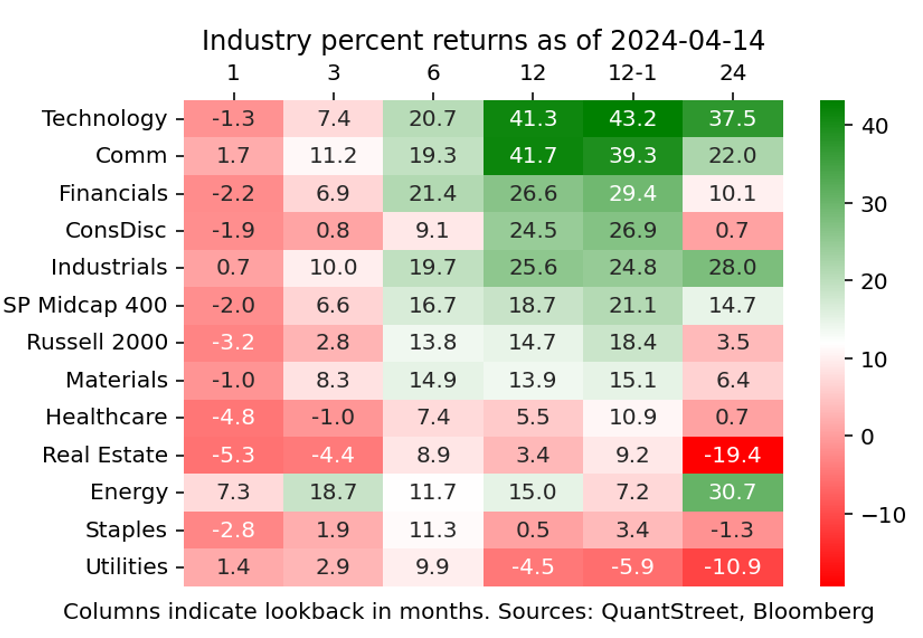

I analyze the returns of these 13 indexes over one-, three-, six-, 12-, and 24-month formation periods. For each horizon, I divide the industries into three groups: the top quintile winners (highest returns over the formation period); the top quintile losers (lowest returns); and the neutral sectors that do not fall into either category. Except for the one-month evaluation horizon, winner sectors outperformed loser sectors in all cases.

The current state of play is shown in the above table, which is sorted by the 12-1 return column (this is the return of each sector over the past 12 months, excluding the most recent month — more on this below). The other columns show industry returns over different horizons, all measured in months. For example, the “1” column shows last month’s returns for all industries, and the “24” column shows the returns of all industries over the prior two years. If one were trading three-month momentum, the current top industry pick is Energy (biggest three-month winner) and the bottom pick is Real Estate (biggest three-month loser). If one were choosing based on the last 12-month returns (the “12” column), then the top choice is Communications and the bottom choice is Utilities.

Momentum strategies

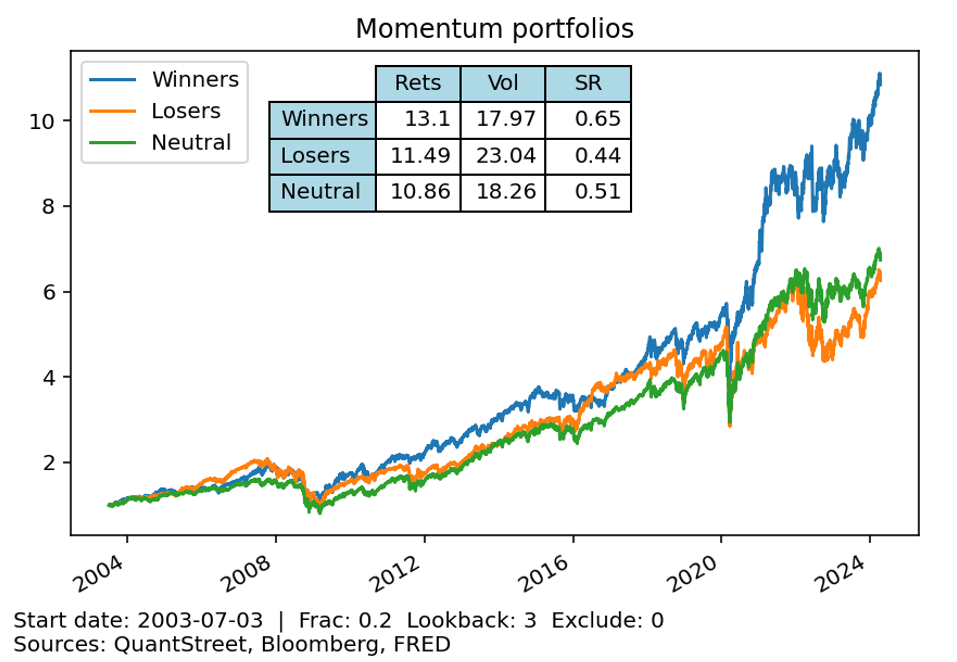

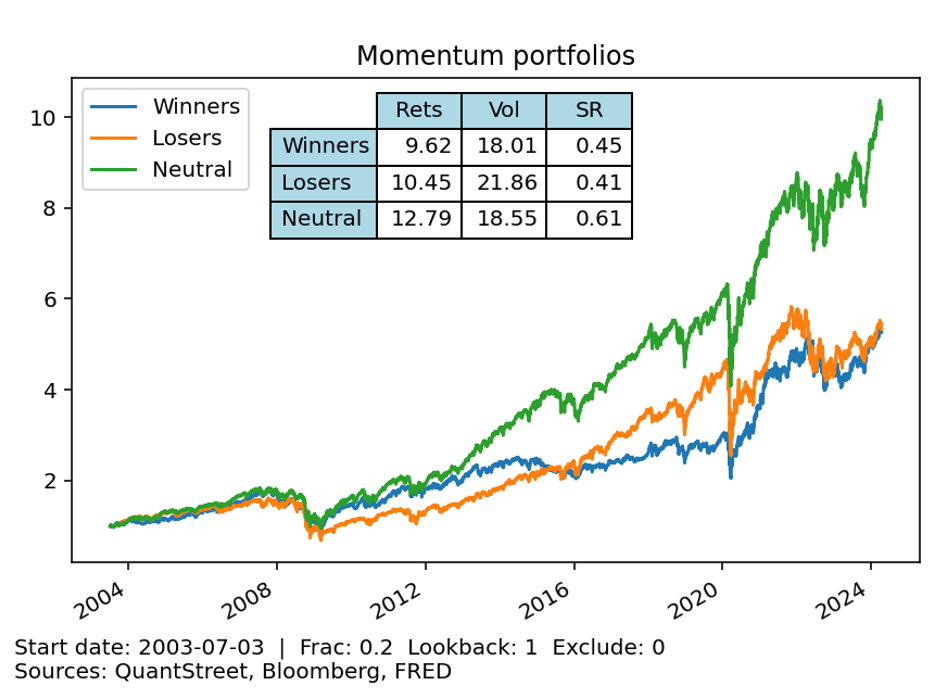

The next chart shows the performance of an industry momentum strategy that selects the top quintile (one-fifth) of industries with the best past three-month returns as the winners and the bottom quintiles of industries based on past three-month returns as the losers. The other industries, the nonwinners and nonlosers, are labeled as neutral.

Each set of stocks is held for the subsequent month, and then the winner, loser, and neutral portfolios are reconstituted. For example, the portfolio held in April of a given year is based on the returns of the industries in January, February, and March. The portfolio held in May depends on the February, March, and April returns, and so on.

The top, blue chart shows that past three-month winners have tended to strongly outperform past three-month losers, as well as the neutral portfolio. Since the start of the analysis in 2003, three-month winners averaged annual returns of 13.1% with a volatility of 18%. The Sharpe ratio for three-month winners was 0.65 (the average return above the risk-free rate divided by return volatility). The analogous Sharpe ratios for losers and neutral sectors were 0.44 and 0.51 respectively. Both sets of portfolios achieved lower returns than winners, with higher volatility.

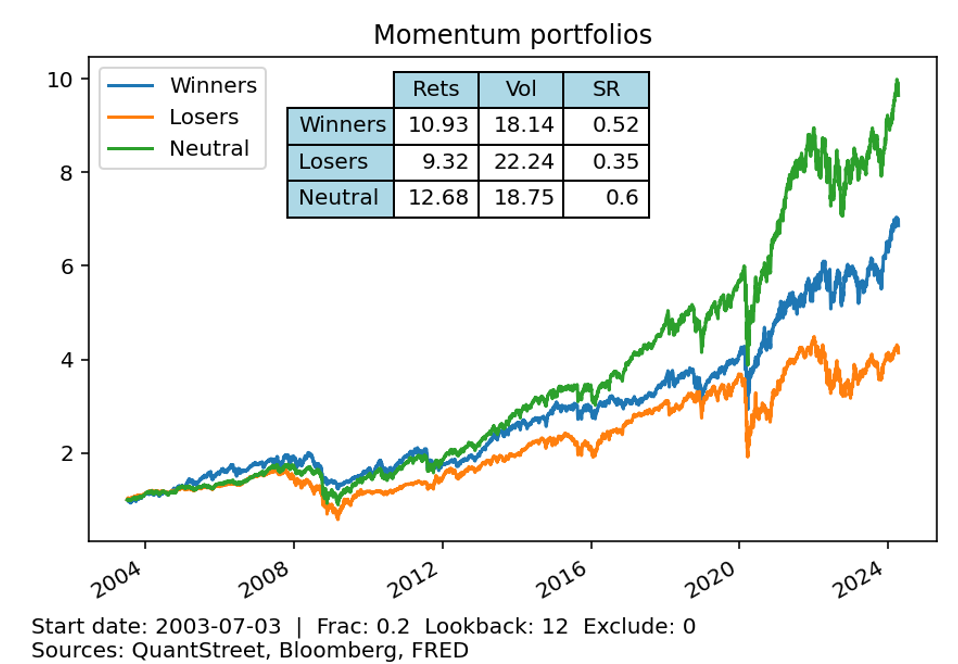

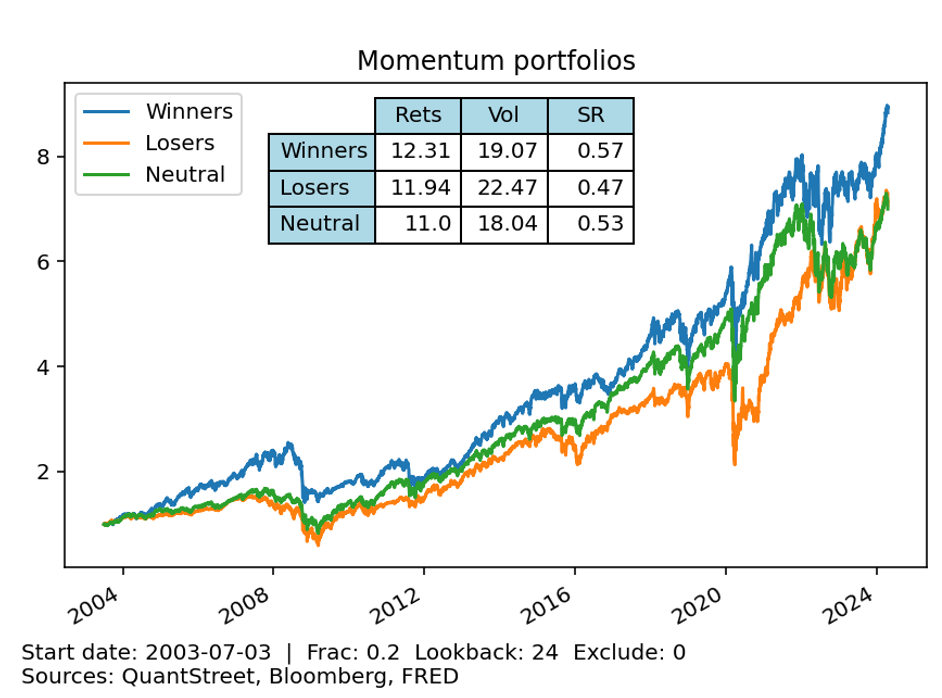

The above chart shows that 12-month winners (the sectors are held for one month based on their last 12-month returns) do better than 12-month losers, but the neutral portfolio does better than both. Past 12-month winners have a Sharpe ratio of 0.52, handily outperforming past losers’ Sharpe ratio of 0.35. However, the neutral portfolio — those industries outside of the top quintiles of winners and losers — does even better, with a Sharpe ratio of 0.60. Many mechanisms that explain the momentum effects have a hard time explaining why the neutral portfolio would outperform winners. We discuss this further below.

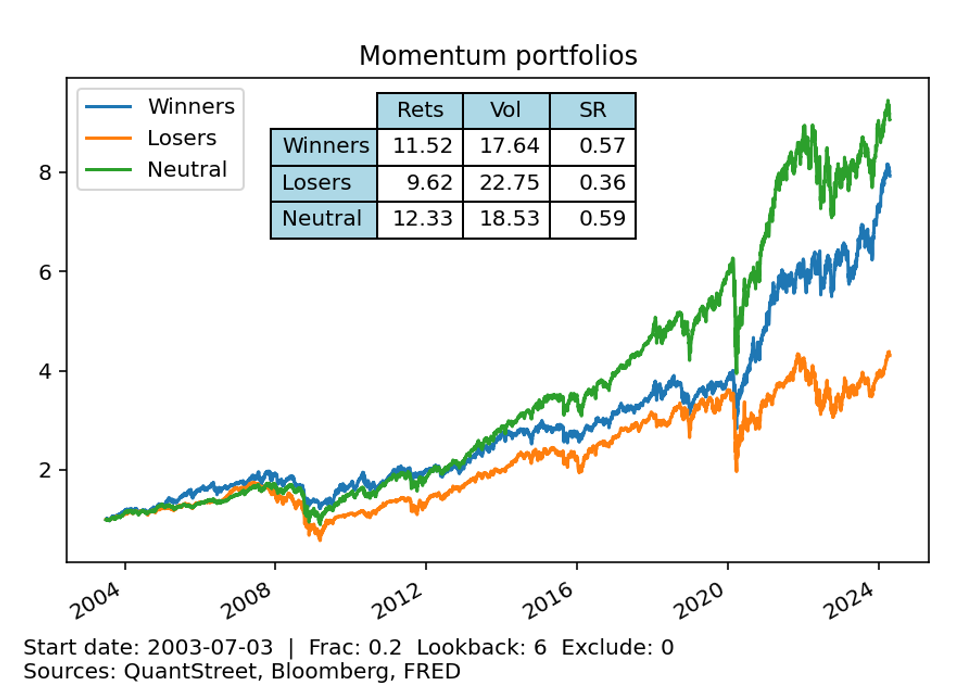

Finally, as can be seen in the Appendix, the momentum effect holds over a 24-month lookback period (where winners and losers are selected based on their last 24-month returns and then held for one month ahead), with winners outperforming losers and the neutral portfolio. Over a six-month lookback, winners again beat losers but slightly lag the neutral portfolio. However, the momentum effect does not hold over a one-month lookback window, with winners underperforming losers on an absolute basis, though winners still have a slightly higher Sharpe ratio.

12 minus 1 momentum

A common implementation of momentum skips the most recent month and calculates the industry returns over prior months two through 12 (see Asness et al. 2013 p. 936). The reason for this is that stocks often have a tendency for short-term mean reversion (see Lehmann 1990 and Jegadeesh 1990), and excluding industry returns in the month prior to the portfolio formation period reduces the impact of this short-term mean reversion on the momentum strategy.

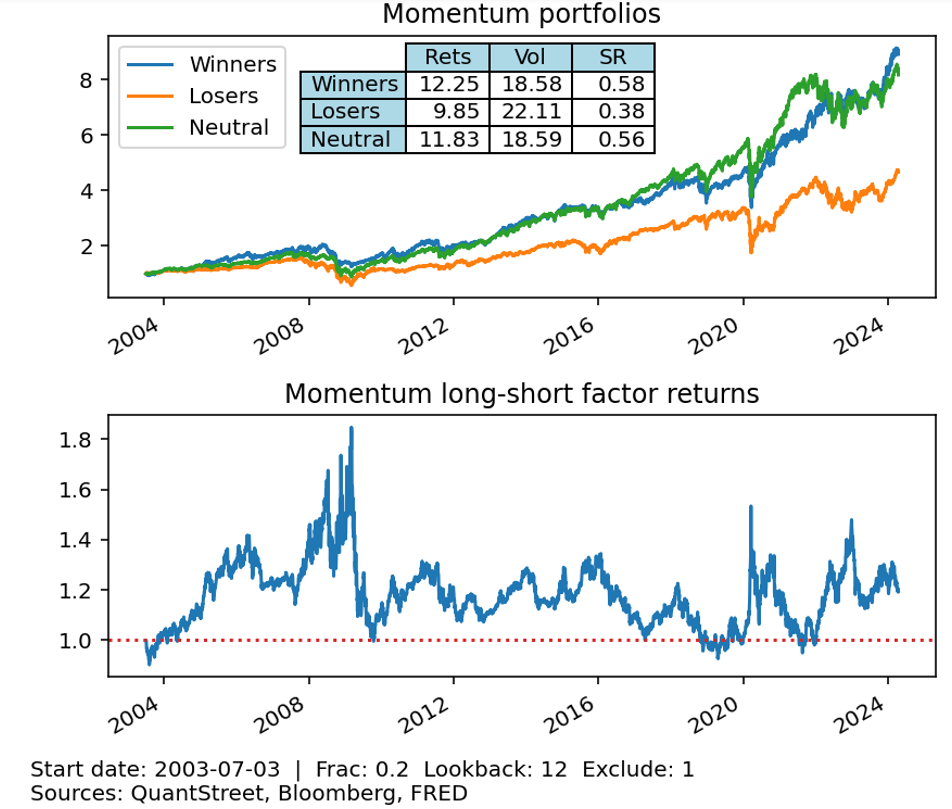

As the next chart shows, implementing the 12-1 version of last 12-month momentum (where winner and loser quintiles are determined based on their 12- through two-month back returns excluding the most recent month, and then held for one month forward) results in better results than simply choosing winners and losers based on the entirety of their last 12-month returns. The 12-1 winners have higher returns and higher Sharpe ratios than the 12-month winners, and now also outperform the 12-1 neutral portfolio (which holds the middle three quintiles of industries based on their 12-1 returns).

Momentum crashes

The bottom panel of the above figure shows the returns of a long/short momentum strategy using the 12-1 momentum signal. For every $100 of investor capital, the long/short momentum portfolio goes long $100 of the past winners and short $100 of the past losers. The neutral portfolio is not present.

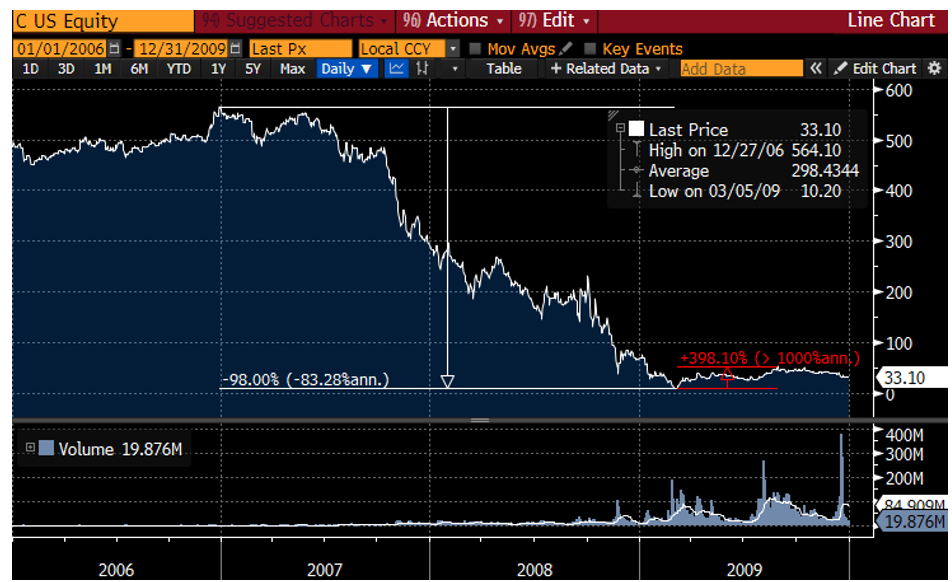

The long-short 12-1 momentum did very well from the start of the sample until the period right after the market trough of the global financial crisis (GFC). At this point, the momentum factor crashed from a cumulative return of above 1.80 down to a cumulative return of 1, a drop of roughly 45%. This momentum crash happened because past losers — like financials and real estate, which were shorted in the portfolio — had a massive rally from their GFC troughs.

An extreme example of this effect was Citigroup’s stock performance during the GFC. The stock fell 98% from its pre-GFC high to its early-2009 low. From that point, the stock has a close to 400% return over the next several months. It doesn’t look like much on the graph (since this sequence of returns still results in a roughly 90% drop from its pre-GFC high), but being short a stock that rallies close to 400% is very painful in a long/short portfolio.

This is the point made by Daniel and Moskowitz (2016), who discuss ways that such bounces of past losers can be detected and managed in a long/short momentum portfolio. From an asset allocation perspective — where short selling is not allowed — the performance of past winners is the key matter to consider. and 12-1 winners have handily outperformed 12-1 losers in our data sample.

Why is there industry momentum?

A lot has been written about the underlying economic mechanisms that might lead to momentum effects in markets. Jegadeesh and Titman 2011 provide a nice summary of the literature. Broadly speaking, there are three classes of explanations.

The first is that past winning stocks are, for some reason, riskier than past losing stocks, and the outperformance of past winners reflects a market risk premium for this unspecified additional riskiness exposure. However, in all cases we analyzed, the past winner portfolios have lower future return volatility than the past loser portfolios, suggesting that a pure risk-based explanation is unlikely to be the ultimate source of the momentum effect.

The second reason is underreaction to either firm-specific or industrywide news. Underreaction might happen because investors are unable to respond to all relevant news instantaneously, either due to information processing constraints or institutional frictions (such as not being able to quickly change a portfolio’s industry allocations because of concentration or other limits).

There is theoretical and empirical evidence that markets are worse at incorporating information across many stocks than information that is specific to one stock (Glasserman and Mamaysky 2019 and 2022). These arguments suggest that momentum might be a more important effect at the industry level than at the individual stock level.

The third reason, related to the second, is that behavioral biases cause investors to be overly fixated on old information (conservatism bias), or to avoid selling losers because realizing losses is unpleasant (disposition effect), or to overextrapolate from new information (representative heuristic). The first two effects would lead to momentum effects that do not reverse over time, while the third effect would cause momentum profits to reverse in the future, as overextrapolation is eventually corrected. My finding that there is momentum even when measured using lagged two-year returns argues against the overextrapolation mechanism, though it is consistent with both the conservatism bias and the disposition effect.

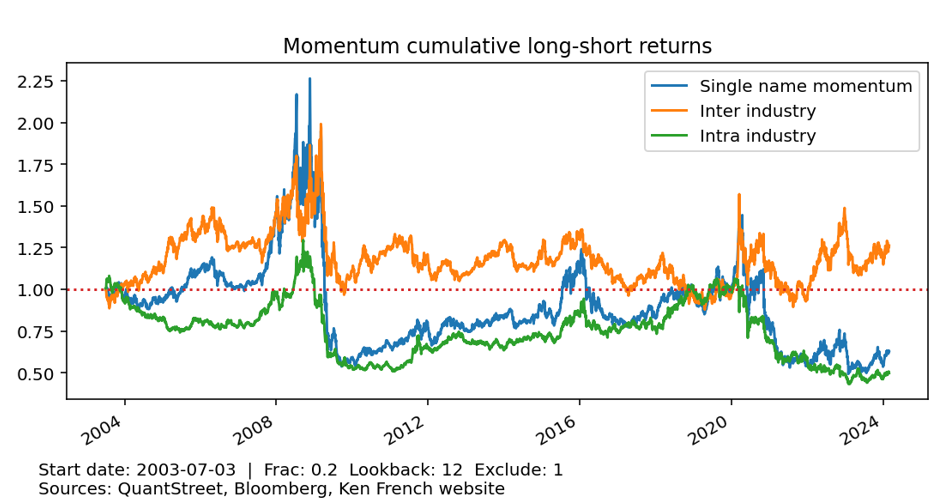

Returning to the idea that industry momentum may be more pronounced than pure single-stock momentum, I download momentum factor returns from Ken French’s website, which follows the 12 minus 1 convention I discussed previously. Unlike my industry momentum measure, the French momentum factor goes long the top quintile of past winners (based on their 12-1 returns) and goes short the bottom quintile of past losers. The cumulative return of this single-name momentum factor is shown as the blue line in the next chart.

Using regressions analysis, I then decompose single-name momentum returns into the part that comes from across industry momentum (my 12-1 industry momentum factor, the orange line) and the part that comes from within industry momentum (i.e., going long and short the winners and losers in a particular industry, the green line). Prior to the GFC, there is evidence of both industry and within industry (i.e., pure single-stock momentum), but after the momentum crash that took place post-GFC, there is very little evidence of pure single-stock momentum.

My finding that within-industry momentum drives the overall momentum is effect is consistent with Moskowitz and Grinblatt (1999), though the present analysis covers a time-period that is strictly after the publication of their paper, suggesting that their initial finding is robust.

What remains puzzling is why, in some cases, the neutral portfolio outperforms winners (for example, this happens with the 12-month momentum rule). Perhaps this can be explained by an underreaction to fundamental information that is followed by an eventual overreaction, which ultimately corrects. Past winners may be particularly prone to overreaction (since they are the industries that are up the most) and may thus be more susceptible to partial reversals relative to the neutral portfolio. A better understanding of this phenomenon is an interesting question for future research.

Conclusion

Industry momentum has been an important effect in U.S. markets since the early 2000s, and has been documented in U.S. data going back to 1963 (Moskowitz and Grinblatt 1999). Industry momentum appears present across multiple portfolio formation horizons, and is not explained by the riskiness of past winners (whose future returns tend to be less volatile than those of past losers). While the underlying explanation for momentum performance is unclear, the robustness of this effect should motivate investors to pay close attention.

Appendix

The Appendix shows the performance of the 24-month, six-month, and the one-month lookback portfolios.

Harry Mamaysky is a professor at Columbia Business School and a partner at QuantStreet Capital.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All