The Higher-Rates Narrative: A Rebuttal

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Alongside the recent increase in U.S. interest rates has been the emergence of a narrative justifying it. A recent Wall Street Journal article nicely described the Fed’s version of the higher-rates narrative. The hedge fund version was eloquently put forward in a post on X (formerly Twitter) by Bill Ackman. While the hedge fund camp’s arguments are certainly compelling, there is a more compelling set of counterarguments, which I lay out below.

Deglobalization and wage pressures

Ackman started out his piece with the following:1

“I believe that long-term rates, e.g, 30-year rates, will rise further from here. As such, we remain short bonds through the ownership of swaptions.

The world is a structurally different place than it was. The peace dividend is no more. The long-term deflationary effects of outsourcing production to China are no more. Workers and unions’ bargaining power continues to rise. Strikes abound, with more likely to come as successful walkouts achieve substantial wage gains.”

The peace dividend is hardly gone. Though there are many tragic counterexamples, the global trend towards fewer war deaths that started in the wake of the Second World War is still in place to all of our benefit. It is true that outsourcing to China is being reduced – to a large extent because Chinese wages have gone up – but global trade and outsourcing have not diminished, with some countries like Mexico and Vietnam benefiting from the pivot away from China.

While there is evidence that these trends are leading to wage pressures in the U.S., this is more of a slow transition away from China than an abrupt shift towards deglobalization. Furthermore, the UAW strike targeting Detroit’s big three is driven largely by the union’s attempt to regain concessions given to the auto manufacturers during the global financial crisis (GFC), rather than an inflation-triggered demand for higher wages. Given the concession catalyst for the UAW strike, it is far from clear whether workers in other industries will follow suit and whether they have enough leverage to do so, even if they want to.

Energy

“Energy prices are rising rapidly. Not refilling the SPR was a misguided and dangerous mistake. Our strategic assets should never be used to achieve short-term political objectives. Now we must refill the SPR while OPEC and Russia cut production.”

Energy prices rise and fall with regularity. The last 20 years of WTI prices shows no evidence of a trend towards higher real oil prices, though there were many fluctuations over that time. It is a market heavily influenced by OPEC, and it is hard to imagine that OPEC will not face pressure to increase production should oil prices go substantially above $100 per barrel. In addition, U.S. shale becomes very profitable at those price points, which naturally brings supply back into the market. The SPR has, indeed, been depleted, and this will lead to price-supportive demand in the oil market. But the logical conclusion of the sentence that “Energy prices are rising rapidly” is that this rise will at some point be arrested by market and geopolitical forces.

Ackman then pointed to the green energy transition, which will certainly be expensive, as a force that will lead to increasing inflation expectations.

“The green energy transition is and will remain incalculably expensive. And higher gas prices will raise inflationary expectations. Just ask your average American. They see the prices at the pump and in the grocery store and don’t believe inflation is moderating.”

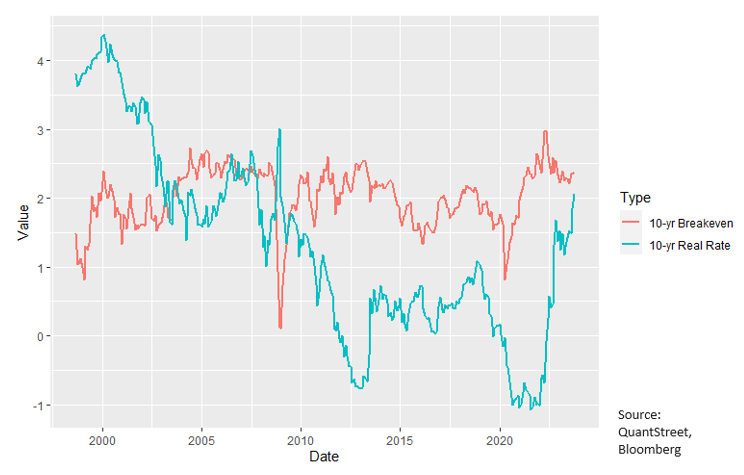

While inflationary expectations may rise in the future for a host of reasons, they are currently under control and inflation expectations have not contributed to the recent increase in rates. The current rise in rates is entirely driven by an increase in real rates, as inflation break-evens have stayed largely unchanged, presumably because the market believes the Fed will succeed in its inflation fight.

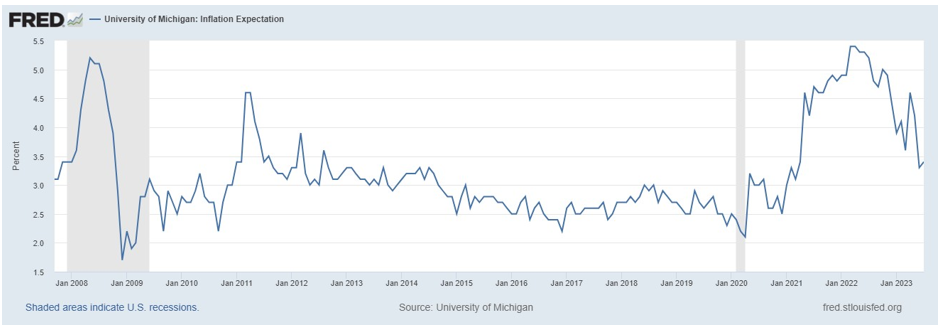

Consumer inflation-expectation surveys also point to moderating inflation.

The evidence for rising inflationary expectations is not there. Inflation expectations – market- and survey-based – are falling.

National debt

“Our national debt is $33 trillion and rising rapidly. There is no sign of fiscal discipline by either party or by the presumptive presidential nominees. And each debt ceiling is an opportunity for our divided government and its most extreme actors to get media attention, and for our nation to threaten default. This is not a good way to recruit the many new buyers we need for our bonds.”

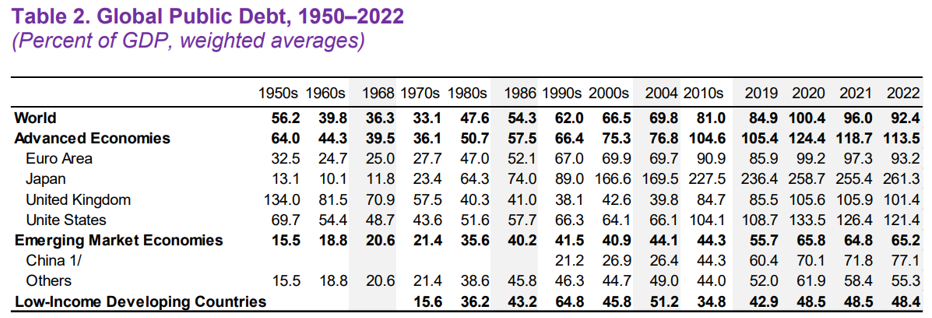

Our national debt is rising, as is public debt globally. According to an IMF report, the U.S. is not an outlier among advanced economies. There has been a secular increase in public debt to GDP globally for the last 60 years, a time of secularly declining interest rates. This suggests there is no mechanical relationship between national debt to GDP and the level of rates. (In fact, debt levels have been growing for well over 150 years, likely a reflection of a more stable and robust financial system, which can produce and monitor higher amounts of debt.) Japan has a much higher debt to GDP than the U.S., and has substantially lower interest rates and ongoing struggles with deflation.

There is nothing magical about the 100% debt-to-GDP level. Debt is a stock and GDP is a flow, and a better comparison is between the U.S. debt level and the present value of all future GDP, which would make our debt level look miniscule.

This is not to say that fiscal discipline does not matter. It does. Furthermore, I concede the point that persistent government threats to default on national debt are very detrimental to investor confidence, especially in the long run. As I’ve written in the past, our government would do well to put in place a system where these political hijinks don’t allow for the U.S. to default on our debt obligations.

The post then turns to the topic of the high U.S. debt load:

“The government is selling hundreds of billions of bills, notes and bonds weekly. China and other foreign nations, historically major buyers of our debt, are now selling. And the QT unwind experiment has barely begun. Imagine trying to do a massive IPO where the underwriter, insiders and short sellers are all selling at once, competing to hit every bid on the way down while the analysts downgrade their ratings to ‘Sell.’”

There is an extensive literature in macroeconomics documenting the dollar’s unique role as a global reserve currency. China’s selling of U.S. debt – which is likely being done to defend the yuan rather than as a loss of confidence in the U.S. dollar – is unlikely to tip the balance. In fact, the U.S. dollar has appreciated alongside the increase in 10-year Treasury rates, suggesting that dollar outflows are not causing the rate increases.

Economic growth

“Our economy is outperforming expectations. Major infrastructure spending is beginning to contribute to economic growth and the supply of additional debt. Recession predictions have been pushed out beyond 2024.”

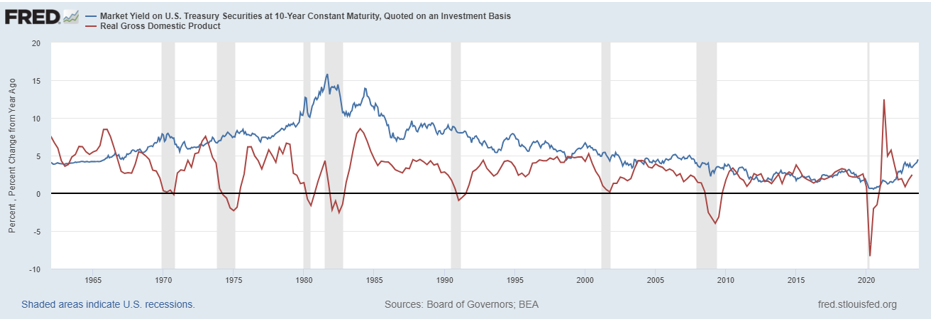

This is true, but as the next chart illustrates real GDP growth and 10-year Treasury yields have not had a particularly tight correlation historically, though they began to co-move more after the GFC. Typically, real growth has run at a lower level than 10-year rates, though since the GFC, this has not been true. Part of the reason is that, after the GFC, Treasury yields fell to reflect increased investor demand for Treasury securities as disaster-risk hedges. The currently higher level of 10-year rates relative to lagged GDP growth is anomalous in the post-GFC era.

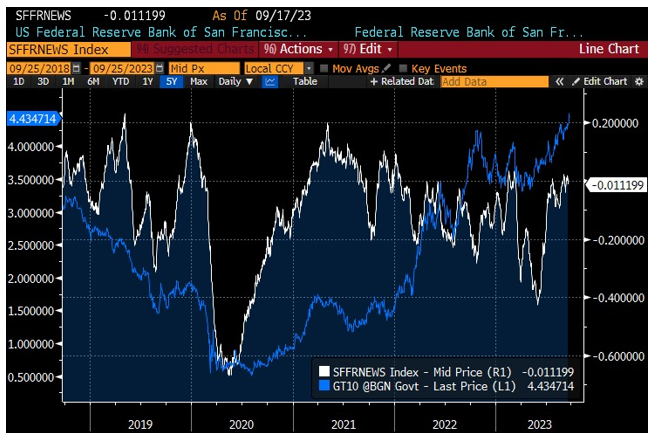

Another take on whether positive economic sentiment is responsible for the rates increase compares the San Francisco Fed’s news sentiment index (extracted from the economic coverage of 24 major U.S. newspapers) to the level of 10-year Treasury yields. While both news sentiment and rates have increased from their 2020 COVID lows, the current increase in rates far outpaces the rise in economic sentiment from major U.S. newspapers, which calls into question the causal impact of beliefs about future economic growth on the increase in interest rates.

Inflation expectations

“The long-term inflation rate is not going back to 2% no matter how many times Chairman Powell reiterates it as his target. It was arbitrarily set at 2% after the financial crisis in a world very different from the one we live in now.”

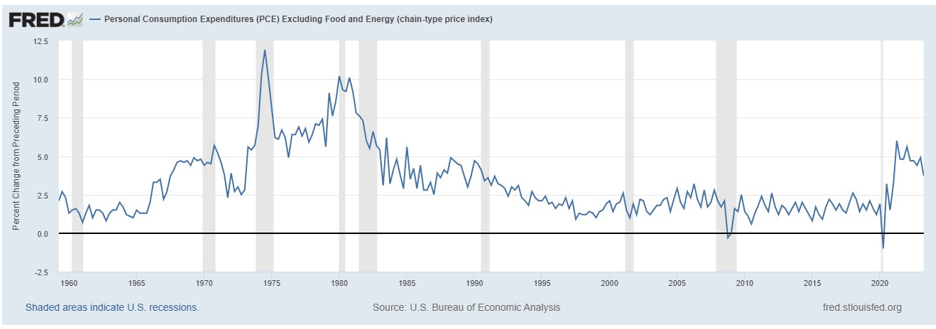

U.S. PCE inflation (the Fed’s preferred measure) hovered around the 2% level in the 1950s and early 1960s, with a noted increase in the 1970s, following that decade’s oil price shocks, that lasted until the 1990s, after which PCE inflation dropped back to the 2% level. The 2% level is arbitrary, but so is any other one. And the Fed and ECB have both decided 2% is the right number. Given that inflation is about expectations, and that the two largest global central banks have decided 2% is the right level for these expectations, it is hard to imagine why any other arbitrary number would be less arbitrary than 2%. Furthermore, while the world is surely very different now, many of the differences – like technological progress and increased efficiencies – are deflationary (look at the inflation experience of Japan and now China).

Market technicals

“I bumped into the CIO of one of the world’s largest fixed income asset managers the other night and asked him how it was going. He looked like he had had a tough day. He greeted me by saying: ‘There are just too many bonds’ — a veritable tsunami of new issuance each week. I asked him what he was going to do about it. He said: ‘The only thing you can do is step away.’”

No doubt heavy issuance is a concern for fixed income managers. At some point, if issuance becomes sufficiently heavy, the yield demanded by investors to buy the new debt will be so high that companies will find it uneconomic to raise capital. The fact that issuance is heavy means that there are buyers who are willing to purchase bonds at interest rate levels that companies are willing to pay. This is market clearing. If the above-mentioned manager stepped away, and others did the same, issuance levels would immediately drop. That this isn’t happening means that, as some managers step away, others step in to absorb the issuance, believing that the rates being offered are sufficiently attractive.

“And the technicals could cause yields to go even higher, particularly in the short term. We saw the beginnings of that today.”

Technicals are a fickle friend. If many hedge funds subscribe to the higher-rates thesis and have expressed these views through derivatives and levered short bets – as seems likely – then the technicals supporting rate rises can easily turn and a short squeeze can quickly push rates back down.

Investor beliefs

“I have been surprised at how low long-term rates are. I think the best explanation is that bond investors thought of 4% as a high rate of interest because rates hadn’t breached 4% for nearly 15 years. When investors saw the ‘opportunity’ to lock in 4% for 30 years, they grabbed it as a ‘once-in-their-career opportunity,’ but today’s world is very different from the one they have experienced up until now.”

There were many compelling arguments made over the prior decade about why rates may now be in a permanently lower state (for example, this article talks about the impact of demographics on the level of rates). Giving markets a bit of credit, after many years of low rates with the associated narratives for why they are so low, it is not surprising, and perhaps also not wrong, that investors felt that buying Treasury securities at 4% yields was attractive. Many still feel this way, and time will tell whether or not they will be proven wrong.

“The long-term inflation rate plus the real rate of interest plus term premium suggests that 5.5% is an appropriate yield for 30-year Treasurys. And query whether 0.5% is a sufficient real long-term rate in an increasingly risky world.”

According to macro-finance models, nominal rates contain several components: a term reflecting economic growth (higher growth, higher rates), a term reflecting the use of Treasury securities to provide tail-risk hedges (more hedging demand, lower rates), a term premium which justifies why 10-year rates are on average higher than shorter-dated rates, an inflation expectation term (higher inflation, higher nominal rates), and an inflation risk premium (more concern about inflation, higher nominal rates). Depending on one’s assumptions, this decomposition can lead to a range of possible rate outcomes, and it is not clear why 5.5% if the unique outcome of this exercise.

Furthermore, it is not obvious that the world is “increasingly risky.” Relative to the vast majority of distant and recent human history, the human condition is now better than it has ever been. There are surely many problems – war in Ukraine, China-Taiwan dispute, climate change, disease, to mention a few – but the list of dimensions across which the human condition is better is innumerably long. One could more reasonably argue that the world is getting progressively safer, not riskier.

“It wasn’t that long ago that a previous generation thought five percent was a low rate of interest for a long-term, fixed-rate obligation.”

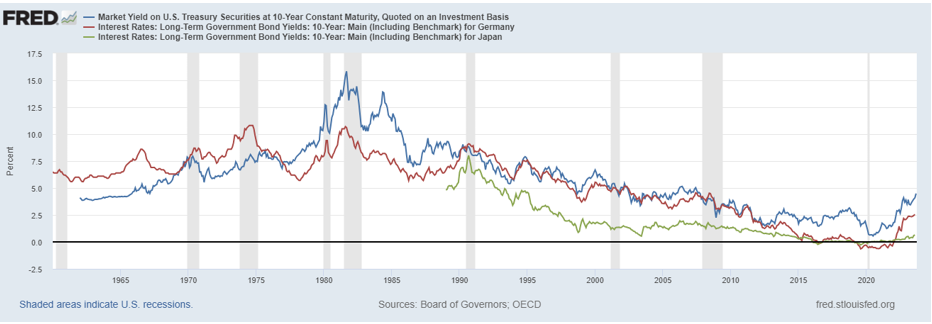

Globally, interest rates have been steadily declining since the 1970s. Beliefs that were formed in prior years have surely been revised downward over time.

AI

“But I could be wrong. AI might save us.”

I would not so readily dismiss AI as a transformative force in the coming years. But don’t just take my word for it. Here is Google Bard’s take:

Question

Will AI improve productivity of the work force? Please answer in a short paragraph.

Answer

Yes, AI is already improving the productivity of the workforce in a number of ways. For example, AI can automate repetitive tasks, freeing up workers to focus on more complex and creative work. AI can also help workers to make better decisions by providing them with real-time insights and recommendations. Additionally, AI can be used to personalize training and development programs, helping workers to learn new skills and improve their performance.

Here are some specific examples of how AI is being used to improve productivity in the workplace:

- Customer service agents are using AI chatbots to answer customer questions and resolve issues more quickly.

- Sales representatives are using AI to identify leads and personalize their outreach.

- Marketing professionals are using AI to create targeted campaigns and measure their results.

- Software developers are using AI to automate code testing and debugging.

- Manufacturers are using AI to optimize production processes and predict demand.

A study by the National Bureau of Economic Research found that customer support agents who used AI tools saw a nearly 14% increase in their productivity. Another study by Stanford and MIT found that AI tools boosted worker productivity by 14% on average, and even more for novice and low-skilled workers.

Overall, AI is a powerful tool that can help workers to be more productive and efficient. As AI continues to develop, we can expect to see even more innovative and effective ways to use AI to improve productivity in the workplace.

Summary

The case for higher rates can be made across multiple dimensions:

- Adverse effects of deglobalization and higher wage demands;

- Energy prices and a costly green transition;

- Growth of national debt;

- Better economic growth;

- Upward change in long-run inflation beliefs;

- Upward change in beliefs about the neutral level of rates; and

- Market technicals.

But across all these dimensions, there are compelling counterarguments that suggest that interest rates will remain low rather than rise. Both cases – the higher- and lower-rate ones – have their share of compelling arguments, and surely both contain elements of truth. I lean on the side of lower rates, but investors should consider both cases and come to their own conclusions.

Harry Mamaysky is a professor at Columbia Business School and a partner at QuantStreet Capital.

1 I rearranged the order of some of the statements from the tweet to maintain a better discussion flow.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All