Is There Still a Value Effect?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Value investing is the lens through which many view financial markets. Yet, a simple value factor has performed poorly for the last 16 years. Is the value effect over, or will it come back in 2024?

From Graham and Dodd’s hugely influential Security Analysis, to Warren Buffett’s storied career, to today’s value investing firms, like GMO, Oaktree, and GAMCO, the value investing ethos permeates financial markets. Indeed, the value effect is at the heart of much of investing practice and folklore.

Value investing typically means buying solid companies at low valuations, as measured by low price-to-earnings or price-to-book ratios, or by high dividend yields, amongst several other value measures. Proponents of value investing believe such stocks will outperform non-value (growth) stocks over time.

Academic theories suggest that this might happen because either (1) value stocks are, in some sense, riskier than growth stocks and thus compensate investors with additional returns for bearing this added risk; or (2) because value stocks have been temporarily mispriced in less than fully efficient markets (see Campbell, Giglio, and Polk 2023 for a recent discussion). If growth stocks have sufficiently high growth rates (of earnings or dividends), then it is possible that growth stocks, despite their higher valuation multiples, might also have higher expected returns than value stocks.

A lower multiple does not mechanically guarantee higher expected returns.

A common way to analyze the value effect – though one that ignores the “solid company” part of the above description – is to classify stocks as cheap or expensive based on some valuation metric, and then to track the performance of portfolios which go long the cheap stocks and short the expensive ones. Following the work of Fama and French (1992, 1993), a commonly used valuation metric is a company’s book-to-market ratio, which measures the accounting or book value of a firm’s equity relative to the firm’s market capitalization (i.e., the market value of its equity). The higher a firm’s book-to-market ratio, the more value-like is the company, and the lower a firm’s book-to-market ratio, the more expensive is the firm’s stock (presumably, at least in part, because the company will grow faster).

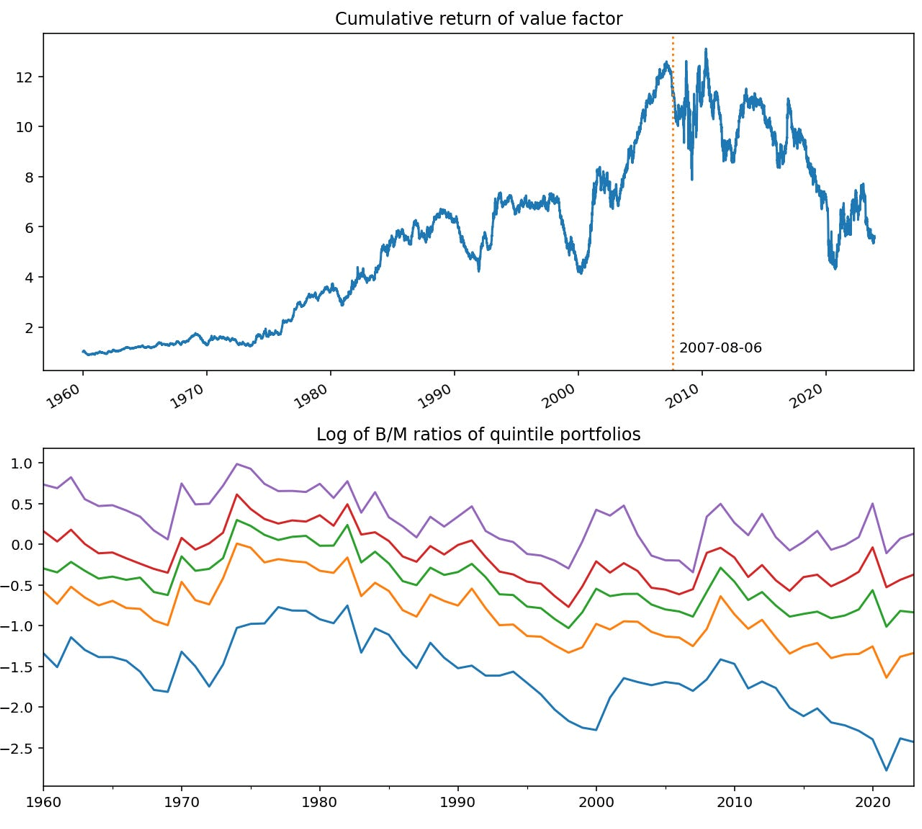

A hypothetical portfolio that is long value and short growth stocks is often referred to as the value factor. While the value factor ignores important implementation details, it nevertheless captures an aspect of the overall performance of real-world value investing strategies. The top panel of the next chart shows the performance of the value factor since 1960. And herein lies the rub: Value did well from the 1960s all the way to 2007, the period just before the global financial crisis (GFC). Since then (the vertical, dotted line in the figure show the start of the quant crisis of 2007), the value factor has performed very poorly, with growth stocks strongly outperforming value stocks over the last 16 years.

The top panel shows the performance of a value factor which goes long the top quintile of book-to-market stocks based on that metric at the start of each year and which concurrently goes short the lowest book-to-market stocks. The bottom panel shows the natural logarithm of the value-weighted average book-to-market of firms in each book-to-market quintile at the end of every year since 1960. Sources: Ken French website, QuantStreet.

The bottom panel of the above chart shows the natural logarithm of the value-weighted average book-to-market ratio in each book-to-market quintile since 1960. The valuation of growth stocks (the bottom blue line with the lowest book-to-market ratios) has, for decades, gotten more “extreme” relative to the valuation of value stocks (the top line with the highest book-to-market ratios). Despite this growing valuation gap, growth stocks have continued to outperform value stocks since 2007.

The million-dollar question for investors is whether the post-2007 experience represents a transient period of underperformance, or whether the GFC signaled the onset of a new regime, where value stocks will consistently underperform growth. I provide some insights into this question in the remainder of this article.

Inter-industry value

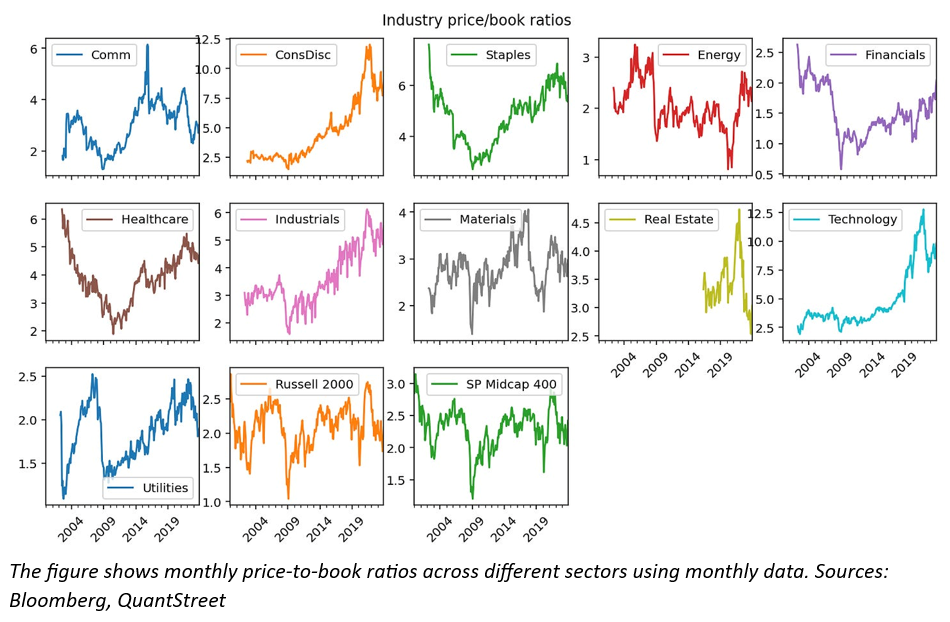

Campbell, Giglio, and Polk (CGP, 2023) make the point that the value effect can be decomposed into intra-industry value (i.e., go long “cheap” and short “expensive” companies in the same industry while maintaining an overall neutral exposure to each industry) and inter-industry value (i.e., go long “cheap” industries and go short “expensive” ones). To further explore this decomposition, the next chart shows the price-to-book (the reciprocal of book-to-market) ratios of different industries. In this analysis, I count the Russell 2000 and the S&P Midcap 400 as “industries,” though excluding them from the analysis would leave the results largely unchanged. There is large variation in price-to-book multiples across and within industries over time.

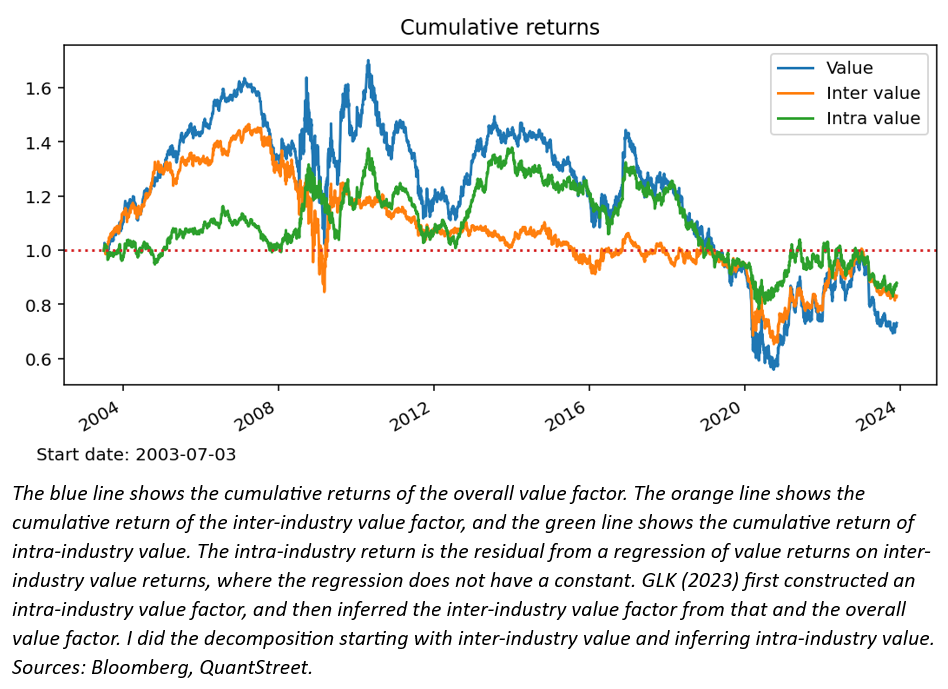

Following the decomposition of the value effect suggested by CGP, I construct an inter-industry value portfolio by going long the bottom quintile of industries with low price-to-book ratios (or, equivalently, high book-to-market ratios) and going short the top quintile of industries with high price-to-book ratios. Using regression analysis, I then decompose the overall value factor into a part that is due to inter-industry value and a part due to intra-industry value. The inter-industry factor captures the degree to which cheaply valued industries perform better than richly valued ones, and the intra-industry factor captures the degree to which cheaply valued firms within a given industry tend to outperform richly valued firms in that same industry.

The decomposition shows that both inter- and intra-industry value strategies did well heading into the value crash of 2007. At that point, inter-industry did very poorly, i.e., “expensive” industries outperformed “cheap” ones, even as intra-industry value did well, i.e., cheaply valued companies outperformed their expensive intra-industry peers. This intra-industry outperformance did not last however, and in fairly short-order, intra-industry value also did poorly even as inter-industry value bounced a bit post its GFC collapse. For the next decade or so, both inter- and intra-industry value bounced around a bit, while exhibiting a generally downward trend (very different from the decades-long outperformance prior to 2007). With the onset of COVID in 2020, value experienced another crash, both a intra- and an inter-industry one, though inter-industry value appears to have done worse.

Overall, since the industry return data starts in 2003, the cumulative returns for the three value series have been negative, suggesting that growth industries and growth stocks have been outperformers, the latter result running contrary to the roughly 50 years of data prior to 2007.

Is inter-industry or intra-industry value more important?

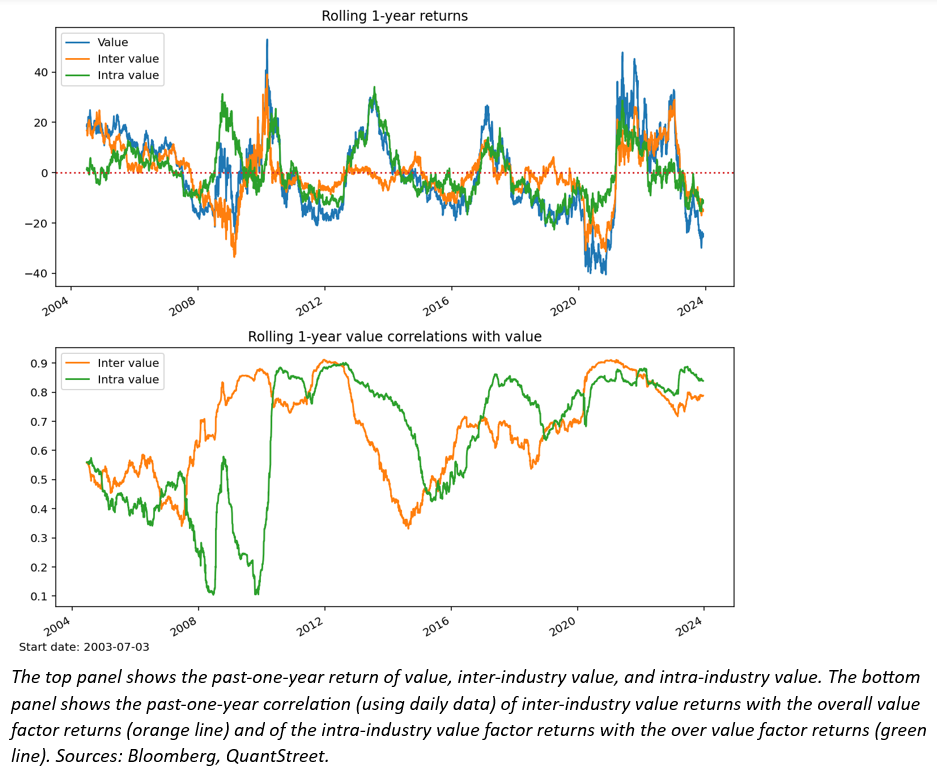

The top panel in the next figure shows the past one-year return of each of the three value series. This figure emphasizes time periods during which the value effect was driven by inter-industry value and those in which value was driven by intra-industry value. From the start of the sample to 2008, value was driven more by inter-industry effects than intra-industry value. From 2008 to 2012, inter-industry value was the key driver of the value effect. From 2012 to 2016, intra-industry value dominated, as inter-industry value remained largely flat over that time period. From 2016 to 2020, the close relationship of value and intra-industry value continued. And since 2020, all value series appear to track rather well.

The bottom panel of the above chart shows the last-year correlation of daily returns between inter-industry value and the value factor (orange line) and between intra-industry value and the value factor (green line). When the orange line is above the green line, the value effect is driven more by inter-industry value effects, and when the green line is above the orange line, the value effect is driven more by intra-industry value. Periods of greater inter- versus intra-industry value contribution are persistent, as indicated by the fact that one or the other correlation dominated for long periods of time. In the most recent few years, both intra- and inter-industry value have contributed to the overall value effect in roughly equal measure.

Why has value underperformed?

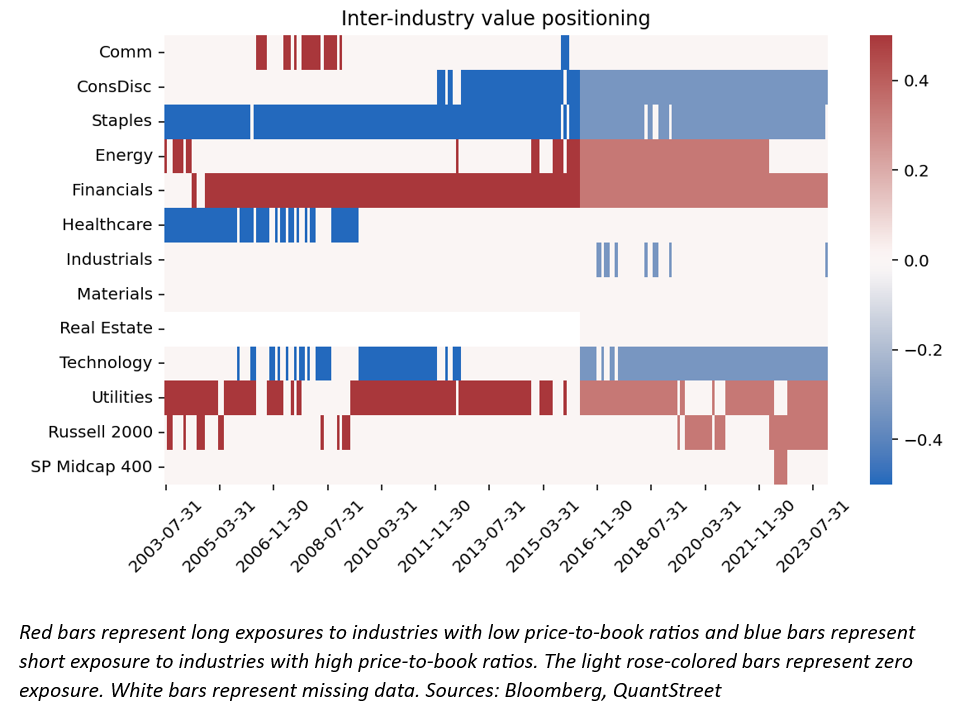

As the cumulative return chart above shows, value, inter-industry value, and intra-industry value factors have all underperformed over the last 20 years. To explore this phenomenon, the next figure shows the industry loadings of the intra-industry value factor. Red bars represent long exposures to industries with low price-to-book ratios and blue bars represent short exposure to industries with high price-to-book ratios. The light bars represent zero exposure.

The above figure illustrates that the mainstays of the long part of the inter-industry factor were energy, financial, and utility stocks, with occasional contributions from the communications sector, the Russell 2000, and S&P Midcap 400. Mainstays on the short side are consumer discretionary (an index with a heavy allocation to Amazon and Tesla), staples, healthcare (in the early part of the sample), occasionally industrials, and technology. An industry switching from the long side to the short side or vice versa was extremely rare. It only happened once with communications (likely because the index added Meta, Alphabet, and Netflix).

The general sector compositions of the long and short legs of the inter-industry factor don’t change much over time, though some industries enter and leave periodically. The long side (energy, financials, utilities, and occasionally small- and mid-caps) represents old economy, slow-growing businesses, whereas the short side (consumer discretionary, staples, healthcare, technology) represents new economy, faster-growing businesses.

For the inter-industry value factor to perform well going forward, one would either need to believe that investors have irrationally underappreciated the prospects of the energy, financials, utility, and non-large-cap sectors, or that these sectors are, by some measure, riskier than their growth counterparts. The former explanation is highly unlikely because the market is fully aware of how the value industries differ from the growth ones. It is hard to argue that the likes of Citigroup, Exxon Mobil, and Duke Energy trade “cheap” because of investor inattention to their prospects. The risk explanation is more plausible, as banks’ balance-sheet problems (e.g., SVB and First Republic), the energy sector’s ESG issues, and utilities’ (fortunately highly remote) Fukushima-type risk could lead investors to demand higher risk compensation for owning these sectors. On the other hand, growth sectors are not without issues, such as the risk of valuation bubbles, technological obsolescence, and higher duration cash flows which are more interest rate sensitive.

The risk exposure discussion is certainly an interesting one (see CGP 2023) and I will return to it in future work. But without the investor irrationality dynamic – which is highly implausible for inter-industry momentum – the risk story by itself does not point to value sectors always having better return prospects than growth ones, despite their valuation differentials.

Does valuation explain the value effect?

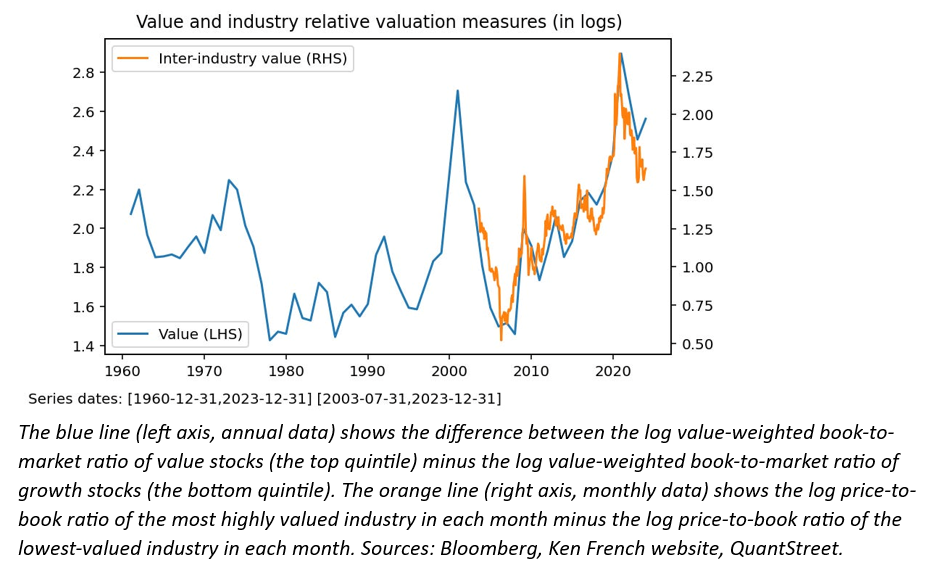

Value-oriented investors often point out that value stocks are particularly attractive when the valuation differential between them and growth stocks becomes especially large. The logic holds that if valuation measures indeed indicate “cheapness” and “richness,” then a large valuation gap between growth and value suggests the former are particularly rich and the latter are particularly cheap. The next chart shows two measures of valuation differential between growth and value. The blue line (left axis) shows the difference between the log value-weighted book-to-market ratio of value stocks (the top quintile) minus the log value-weighted book-to-market ratio of growth stocks (the bottom quintile), on an annual basis. The orange line (right axis) shows the log price-to-book ratio of the most highly valued industry in each month minus the log price-to-book ratio of the lowest-valued industry in each month.

The two series track each other reasonably closely, suggesting that valuation differentials between individual stocks within an industry generally follow valuation differentials across industries. The valuation differential between growth and value has been growing for the last 15 years. Arguably, the longer, annual value differential series (blue line) shows some evidence of an increasing trend over the last six decades.

Here the growth versus value debate devolves into a tribal conflict. The value tribe will argue that given the extremely large valuation differential, value is now highly attractive. The growth tribe will argue that growth has outperformed value for the last 16 years, even as the valuation differential has continued to widen, suggesting the valuation differential is not a forecaster of value-factor performance.

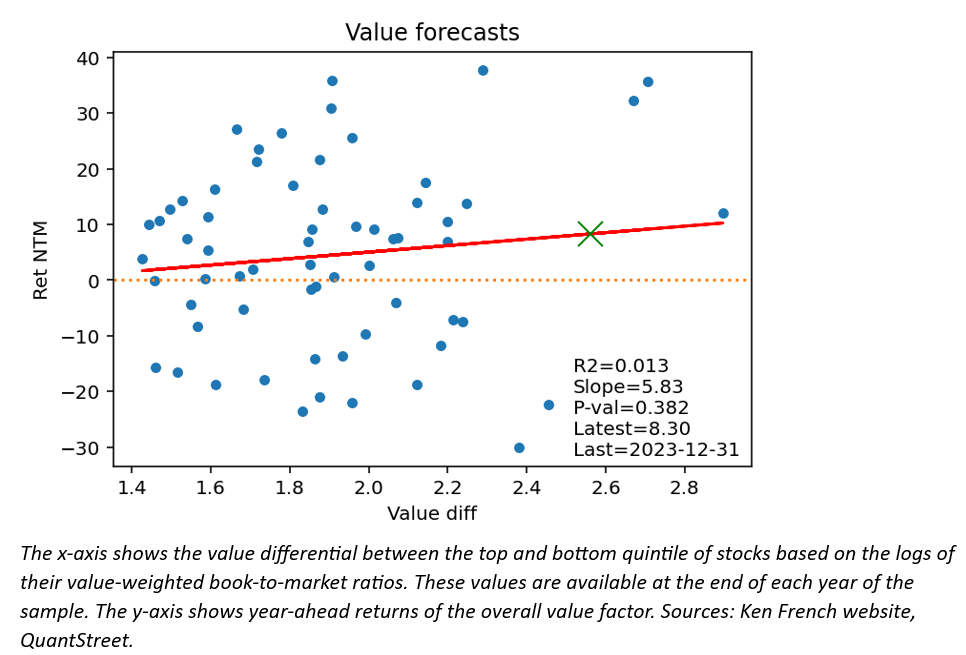

To examine the empirical evidence, the next chart shows a scatter plot of the annual valuation differential of the value factor plotted on the x-axis and the next 12-month return of the value factor plotted on the y-axis. The explanatory power of the valuation differential for one-year ahead value factor returns is very low, with an R-squared of only 1.3%. The slope coefficient of the regression line is, indeed, positive. But it is statistically insignificant, suggesting that a higher valuation difference between growth and value does point to higher value factor performance, but that this relationship is weak and might even be non-existent. The green X shows the most recent valuation differential and the one-year ahead return forecast for the value factor that it implies. This forecast currently stands at 8.3%, but should be taken with a large grain of salt given the noisiness of the relationship between valuation differentials and future value factor returns.

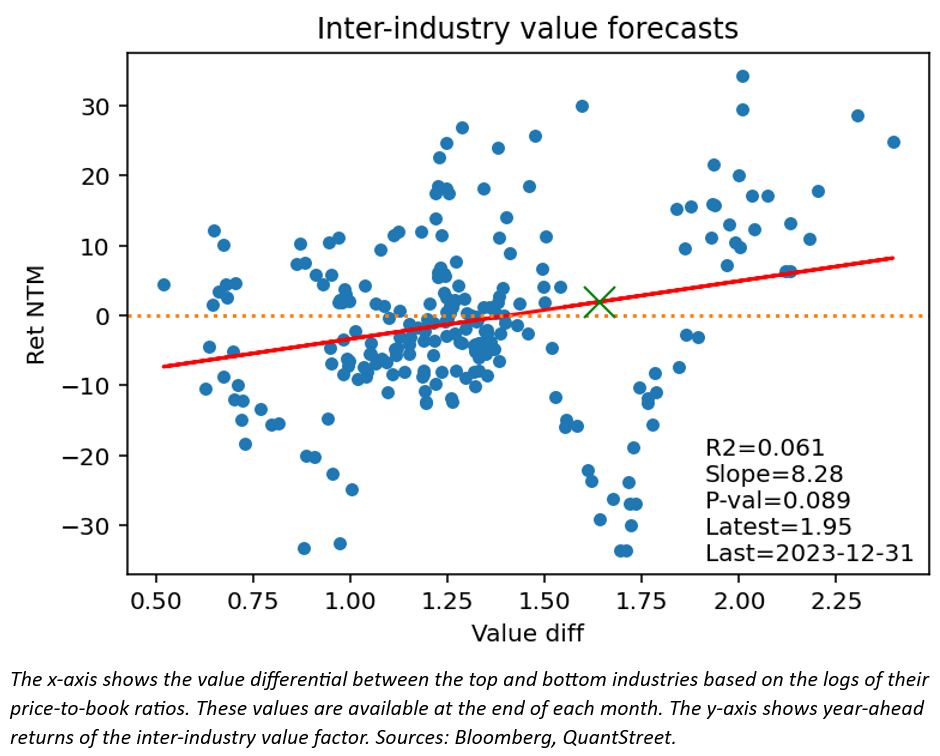

The next chart shows the same analysis, except for inter-industry value, which is a monthly series. The valuation metric is the difference in log price-to-book ratios between the most highly- and most lowly-valued industries in each month. The y-axis shows the next 12-month return from the inter-industry value factor. Here, the explanatory power is a little greater than in the prior figure (and the period of the analysis only goes back to 2003, versus 1960 for the annual value factor) with an R-squared of 6.1%. The slope coefficient is now statistically significant at the 10% level (the p-value is 8.9%) and the most recent forecast for the year-ahead inter-industry value factor return is 1.95% (the green X). But the figure again makes clear that there is a large variation in outcomes at each level of the inter-industry valuation differential, with the most extreme valuation differentials being associated with positive next 12-month inter-industry value factor returns. But inter-industry valuation differentials in the current range have historically been associated with negative next 12-month returns, as the scatter plot shows.

Is there still a value effect?

While the value effect may yet come roaring back, as its proponents claim it will, a simple implementation has performed very poorly since 2007. This is true for the overall value effect and for its inter-industry and intra-industry components. At the inter-industry level, growth and value industries don’t change much over time, and have distinctly different economic and growth profiles. It is implausible that investor inattention is the main culprit for why value industries trade at lower multiples relative to growth ones. The more likely reason for the valuation gap is that (1) value industries grow more slowly (which is true); (2) value industries may have higher expected returns (possible but hard to prove); and (3) investors underreact to the growth prospects of faster growing firms (also hard to prove but related to macro momentum). There is evidence, especially for the inter-industry value factor, that valuation differentials forecast future value factor returns positively. But the current year-ahead, inter-industry value factor forecast is close to zero (1.95%), though the inter-industry valuation differential series bears watching for future extreme values.

Harry Mamaysky is a professor at Columbia Business School and a partner at QuantStreet Capital.

A message from Advisor Perspectives and VettaFi: Advisors: You're Invited to Exchange! Nothing would be a better start to the new year than if you joined us at Exchange, an in-person conference for members of the financial services community in Miami, Florida on February 11-14th. For a limited time, we're offering you a free Exchange ticket!* Register today with code WINTER24 to claim your pass.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits