April showed us just how sensitive markets can be to a small number of powerful forces: energy prices, inflation and geopolitical risk. The conflict in the Middle East dominated headlines, with a ceasefire helping to steady markets even as energy prices remained elevated.

Streamlining the rules is undoubtedly appealing. The new proposal would do this, in part, by allowing the largest banks to use one method to calculate the risk of their assets instead of two, as currently required. That makes sense as far as it goes. Yet other requirements — including leverage ratios and certain capital surcharges — are being loosened or otherwise made more bank-friendly at the same time.

Artificial intelligence might be the most transformative technology ever devised. Exactly how its effects will work through the economy is impossible to say, but serious disruption of one kind or another seems likely. Millions of jobs — in the end, maybe most jobs — could radically change, and many will disappear entirely.

In today’s market, income investors remain firmly focused on one objective: yield. With traditional sources of income still under pressure, demand for high-income ETFs continues to grow — especially those capable of delivering consistent monthly payouts.

Volatility ETFs have specific purposes to fulfill for investors -- so have they done so in a very volatile year?

Core aggregate benchmarks remain the bedrock of many fixed income portfolios but advisors are increasingly looking to income alternatives.

Global risks have tilted against both growth and price stability. The ceasefire in the Middle East has brought a measure of calm to financial markets, but it has not resolved the underlying economic shock. With the Strait of Hormuz effectively shut, supply constraints continue to ripple through energy markets and are increasingly spilling over into downstream sectors.

The stock market would love to see nothing more than the labor market holding up. Time and again, we find monetary policy having a beautiful, lagged effect in the jobless claims series. We are of the view that the cumulative 175 basis points of Fed rate cuts that hit the market in 2024 and 2025 is exactly what the labor market needs in 2026-2027. We will soon find out if manufacturing employment continued to mend in April.

When Jamie Dimon turned to competitive threats in his shareholder letter this year, the chief executive officer of JPMorgan Chase & Co. did something unusual: He named some. Citadel Securities LLC and Revolut Ltd. were two of the firms Dimon picked out.

Where should advisors and investors be looking to find the best opportunities in fixed income? Given the current macroeconomic picture, now is certainly a good time to consider shifting one’s fixed-income portfolio.

International deep value stocks are a high-conviction, active position across all GMO Asset Allocation portfolios. We define the deep value group of securities as the cheapest 20% of the market, a broad opportunity set that allows us to construct portfolios that are cheaper than traditional value indexes but still high in quality.

The AI hyperscalers are lumped together for obvious reasons, but after the four largest reported their earnings on Wednesday night, it became abundantly clear that one of these big-spending giants is not like the others.

The European Union (EU), pursuing ambitious decarbonization goals, is significantly recalibrating its emissions compliance regime with the Carbon Border Adjustment Mechanism (CBAM). This new border tax intends to promote fair competition amid varying emissions rules and costs. Our research suggests it could also offer insight into profitability as the rising costs to meet carbon limits weigh on corporate financial health, creating winners and losers.

As widely expected amid rising oil, rates will remain 3.5% to 3.75%. However, four policymakers dissented. And Fed Chair Powell will stay as governor after his chairmanship ends.

The rapid institutionalization of the $3 trillion private credit market has left many financial advisors racing to catch up. While the asset class was once a walled garden for pension funds, the mainstreaming of private debt requires a new level of diligence and education. The shift toward transparency is finally allowing advisors to look under the hood of these complex structures.

Lance Humphrey, head of portfolio management at Victory Capital, and Dom Rizzo, portfolio manager at T. Rowe Price, joined Nate Geraci on this week’s ETF Prime to discuss quality investing and active technology strategies. Victory Capital now ranks as a top 30 ETF issuer with 23 ETFs and over $21 billion in assets, having attracted $1.7 billion in inflows year-to-date.

Treasury Inflation-Protected Securities, or TIPS, can help buffer a portfolio against inflation. However, it's important to understand their unique characteristics and complex nature.

For much of 2025, the U.S. dollar looked vulnerable: expensive, less supported by the exceptionalism narrative and heading toward a weaker regime. Then the war in the Middle East changed the picture. Energy prices rose, risk sentiment shifted and the dollar reclaimed its safe-haven role.

Reaching age milestones triggers critical financial and tax-planning actions. This guide explores how specific ages impact decisions regarding Medicare, Social Security, charitable giving and retirement withdrawals, helping you navigate these milestones to optimize your long-term wealth strategy.

In a choppy year for tech investors, one trade has stood out as a success: buy chip stocks, sell software shares. And the divide between winners and losers is getting bigger as 2026 moves along.

Now and then, advisors need to get a sense of how Americans of all ages approach retirement planning. Back in March, Fidelity Investments released its 2026 State of Retirement Planning Study. The report took a deep dive into how different age groups of Americans are viewing retirement preparations.

For the third consecutive policy gathering, the Federal Open Market Committee (FOMC) decided to remain ‘on hold,’ keeping the fed funds trading range at 3.50%–3.75%. This result was largely expected by the markets. Unfortunately for the Fed, the policymakers are in a challenging position of juggling incoming economic and inflation data as well as the uncertainties emanating from the Middle East war.

The U.S. stock market hit a record high on January 27, 2026, as investors prepared for additional Fed rate cuts, fiscal stimulus, and fading inflation.

Hyperliquid, the decentralized crypto exchange that has emerged as one of the most active trading venues in digital assets, is proposing to add prediction markets to its platform — a direct challenge to Kalshi and Polymarket as the fast-growing sector draws new competitors.

Hedge fund manager turned NBA owner Gabe Plotkin, who shut his firm after a bruising showdown with meme-stock traders, is planning to convert some of his own assets into an ETF using a tactic that’s helped a slew of wealthy investors defer tax.

The Department of Justice drops probe into Fed Chair Jerome Powell, Kevin Warsh's confirmation moves forward, and Department of Homeland Security funding is back in the spotlight.

It’s a stressful investing landscape right now and investors are feeling it. Volatility, driven by a chaotic geopolitical landscape, has defined much of the market narrative this year — perhaps just second to everything AI. Although markets have marched steadily upward, a growing number of investors are making more defensive moves to adapt. In fact, recent data from VettaFi suggests downside protection ETFs are gaining significant traction.

Active ETFs are punching well above their weight in 2026. Despite representing just 12% of total ETF assets, actively managed funds have captured 40% of year-to-date flows, Todd Mathias, head of North America ETF product strategy at Franklin Templeton, told attendees at an April 27 roundtable discussion at the firm’s Manhattan office.

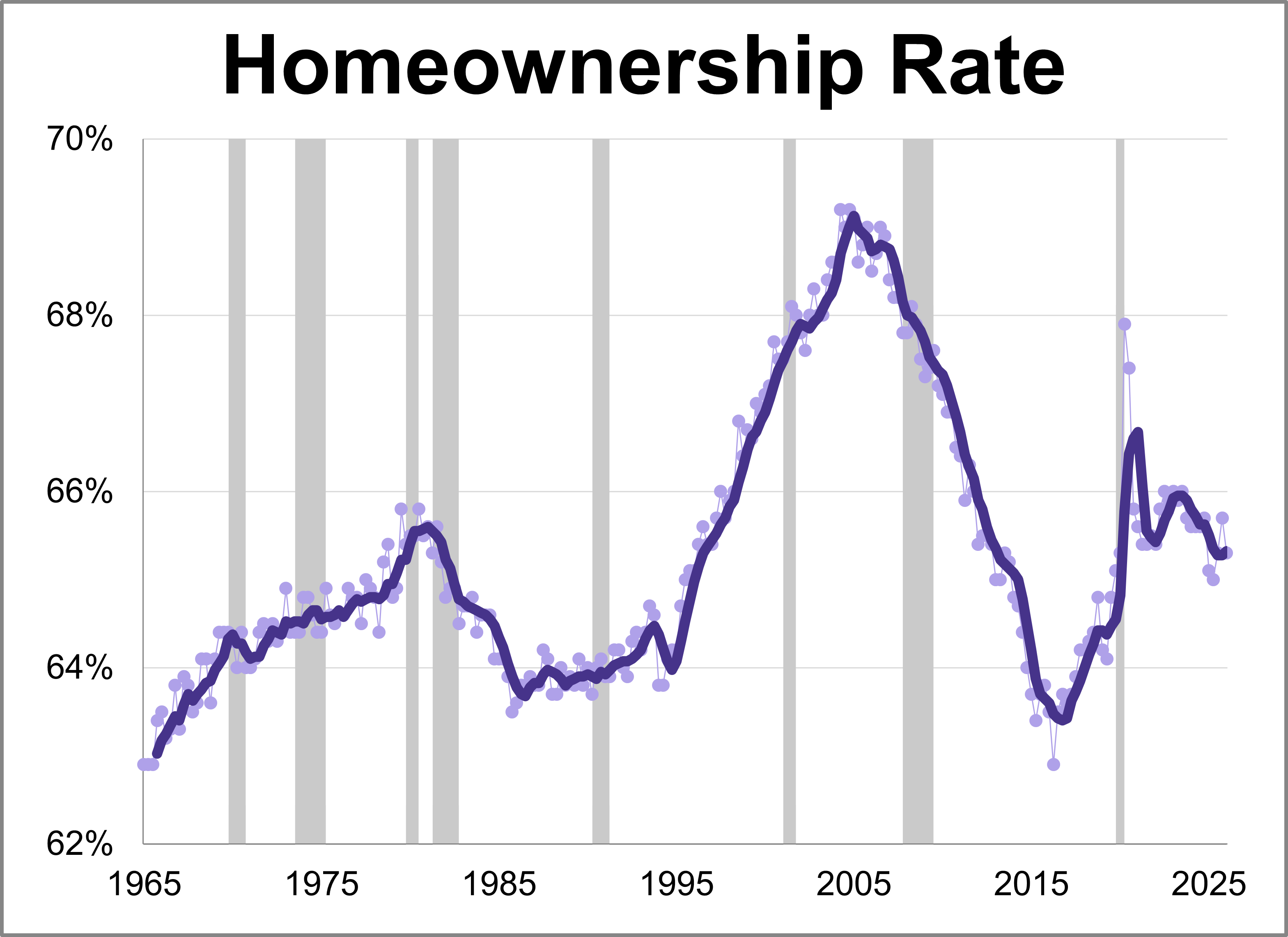

The Census Bureau released its latest quarterly report for Q1 2026 showing the latest homeownership rate is at 65.3%.

Technology megacaps are pushing benchmark indexes to new records while the rest of the market is lagging behind. Traders can be forgiven for feeling like they’ve seen this movie before.

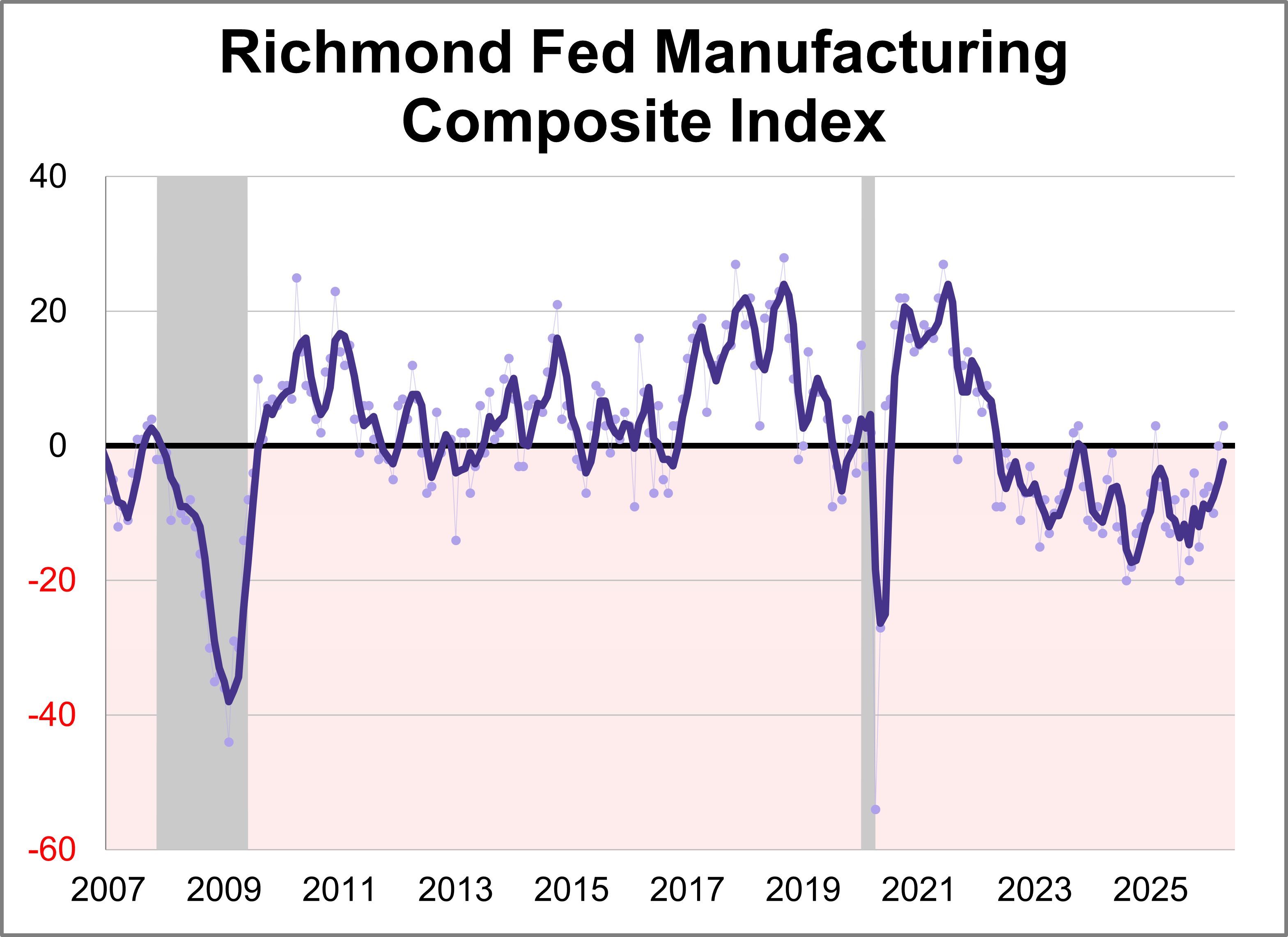

Fifth district manufacturing activity increased in April according to the most recent survey from the Federal Reserve Bank of Richmond. The composite manufacturing index rose three points points to 3, marking the highest level for the index in 20 months. This month's reading was above the forecast of 2.

European stocks started the year much stronger than their US peers but the tantalizing prospect of the euro area clawing back some of its persistent gap in earnings growth, and the higher company valuations that come with it, looks to have slipped through its grasp again.

The chip industry seems to be the only game in town lately. The Philadelphia Semiconductor Index, known as the SOX, has risen 48% this year. Bourses in Taiwan, South Korea and Japan are riding the wave and hitting record highs, brushing away potential energy shocks from the military conflict over Iran.

The “American Industrial Renaissance” is an investment theme investors and allocators alike have probably been pitched several times, or at the very least heard about. Supply chains for manufactured goods have evolved to become more complex, while U.S. manufacturing employment as a share of total employment has steadily declined, leaving policy makers to grapple with the ramifications of a shrinking manufacturing base.

Markets continue to ebb and flow with every headline out of Iran and the Strait of Hormuz, but the most important message from the markets is resilience. Earnings season is off to a very strong start, with roughly a 75% beat rate, and the AI investment cycle continues to provide a powerful tailwind for equities.

Many people seem surprised by the US stock market’s resilience during the Iran war. I’m not one of them, and I don’t see the war becoming a significant threat to the market, even if it drags on.

It’s the big story so far in 2026. Alongside AI, geopolitical market volatility is creating dislocations for investors to target. While some are more immediate and some are longer term, the ETF wrapper offers strategies that can attack all kinds of sectors. In corporate bonds, for example, growing volatility could create opportunities.

Despite the turbulence, the global LCC market remains an enormous force. Four of the world’s 10 largest airlines—Ryanair, Southwest, IndiGo and easyJet—operate on a low-cost model. The broader budget travel market is projected to exceed $315 billion by 2028, according to Statista.

The midstream energy arena, which includes master limited partnerships (MLPs), has long lured income-hungry investors. A new ETF amplifies that proposition. The MLP & Energy Infrastructure High Income ETF (MLPI) debuted last December. It’s generating buzz, helped by the White House’s rhetoric on bolstering American energy independence, which is viewed as a potential boon for MLPs.

It’s tax season, and we’ve been reading a lot about taxes — and strategies for mitigating them. In this note, we’ll take a close look at one such strategy, known as leveraged long/short direct index tax-loss harvesting (LSDI), and explain how investors being pitched the strategy can assess whether it’s right for them.

If the first quarter of 2026 taught us anything, it's that markets are dynamic and that the factors shaping them extend well beyond corporate fundamentals. The road ahead presents a wider range of outcomes than investors have faced in some time. The outlook remains fluid and highly dependent on how several key factors evolve.

On Monday, the index returned to record highs, eclipsing the previous peak hit before the war started in Iran. Yet, when compared with the US market, emerging-market shares screen as cheaper than at the start of the war, reinforcing the case for investors to add exposure.

Like many of you, I am inundated with information. Most of it is not useful or repetitive. Today, were going to do something different. Rather than one theme, let’s look at various bits of data that I found interesting this week.

Maharrey identified October 2025 as the turning point when a full-scale silver squeeze took hold. Tight inventories collided with logistical disruptions and surging physical demand.

Last week’s economic data was defined by conflicting signals from the consumer. While retail figures suggest resilience, sentiment levels have plummeted to record lows. Meanwhile, the S&P 500 continued its historic rally as markets prepare for the upcoming Fed decision.

After positive earnings releases from peer semiconductors like Texas Instruments, Taiwan Semiconductor, and ASML, it was Intel’s turn to further support the notion that the semiconductor industry is doing just fine amid the recent volatility.

The primary contagion risk is sector concentration. Software and tech-enabled services represent roughly 15-20% of direct lending portfolios. A meaningful portion of these loans also resides in the Broadly Syndicated Loan (BSL) market – the bedrock of CLO ETFs – leading to a software weighting of 12–18% in typical CLO collateral pools.

Clients may love the relative safety of cash, but many advisors know those assets could do more. A multisector bond approach for example, offers plenty of rewards for those willing to dive in. The right ETF can give tax efficient exposure to the space, providing both yield and total return.

Even before the first active dual share class fund from Dimensional launched, active mutual funds and ETFs were already roommates rather than existing in separate silos. Ben Johnson, head of client solutions at Morningstar, revealed in a LinkedIn post that active managers are increasingly using ETFs as essential tools for building portfolios.

Elon Musk’s SpaceX is no stranger to the stratosphere, and neither is its coming initial public offering.