Adjusted earnings forecasts tend to overshadow reported earnings and add uncertainty to corporate outlooks.

Despite softening demand, US home prices remain elevated. The culprits are high interest rates, limited supply and owners' reluctance to take on new mortgages.

Investors should take a closer look at companies that help create a more energy-efficient ecosystem for AI.

Progress toward a sustainable world would be hamstrung without the backing of global banks and their sponsorship of green and sustainable bonds.

AI development is racing ahead. A thoughtful framework to making decisions and leveraging tools can help investors stay on course.

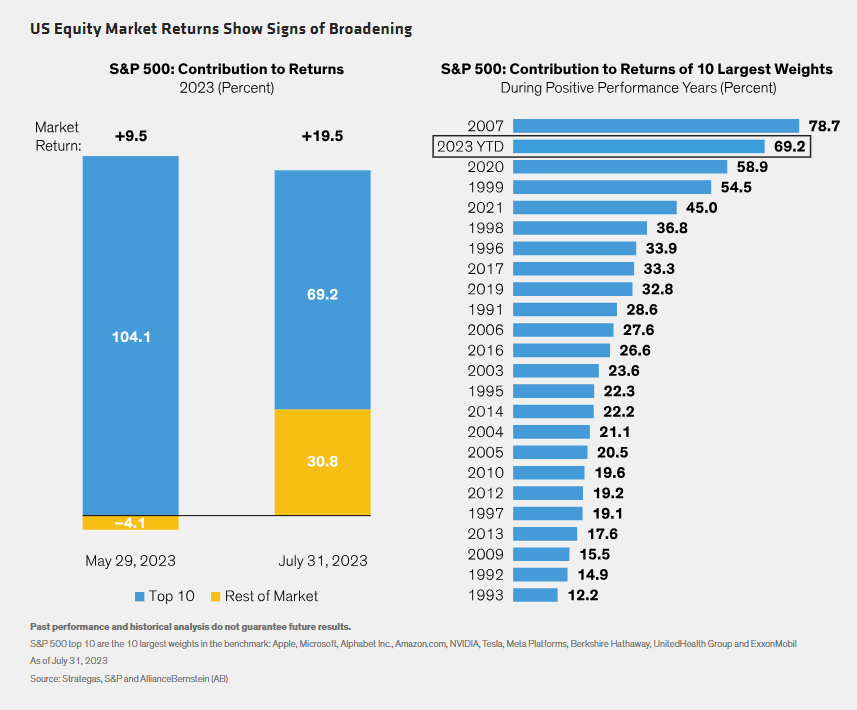

Ten stocks have dominated US equity market gains for most of this year. But the rest of the market may be waking up. That’s good news for active managers who seek to tap diversified sources of long-term returns that can withstand challenging macroeconomic conditions.

With the second half of 2023 underway, how are the macro and market landscapes unfolding?

Recession? Soft Landing? Getting a read on where the US economy is headed hasn’t been easy.

Flagging office occupancy rates have municipal bond investors concerned. But US cities have more than one card to play in the revenue game.

Do high-yield bonds still make sense for income investors at this stage of the credit cycle? We think so.

Investors are taking fright at commercial real estate risks in Sweden. But we think the situation is less threatening than feared.

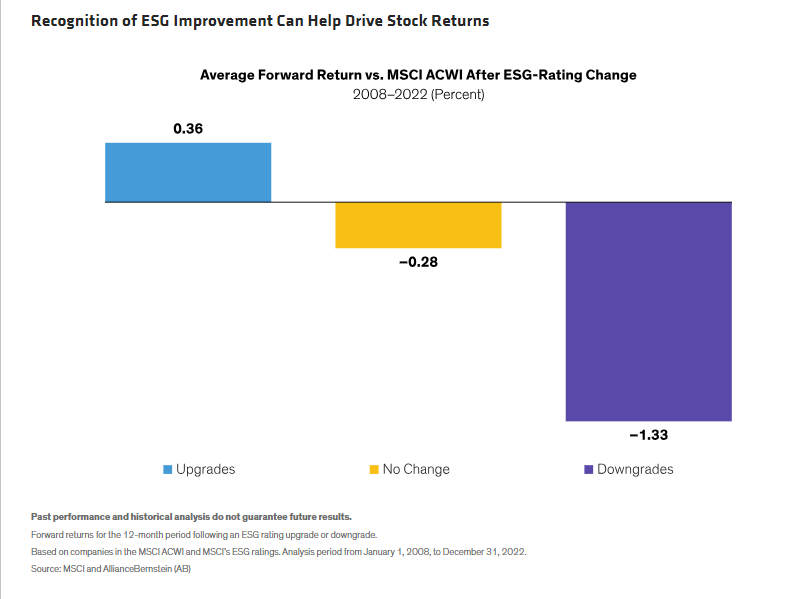

Companies that are on course to overcome ESG controversies deserve closer attention from investors.

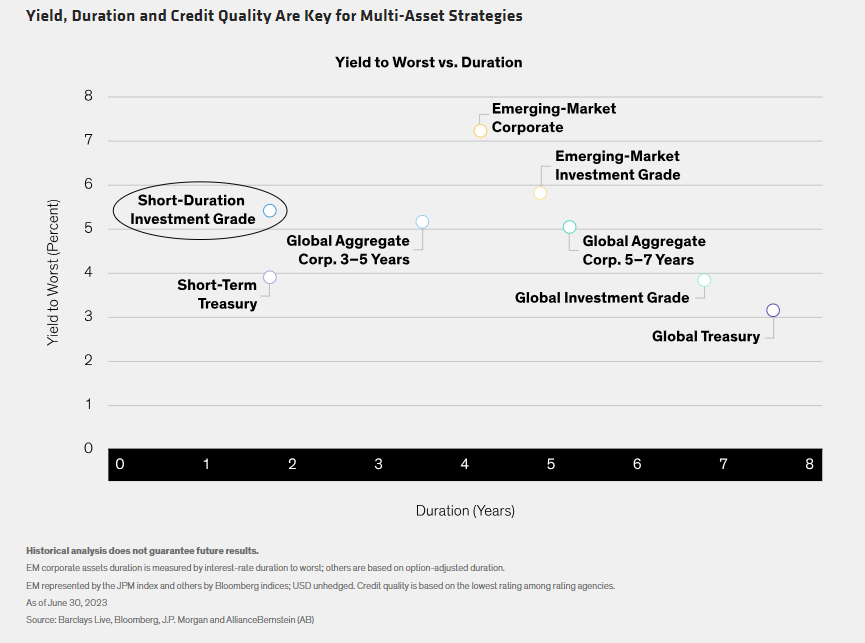

In any environment, multi-asset investors should prudently balance risks across equity, corporate credit and government bonds. But near-term tactical shifts can help take advantage of ever-evolving market conditions in the pursuit of long-term returns.

The more painful the situation, the more motivated we are to act. Here, we share an example of how an advisor can build a relationship with a client to become a trusted advisor and how that trust helps inspire referrals.

New public policies reflect growing urgency to address climate risk, which equity investors should emphasize, too.

Markets posted a strong first quarter, though it was a rollercoaster ride. The path forward will likely stay turbulent, with bank turmoil likely tightening credit conditions and the Fed still wrestling with inflation.

Over the past 18 months, high inflation drove rapid monetary policy tightening, which weighed heavily on consumer spending power and corporate margins. As inflationary pressures now abate, we see eventual improvement in both real incomes and profits, which should enhance prospects for multi-asset investors.

When markets are rising, investors don’t always prepare for turbulence. Yet we think the best time to build a defensive plan for an equity allocation is before volatility strikes.

Solid fundamentals, decent valuations, and attractive income potential make a case for continued exposure to corporate credit even in an uncertain economic environment.

Biodiversity is taking on increasing importance as a consumer concern, but it isn’t always top of mind for investors. We think that could soon change. Beyond the obvious environmental benefits, there’s an economic case to be made for protecting biodiversity.

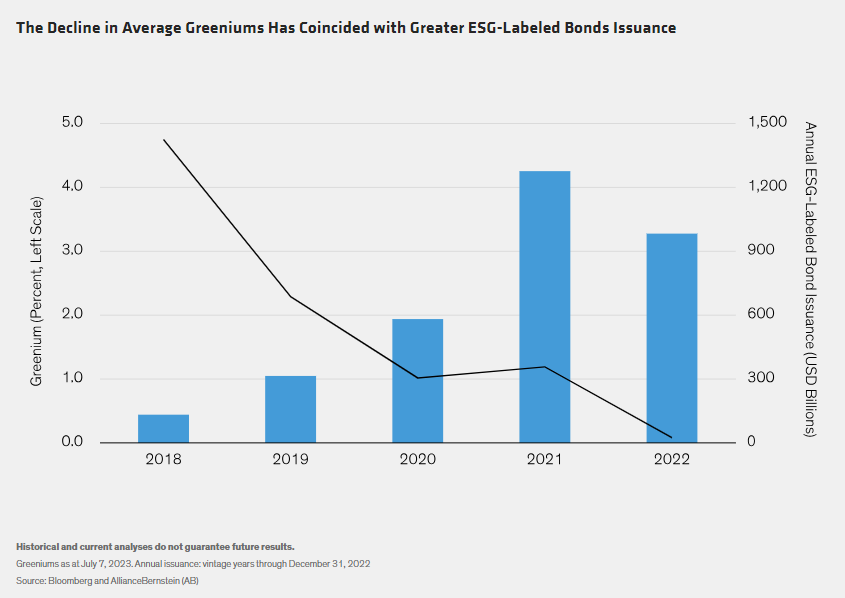

Investors in ESG-labeled bonds expect well-structured issues with strong green or social credentials to command higher prices than the same issuer’s conventional bonds.

Financial companies that help address some of the world’s most pressing socioeconomic challenges deserve attention from sustainability-focused investors.

Even benchmark-makers are starting to address the supersized influence of heavyweight stocks. Nasdaq’s plan to reconfigure the weights of its constituents should prompt investors to think about the broader concentration risks in US equity markets, particularly in passive portfolios.

An improved income outlook for multi-asset investors, including higher yields, sharply contrasts with cloudy conditions at 2023’s start.

With the highest yields in years, the muni bond market looks increasingly attractive.

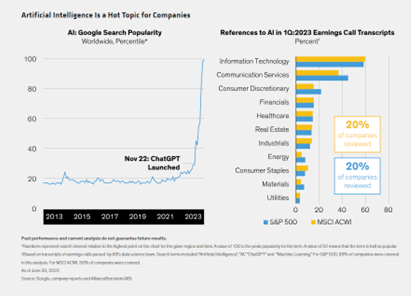

Artificial intelligence has quickly become a hot topic around dinner tables and in corporate boardrooms. But delivering business benefits from AI will take time. Investors should proceed with caution.

Global equity markets have had a very strong first half of the year, but it’s a pretty unusual time because, on the one hand, equities are contending with a pretty difficult macro backdrop.

We’re tactically cautious on developed-market equities with a broadly risk-off stance, but we have a relative preference for emerging-market (EM) stocks over a 6- to 12-month horizon.

Steadfast global resilience to recession highlighted the quarter, although the outlook hasn’t necessarily improved. But with labor markets tight and wages keeping pace with inflation, consumers are navigating the economy’s rough patches. Still, we expect growth to slow in time.

For over a decade, emerging markets (EMs) have been full of promise—and disappointment. Year after year, investors have waited for the powerful growth trends of the past that drove developing markets from Mexico to Malaysia to reassert themselves.

Surf’s up! Elevated yields and negative correlations are good news for bond investors. We share strategies for making the most of today’s opportunities.

Excitement over AI has driven equities this year. Yet investors should maintain a disciplined, long-term focus amid uncertain market conditions.

Central banks in the developed world have raised interest rates higher and faster than at any time in recent memory. But until labor markets start to slow, policymakers are unlikely to take their feet off the brakes.

Lower bond-market liquidity and insurance investors’ unique needs raise the stakes for liquidity management in what’s likely to be a volatile environment.

After the disruptions of the past few years, many of us are looking for a return to normal. For investors in emerging-market bonds, normal would mean a world in which global inflation is in check, interest rates are no longer rising, China is healthy, and traditional asset correlations resume.

Striking the right balance between interest rate and credit risk can be a good idea in the late stages of a credit cycle. We think it’s a particularly good idea in this credit cycle.

Naturally, the recent banking crises in the US and Europe raise concerns about EM exposure to financial sector risks too. We’ve found that the EM financial sector overall looks strong and resilient—but that several individual EM countries’ banks could be vulnerable.

Recruiting talent is a basic ingredient for business success. Companies that are more inclusive in their recruiting will discover better-qualified employees, which can bolster competitive advantages and help deliver better outcomes for investors.

Corporate bonds that fund environmental, social and governance (ESG) initiatives continue to capture investor hearts and minds. But ESG-labeled bonds come in different stripes, so investors need to discern among the good, the bad and the occasional ugly ones merely posing as ESG bonds.

Healthcare companies are beginning to explore how artificial intelligence (AI) might unlock efficiencies for patients and medical systems. But to transform science fiction into reality, AI applications in the sector must prove that they can improve business profitability to deliver returns for investors.

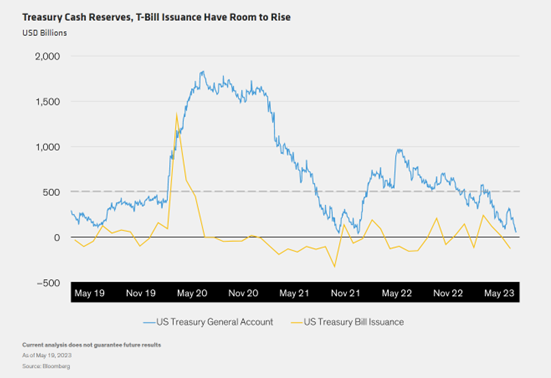

According to the ICI, assets in money markets have ballooned to $5.3 trillion—the equivalent of the world’s 5th largest economy. And with so much cash sitting on the sidelines, a fundamental question persists. Are investors being compensated to wait? Find out why sitting in cash could be a risky proposition as inflation and economic growth show signs of slowing.

Don’t miss an in-depth conversation with fixed income experts from VettaFi and AllianceBernstein, who will share insights on how to position portfolios amid a challenging market environment.

Topics will include:

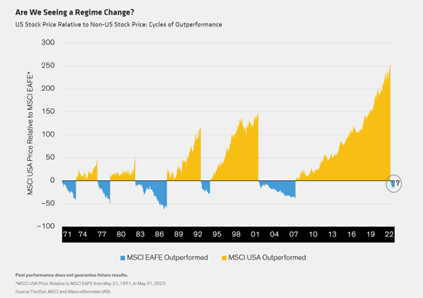

When it comes to their equity portfolios, US investors have historically exhibited a high degree of home-country bias. But in today’s fast-changing global market landscape, they may find that there are good reasons to rethink regional allocations to stocks.

If price stability is the legal mandate of the Bank of Japan (BOJ), and the central bank’s official target for price stability is 2%, as measured by the Consumer Price Index (CPI),* then why are fluctuations in prices the norm for Japan?

The standoff between the White House and Congress over raising the US debt ceiling has been the talk of the town for months. Now that the government has reached an agreement, savvy investors will be on the hunt for opportunities—and we think there will be some attractive ones.

The financial markets are giving off mixed signals of late, and credit investors may wonder whether to be downbeat or optimistic.

Here’s what we learned in earnings season about how companies are coping with a particularly tricky set of macroeconomic conditions.

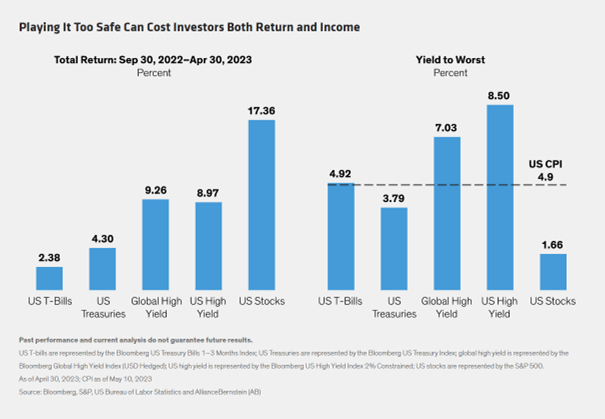

Parking your fixed-income assets in cash may seem like a safe choice in today’s volatile investing environment, but it’s actually a risky proposition. Here are three reasons why sitting on the sidelines can be a dangerous game.

The Federal Reserve’s latest 0.25% interest-rate hike has likely capped one of its most aggressive policy-tightening cycles in 40 years. And the cumulative 5% policy rate increase in just over a year is now starting to have an effect on rate-sensitive sectors and inflation.

Muni investors have more reasons for optimism than concern as California tackles a projected $31.5 billion budget deficit.

As the US economy begins to feel the weight of the Federal Reserve’s rate hikes, investors have grown leery of US high-yield corporate bonds. On the surface, that makes sense. Historically, credit conditions soured when growth slowed.