Flagging office occupancy rates have municipal bond investors concerned. But US cities have more than one card to play in the revenue game.

From the Bay Area to Boston, shrinking office footprints have been generating gloomy headlines. With talk of downtown death spirals, some municipal bond investors fear that declining office occupancy—a side effect of increased workplace flexibility—could deplete large cities’ coffers. But while office vacancies remain a concern, most US cities have mechanisms to protect their finances—and those of municipal bondholders.

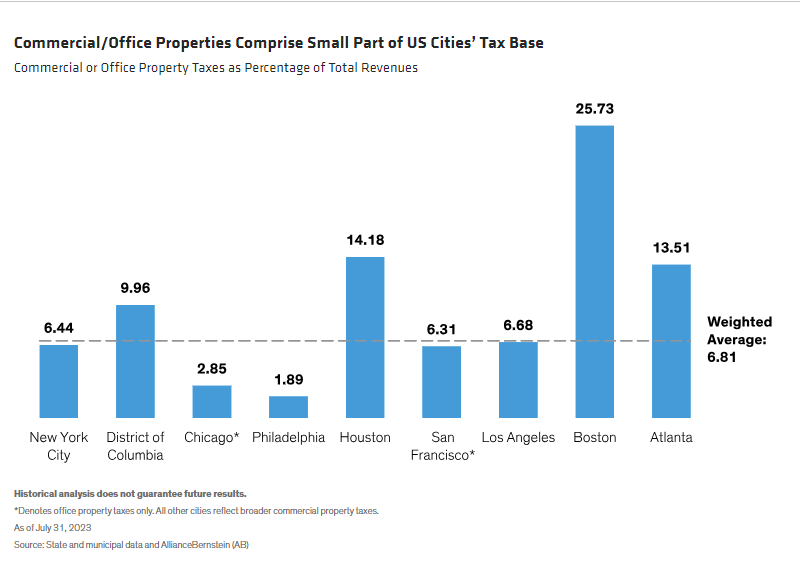

Cities Have a Wide Range of Funding Sources

First off, we need to address a misconception: US cities aren’t nearly as dependent on commercial and office taxes as many believe. It’s true that property taxes are typically the largest source of tax revenue for large cities, but they account for just 30% of total revenue, on average, according to the Urban Institute—with the office contributing just a portion of that. In fact, of the largest US cities by debt outstanding, commercial or office property taxes account for just 6.8% of total revenues, on average (Display).

Cities have other important sources of revenue they can tap. These include user charges, such as sewerage and parking fees, income taxes, sales and use taxes, and intergovernmental transfers. The ability to draw from a wide range of funding means that even a 50% drop in office property tax revenues would represent a 3.4% decrease, on average, in total revenues—not a debilitating challenge to cities, in our view.

Untethering Taxes from Property Values

Even if office properties were to experience steep valuation declines, cities have mechanisms to blunt or even nullify the effect on property taxes, cushioning the budgetary impact of declining real estate values.

For example, Chicago sets its property tax levies independently of real estate value. The process is similar for most cities in New York State as well, where annual property-tax increases are limited to the lesser of 2% or the rate of inflation. This effectively untethers property taxes from real estate values—though it doesn’t limit property tax rates or assessment values.

And while New York City’s property taxes are more closely tied to real estate values, changes in the value of the city’s tax base are phased in over five years. This limits downside risk in any given year and gives the city time to adjust to changing values.

Thanks to similar mechanisms across the US, city property-tax revenue is somewhat insulated from broader real estate shocks. A 2008 study by the Federal Reserve found that property taxes have a beta of 0.4, meaning that property taxes rise or fall by 40% as much as the broader real estate market. Moreover, this relationship tends to have a three-year lag, providing time for cities to adjust.

A Closer Look at Office Property Values

Like many investors, we’re concerned about the value of office properties in the new world of hybrid work and work-from-home. Dwindling workforces can sap the vitality of downtowns and have a multiplier effect on businesses that depend on foot traffic. Higher interest rates also make financing office properties more challenging, putting added pressure on valuations.

But there’s more to the picture than meets the eye.

Some market observers estimate that office property values have fallen in the neighborhood of 30% since March 2022. These estimates are derived from appraisal-based data—not actual transactions, which tell a different story. While declines in appraisal-based indices can look dramatic, transaction-based indices show that office property values have fallen only 8% over the past 12 months ended June 30, 2023, on very low sales volume. We’re not saying that significant declines won’t happen, but the illiquid nature of commercial real estate lengthens the duration over which potential declines are realized—to cities’ benefit.

Cities Have the Flexibility to Address Market Shifts

The trump card for large municipal bond issuers is that, as government entities, they can and do change the rules to help protect themselves against economic shifts. For example, in response to the rise in digital commerce, many states enacted laws allowing them to collect sales taxes from online retailers with no physical presence in the state. In a similar vein, we expect cities to reallocate their taxing authority to capture shifts in economic activity away from offices and toward more active uses. As long as cities attract people, governments will find a way to tax them.

That should provide a measure of confidence for municipal bondholders. According to Moody’s, US cities’ median cash balance as a percentage of operating revenues increased to 71% in 2021 from 34% in 2013, helping to buffer against a weak office market.

We believe the outlook for American downtowns isn’t nearly as grim as some maintain. In our view, declining occupancy rates represent a shift in how US cities allocate resources, rather than a harbinger of secular decline. Fewer employees going to the office isn’t hurting the desirability of cities, which have seen a demographic recovery since the pandemic.

In contrast to an era when deindustrialization spurred a decades-long exodus, US cities have the tools to weather generational changes in how Americans live and work—good news for both cities and the municipal bond investors who place their trust in them.

The views expressed herein do not constitute research, investment advice, or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: Just as artificial intelligence (AI) is helping advisors create videos, write blogs, construct portfolios and coach clients, companies throughout the world are using it to deliver more value to their clients. Learn about the future of AI and the investment opportunities it is creating at our next symposium, on August 30 at 11 am ET. Click here to register.

© AllianceBernstein

Read more commentaries by AllianceBernstein